What will Warsh say about June CPI?

Key data to move markets today

EU: A speech by ECB President Christine Lagarde

UK: A speech by BoE Governor Andrew Bailey

USA: ADP Employment Change 4-week average, CPI, Core CPI, Fed Chair Kevin Warsh testifies on the Semiannual Monetary Policy Report before the US House Financial Services Committee and speeches by Fed Vice Chair for Supervision Michelle Bowman, Fed Governors Michael Barr and Lisa Cook and Chicago Fed President Austan Goolsbee

CHINA: Industrial Production, GDP and Retail Sales

Global Macro Updates

June Core CPI preview. The June core CPI report, due today at 8:30 EDT, is expected to show a 0.26% m/o/m increase, up from the 0.20% gain recorded in May. On a y/o/y basis, core CPI is expected to remain unchanged at 2.9%. Headline CPI is expected to decline -0.15% m/o/m after rising 0.5% in May. The annual headline rate is forecast to ease to 3.8% from May’s 4.2%.

Within core services, previews point to more moderate rent and owners’ equivalent rent inflation. However, BofA noted that the disinflationary impulse from housing may be fading as price increases have normalised. At the same time, a potential rebound in motor vehicle insurance, which fell 1.7% m/o/m in May, along with World Cup-related effects on hotels, airfares and car rentals, could present upside risks.

In core goods, previews suggest a more limited tariff impact following the IEEPA decision. Autos could be softer, with Goldman Sachs forecasting declines in both new and used vehicles. JPMorgan noted that computer software and accessories, which have recently contributed significant upward pressure, may cool as retail memory prices were flat m/o/m.

The Street remains divided on the inflation outlook and the Fed’s reaction. Citi said slower shelter inflation and limited passthrough from energy costs could lead markets to price out Fed rate hikes entirely. By contrast, BofA argued that still-firm core CPI readings, driven primarily by services, should strengthen the case for near-term rate hikes.

Fed Chair Warsh testimony on Capitol Hill preview. Fed Chair Warsh is scheduled for two days of testimony this week, beginning with an appearance before the House Financial Services Committee today at 10:00 EDT, followed by testimony before the Senate Banking Committee tomorrow at 10:00 EDT.

The testimony follows Friday’s release of the Fed’s latest Monetary Policy Report, which was broadly uneventful. The report characterised the labour market as stable, while noting that labour supply growth remains extremely subdued. It also said upward market assessments of the policy path reflect concerns over the Middle East and increased confidence in the labour market.

Previews suggest Warsh is unlikely to offer substantial new guidance. This is consistent with his preference to avoid communicating Fed policy outside formal meetings or providing anything resembling forward guidance.

BofA argued that Warsh’s remarks may align more closely with his comments in Sintra than with his June FOMC press conference, which could be interpreted as dovish. In Sintra, Warsh said inflation risks had fallen in the weeks since the meeting, declined to comment on whether the Fed would raise rates at its next meeting, emphasised the importance of adjusting to changing economic conditions and highlighted potential AI-related supply-side implications for policy.

Some press previews also noted that Warsh has an opportunity to guide consensus within a divided Fed when he testifies this week, particularly given that the June CPI release is scheduled shortly before the hearing and is just two weeks ahead of the July FOMC decision. However, his testimony follows hawkish-leaning remarks from Fed Governor Waller on Monday, who said the FOMC will need to consider near-term tightening if CPI remains elevated.

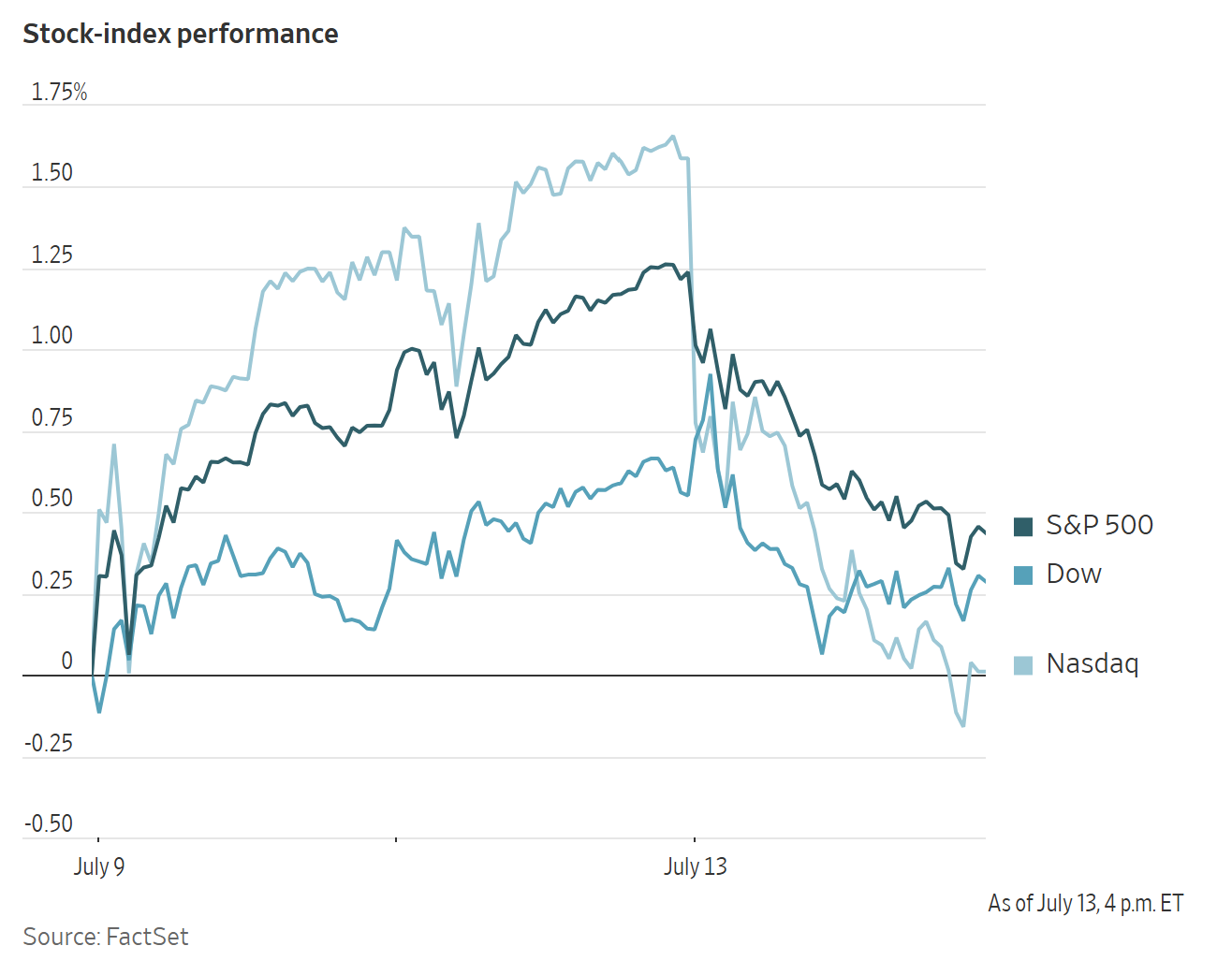

US Stock Indices

Dow Jones Industrial Average -0.26%

Nasdaq 100 -1.88%

S&P 500 -0.79%, with 5 of the 11 sectors of the S&P 500 down

On Monday, the Nasdaq Composite retreated by -1.55%, the Dow industrials declined -0.26%, or 138.37 points, while the S&P 500 lost -0.79%.

In corporate news, Meta Platforms announced plans to invest an additional $40 billion in its large-scale data centre campus in Louisiana, bringing total expected spending on the site to more than $250 billion.

Intel plans to invest €5 billion to expand its manufacturing facility in Ireland, as the chipmaker seeks to strengthen its production capabilities and regain competitiveness amid rising demand linked to AI.

A coalition of 12 states led by California filed a lawsuit seeking to block Paramount Skydance’s $81 billion acquisition of Warner Bros. Discovery. The complaint argues that the transaction would be anticompetitive, as the combined company would control nearly one-third of theatrical films and basic cable. If the deal is delayed beyond 30 September, Paramount would be required to pay Warner shareholders a quarterly ticking fee of approximately $650 million.

European Stock Indices

CAC 40 +0.31%

DAX +0.19%

FTSE 100 +0.01%

Commodities

Gold spot -2.90% to $4,000.65 an ounce

Silver spot -3.68% to $57.64 an ounce

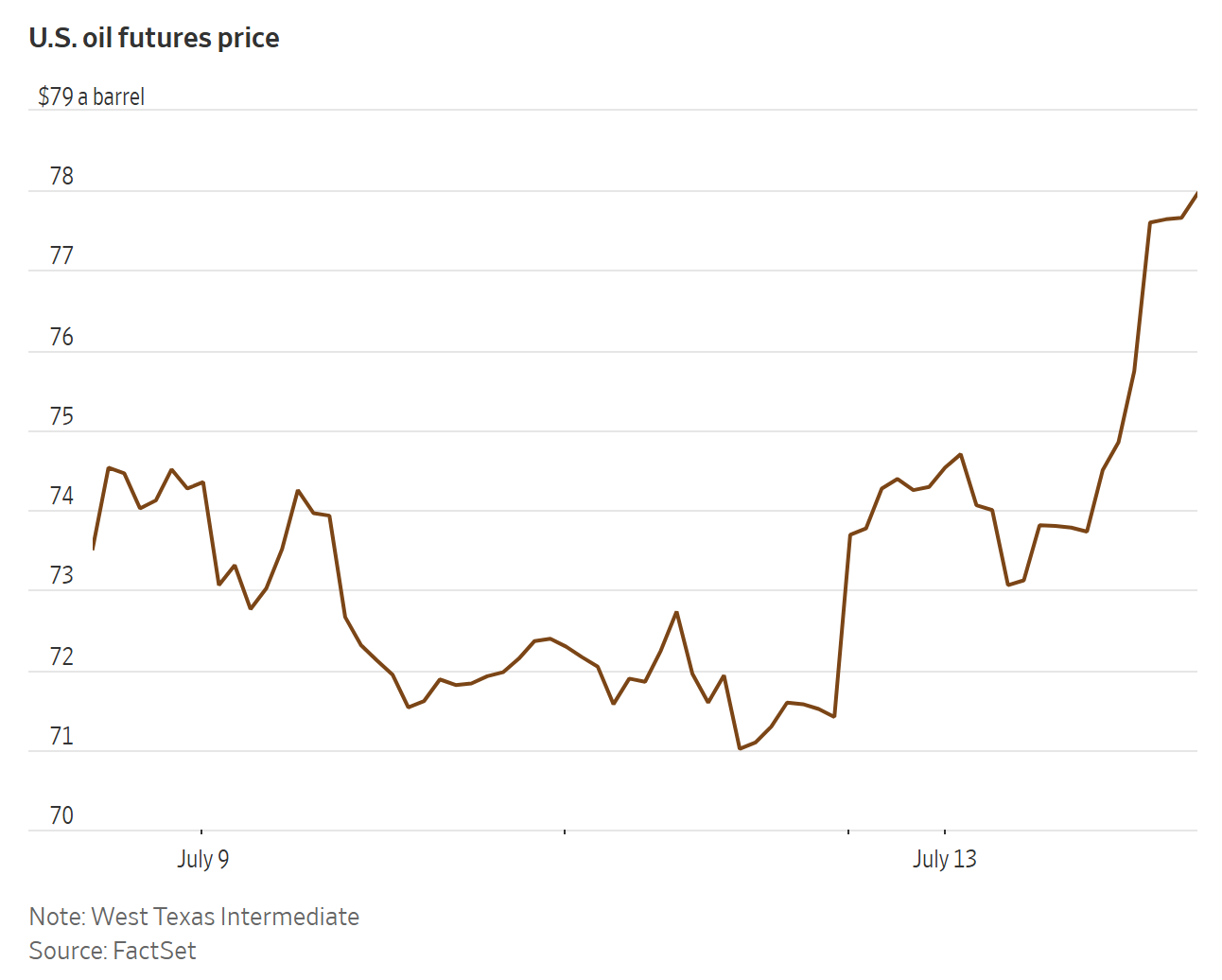

West Texas Intermediate +9.08% to $78.00 a barrel

Brent crude +9.52% to $83.21 a barrel

Gold prices declined again on Monday due to a stronger dollar, with spot gold falling -2.90% to $4,000.65 per ounce after touching its lowest level since 1 July earlier in the day.

Spot silver also weakened, falling -3.68% to $57.64 per ounce.

Oil prices settled at a one-month high on Monday. They were supported by renewed concerns over energy shipments through the Strait of Hormuz after reports that a US naval blockade, due to begin on Tuesday, would cover Iran’s entire coastline, ports and oil terminals, as well as all vessels regardless of flag.

Brent crude futures settled up $7.23, or +9.52%, at $83.21 per barrel. This was the largest single-day dollar gain since 2 April and the highest settlement price since 12 June. US WTI crude settled up $6.49, or +9.08%, at $78.00 per barrel. This was the strongest daily gain since 29 April and its highest settlement price since 15 June.

The US President announced on Sunday that the US was reinstating the Iranian blockade and would impose a fee to cover the costs of providing safe transit through the Strait, equivalent to a +20% rate on all shipped cargo. The announcement followed multiple Iranian attacks over the weekend against several Gulf countries and vessels in the Strait of Hormuz.

The US responded with strikes against several Iranian positions. After the oil market closed, the US President notified Congress that limited military action had resumed in Iran.

Shortly before 14:00 EDT yesterday, the US-led Joint Maritime Information Center said a naval blockade of all Iranian ports and coastal areas would be enforced from 20:00 GMT on 14 July and would apply to all vessel traffic regardless of flag.

Senior Houthi officials told local media that the Bab el-Mandeb strait would also be closed, similar to the Strait of Hormuz, and that the group would target Saudi Arabia’s vital infrastructure. Reports shortly after 12:00 EDT indicated that missiles launched from Yemen toward Saudi Arabia were intercepted, following Saudi strikes on sites at Sanaa airport.

Tanker data continued to indicate a slowdown in Strait of Hormuz traffic, with only five vessels making the journey on Sunday. MarineTraffic data showed Hormuz traffic down more than 50% w/o/w during the first half of July.

The Abu Dhabi National Oil Company set the August official selling price for its benchmark Murban crude at $80.01 per barrel, down from $101.48 per barrel the previous month.

Ukraine continued attacks on Russian refineries, while there were more than 100 hundred estimated strikes against Russian ships and tankers over the past eight days. Ukraine’s Security Service said it struck an oil depot in Russia’s Stavropol region overnight, as well as three storage tanks at an oil-loading site in the port of Kavkaz in Russia’s southern Krasnodar region.

The Caspian Pipeline Consortium, which accounts for 80% of Kazakhstan’s oil exports, cut supplies by 7% m/o/m from May due to maintenance at Tengiz, the country’s largest oilfield, and lower Russian flows, according to two industry sources.

The OPEC MOMR left 2026/2027 non-DoC production estimates unchanged, slightly lowered its 2026 global demand growth estimate and raised its 2027 demand growth expectations. OPEC production rose 3.051 million bpd m/o/m, including a 1.64 million bpd increase from the UAE, while non-OPEC DoC supply fell by roughly 50,000 bpd on weaker Russian output.

Global refining margins remained near record levels, with the CME 3-2-1 crack spread averaging roughly $61.00 per barrel so far this month and briefly exceeding $64.00 on Monday.

Note: As of 4 pm EDT 13 July 2026

Currencies

EUR -0.26% to $1.1383

GBP -0.47% to $1.3342

Bitcoin -3.07% to $62,021.81

Ethereum -1.84% to $1,760.02

The US dollar strengthened broadly on Monday, with the dollar index up +0.33% at 101.30.

The euro fell -0.26% to $1.1383, while sterling declined -0.47% to $1.3342.

The Japanese yen weakened against the dollar after Reuters reported that Tokyo had no imminent plans to alter the asset allocations of its state pension funds. The dollar rose +0.43% to ¥162.39.

Fixed Income

US 10-year Treasury +5.8 basis points to 4.620%

German 10-year Bund +6.5 basis points to 3.132%

UK 10-year Gilt +9.8 basis points to 4.974%

US Treasury yields rose sharply on Monday.

Yields extended their gains alongside crude prices after the US President said the US was reinstating a naval blockade on Iran.

The US 10-year Treasury yield rose +5.8 bps to 4.620%, its highest level since 21 May. The US 30-year bond yield increased +4.6 bps to 5.107%, also its highest level since 21 May.

The US two-year Treasury yield, which is closely tied to Fed funds rate expectations, jumped +8.0 bps to 4.296%, its highest level since February 2025.

Eurozone government bond yields also rose on Monday.

Germany’s 10-year Bund yield rose +6.5 bps to 3.132%. The two-year Schatz yield, which is more sensitive to ECB deposit rate expectations, increased +8.5 bps to 2.747%, its highest level in a month. Last week, the Schatz recorded its largest weekly rise since early June after climbing +10.9 bps.

Italy’s 10-year BTP yield rose +5.2 bps to 3.865%, while France’s 10-year OAT yield increased +15.4 bps to 3.875%.

Money markets are pricing in 37 bps of ECB tightening by year-end, implying one additional quarter-point rate hike and nearly a 50% probability of a second move, slightly above Friday’s implied probability.

Note: As of 4 pm EDT 13 July 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.