Will earnings power a summer rally?

Key data to move markets today

EU: Italian CPI

UK: GDP, Industrial Production and Manufacturing Production

USA: Initial and Continuing Jobless Claims, Philadelphia Fed Manufacturing Survey, Retail Sales, Pending Home Sales and speeches by Dallas Fed President Lorie Logan, Kansas City Fed President Jeff Schmid and Fed Vice Chair Philip Jefferson

Global Macro Updates

Softer June PPI. June core PPI rose 0.2% m/o/m, below consensus of 0.4% and following May’s revised 0.1%. On an annualised basis, core PPI increased 4.7%, compared with consensus of 5.2% and May’s revised 4.6%.

Headline PPI declined 0.3% m/o/m, weaker than consensus of 0.0% and down from May’s revised 0.6%, increase marking the coolest monthly headline reading since April 2025. Annualised headline PPI rose 5.5%, versus consensus of 6.4% and May’s revised 6.0%.

Within final demand, goods prices fell 1.4% in June, the largest monthly decline since July 2022, driven by a 6.4% drop in energy prices. Services prices rose 0.2%, rebounding from a 0.1% decline in May, with the increase led by a 0.4% rise in trade services margins.

Among components that feed into PCE, portfolio management rose 0.5%, slowing sharply from May’s 4.8%. Airline passenger services declined 0.4% after rising 2.8% in May, hospital outpatient care fell 0.2% after a 0.1% increase and physician care rose 0.1% after being unchanged in May.

Separately, the July Empire State Manufacturing Index rose to 15.6, above consensus of 8.8 and June’s 5.7. New orders increased to 22.2 from 3.5, while shipments rose to 24.4 from 8.6, reaching a four-year high.

Labour indicators were also firmer, as the number of employees index rose to 11.4 from 9.6, its highest level since December 2022. The average employee workweek eased to 2.8 from 5.1, while price pressures moderated, with prices paid falling to 52.3 from 61.0 and prices received declining to 27.6 from 31.4.

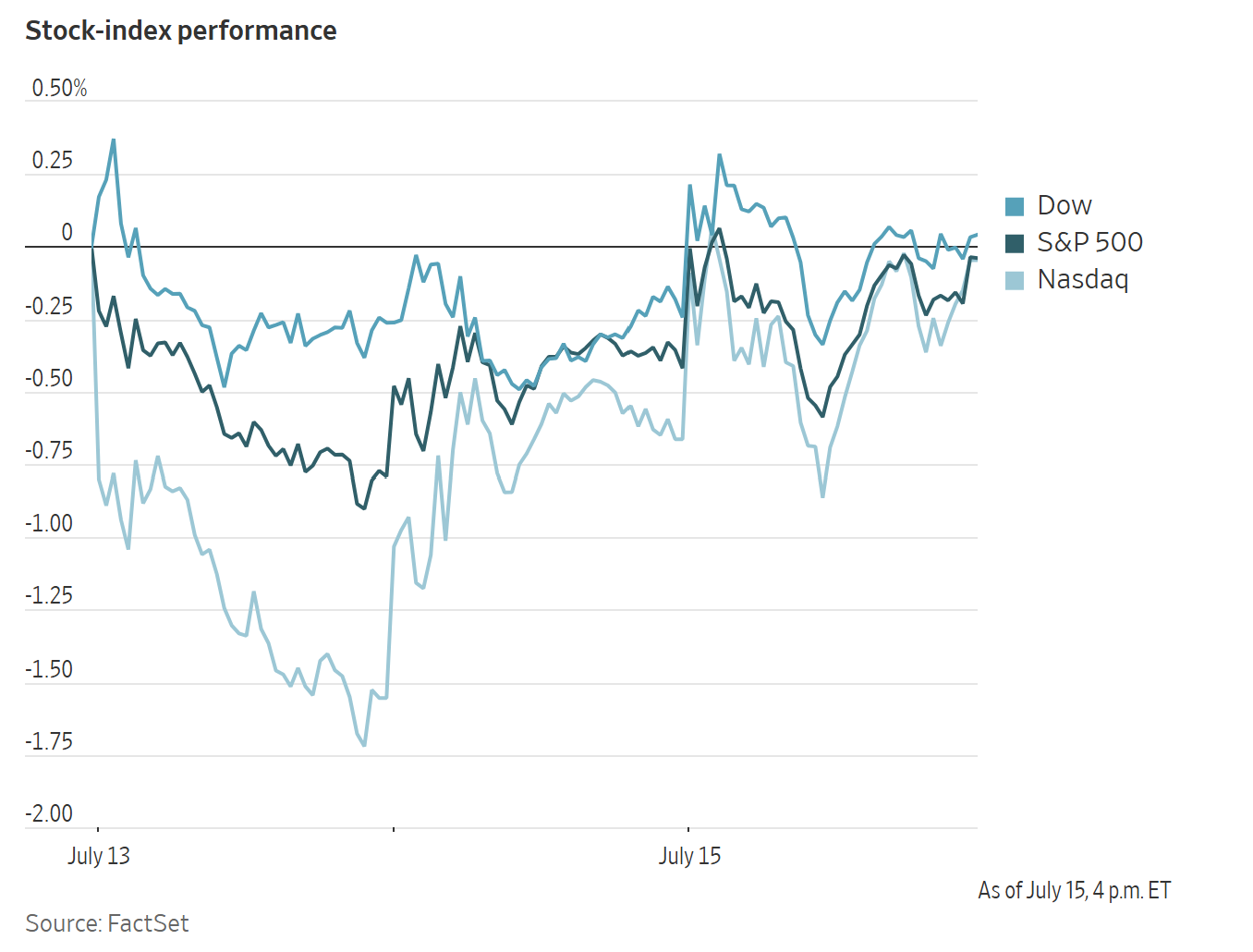

US Stock Indices

Dow Jones Industrial Average +0.29%

Nasdaq 100 -0.28%

S&P 500 +0.38%, with 5 of the 11 sectors of the S&P 500 up

Major US equity indexes advanced Wednesday, supported by a series of stronger earnings reports. The Nasdaq Composite rose +0.62%, the S&P 500 gained +0.38% and the Dow Jones Industrial Average added +0.29%, or 150.37 points. Megacap names including Apple, Alphabet, Microsoft and Amazon each rose more than 2.5%, helping lift the broader benchmarks.

In corporate news, Apple secured long-awaited government approval to launch Apple Intelligence in China, a move that could strengthen its position in the world’s most competitive smartphone market.

Morgan Stanley’s equity traders exceeded Wall Street expectations and delivered another quarterly record, extending the industry’s second-quarter gains from resilient markets and elevated volatility.

PayPal is working with advisers to assess strategic options, according to people familiar with the matter, as Stripe and private equity firm Advent pursue a takeover of the fintech pioneer valued at more than $53 billion.

Lucid shares rebounded +28.79% after falling -16.61% on Tuesday, when a report suggested the company could seek bankruptcy protection.

European Stock Indices

CAC 40 +0.19%

DAX -0.59%

FTSE 100 -0.13%

Commodities

Gold spot +0.09% to $4,057.80 an ounce

Silver spot -2.58% to $57.34 an ounce

West Texas Intermediate +0.51% to $80.24 a barrel

Brent crude +0.35% to $85.64 a barrel

Gold and energy markets moved higher on Wednesday, with precious metals firmer and crude benchmarks extending recent gains amid escalating geopolitical tensions and supportive US inventory data.

Spot gold rose +0.09% to $4,057.80 per ounce after falling nearly one percent earlier in the session, while spot silver declined -2.58% to $57.34 per ounce.

WTI and Brent also closed higher, after both benchmarks advanced more than eleven percent over the prior two sessions, as markets continued to price in worsening violence in the Gulf region, further Iranian threats to restrict Red Sea exports and the latest US stockpile figures.

Brent crude futures rose 30 cents, or +0.35%, to $85.64 per barrel, while US WTI futures gained 41 cents, or +0.51%, to $80.24 barrel; both benchmarks remained close to the one-month highs reached on Tuesday.

The US continued strikes on multiple Iranian positions yesterday, with attack waves launched at 6:00 ET and 15:00 ET, while Iran struck several neighboring countries, including Bahrain, Jordan, Kuwait and the UAE. The US President told Fox that strikes against Iran would expand next week.

The IRGC also threatened to close additional export corridors that benefit the US and its allies, after the US reimposed a blockade on all Iranian vessels as of 16:00 ET on Tuesday.

Shipping companies are avoiding a US military-guided transit scheme through the Strait of Hormuz after a series of Iranian attacks on vessels raised safety concerns, according to seven maritime security and shipping industry sources cited by Reuters.

The DOE Weekly Petroleum Status Report showed crude inventories drawing 1.69 million barrels, gasoline stocks drawing 1.53 million barrels and distillate stocks building 4.56 million barrels, while Cushing and jet fuel inventories increased by 400,000 barrels and 800,000 barrels, respectively. Crude exports recovered from eight-month lows, while jet fuel production held above 2.0 million bpd for an 11th consecutive week.

Ukraine attacked another 17 oil tankers and two gas carriers yesterday, according to the country’s drone commander. Separately, Russian energy companies reportedly asked Indian refiners for more gasoline, though Reuters sources said at least three Indian refiners indicated they had no surplus volumes available for export.

Official Chinese data showed June refinery throughput down -18.0% y/o/y to 51.24 million tons, the lowest level since March 2020.

Note: As of 4 pm EDT 15 July 2026

Currencies

EUR +0.39% to $1.1463

GBP +1.09% to $1.3532

Bitcoin +0.23% to $64,801.62

Ethereum +2.44% to $1,921.08

The US dollar weakened against major currencies on Wednesday, with the dollar index falling -0.41% to 100.51, its lowest level since mid-June.

The dollar slipped -0.04% against the yen to ¥161.12, while the euro rose +0.39% to $1.1463, its highest level since 19 June.

Sterling advanced +1.09% to $1.3532, its strongest level since mid-May. The British pound strengthened against both the dollar and the euro on Wednesday, as markets focussed on the likely composition of a Burnham government and the implications for fiscal policy.

Against the euro, the pound rose +0.30% to 85.05 pence, its strongest level since June last year.

Andy Burnham is expected to be formally named prime minister on 20 July, shifting investor attention to his finance minister selection against the backdrop of the UK’s fragile public finances.

The Financial Times reported that Home Secretary Shabana Mahmood is likely to lead the finance ministry, easing concerns that Burnham could appoint Ed Miliband, who is viewed as favouring a more expansionary fiscal stance.

Money markets are fully pricing in a BoE hike by the November policy meeting, with a second hike priced by April 2027.

Fixed Income

US 10-year Treasury -3.7 basis points to 4.555%

German 10-year Bund +0.7 basis points to 3.150%

UK 10-year Gilt -5.8 basis points to 4.934%

US Treasury yields declined on Wednesday, with the 10-year note registering its first back-to-back daily decline in nearly three weeks, after a second consecutive day of US economic data pointed to easing price pressures.

The 10-year yield fell -3.7 bps to 4.555%, while the two-year US Treasury yield, which typically tracks Fed funds rate expectations, declined -6.9 bps to 4.143%, marking its largest two-day drop since late March.

The US 2s10s curve steepened to 41.2 bps from 38.0 bps on Tuesday.

Eurozone bond yields were mixed. Germany’s two-year Schatz yield fell -2.8 bps to 2.744%, while the 10-year Bund yield edged up +0.7 bps to 3.150%.

Money markets are pricing in 43 bps of further ECB tightening this year, up from 30 bps one week ago but below Tuesday’s peak of 48 bps.

Note: As of 4 pm EDT 15 July 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.