Will CPI confirm stagflation fears?

Key data to move markets today

EU: German Harmonised Index of Consumer Prices and a speech by ECB Vice President Luis de Guindos

US: CPI, Factory Orders, Michigan Consumer Expectations Index, Michigan Consumer Sentiment Index and UoM 1-year and 5-year Consumer Inflation Expectations

CHINA: CPI and PPI

Global Macro Updates

February PCE, initial jobless claims and final Q4 GDP. In February, the headline Personal Consumption Expenditures (PCE) price index increased by 0.4% m/o/m, exceeding the consensus estimate of a 0.3% rise and January's 0.3% gain. The annualised headline figure stood at 2.8%, aligning with both consensus expectations and the previous month's reading. Core PCE also advanced 0.4% m/o/m, matching consensus forecasts and January's increase; the annualised core rate registered at 3.0%, slightly above the consensus of 2.9% and just below January's 3.1%.

For the same period, US personal spending rose by 0.5% m/o/m, in line with consensus estimates and higher than January's revised 0.3% increase (previously reported as 0.4%). Conversely, personal income declined 0.1% m/o/m, falling short of the expected 0.3% rise and January's unrevised 0.4% gain.

These results follow the release of the FOMC minutes, which underscored stalled progress on inflation. Tariff-related goods inflation has re-accelerated, offsetting the easing observed in housing services. At the same time, consumer spending remains resilient and the labour market appears balanced, thereby reducing the expectations of imminent interest rate cuts.

Initial jobless claims totaled 219,000, surpassing the consensus of 210,000 and the previous week's upwardly revised figure of 203,000 (previously 202,000). Continuing claims came in at 1,794,000, below the consensus estimate of 1,840,000 and last week's downwardly revised total of 1,832,000 (previously 1,841,000).

The final reading for Q4 GDP indicated a growth rate of 0.5%, which was lower than the consensus projection of 0.7% and the prior revision of 0.7%. The downward adjustment was primarily attributed to reduced investment.

Prospects for an Iran-US ceasefire enhanced by negotiations between Israel and Lebanon. Renewed optimism regarding the US - Iran ceasefire surfaced after Israeli Prime Minister Netanyahu told his cabinet to initiate direct negotiations with Lebanon. As reported by Axios, this development followed Netanyahu’s conversation yesterday with President Trump and envoy Steve Witkoff, both of whom encouraged him to reduce military operations in Lebanon and pursue diplomatic dialogue.

This positive diplomatic progress triggered a risk-on sentiment in US equity markets, alleviating earlier concerns about the ceasefire's durability that had intensified following vigorous Israeli strikes on Lebanon Wednesday and Iran's warning that it would abandon the broader ceasefire should the attacks persist.

Concurrently, direct negotiations between the US and Iran are scheduled to take place on Saturday in Islamabad, Pakistan, with Vice President Vance heading the US delegation, which will include Steve Witkoff and Jared Kushner.

However, tanker movement through the Strait of Hormuz remains severely restricted. On Thursday, the CEO of the UAE state-run oil company confirmed that the strait is effectively closed with limited access. Ship tracking data indicated that only one oil products tanker and five dry bulk carriers transited the strait on Wednesday.

Furthermore, there is increasing attention on the domestic political repercussions of the conflict. Some commentators have characterised the situation as a strategic setback for the US, expressing concerns about the potential impact on midterm elections due to affordability pressures stemming from war-related factors.

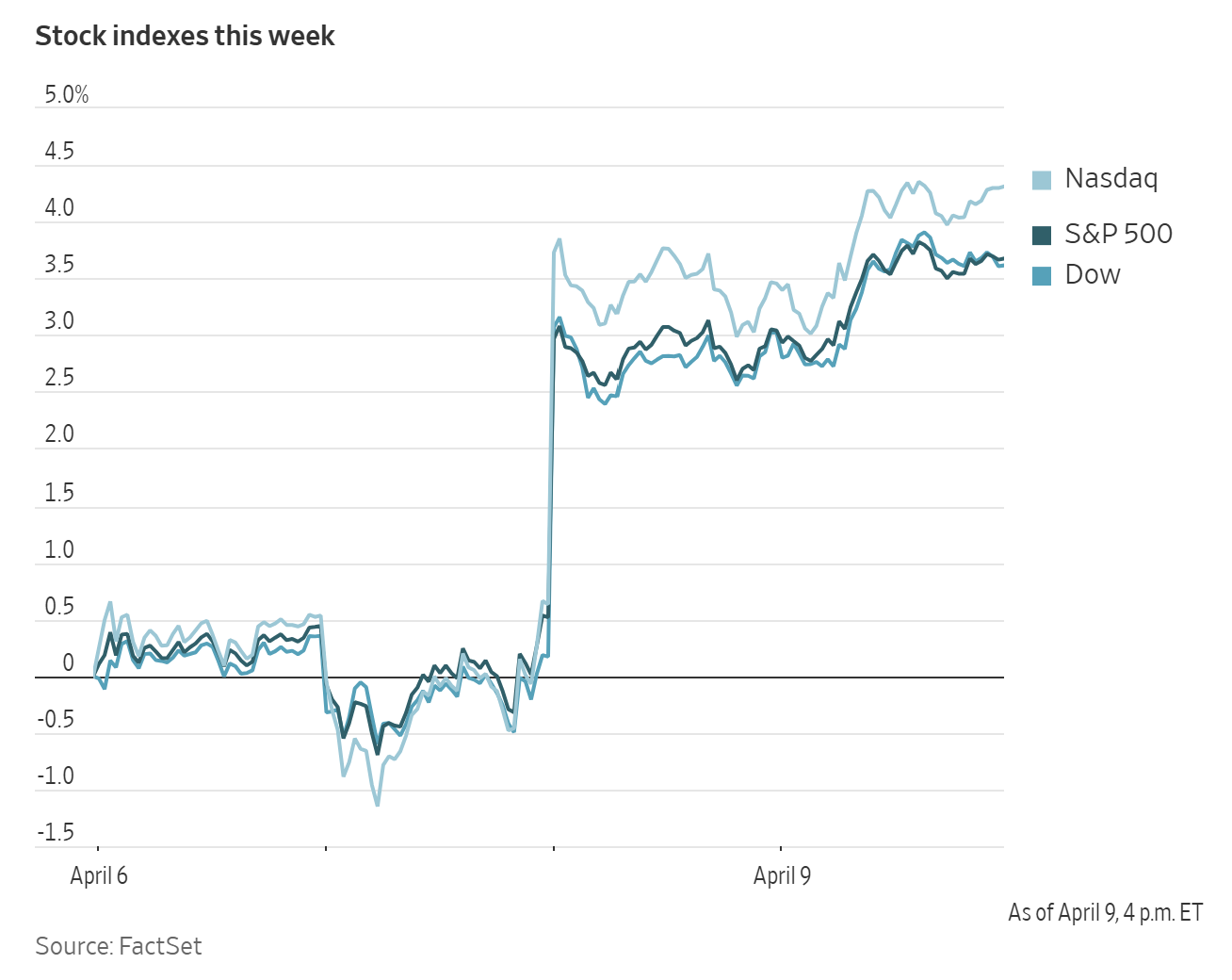

US Stock Indices

Dow Jones Industrial Average +0.58%

Nasdaq 100 +0.72%

S&P 500 +0.62%, with 9 of the 11 sectors of the S&P 500 up

The S&P 500 extended its winning streak to seven consecutive sessions, buoyed by optimism surrounding the potential for the US to secure a lasting peace agreement with Iran.

During the morning, equity markets traded lower amid ongoing Israeli strikes on Lebanon and reports that the Strait of Hormuz remained largely inaccessible. Market participants expressed concern that continued violence in Lebanon could undermine the fragile two-week ceasefire announced by the Trump administration and Iran.

Around midday, stocks began to recover following comments from Israeli Prime Minister Benjamin Netanyahu, who indicated that Israel would soon engage in direct negotiations for a peaceful resolution with Lebanon. President Trump stated to NBC News that he had requested the Israeli leader to scale back military operations.

The Dow Jones Industrial Average advanced +0.58%, returning to positive territory for the year. The S&P 500 increased +0.62%, while the Nasdaq Composite Index rose +0.83%, closing higher than its level prior to the onset of the Iran conflict.

In corporate news, The Wall Street Journal reported that Walt Disney is preparing for substantial layoffs, marking one of the first significant actions under new CEO Josh D’Amaro.

Constellation Brands posted lower revenue, but noted encouraging signs of a rebound in spending among Hispanic consumers.

Seven & i Holdings, the parent company of 7-Eleven, issued a warning regarding a decline in annual profits and announced a delay in the planned initial public offering of its North American convenience-store business.

Shares of Brown-Forman increased on Thursday following a report from The Wall Street Journal that closely-held Sazerac had approached the company regarding a potential transaction. Brown-Forman, producer of Jack Daniel’s, revealed last month that it was in discussions to merge with French spirits manufacturer Pernod Ricard. The proposed deal, if finalised, would involve a significant stock component, and the families behind both companies would likely retain substantial stakes in the merged entity, according to individuals familiar with the matter.

S&P 500 Best performing sector

Consumer Discretionary +2.46%, with Amazon +5.60%, Lululemon Athletica +4.82% and Deckers Outdoor +3.22%

S&P 500 Worst performing sector

Energy -1.16%, with Texas Pacific Land -15.68%, Phillips 66 -4.13% and Marathon Petroleum -3.65%

Mega Caps

Alphabet +0.52%, Amazon +5.60%, Apple +0.61%, Meta Platforms +2.61%, Microsoft -0.34%, Nvidia +1.01% and Tesla +0.69%

Information Technology

Best performer: Lam Research +4.98%

Worst performer: ServiceNow -7.86%

Materials and Mining

Best performer: Freeport-McMoRan +2.07%

Worst performer: CF Industries -5.37%

European Stock Indices

CAC 40 -0.22%

DAX -1.14%

FTSE 100 -0.05%

Commodities

Gold spot +0.39% to $4,763.62 an ounce

Silver spot +1.94% to $75.56 an ounce

West Texas Intermediate +2.59% to $99.00 a barrel

Brent crude +0.30% to $96.47 a barrel

Gold and silver prices advanced on Thursday as market participants closely followed developments related to the two-week ceasefire agreement between the US and Iran.

Investors are also anticipating today’s US March CPI report, which is projected to reflect an increase in energy prices attributed to ongoing tensions in the Middle East.

Gold rose +0.39% to $4,763.62, while spot silver climbed +1.94% to $75.56.

WTI and Brent crude oil prices closed higher on Thursday, recovering from losses recorded during the previous session. The day began with both crude benchmarks trading up, as Iran stipulated that Israeli attacks on Lebanon must be included in the terms of the ceasefire established on Tuesday; otherwise, Iran would not reopen the Strait of Hormuz. Consequently, tanker traffic through the Strait on Thursday reached its lowest level since the onset of the conflict, attributed to the Iranian Revolutionary Guard Corps (IRGC) restricting passage to twelve vessels per day and ship operators seeking clearer guidance on requirements for safe transit.

During the session, both WTI and Brent crude began to decline from their respective intraday highs of $102.75 and $99.25. This downturn followed Israeli Prime Minister Netanyahu’s announcement that he had told his cabinet to initiate direct negotiations with Lebanon at the earliest opportunity. Around the same time, NATO Secretary General Mark Rutte stated that most member countries had agreed to deploy military assets to secure the Strait of Hormuz. Rutte also briefed several NATO member nations earlier in the day, indicating that former President Trump expects concrete commitments in the coming days to help safeguard the strait.

Persistent concerns regarding the ceasefire remain, as Iran continues to demand full compensation for war-related damages and insists on managing all maritime traffic passing through the Strait, conditions that Washington has deemed unacceptable. Later in the day, Netanyahu clarified that his authorisation was limited to direct negotiations with Lebanon, not to a comprehensive ceasefire.

Saudi Arabia’s state news agency reported that recent attacks had resulted in the loss of 700,000 barrels per day (bpd) of refining capacity and 600,000 bpd of production capacity, impacting major facilities such as Manifa, Satorp, Ras Tanura, refineries near Yanbu and the East-West pipeline.

At the close of trading, Brent crude futures settled at $96.47 per barrel, up 29 cents or +0.30%, while WTI futures rose by $2.50, or +2.59%, to $99.00 per barrel.

Following the close of the oil market, reports emerged of explosions in Dubai, with Kuwait indicating ongoing interceptions of missiles and drones targeting critical energy infrastructure. At the same time, Prime Minister Netanyahu announced that Israel was conducting strikes against Hezbollah launch sites in Lebanon.

Note: As of 4 pm EDT 9 April 2026

Currencies

EUR +0.31% to $1.1701

GBP +0.18% to $1.3424

Bitcoin +0.99% to $72,260.18

Ethereum -0.17% to $2,210.81

The US dollar extended its decline on Thursday against the euro and the British pound, but traded higher against the Japanese yen. The US dollar index declined -0.21% to 98.80.

The Japanese yen experienced a modest depreciation, falling -0.29% against the dollar to ¥158.96 per dollar. The euro advanced +0.31% to $1.1701, and the British pound rose +0.18% to $1.3424. Additionally, the euro was at 87.11 pence, a touch higher on the day, and bouncing off its Wednesday low of 86.88 pence.

Fixed Income

US 10-year Bond -2.0 basis points to 4.281%

German 10-year Bund +3.7 basis points to 2.988%

UK 10-year gilt +2.8 basis points to 4.679%

US Treasury yields ended slightly lower on Thursday amid volatile trading, following the release of a series of economic reports. Investors shifted their attention from earlier highs as they assessed the prospects for a lasting truce in the Middle East.

Yields initially increased following the release of economic data. According to the Commerce Department, GDP expanded in Q4 at an annualised rate of 0.5%, revised downward from the previously reported 0.7% and below economists' consensus estimate of 0.7%.

The yield on the US 10-year Treasury note declined -2.0 bps to 4.281%, after reaching a high of 4.321% earlier in the session.

The yield on the 30-year Treasury bond edged down -0.3 bps to 4.885%. The two-year US Treasury yield, closely tied to Fed fund rate expectations, declined -2.7 bps to 3.773%.

The spread between yields on two- and 10-year US Treasury notes stood at 50.8 bps.

A $22 billion auction of 30-year Treasury bonds concluded the week’s new supply, with results described by analysts as somewhat soft. The bid-to-cover ratio was 2.39x, slightly below the historical average.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing in 8.3 bps of rate cuts in 2026, in contrast with the 6.4 bps of rate hikes priced in a week ago. Fed funds futures traders are now pricing in a 1.6% probability of a 25 bps rate hike at the 29 April FOMC meeting, compared to last week’s 0.0% probability.

Eurozone government bond yields increased on Thursday, partially reversing the significant decline observed in the previous session, as market participants evaluated the sustainability of the US - Iran ceasefire.

The yield on the German 10-year bund rose +3.7 bps to 2.988%, following a decrease of -13.5 bps on Wednesday.

Italy’s 10-year government bond yield increased +6.4 bps to 3.773%, maintaining the spread over bunds at 78.5 bps.

In addition, traders moderated expectations for future European Central Bank rate hikes. Nevertheless, money markets continue to price in two ECB policy increases for this year, with a modest possibility of a third. During the conflict, markets have, at times, anticipated three rate hikes from the ECB in 2026.

Germany’s 2-year bond yield, sensitive to ECB rate expectations, climbed +1.8 bps to 2.521% after falling -21.9 bps on Wednesday.

The probability of a rate hike at the ECB’s upcoming 29 April meeting stood at 23% on Thursday.

Note: As of 4 pm EDT 9 April 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.