Will the euro stay higher for longer?

Key data to move markets today

EU: German, French, and eurozone’s HCOB Services, Manufacturing, and Composite PMIs, and speeches by Dutch Central Bank Governor Olaf Sleijpen, German Bundesbank President Joachim Nagel, ECB’s Executive Board Member Piero Cipollone, and Chief Economist Philip Lane

UK: S&P Global Services, Manufacturing and Composite PMIs

US: ADP Employment Change, Nonfarm Payrolls, Unit Labor Costs, S&P Global Services, Manufacturing and Composite PMIs, and a speech by Fed Governor Michael Barr

JAPAN: BoJ Monetary Policy Meeting Minutes

Global Macro Updates

ECB eyes April meeting as war threatens inflation and growth. The ECB is reportedly maintaining a heightened state of alert as the ongoing conflict involving Iran presents renewed inflation risks across the eurozone, according to Bloomberg news. ECB Vice President Luis de Guindos has indicated that the ECB stands prepared to take appropriate action if necessary, while emphasising that monetary policy cannot fully insulate the euro area economy from the immediate effects of war on both prices and growth. Attention is now firmly directed toward the Governing Council meeting scheduled for 29th - 30th April. Policymakers, including Bundesbank’s President Joachim Nagel and Irish Central Bank Governor Gabriel Makhlouf, have signalled that a rate hike may be considered at that meeting should inflationary pressures intensify, a sentiment reflected in market expectations, which currently price in just over two ECB rate increases throughout 2026.

Investment bank Berenberg projects eurozone GDP growth at 0.8% for this year, down from a pre-conflict forecast of 1.3%, with average inflation now estimated at 2.7%, compared to 1.8% previously. However, analyst opinions remain divided. UBS and Danske Bank advise against positioning for an imminent hike, citing the ECB’s own downward revision of growth forecasts as a reason early tightening is unlikely. While Citi shares this perspective as its base case, the firm cautions that it is extremely challenging to anticipate near-term movements at the front end.

US Stock Indices

Dow Jones Industrial Average +1.38%

Nasdaq 100 +1.22%

S&P 500 +1.15%, with all of the 11 sectors of the S&P 500 up

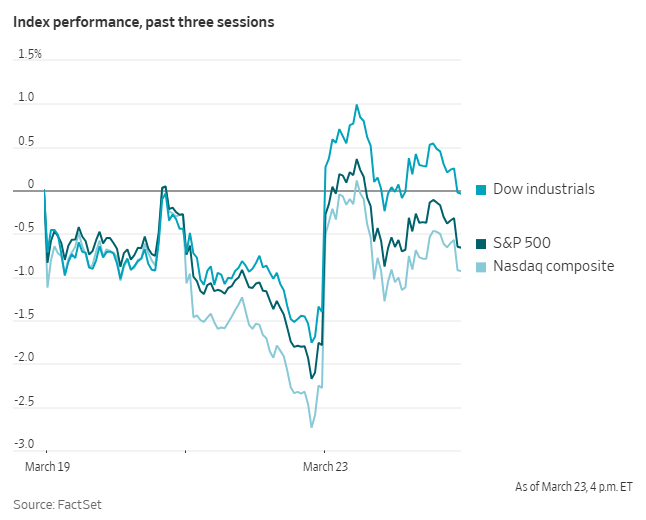

As dawn broke on Monday, financial markets faced renewed pressure: oil prices were higher, stock futures lower, and the ongoing selloff in government bonds showed little sign of respite. Then, the US President issued a statement on social media.

Shortly after 7 am ET, President Trump announced that the US military would delay planned strikes on Iranian power plants, citing ‘productive conversations regarding a complete and total resolution of our hostilities.’

The market reaction was swift and significant. On the day, the Dow Jones Industrial Average and the S&P 500 recorded their largest one-day gains since early February, with the Dow advancing +1.38% and the S&P rising +1.15%. The Nasdaq Composite gained +1.38%.

In corporate news, Apollo Global Management imposed a cap on withdrawals from its private credit fund, adhering to the stated 5% limit after redemption requests exceeded twice that amount.

The Apollo Debt Solutions BDC, a semi-liquid private credit fund targeted at high-net-worth individuals, received redemption requests totalling 11.2% of its shares for the most recent quarterly period, as disclosed in a regulatory filing on Monday.

The fund commits to repurchasing up to 5% of its shares each quarter from investors seeking liquidity; redemptions above this threshold are not guaranteed. According to The Wall Street Journal, John Zito, co-president of Apollo's asset-management division, supports maintaining the 5% limit. The company anticipates net flows to the Debt Solutions fund will remain roughly flat for the first quarter, based on the filing.

Apple has announced it will hold its annual Worldwide Developers Conference from 8-12 June, during which the company is expected to unveil a pivotal suite of artificial intelligence features.

Banks led by JPMorgan Chase have initiated an $8 billion high-yield bond sale to finance the record leveraged buyout of Electronic Arts, adjusting the debt structure of the transaction to navigate fluctuating risk appetite.

Shares of DraftKings and Flutter Entertainment climbed following reports from The Wall Street Journal that US senators are preparing to introduce bipartisan legislation to prohibit sports bets on prediction markets.

Elliott Investment Management has taken a multibillion-dollar stake in Synopsys and intends to advocate for strategic changes.

Estée Lauder is reportedly in discussions to acquire Spanish beauty conglomerate Puig Brands, a potential transaction that would unite two of the world's largest beauty companies.

S&P 500 Best performing sector

Consumer Discretionary +2.46%, with Norwegian Cruise Line +6.17%, Mohawk Industries +5.84%, and Royal Caribbean Group +5.81%

S&P 500 Worst performing sector

Health Care +0.03%, with Centene -4.62%, Molina Healthcare -2.99%, and UnitedHealth Group -2.20%

Mega Caps

Alphabet +0.08%, Amazon +2.32%, Apple +1.41%, Meta Platforms +1.75%, Microsoft +0.30%, Nvidia +1.57%, and Tesla +3.50%

Information Technology

Best performer: Palantir Technologies +6.74%

Worst performer: Enphase Energy -7.59%

Materials and Mining

Best performer: FMC +8.71%

Worst performer: CF Industries -3.78%

European Stock Indices

CAC 40 +0.79%

DAX +1.22%

FTSE 100 -0.24%

Commodities

Gold spot -1.82% to $4,405.77 an ounce

Silver spot +2.02% to $69.13 an ounce

West Texas Intermediate -9.72% to $89.21 a barrel

Brent crude -8.66% to $100.06 a barrel

Gold managed to trim its losses and recover from a four-month low on Monday, buoyed by news that the US President postponed strikes on Iranian infrastructure.

Spot gold closed down -1.82% at $4,405.77 per ounce, rebounding significantly after tumbling over 8% earlier in the session. Despite the recovery, the metal posted its worst weekly performance since 1983 last Friday. Since the Middle East conflict escalated on 28th February, spot prices have declined -16.82%, retreating -21.25% from the record peak of $5,594.82 set on 29th January.

Spot silver bucked the daily trend, rising +2.02% to $69.13. However, it remains down -26.76% overall since the onset of hostilities.

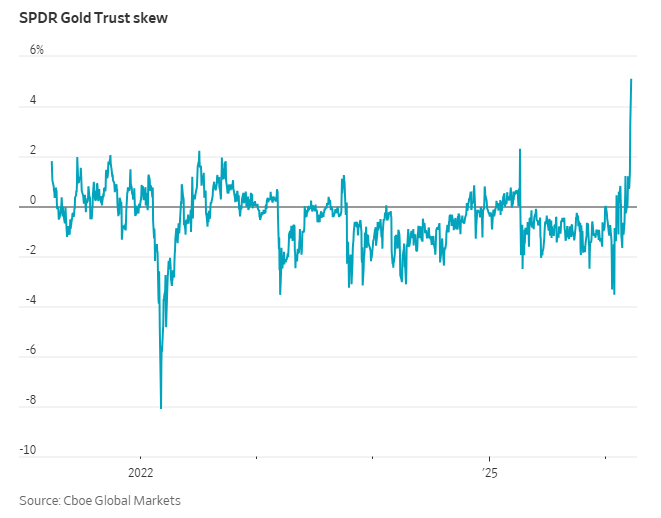

Gold options signal bearish sentiment amid Middle East tensions. Options market participants are increasingly positioning for continued declines in gold prices, as persistent geopolitical tensions in the Middle East heighten concerns about inflation.

According to data from Cboe Global Markets, the ‘skew’ for options linked to the largest gold ETF has reached its highest level since at least 2021. This elevated skew indicates that bearish put options are commanding higher premiums compared to bullish call options, reflecting a greater demand for downside protection. Put options provide the right to sell at a specified price, whereas call options grant the right to buy.

The ongoing conflict involving Iran has significantly increased the risk of stagflation, a situation in which economic growth stagnates even as inflation accelerates.

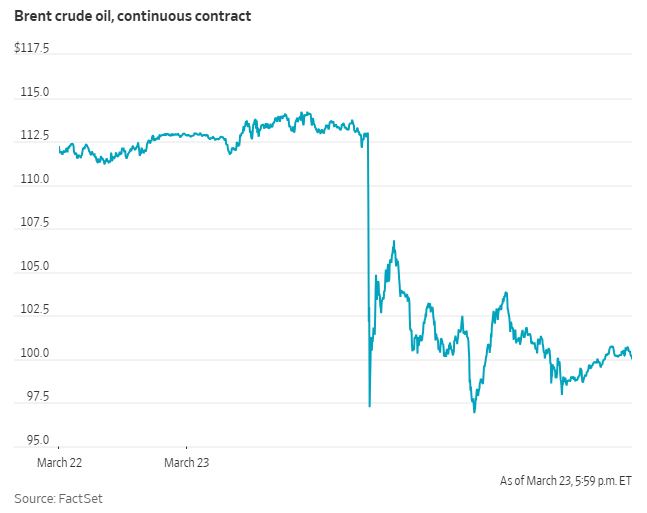

Oil prices declined sharply on Monday, following the US President's announcement of a five-day delay on military strikes against Iranian power plants, citing constructive talks to resolve hostilities just hours before a critical escalation deadline.

Brent futures fell $9.49, or -8.66% to settle at $100.06 a barrel. US WTI lost $9.60, or -9.72% to settle at $89.21.

Crude futures plunged nearly 15% earlier in the day but pared losses after Iran claimed it had launched new attacks on Israel and other regional sites, outright denying any negotiations with Washington. Furthermore, Iran's Revolutionary Guards threatened to target Israeli power plants and US bases in the Gulf if the US followed through on threats to ‘obliterate’ Iran's power network.

Extreme price swings, including Brent closing at its highest level since July 2022 last Friday, have pushed both crude benchmarks' 30-day futures volatility to their highest levels since April 2022.

The four-week war has severely damaged Gulf energy facilities and effectively halted shipping through the Strait of Hormuz, a choke point for one fifth of global oil and LNG flows. Global air travel is also severely disrupted, with key hubs like Dubai, Doha, and Abu Dhabi closed, stranding thousands of passengers.

Fatih Birol, Executive Director of the IEA, stated that the current crisis is worse than the two 1970s oil shocks combined.

The supply crunch has prompted temporary waivers on US sanctions for Russian and Iranian oil currently at sea. Indian refiners are planning to resume buying Iranian oil, with other Asian refiners exploring similar moves. However, US Energy Secretary Chris Wright noted it is highly unlikely the US will release more oil from its Strategic Petroleum Reserve.

In Russia, the Baltic Sea port of Ust-Luga resumed oil loadings after a drone alert was lifted, though the neighboring Primorsk port remains shut following airstrikes, exacerbating global shortages.

Note: As of 4 pm EDT 23 March 2026

Currencies

EUR +0.66% to $1.1614

GBP +0.93% to $1.3424

Bitcoin +0.40% to $70,820.42

Ethereum +1.10% to $2,156.96

The US dollar weakened against most major currencies on Monday as the inflationary effects of surging oil prices prompted central banks to adopt hawkish stances, bolstering other currencies.

The Dollar Index dropped -0.39% to 99.12, following Friday's close which marked the index's first weekly decline since the start of the war.

In afternoon trading, the euro rose +0.66% to $1.1614, having hit its highest level since 11th March earlier in the day. Sterling advanced +0.93% to $1.3424, its highest point since 10th March.

The dollar also weakened by -0.55% against the Japanese yen to ¥158.35, retreating from the critical ¥160 threshold that has traders on high alert for potential BoJ intervention.

Fixed Income

US 10-year Bond -3.6 basis points to 4.351%

German 10-year -4.5 basis points to 3.008%

UK 10-year gilt -8.3 basis points to 4.857%

US Treasury yields pulled back from multi-month highs early Monday. The 10-year yield declined by -3.6 bps to 4.351%, settling down after spiking to an eight-month peak of 4.445% in overnight trading and dropping to 4.305% earlier in the session.

The two-year yield fell -5.3 bps to 3.860%, stepping back from an earlier post-July high of 4.016%, while the 30-year yield declined by -2.1 bps to 4.923%.

The yield curve spread between the two-year and 10-year notes widened to 49.1 bps, up from 47.4 bps late Friday.

Additionally, on the supply side, the US Treasury auctioned $89 billion in 13-week notes and $77 billion in 26-week notes.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing in just 2.6 bps of cuts in 2026, in contrast with the 25.2 bps of rate cuts priced in the previous week. Fed funds futures traders are now pricing in a 7.2% probability of a 25 bps rate hike at the 29th April FOMC meeting, up from 0.0% a week ago.

Euro area government bond yields dropped sharply as hopes for a resolution in the Middle East eased inflation fears. Consequently, traders scaled back their bets on future ECB rate hikes, though markets still fully price in two increases by July.

Germany's 10-year government bund yield fell -4.5 bps to 3.008%, retreating from an early-session high of 3.077%, its highest since June 2011.

The two-year Schatz yield dropped -10.2 bps to 2.576% after reaching a peak of 2.764%. On the long-end of the German curve, the 30-year yield declined -2.4 bps to 3.507%.

Money markets are now pricing the ECB deposit facility rate, currently at 2%, to hit 2.50% by July, down from 2.67% earlier in the session.

Italy’s 10-year BTP yield declined by -9.8 bps to 3.863%, and its spread over German bunds tightened to 85.5 bps after an early spike to 103.60 bps. Meanwhile, the French 10-year OAT spread widened slightly by 1.5 bps to 71.5 bps.

Note: As of 4 pm EDT 23 March 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.