Economic and US Treasury Market Review

- US GDP increased at a 2.0% annualised rate last quarter, the Commerce Department said in its third estimate of first-quarter GDP. That was revised up from the 1.3% pace reported in May.

- The US labour market remained relatively strong despite the unemployment rate climbing to 3.7% in May, up from a 53-year low of 3.4%. Nonfarm payrolls increased 339,000 in May, well above forecasts.

- Inflation continued to decline, with headline inflation falling to 4% in May, down from April’s 4.9%.

- The US Consumer Confidence Index was 109.7 in June, rising from 102.5 in May.

- Flash PMIs in the US, UK and Eurozone were softer in June with the S&P Global/CIPS Flash UK Composite Output Index showing business activity moderating to a three month low at 52.8 in June, down from May’s 54. The HCOB flash Composite PMI for the Eurozone dropped to its lowest over a five-month period to 50.3 in June, down from 52.8 in May. In the US the flash S&P Composite PMI also came in at a three-month low at 53.0, down from May’s 54.3.

- The US housing market showed unexpected strength with housing starts hitting 30 year highs.

Yield curves

Rates across the US Treasury yield curve were higher in June with the very short end

rising significantly. The yield on the 2-year Treasury note, which is highly sensitive to expectations for the Fed Funds rate, is at 4.71%, up from 4.4% at the start of the year. The benchmark 10-year US Treasury note yield is at 3.71% while the yield on the 30-year bond is at 3.81%. As a result of rising rates US government bond investors have experienced positive returns so far this year in contrast to 2022 which marked the end of a 40 year bull market in bonds.

Rising rates tend to impact shorter-dated bonds more than longer ones. And higher borrowing costs increase the odds of a recession, when investors typically seek protection in longer-dated securities. The yield curve inversion, the yield level on shorter-dated Treasuries being above longer dated Treasuries, deepened in June after Fed Chair Jerome Powell indicated that the central bank would likely raise rates two more times this year by another 50 basis points and may even go further depending on what the data reveals. The CME Market Watch tool now shows an 81.8% chance of the Fed raising rates by 25 basis points in July.

While the US growth outlook remains positive but subdued due to tightening credit conditions resulting in lower capital investment rates and a slight loosening in labour market tightness, the Fed paused its hiking path during its 14 June meeting and maintained the Fed Funds rate to a range of 5.00-5.25%. The lagged effects of previous rate rises and credit market conditions following banking sector volatility in March and April may not have fed through to the market.

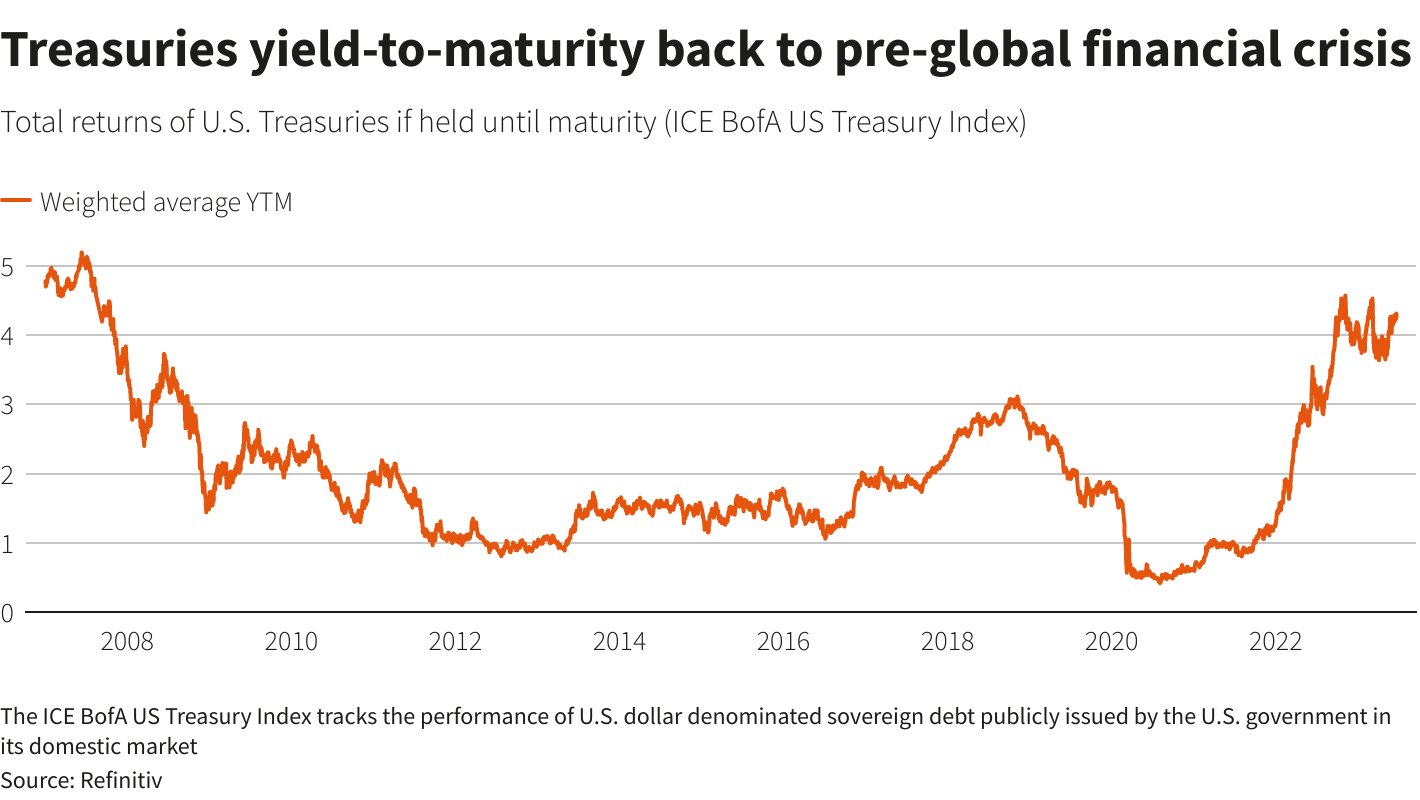

Returns on US bonds, including interest payments and price changes, totaled 2.4% so far this year, compared with negative 13% last year, according to the Morningstar US Core Bond TR USD index. As noted by Refinitiv, yield-to-maturity of government bonds, as measured by the ICE BofA US Treasury Index, stood at 4.3% as of last week, up from 3.1% a year earlier.

Source: Bloomberg 6 pm EDT 28 June 2023

Global Economic and Market Review

The Bank of England surprised markets by raising rates by 50 bps at its 22 June policy meeting, likely due to hotter than expected headline inflation at 8.7% in May. Core inflation came in at 7.1% in May, up from 6.8% in April and the highest it's been since 1992.The BoE, which has raised interest rates to a 15-year high, has said the UK labour market and not Brexit is to blame for stubbornly high inflation. As noted by Sky news, BoE Governor Andrew Bailey said the tight jobs market - with near-record low unemployment, more than a million jobs vacancies and wage growth of 7.2% - was the reason the UK inflation rate is higher than both the US and Eurozone.

The ECB, as expected, raised rates by another 25 basis points at its meeting on 15 June despite signs of slowing growth in the Eurozone. However, Eurozone bonds have been falling through June and investors may start to demand a greater term premium as the ECB is very likely to continue raising rates until at least September. This will put peripheral bonds such as Italy’s at risk from tighter financial conditions. According to Worldgovernmentbond.com, the spread between Germany’s 10 Year and Italy’s 10 year is 167.4, up 17.5 basis points this month. Germany’s spread vs the US is -140.6 basis points. The spread between Germany’s and Greece’s 10 year is now only 123.5 basis points.

Globally it is clear that the differences in domestic interest rates and monetary policy cycles will continue to drive yields. It comes as central banks continue to face sticky inflation, slow growth, energy uncertainty, and rising geopolitical stresses as the war in Ukraine continues, and tensions between the US and China remain high

Key risks

Markets are not, it seems fully appreciating the persistence of high inflation, particularly of core inflation, and have, to some extent, tried to bet against the Fed this year with expectations of a rate cut towards the end of this year or early next. These have only finally been extinguished by Fed Chair Powell stating during the press conference following the June meeting, that it would be a couple of years before rate cuts kicked in. As a result of this long-term yields will need to move up further. Short-dated government bonds, which are subject to higher levels of volatility, are offering higher yields, which, if interest rates stay in line with expectations over the next 2 to 3 months, should offer attractive income with limited risk. However, if inflation remains stubbornly high, bond prices could still weaken. However, investors should remain wary of the yield curve suddenly changing. As noted by Bloomberg news, if the yield curve were to suddenly steepen, either because long-term yields rise or short-term rates slump, it would result in some traders quickly shifting their portfolios to close basis trade bets.

However there are some other risks:

- Inflation fails to moderate as expected, weighing on asset prices. US headline and core inflation remains well above target for longer than forecast. likely to cause a hit to interest sensitive stocks in the technology sector, financials, telecommunications, and infrastructure.

- Policymakers tighten too rapidly, undermining global economic expansion. In the 28 June ECB summer meeting of central bankers in Portugal, the Fed, the BoE, and the ECB all agreed that rates will remain higher for longer as they battle persistently high core inflation.

- Geopolitical flare-ups. In a sign of rising tensions between the US and China, the US is contemplating new export controls on chips for artificial intelligence to China and ASEAN countries are now planning on holding military exercises outside the South China sea.

DISCLAIMER: While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here.