Is the US on the brink of stagflation?

Key data to move markets today

EU: German IFO Survey of Business Climate and Current Assessment and Expectations Surveys and speeches by Dutch Central Bank Governor Olaf Sleijpen, German Bundesbank President Joachim Nagel, ECB President Christine Lagarde, and ECB Chief Economist Philip Lane

UK: Consumer Price Index (CPI), Core CPI, Producer Price Index (PPI), Core PPI, Retail Price Index and a speech by BoE External Member Megan Greene

US: A speech by Fed Governor Stephen Miran

Global Macro Updates

March preliminary S&P PMIs indicate stagflationary pressures; Richmond Fed Index surpasses expectations. The flash March S&P Global US Composite PMI registered at 51.4, modestly below both the consensus expectation of 51.7 and the final reading of 51.9 for February. The Manufacturing PMI outperformed, coming in at 52.4 against a consensus of 51.7 and February’s 51.6. Meanwhile, the Services PMI declined to 51.1, underperforming relative to the consensus of 52.0 and the prior month’s 51.7.

The report highlighted that US business activity growth slowed to an 11-month low, attributable to softer new orders and a marked increase in prices following the outbreak of conflict in the Middle East. Initial assessments suggest some impact from recent developments in the war with Iran.

Input costs surged, primarily driven by elevated energy prices related to the ongoing conflict, resulting in overall input costs reaching a 10-month peak. This, in turn, prompted the most significant rise in selling prices in over three and a half years, with notable increases observed across both services and goods sectors.

Employment contracted for the first time in more than a year, as firms sought to reduce overheads amid heightened economic uncertainty.

Chris Williamson, Chief Business Economist at S&P, noted that the PMI data point towards an annualised GDP growth of merely 1.0% and a modest 1.3% expansion for Q1. At the same time, price indicators suggest inflation may accelerate towards 4%, thereby elevating the risk of stagflation.

Elsewhere, the March Richmond Fed Index recorded a reading of 0.0, surpassing both the consensus forecast of -5.0 and February’s -10.0. Shipments improved to -2.0 from -13.0, new orders rose to 4.0 from -9.0, and employment increased to -2.0 from -7.0. While growth in prices paid eased slightly, the rate of increase in prices received accelerated.

Additionally, final figures for Q4 nonfarm productivity showed an increase of 1.8%, falling short of the 2.0% consensus and the preliminary estimate of 2.8%. Unit labour costs rose by 4.4%, outpacing both the consensus of 3.5% and the preliminary reading of 2.8%.

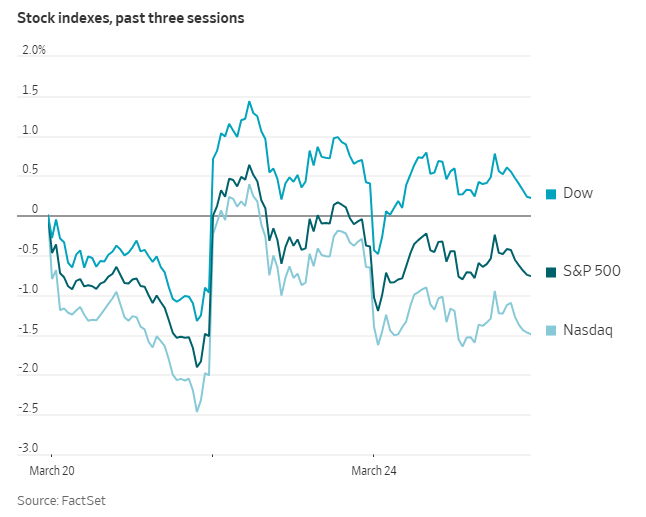

US Stock Indices

Dow Jones Industrial Average -0.18%

Nasdaq 100 -0.77%

S&P 500 -0.37%, with 4 of the 11 sectors of the S&P 500 down

On Tuesday, Wall Street moderated its expectations for a swift resolution to avert an oil shock. However, investors struggled to find clear direction. News emerged that the Pentagon is deploying a combat brigade to the Middle East, which was soon followed by the US President’s assertion that peace talks were making progress.

The Nasdaq Composite fell -0.84%, while the S&P 500 slipped -0.37%. The Dow Jones Industrial Average edged down -0.18%, losing 84.41 points.

In corporate news, KB Home revised its fiscal-year guidance downward, citing ongoing challenges in the housing market.

Shares of Jefferies rose following reports by the Financial Times that Japan's Sumitomo Mitsui Financial Group is considering plans for a potential takeover.

Nintendo shares declined in Tokyo after Bloomberg news reported that the company is reducing production of its Switch 2 gaming console in response to sluggish sales in the US.

S&P 500 Best performing sector

Energy +2.05%, with Marathon Petroleum +4.89%, APA +4.53%, and Phillips 66 +4.16%

S&P 500 Worst performing sector

Communication Services -2.50%, with Take-Two Interactive Software -4.72%, Alphabet -3.28%, and Netflix -3.28%

Mega Caps

Alphabet -3.28%, Amazon -1.43%, Apple +0.06%, Meta Platforms -1.90%, Microsoft -2.73%, Nvidia -0.27%, and Tesla +0.57%

Information Technology

Best performer: Corning +8.43%

Worst performer: Gartner -6.89%

Materials and Mining

Best performer: Celanese +8.32%

Worst performer: Amcor -0.58%

European Stock Indices

CAC 40 +0.23%

DAX -0.07%

FTSE 100 +0.72%

Commodities

Gold spot +1.54% to $4,473.59 an ounce

Silver spot +3.03% to $71.23 an ounce

West Texas Intermediate -0.92% to $88.39 a barrel

Brent crude -0.15% to $99.91 a barrel

Gold prices rebounded on Tuesday, as Middle East tensions boosted bullion's status as a safe haven, despite ongoing geopolitical uncertainty raising inflation concerns and expectations of more global interest rate increases.

Spot gold rose +1.54% to $4,473.59 per ounce, following a drop to its lowest level since November on Monday. Since the onset of the US-Israeli led conflict with Iran on 28th February, spot gold has fallen -15.54%.

Spot silver increased +3.03% to $71.23 per ounce.

Oil prices edged lower on Tuesday after a volatile session, as the largest disruption to crude supplies continued. Iran refuted claims of negotiations with the US to resolve the conflict in the Gulf. This denial directly contradicted statements from the US President, who suggested that an agreement could soon be reached.

Brent crude futures settled 15 cents lower, marking a -0.15% decrease to $99.91 per barrel. US WTI declined by 82 cents, or -0.92%, closing at $88.39 per barrel.

The ongoing conflict has effectively halted the transit of approximately one-fifth of the world’s oil and liquefied natural gas through the Strait of Hormuz. According to the International Energy Agency, this represents the most significant oil supply disruption in history.

Conditions on the ground remain unchanged, with the Strait of Hormuz essentially closed and persistent supply disruptions continuing to tighten global oil markets.

With each day that hostilities persist, the probability of temporary shipping interruptions evolving into prolonged supply shortages increases. As a result, global energy forecasts are shifting from expectations of oversupply toward the possibility of deficits.

On Tuesday, Pakistan’s prime minister expressed willingness to facilitate talks between the US and Iran aimed at ending the Gulf conflict.

This offer followed the US President’s decision on Monday to postpone attacks on Iranian power plants for five days. He reported that discussions with unnamed Iranian officials yielded ‘major points of agreement,’ which led to crude futures declining by more than ten percent.

However, Iran denied on Monday that any negotiations with the US had taken place.

In the latest incidents targeting energy infrastructure across the region, a gas company office and a pressure-reduction station in the city of Isfahan were struck, and a projectile damaged a gas pipeline supplying a power station in Khorramshahr, according to Iran’s Fars news agency.

Highlights from Day 2 of CERA week:

Kuwait Petroleum CEO Al-Sabah has stated that, should the conflict in Iran end immediately, Kuwait could restore its oil production rapidly, reaching full capacity within three to four months. He also pointed out that emergency Strategic Petroleum Reserve releases from major economies would not be able to fully compensate for the supply shortfall resulting from the ongoing hostilities.

Shell CEO Sawan has cautioned that Europe may soon face energy shortages, likely as early as next month. He emphasised that the continent will begin to experience disruptions to fuel supplies similar to those already affecting Asia due to the Iran conflict.

German Energy Minister Reiche has warned that, if the Iran war persists, Germany is likely to encounter physical supply shortages in April or May.

API President Sommers has remarked that US oil drillers are unlikely to respond to the Trump administration's call for increased crude production, given the current turmoil in the market.

ConocoPhillips CEO Lance anticipates that crude markets will shift to a contango structure and has urged the US to safeguard assets in the Middle East.

There is renewed discussion about the Keystone XL oil pipeline, as Canadian officials have spoken with representatives of the Trump administration regarding a possible revival of portions of the cancelled project.

Note: As of 4 pm EDT 24 March 2026

Currencies

EUR -0.03% to $1.1611

GBP -0.10% to $1.3410

Bitcoin -0.74% to $70,298.77

Ethereum -0.42% to $2,147.82

On Tuesday, the dollar advanced modestly as investors tempered their expectations for a swift resolution to the ongoing conflict in the Middle East. The dollar index rose +0.06% to 99.18 after having fallen to a nearly two-week low on Monday. MTD the index is +1.57%, positioning it for its strongest monthly performance since October.

With geopolitical tensions and energy market developments continuing to drive investor sentiment, participants largely disregarded data indicating that US business activity slowed to its lowest point in eleven months in March. The conflict has elevated energy and other input costs, heightening concerns that inflation may accelerate further.

The euro declined -0.03% against the dollar to $1.1611, following a +0.66% increase in the previous session.

The British pound also weakened, falling -0.10% versus the dollar to $1.3410 after surging +0.93% on Monday.

During afternoon trading, the dollar gained +0.16% against the Japanese yen, reaching ¥158.61.

Fixed Income

US 10-year Bond +1.8 basis points to 4.369%

German 10-year +2.9 basis points to 3.037%

UK 10-year gilt +9.5 basis points to 4.952%

US Treasury yields advanced on Tuesday following a lackluster auction of two-year notes, reflecting ongoing market uncertainty stemming from the conflict with Iran and persistently high oil prices.

The Treasury Department issued $69 billion in two-year notes during Tuesday’s auction. The sale recorded a bid-to-cover ratio of 2.45x, falling below the typical range of 2.50x to 2.60x. After the auction, the two-year yield climbed to a session high of 3.963% before dipping to end the day +6.7 bps to 3.927%.

Yields continued to edge higher during the morning session as hopes for a swift resolution to the Middle East crisis diminished, reigniting concerns about potential inflationary pressures.

The yield on the 10-year Treasury note rose +1.8 bps to 4.369%, though it remained below the nearly eight-month high reached on Monday. At the longer end of the curve, the 30-year yield increased +0.9 bps to 4.932%.

The yield curve, represented by the spread between two- and 10-year Treasury notes, stood at 44.2 bps, narrowing by 4.9 bps compared to Monday’s close.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing in 2.9 bps of rate hikes cuts in 2026, in contrast with the 26.4 bps of rate cuts priced in the previous week. Fed funds futures traders are now pricing in a 4.1% probability of a 25 bps rate hike at the 29th April FOMC meeting, up from 2.1% a week ago.

Short-term Bund yields continued to rise on Tuesday, as market participants grew increasingly cautious amid ongoing tensions in the Middle East, following conflicting reports regarding possible negotiations between the US and Iran.

Germany's 10-year government bond yield rose +2.9 bps to reach 3.037%. The yield had climbed to 3.077% on Monday, marking its highest level since June 2011.

Money markets have now fully priced in two interest rate hikes by the ECB by July, with the deposit facility rate expected to approach 2.75% by year-end, indicating a strong likelihood of a third rate increase. Currently, the deposit facility rate stands at 2%.

Germany’s 2-year government bond yields, more sensitive to shifts in monetary policy expectations, increased +10.4 bps to 2.680%. The previous day, these yields had reached 2.764%, the highest point since July 2024. In contrast, yields at the long end of the German curve declined, with the 30-year yield falling -1.3 bps to 3.494%.

Italy’s 10-year government bond yields advanced +7.6 bps to 3.939%, after hitting 4.119% on Monday, their highest level since July 2024.

The yield spread between Italian 10-year BTPs and Bunds widened to 90.2 bps, an increase of 4.7 bps from late Monday. The spread on French OATs stood at 71.3 bps, showing little change, down just 0.2 bps from Monday’s close.

Note: As of 4 pm EDT 24 March 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.