Will the ECB prioritise inflation over growth?

Key data to move markets today

EU: German and French CPIs, German Harmonised Index of Consumer Prices and a speech by ECB Vice President Boris Vujčić

Global Macro Updates

ECB minutes. The ECB’s June minutes showed broad agreement among policymakers that a 25 bps rate increase was warranted after higher inflation pressures materialised following the Iran-related energy shock. However, the discussion also revealed differing views on whether additional tightening would be needed.

Since the June decision, policymakers have continued to debate the issue publicly. Hawkish officials have warned of upside inflation risks and expressed concern that the energy shock could prove more persistent and trigger second-round effects. Dovish officials, meanwhile, have pointed to a fragile growth outlook, unusually high uncertainty and the risk of overtightening. These concerns have also been emphasised by sell-side economists.

The ECB reiterated that incoming data will guide future policy decisions. ECB source reports have suggested a July pause is likely, although this week’s renewed escalation in Middle East tensions supports a cautious approach.

Eurozone rate markets are pricing in roughly one additional 25 bps increase by year-end, with a more than 50% probability of a September hike. The decline in energy prices from early May through the end of June had reduced those rate hike expectations. However, those expectations firmed modestly this week as Brent crude and Dutch TTF gas prices have both risen approximately nine percent week-to-date.

The latest Fedspeak. Speaking at The Future of Market Liquidity and Functioning Workshop, New York Fed President John Williams said policy should remain data-dependent. He noted that the labour market remains strong and that there are no signs of second-order inflation effects, though inflation is still too high.

Williams said he is closely watching the potential impact of AI on inflation. He noted that if the AI boom persists and demand continues to outpace supply, it could create another upside inflation risk and potentially lift the neutral rate. Nevertheless, his baseline view is that AI adoption will raise productivity, representing a significant positive supply shock.

Dallas Fed President Lorie Logan, a voting FOMC member, offered limited direct guidance on the policy outlook. Speaking at the same conference, she said the FOMC could improve the efficiency and effectiveness of its open market operations by centrally clearing transactions on a voluntary basis. NY Fed System Open Market Account (SOMA) Manager Roberto Perli also noted that reserve-management purchases are not on a preset path and may be adjusted in any given month depending on money-market conditions. He cautioned that conditions could tighten through August as markets absorb a heavy influx of Treasury bill issuance.

US Stock Indices

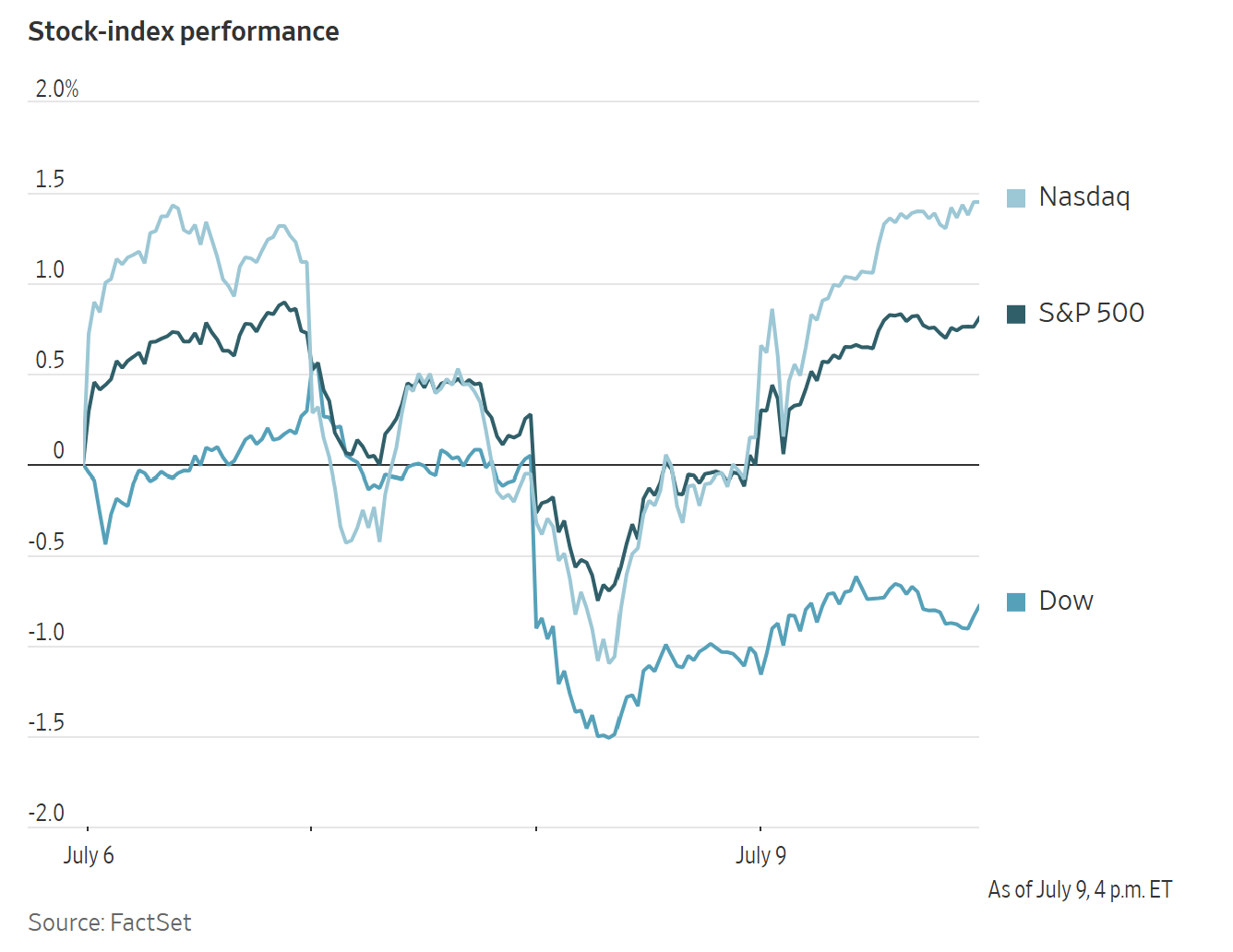

Dow Jones Industrial Average +0.27%

Nasdaq 100 +1.62%

S&P 500 +0.81%, with 7 of the 11 sectors of the S&P 500 up

On Wednesday, the Nasdaq Composite gained +1.30%, the Dow industrials rose +0.27%, or 139.02 points, and the S&P 500 advanced +0.81%, closing within one percent of a new all-time high.

Gains were led by a familiar group of market leaders, with semiconductor and memory stocks including Sandisk, Micron and Western Digital moving higher.

In corporate news, SK Hynix priced its American depositary receipt offering at $149 per depositary share, raising $26.5 billion in the latest major transaction for US capital markets.

Salesforce shares declined after KeyBanc issued a sharply negative downgrade, with analysts, led by Jackson Ader, lowering the stock to Sector weight from Overweight.

S&P Global Ratings downgraded Oracle’s credit rating on Thursday to BBB- from BBB, leaving it one notch above speculative-grade, or junk-bond, territory. Analysts said Oracle’s expanding AI infrastructure business is weakening its strong business-risk profile and noted they had previously underestimated the investment needed to scale the AI business and its effect on the company’s creditworthiness.

European Stock Indices

CAC 40 +0.90%

DAX +0.89%

FTSE 100 -0.16%

Commodities

Gold spot +1.10% to $4,121.02 an ounce

Silver spot +1.32% to $59.57 an ounce

West Texas Intermediate -2.95% to $71.81 a barrel

Brent crude -4.10% to $76.05 a barrel

Spot gold rose +1.10% to $4,121.02 per ounce on Thursday, supported by renewed demand after the prior session’s decline.

Spot silver gained +1.32% to $59.57 per ounce.

Crude benchmarks ended lower on Thursday as concerns over weakening oil demand outweighed the recent escalation in US - Iran tensions.

Brent futures fell $2.95, or -2.95%, to settle at $71.81 per barrel. US WTI crude declined $3.25, or -4.10%, to settle at $76.05 per barrel.

Qatar and Pakistan are reportedly working to bring Washington and Tehran back to the negotiating table, according to CNBC.

Goldman Sachs analysts noted that a recovery in Middle East oil supplies could be delayed if renewed tensions disrupt shipping through the Strait of Hormuz, as reported by Bloomberg news. The bank expects flows to normalise by the end of July if negotiations continue, sanctions waivers on Iranian oil are reinstated and shippers receive sufficient security assurances.

Iraqi Prime Minister Ali Al-Zaidi said Iraq will not leave OPEC, but is seeking a fair output quota within the producer group, according to Reuters.

Mediterranean diesel supply is tightening as Russian exports declined sharply in June due to damaged infrastructure, according to S&P Global. Russian diesel and gasoil exports to Turkey fell -44% y/o/y in June.

The EU is reportedly expected to unveil a 2040 electrification target next week to reduce its dependence on oil and gas following disruptions related to the Iran war. Analysts and officials also said governments are set to purchase millions of barrels of oil through 2028 to rebuild emergency reserves depleted by drawdowns after supply disruptions caused by the US - Israeli-led war on Iran, according to Reuters.

Note: As of 4 pm EDT 9 July 2026

Currencies

EUR +0.13% to $1.1429

GBP +0.09% to $1.3401

Bitcoin +1.74% to $63,235.47

Ethereum +0.54% to $1,747.08

The US dollar declined for a second consecutive session on Thursday. The dollar index slipped -0.11% to 100.94, while the euro rose +0.13% to $1.1429. Sterling strengthened +0.09% to $1.3401 after reaching a fresh three-week high of $1.3430.

The dollar weakened -0.13% against the Japanese yen to ¥162.32. The BoJ said the Iran war is likely to prompt more firms to raise prices later this year. It noted mounting inflationary pressures could strengthen the case for further rate hikes.

According to Reuters, Japan’s government plans to add an explicit reference to BoJ independence in its economic blueprint, after concerns over political interference in monetary policy helped push bond yields to multi-decade highs.

Fixed Income

US 10-year Treasury -1.9 basis points to 4.558%

German 10-year Bund -4.0 basis points to 3.055%

UK 10-year Gilt -8.1 basis points to 4.901%

US Treasuries firmed on Thursday as investors took advantage of this week’s selloff to add duration.

Treasuries extended gains and yields moved lower after the US Treasury sold $22 billion in 30-year bonds to strong demand, following solid results from 3-year and 10-year note auctions. The bonds were awarded at a yield of 5.058%, below market forecasts, suggesting investors did not require additional compensation to absorb the issuance.

In afternoon trading, the 10-year yield fell -1.9 bps to 4.558%, after reaching a seven-week high on Wednesday. The US 30-year yield declined -1.1 bps to 5.067%, after also climbing to a seven-week peak in the prior session.

The 2-year yield, which is most sensitive to Fed fund rate expectations, fell -4.0 bps to 4.189%. It had touched its highest level in two weeks on Wednesday.

Eurozone bond yields also declined on Thursday.

Germany’s 10-year yield fell -4.0 bps to 3.055%, after rising +9.6 bps on Wednesday to reach its highest level since mid-May.

Germany’s 2-year yield declined -6.0 bps to 2.654%, after rising +11.9 bps the previous day.

Money markets were pricing in 37 bps of additional ECB tightening on Thursday, down from 40 bps at one point on Wednesday. However, this was still well above the 21 bps expected at the start of the week.

Note: As of 4 pm EDT 9 July 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.