Is it ‘getting as close to as good as it gets’?

Key data to move markets today

EU: Spanish Harmonised Index of Consumer Prices, Eurozone Industrial Production and speeches by Austrian National Bank Governor Martin Kocher, Banca d'Italia Governor Fabio Panetta and Bundesbank President Joachim Nagel

UK: A speech by BoE Chief Economist Huw Pill

USA: PPI, Core PPI, NY Empire State Manufacturing Index, Fed’s Beige Book, Fed Chair Kevin Warsh testifies on the Semiannual Monetary Policy Report before the US Senate Committee on Banking, Housing and Urban Affairs and speeches by Fed Governor Lisa Cook, New York Fed President John Williams and St Louis Fed President Alberto Musalem

Global Macro Updates

Softer June Headline CPI. The US Department of Labor’s Bureau of Labor Statistics’ June CPI was materially softer than expected. Core CPI was flat m/o/m versus consensus for a 0.2% increase, while headline CPI declined 0.4% m/o/m versus expectations for a 0.1% decline. On an annualised basis, core CPI cooled to 2.6% and headline CPI eased to 3.5%, with both measures reaching their lowest levels since early 2026.

The decline in headline CPI was driven primarily by a 5.7% drop in energy prices, which more than offset modest increases in shelter (0.1%) and food (0.2%). Shelter inflation cooled from May, while core goods fell 0.1% for a second consecutive month. Core services were flat, suggesting limited pass-through from earlier energy-price increases.

Several categories contributed to the softer reading, including declines in motor-vehicle insurance, apparel, medical-care services and used vehicles. Household furnishings fell for a fourth consecutive month, suggesting that tariff effects have largely faded. Price gains were concentrated in airfares, vehicle maintenance and software, the latter of which carries a larger weight in core PCE.

Sell-side reactions were mixed. Citi said the softer CPI print, easing core PCE outlook and cooling labour market significantly reduced the likelihood of a July Fed rate hike and potentially any hikes this year. Bank of America said the report gave the Fed room to remain on hold in July, but continued to expect 75 bps of hikes beginning in September. UBS said the June reading did not yet indicate a new trend, although it noted that May likely marked the recent peak in inflation.

Fed Chair Kevin Warsh’s first day of congressional testimony. Fed Chair Kevin Warsh delivered the first day of his semiannual testimony to Congress, appearing before the House Financial Services Committee yesterday. He is scheduled to testify before the Senate Banking Committee today at 10:00 EDT.

In prepared remarks, Warsh reaffirmed policymakers’ commitment to restoring price stability. He noted the challenges the Fed faces in assessing the inflation and labour-market implications of rapid AI investment, stressed the need to reassess current Fed practices and reiterated his task-force approach.

During questioning, Warsh addressed repeated inquiries about Fed independence by emphasising the importance of an independent central bank and stating that he would pursue the Fed’s statutory mandate. Asked how he would respond if personally challenged by the US President, Warsh said, ‘I will do my job.’

As expected, and consistent with his remarks at the ECB’s recent Sintra conference, Warsh offered little direct policy guidance. Asked about the softer-than-expected June CPI report, he said he was not prepared to declare ‘mission accomplished’ and continued to see substantial work ahead. He also pushed back against the view that the Dallas Fed’s trimmed-mean CPI is his preferred inflation gauge and disagreed with the premise that the Fed’s dual mandate creates a ‘cruel choice’ between price stability and employment.

Warsh described AI as a supply shock unfolding faster than he had expected. On the balance sheet, he said he was not seeking a return to pre-GFC levels, but believed there was an equilibrium point below the current level. Regarding Fed communications, he said he preferred a more circumspect approach, while not ‘hiding the ball’, adding that he had found colleagues open-minded toward a more deliberate communications strategy.

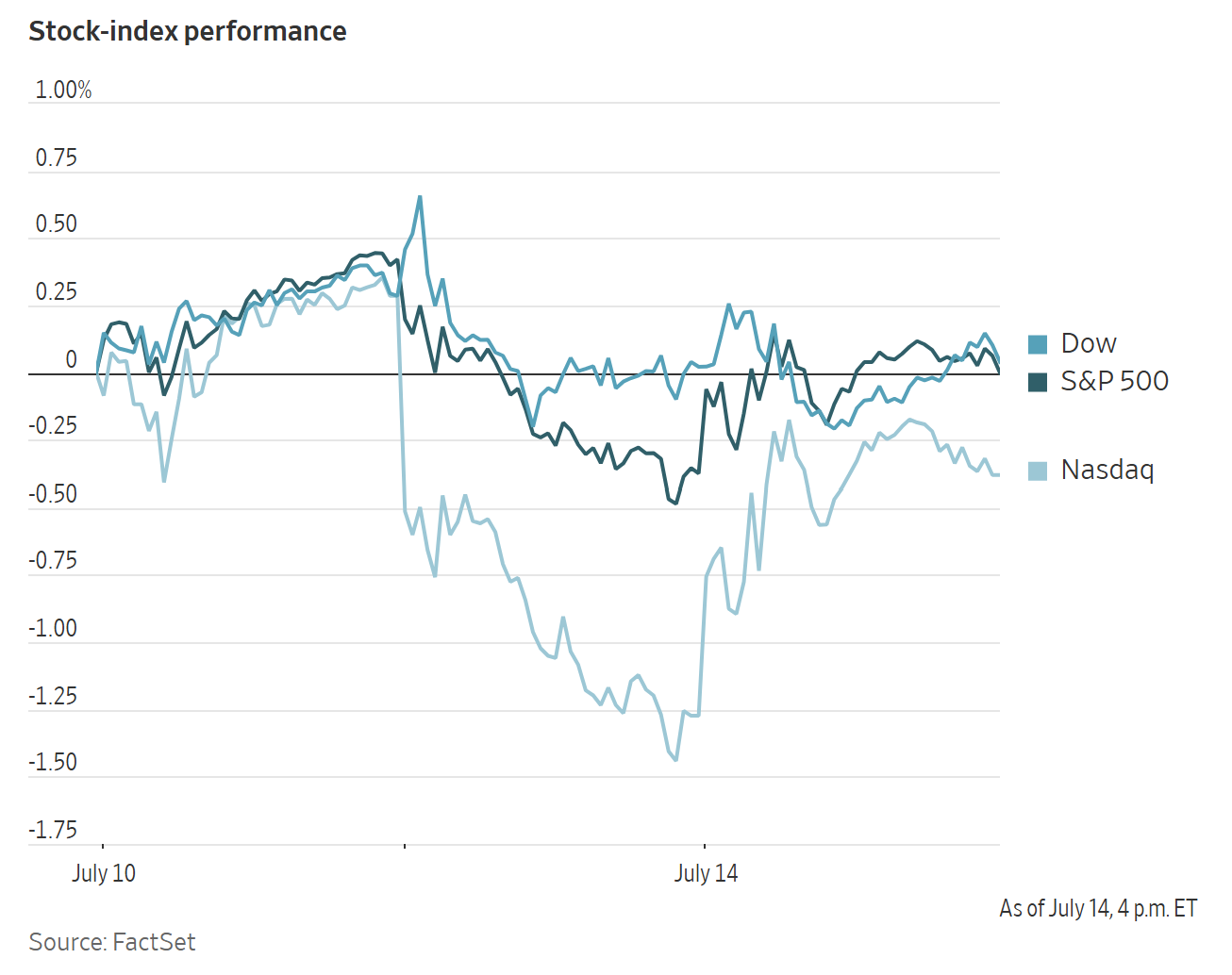

US Stock Indices

Dow Jones Industrial Average +0.02%

Nasdaq 100 +1.10%

S&P 500 +0.38%, with 6 of the 11 sectors of the S&P 500 up

US equities advanced on Monday, supported by strength in technology shares and a strong start to the Q2 earnings season. The Nasdaq Composite rose +0.90%, while the S&P 500 gained +0.38%. The Dow Jones Industrial Average lagged, finishing nearly unchanged at +0.02%, or 9.63 points, as IBM weighed on the index after its shares fell -25.21% following a sharp profit warning.

Q2 robust start to earnings. Bank earnings were notably strong, as robust equity issuance, active trading conditions and elevated market volatility supported a sharp increase in profitability across the largest US banks.

JPMorgan Chase, Goldman Sachs, Bank of America, Citigroup and Wells Fargo generated more than $49 billion in combined earnings, representing a 39% increase from a year earlier and exceeding analyst expectations. Aggregate revenue rose by more than 20%.

Results were also solid across consumer businesses, indicating that the US economy continued to benefit from resilient household demand and constructive corporate sentiment.

‘It’s getting close to as good as it gets,’ JPMorgan CEO Jamie Dimon said in its earnings call. Industrywide M&A volumes in the first half rose 72% in the US and 45% globally, with both reaching the highest levels in Dealogic data dating back to 1995.

Bank share performance was mixed following the results. JPMorgan and Bank of America rose +2.50% and +1.88%, respectively, while Goldman Sachs advanced +9.00% to a record closing high. By contrast, Citigroup fell more than -5.29% after management signalled a willingness to increase investment spending, raising analyst concerns about expenses. Wells Fargo declined -2.71%.

Trading businesses were a key source of strength. Goldman Sachs reported record equities revenue, up 72% from a year earlier, including a 91% increase in financing activity for institutional clients. JPMorgan’s equity markets revenue rose 86% y/o/y.

Bank of America posted record sales and trading revenue of $7.1 billion. Equities revenue also reached a record, rising 70% y/o/y to $3.6 billion.

However, Street commentary also emphasised a high earnings bar, limited net interest income upside, selective expense pressures and lingering deposit-cost overhangs. The profit outlook was mixed: investors were disappointed that Citi did not raise its RoTE target, while JPMorgan’s 22% RoTE was viewed positively despite higher investment spending.

On earnings calls, executives pointed to continued strength in consumer spending. Bank of America said H1 consumer spending rose +5% y/o/y and accelerated to 6% in Q2, while JPMorgan described spending growth as broad-based and said its data did not support a K-shaped-consumer narrative.

Credit quality was broadly characterised as stable. Citi said consumer credit card performance was better than expected, while Wells Fargo noted that net charge-offs declined 10 bps y/o/y. However, JPMorgan cited very mild deterioration in market credit-underwriting standards. Wells Fargo flagged substantial capital deployment into higher-risk wholesale assets, including AI data-centre construction.

JPMorgan also highlighted the strength of the labour market, while Wells Fargo said solid wage growth and employment conditions had helped offset inflationary pressure on consumers.

European Stock Indices

CAC 40 +0.03%

DAX +0.13%

FTSE 100 +0.30%

Commodities

Gold spot +1.33% to $4,053.98 an ounce

Silver spot +2.11% to $58.86 an ounce

West Texas Intermediate +2.35% to $79.83 a barrel

Brent crude +2.56% to $85.34 a barrel

Gold advanced on Tuesday, with spot prices up +1.33% at $4,053.98 per ounce, after earlier touching their lowest level since 1 July.

The US dollar index fell -0.37%, making dollar-denominated bullion more affordable for holders of other currencies.

Spot silver rose +2.11% to $58.86 per ounce.

Oil prices climbed to a one-month high on Tuesday after the US reimposed a naval blockade on Iran, a move expected to curb regional oil flows through the Strait of Hormuz.

Brent futures settled up $2.13, or +2.56%, at $85.34 per barrel, its highest level since 12 June. US WTI crude rose $1.83, or +2.35%, to $79.83 per barrel, its highest since 15 June.

Crude benchmarks had fallen to session lows after the US President said the Strait of Hormuz remained open to all traffic except Iran. He also said he would replace the 20% US reimbursement fee for safe passage through the waterway, announced Monday, with large trade and investment agreements from Gulf states. He did not rescind his pledge to restart the Iranian blockade, which took effect at 16:00 EDT yesterday.

Prices later rebounded on reports that Kuwait was engaging multiple projectiles launched from Iran. Shortly after 14:00 EDT, separate reports said another tanker off the coast of Oman had been struck, causing a fire in the engine room. Iran’s deputy foreign minister said that ‘we currently have no commitments when it comes to the Islamabad MOU with the United States.’

Tensions between Saudi Arabia and Yemen’s Houthis remained elevated.

Ukraine’s military said it struck two Russian oil refineries in the Bashkortostan and Krasnodar regions overnight. Ukrainian attacks on Russia’s energy infrastructure have forced Moscow to curtail diesel exports, lifting diesel prices globally. Kpler estimates Russian refinery throughput has fallen to a 21-year low of 3.8 million bpd.

In the US, diesel futures are up 21% so far in July, compared with a 13.98% gain in WTI crude. The move has lifted 3-2-1 and diesel crack spreads, key measures of refining margins, to record highs.

China customs data showed June crude imports fell to their lowest level in more than nine years, while OilChem estimated the country’s June refinery throughput also declined to a nine-year low.

Note: As of 4 pm EDT 14 July 2026

Currencies

EUR +0.32% to $1.1419

GBP +0.33% to $1.3386

Bitcoin +4.24% to $64,651.69

Ethereum +6.55% to $1,875.35

The US dollar weakened against major peers on Tuesday.

The dollar index was down -0.37% at 100.92, paring earlier losses after Fed Chair Kevin Warsh delivered his first semiannual testimony to Congress.

The euro gave back part of its earlier gains,but remained up +0.32% on the day at $1.1419, while sterling traded +0.33% higher at $1.3386.

Overnight currency volatility rose sharply, reflecting heightened trader caution. Overnight implied volatility for the euro, a gauge of demand for protection against large near-term currency swings, briefly topped 10% on Tuesday, a level rarely seen since April.

The Japanese yen rose +0.12% to ¥162.19 per dollar on Tuesday, remaining near 40-year lows and keeping traders alert to potential official buying from Tokyo.

The Japanese currency briefly strengthened after Finance Minister Satsuki Katayama said Tokyo could consider adjusting state pension fund asset allocations if the asset-management environment changed sharply.

Health Minister Kenichiro Ueno told a separate press conference that the ministry would review the Government Pension Investment Fund’s asset allocation if necessary, while downplaying the prospect of near-term changes.

Fixed Income

US 10-year Treasury -2.8 basis points to 4.592%

German 10-year Bund +1.1 basis points to 3.143%

UK 10-year Gilt +1.8 basis points to 4.992%

US Treasury yields declined across the curve on Tuesday after data showed consumer inflation slowed more than expected in June, reducing market expectations for a near-term Fed rate hike.

Yields later pared declines after Fed Chair Kevin Warsh told the House Financial Services Committee that today’s data did not mean the central bank had satisfied its price-stability mandate.

The US 10-year Treasury yield fell -2.8 bps, its largest daily decline since 24 June, to 4.592%, after earlier dropping to 4.525%.

Expectations for a Fed rate hike of at least 25 bps at the July meeting fell to 16.6% from 41.7% in the prior session, according to CME Group’s FedWatch tool. For the remainder of 2026, markets priced in 31.7 bps of hikes, down from 41.8 bps on Monday.

The US two-year Treasury yield, which tracks expectations for the Fed funds rate, fell -8.4 bps to 4.212% after earlier touching 4.147%, marking its largest daily decline since 11 June.

Germany’s policy-sensitive two-year government bond yield reached its highest level since July 2024 on Tuesday, as the Iran conflict fueled concerns that higher energy prices could lift inflation and interest rates.

Germany’s two-year Schatz yield, which is sensitive to expectations for the ECB deposit rate, rose +2.5 bps to 2.772% after reaching 2.798% earlier in the session, its highest level since July 2024.

Money markets implied an ECB deposit rate of 2.65% in December, compared with the current 2.25%, and fully priced a September rate hike.

Germany’s 10-year government bond yield rose +1.1 bps to 3.143%.

France’s spread widened recently as investors monitored domestic politics and fiscal plans, with the country at risk of missing its deficit-reduction target this year.

The French 10-year spread versus Bunds stood at 73.5 bps, above Italy’s 10-year BTP-Bund spread of 72.3 bps.

Note: As of 4 pm EDT 14 July 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.