Should investors be spooked?

- Markets in October

- The economic picture

- Global market indices

- Commodity sector news

- Currencies

- Cryptocurrencies

- Fixed Income

- What to think about in November

- Key events in November

Markets in October

Equities markets have been slightly mixed in October as investors focused on corporate earnings. The S&P 500 is +0.89% MTD, the Dow is up -0.23% MTD, while the Nasdaq 100 is +2.44% MTD. The NYSE is -0.51% MTD.

European equity markets were largely down in October on weak earnings data, with the STOXX 600 poised to drop for a second month. Markets appear concerned that sluggish economic growth could reflect in corporate performance this quarter.

In the bond market, yields have surged in the US, UK and in Europe in reaction to concerns about the increasing likelihood of a Republican sweep, which means a return to a Trump presidency with Republican majorities in the Senate and House, with the spectre of tariffs and rising inflation this brings. The potential higher budget deficits from suggested tax cuts and possible expansionary fiscal policies, would likely result in higher real interest rates moving forward. In addition, the stronger-than-expected US macroeconomic data which implies fewer cuts, along with statements by Fed policymakers suggesting a higher terminal rate, has increased the chances of a bond sell-off. These factors led to extreme volatility in bond markets in October with the MOVE index hitting a one-year high on 7 October 2024.

The Economic Picture

The US labour market appears to be sending some conflicting signals with the September JOLTS report indicating a significant drop in job openings, falling to 7.443 million, marking the lowest level since March 2021. This represents a substantial 1.9 million decrease y/o/y. The number of lay-offs edged slightly higher to 1.2% or 1.8 million while the quits rate remained relatively stable at 1.9% or 3.1 million. However, ADP private job growth pointed to a solid demand for labour and was up to its highest in over a year, increasing by 233,000 in October with September revised higher. Traders will be looking to September's total nonfarm payroll, average hourly earnings and employment data on Friday for further indications of the possible depth and pace of future Fed rate cuts.The consensus forecast for Friday's nonfarm payrolls report is 120,000 jobs added, less than half of September's 254,000 figure. On the growth front the flash Composite PMI in October increased to 54.30 points in October from 54 points in September. The Flash US Services Business Activity Index came in at 55.3, up slightly from September’s 55.2. The US economy is still showing solid strength. GDP increased at a 2.8% annualised rate in Q3 after rising 3% in the previous quarter. Consumer spending, which comprises the largest share of economic activity, advanced 3.7%, the most since early 2023. The acceleration was led by broad based spending increases including autos, household furnishings and recreational items. The personal consumption expenditures price index, excluding the volatile food and energy components was 2.2%, down from the 2.8% pace in the second quarter. Nevertheless, US consumers are feeling more confident. The Conference Board's consumer confidence index increased in October to 108.7, surpassing the consensus forecast of 99.4 and up from September’s revised reading of 99.2. This marks the strongest monthly gain since March 2021 and the highest overall level since August 2023. The Present Situation Index—based on consumers’ assessment of current business and labour market conditions—increased by 14.2 points to 138.0. The Expectations Index—based on consumers’ short-term outlook for income, business, and labour market conditions—increased by 6.3 points to 89.1, well above the threshold of 80 that usually signals a recession ahead.

In the eurozone inflation fell to 1.7% in September 2024, down from 2.2% in August. Core inflation - excluding volatile items such as food, energy, alcohol, and tobacco -fell to a five-month low of 2.7% in September, down from 2.8% in August. Services inflation fell slightly to 3.9% from August’s 4.2%. On the growth front, the eurozone HCOB flash Composite PMI came in at 49.7, a slight nudge above September’s 49.6. However, the HCOB Flash Eurozone Services PMI Business Activity Index came in at 51.2, down from September’s 51.4 and an 8-month low. Growth in the eurozone came in at 0.4% in Q3, above expectations of a 0.2% rate. However, industry remained in recession and household consumption barely grew. This higher than expected growth might support arguments to maintain a gradual pace of easing moving forward.

In the UK inflationary pressures continued to fall with the headline rate in September coming in at 1.7% year-on-year, down from August’s 2.2%. Core inflation measured 3.2%, while services inflation remained elevated, although down to 4.9% from August’s 5.6%. However, consumer confidence fell again in October to -21, down one point from September. The index measuring changes in personal finances over the past year was down one point at -10, while the outlook for the next 12 months was up one point at -2. According to the UK’s Office of National Statistics (ONS), average earnings excluding bonuses rose 4.9% in the three months through August from a year earlier. Private sector wage growth slowed to 4.8% from 5%. The UK's unemployment rate fell to 4% in the latest three months, however vacancies fell by 32,000 to 841,000 in the three months through September, the lowest since the spring of 2021. However, on the growth front the UK appears to be struggling. October data pointed to a moderate increase in UK private sector output, but the rate of expansion slowed for the second month running to its lowest since November 2023. The composite PMI fell to 51.7, down from 52.6 in September. This was an 11-month low. The services PMI business activity index fell to 51.8, down from 52.4 in September, also an 11-month low. The Flash UK Manufacturing PMI came in at 50.3, down from September’s 51.5 and a 6-month low. Real GDP is estimated to have grown by 0.2% in the three months to August 2024 compared with the three months to May 2024. Services output was the main contributor to the growth in the three months to August, rising by 0.1%. Gross domestic product is estimated to have grown by 0.2% in August 2024, after showing no growth in July 2024. The Office for Budget Responsibility (OBR) has now forecast that real GDP growth will be 1.1% this year from close to zero last year, 2.0% in 2025, and 1.8% in 2026, and then fall back to around 1.5% thereafter. However, as the government has extended the freeze on personal tax thresholds during the budget announced yesterday, this fiscal drag might continue to slow the economy down. The rise in employer national insurance contributions and the lowering of the threshold from which they will be applied is also expected to be a drag on growth moving forward.

US:

S&P 500 +0.89% QTD and +21.88% YTD

Nasdaq 100 +1.63% QTD and +22.14% YTD

Dow Jones Industrial Average -0.45% QTD and +12.06% YTD

NYSE Composite -0.51% QTD and +15.21% YTD

The Equally Weighted version of the S&P 500 posted a -0.63% decrease this month, its performance is +12.82% YTD, 9.06 percentage points lower than the benchmark.

The S&P 500 Financials sector is the top performer this month at +3.82% MTD, and +25.01% YTD, while Health Care is -3.95% MTD, and +8.50% YTD.

US stock indexes experienced a moderate decline on Wednesday, with the Nasdaq Composite retreating by 0.6% a day after achieving a new record high. The S&P 500 shed 0.3%, while the Dow Jones Industrial Average edged down 0.2%.

Despite this slight downturn, several factors suggest a potential market rally may be on the horizon. Historically, stocks tend to perform well during this season, and companies are poised to resume share buybacks. Furthermore, investors may have implemented excessive hedging strategies in anticipation of earnings reports, the US election, and central bank announcements, potentially creating an opportunity for a market rebound. As market volatility subsides from its early-August peak, systematic investors and options desks may be compelled to increase their equity holdings.

Adding to the positive outlook, mutual funds, typically the largest sellers of stocks, have reduced their selling activity towards the end of the month. This trend is expected to reverse in November, with equities traditionally experiencing inflows. Simultaneously, the window for corporate share buybacks is reopening, with estimates suggesting daily purchases could reach $6 billion throughout November.

In other market developments, companies planning to go public in the US this year appear to have abandoned the customary post-Labor Day window, dampening expectations for a surge of initial public offerings before the presidential election. Data compiled by Bloomberg reveals that proceeds from inaugural share sales have totaled $7.7 billion since 2nd September.

In corporate news, chipmaker AMD issued disappointing revenue guidance, causing its stock to fall by 11% and impacting other semiconductor stocks like Qualcomm. Super Micro Computer shares experienced a significant decline of 33% following the server maker's disclosure that Ernst & Young had resigned as its auditor, citing concerns about management representations.

On a positive note, DoorDash exceeded Wall Street's expectations across virtually all key earnings metrics, enabling the delivery service to report its first operating profit since the onset of the pandemic. Humana also presented a more optimistic forecast for 2024 after its Q3 profit surpassed expectations, contrasting with the challenges faced by larger peers in managing medical costs.

In the entertainment sector, Walt Disney secured a 10-year deal to broadcast the annual Grammy music awards, wresting the show from its long-held position on Paramount Global's CBS.

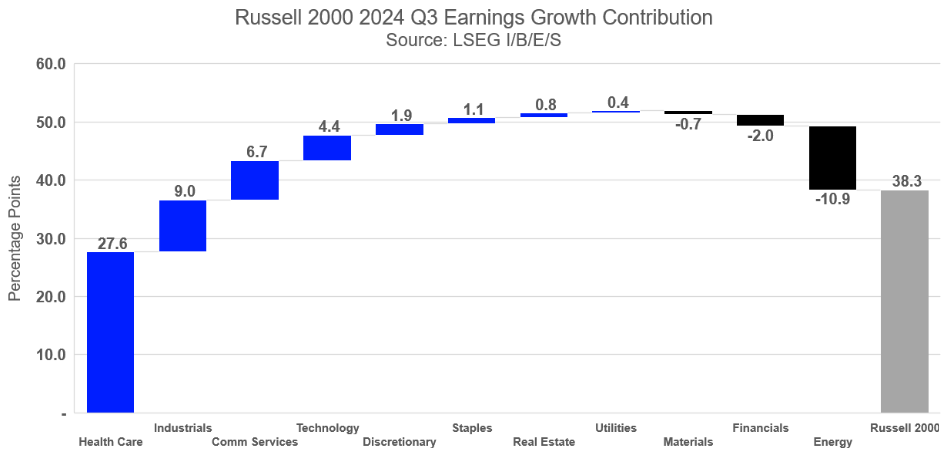

Russell 2000 Q3 earnings outlook. Analyst estimates suggest a positive outlook for the Russell 2000's earnings growth, following its emergence from an earnings recession earlier this year.

Despite a reported 38.3% earnings growth for Q3, coupled with a 1.1% revenue growth, it is crucial to acknowledge the influence of the Healthcare sector. Excluding Healthcare, the earnings growth for the Russell 2000 falls considerably to 6.2%. This disparity arises from favourable y/o/y comparisons within the Healthcare sector, where earnings, although remaining negative at -$6.3 billion, have improved from -$10.2 billion the previous year.

Further emphasising the reliance on Healthcare's contribution is the modest q/o/q growth observed for the index as a whole. Earnings rose by 1.5%, accompanied by a marginal 0.1% increase in revenue.

Notably, all sectors, with the exception of Healthcare, have undergone downward revisions in their earnings growth forecasts over the past three months. Energy, Communication Services, and Materials sectors have been particularly impacted, experiencing the most substantial reductions.

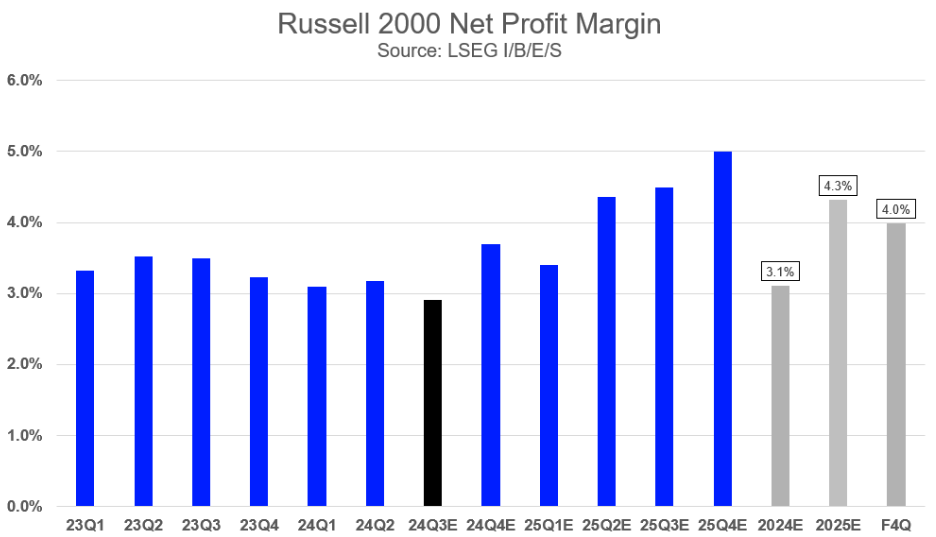

While net profit margins at the index level have declined in recent quarters, analysts anticipate a rebound later this year, with Q3 net margin estimates currently at 2.9%.

LSEG I/B/E/S data reveals that an estimated 28.8% of Russell 2000 constituents are projected to report negative earnings in 2024. However, this figure significantly improves to 16.9% when the Healthcare sector is excluded. Projections for 2025 indicate further improvement, with negative earnings expected to decrease to 23.4% overall and 11.5% excluding Healthcare, suggesting a gradual earnings recovery across the index.

Analyst estimates anticipate a resurgence in earnings in the coming quarters, with Q4 earnings projected to reach $22.9 billion, an all-time high since the inception of the Russell 2000 Earnings Scorecard. Furthermore, full-year earnings growth for 2024 and 2025 is estimated at 26.2% and 44.2%, respectively. It is worth noting that while the forward four-quarter price-to-earnings ratio stands at 25.9x, this figure drops to 16.3x when Healthcare is excluded.

As of 24th October, forecasts the Russell 2000 Q3 blended earnings at $19.2 billion, representing a 38.3% y/o/y increase (1.5% q/o/q increase). Revenue is projected at $462.1 billion, reflecting a 1.1% y/o/y growth and (0.1% q/o/q growth).

Excluding Healthcare, y/o/y earnings growth declines sharply to 6.2%, marking the first quarter of positive growth outside of Healthcare since 2023.

At the constituent level, Cargo Therapeutics is anticipated to be the primary contributor to earnings growth within the Healthcare sector, benefiting from a more favourable y/o/y comparison. CleanSpark and Diebold Nixdorf are expected to lead in Information Technology, while Clear Channel Outdoor Holdings is projected to stand out in Communication Services.

LSEG I/B/E/S Russell 2000 earnings estimates employ a share-weighted methodology. For the fifth consecutive quarter, Financials retain the largest earnings weight at 42.0%, notably surpassing its market-cap weight of 18.3%.

The Consumer Discretionary sector also presents a significant contrast between market-cap and earnings weights. With an earnings weight of 19.9% compared to a market-cap weight of 9.7%, the sector is poised to outperform relative to its market capitalization. This suggests that the sector is generating substantial earnings relative to its size within the index.

In contrast, the Information Technology sector demonstrates a negative differential in both earnings and revenue weight relative to its market capitalization, while its market cap weight within the Russell 200 index stands at 12.6%, its earnings contribution to the index is 9.2%.

The estimated Q3 blended net profit margin has gradually declined over the past three months, decreasing by 0.70 percentage points (pps) to its current value of 2.9%. During this period, eight sectors experienced a decline in their net margin estimates. Energy faced the most significant reduction in margin expectations (-3.54 pps, current value: 2.0%), followed by Real Estate (-1.12 pps, 1.4%) and Communication Services (-0.94 pps, 0.0%).

Current estimates for the Russell 2000’s net margin full year 2024 and 2025 stand at 3.1% and 4.3%, respectively, while the forward four-quarter estimate is 4.0%.

Europe:

Stoxx 600 -2.18% QTD and +6.79% YTD

DAX -0.35% QTD and +14.96% YTD

CAC 40 -2.72% QTD and -1.52% YTD

FTSE 100 -0.94% QTD and +5.51% YTD

IBEX 35 -1.37% QTD and +15.97% YTD

FTSE MIB +1.11% QTD and +13.68% YTD

In Europe, the Equally Weighted version of the Stoxx 600 is -2.83% in October, and its performance is +5.03% YTD, 1.70 percentage points below the benchmark.

The Stoxx Europe 600 Travel & Leisure is the leading sector this month, up +2.99% MTD +7.41% YTD, while Chemicals has exhibited the weakest performance at -6.14% MTD and -2.96% YTD.

STOXX 600 Earnings Q2 2024

Global:

MSCI World Index -0.45% QTD and +16.95% YTD

Hang Seng -3.56% QTD and +19.55% YTD

Mega cap stocks had a mostly positive performance in October with 5 of the Magnificent Seven members recorded gains, as Alphabet +5.19%, Amazon +3.43%, Apple -1.24%, Meta Platforms +3.38%, Microsoft +0.52%, Nvidia +14.74%, and Tesla -1.56%.

Microsoft Q3 earnings. Microsoft shares experienced a postmarket surge of approximately 1.1% following the technology giant's release of its latest financial results, which surpassed analyst expectations for both revenue and profit.

Key highlights from the report include a 33% y/o/y increase in revenue for Azure, Microsoft's cloud computing platform and a cornerstone of its artificial intelligence offerings. This robust growth in Azure contributed to a 16% rise in overall revenue, reaching $65.6 billion, while net income climbed 11% to $24.7 billion. These figures exceeded analyst projections, which had anticipated revenue of $64.57 billion and net income of $23.15 billion.

Meta Platforms Q3 earnings. Meta Platforms shares experienced a modest decline of 1% in after-hours trading as investors assessed the social media giant's Q3 financial results.

Despite a deceleration in digital advertising growth, the company achieved record revenue for the quarter, reaching $40.59 billion.This represents a 19% increase compared to the same period last year and slightly exceeded Wall Street expectations. The robust revenue performance bolstered profits, enabling continued investment in artificial intelligence and augmented reality initiatives.

Looking ahead, Meta Platforms projects Q4 revenue to fall between $45 billion and $48 billion, compared to analysts' consensus estimate of $46.12 billion. Furthermore, the company revised its CapEx forecast for 2024, raising the lower end of the range to $38 billion from $37 billion. The upper end of the forecast remains at $40 billion.

Energy stocks have experienced a slightly positive performance this month, with the Energy sector +0.05% so far in October and +5.74% YTD due to economic data signalling softening demand in China and subdued demand in the US compared to previous years, as well as easing tensions in the Middle East. Energy Fuels +18.44%, and Baker Hughes Company +3.71%, Shell +2.70%, and Chevron +0.53%, while Marathon Petroleum -11.14%, Phillips 66 -7.14%, Halliburton -4.68%, Apa Corp -4.05%, ConocoPhillips -2.18%, and ExxonMobil -0.45%.

Materials and Mining stocks had a negative performance this month. The Materials sector is -2.06% so far in October and +10.30% YTD. Gold reached new highs in October and is +5.78% MTD +35.21% YTD, while copper prices fell by -3.75% MTD. Sibanye Stillwater +21.85%, Mosaic +1.46%, Albemarle +0.86%, Yara International +0.21%, while Newmont Mining -12.18%, Freeport-McMoRan -7.91%, Celanese Corporation -6.58%, and Nucor Corporation -5.08%.

Commodities

Oil prices had a volatile October with WTI -2.30% MTD and Brent +1.27% MTD. This price volatility was primarily driven by market anxieties surrounding potential supply disruptions, coupled with the recent easing of concerns regarding a broader escalation of the conflict in the Middle East.

Gold has rallied this year, surging +35.21% YTD, marking its best performance since 1979. Gold prices increased by 0.45% on Wednesday settling at $2,786.90 after reaching an all-time high of $2,789.73 earlier in the session. According to the World Gold Council, total gold demand gained 5% y/o/y to 1,313 tonnes – a record for a third quarter. Total demand exceeded $100 bn for the first time on record. This strength was reflected in the gold price, which reached a series of new record highs in October on expectations of further rate cuts by the Fed and other major global banks, on rising geopolitical concerns around the conflicts in the Middle East and Ukraine, on the uncertainty surrounding the US election, and as central banks diversified away from the US.

Oil prices experienced a rebound on Wednesday, rising over 2% following reports of unexpected declines in US crude and gasoline inventories last week, coupled with indications that OPEC+ may defer a planned increase in oil output.

Brent crude futures, which had previously declined by more than 6% earlier in the week due to a perceived reduction in the risk of a broader Middle East conflict, settled at $73.03 per barrel, marking an increase of $1.61 or +2.25%. Similarly, WTI crude rose by $1.56, or +2.31%, to reach $69.03 per barrel.

Furthermore, Reuters reported that OPEC+ may consider delaying a planned oil production increase scheduled for December. This potential delay, which could be by a month or more, stems from concerns over weak oil demand and rising supply.

Currently, the group is slated to increase output by 180,000 barrels per day (bpd) in December. It is noteworthy that OPEC+ has previously implemented production cuts totaling 5.86 million bpd, equivalent to approximately 5.7% of global oil demand. According to sources within OPEC+, a decision to postpone the planned increase could be reached as early as next week. OPEC+ is scheduled to meet on 1st December to decide its next policy steps.

EIA report reveals surprising decline in US oil inventories despite reduced refinery runs. In the week ending 25th October, the Energy Information Administration (EIA) reported an unexpected decline in US gasoline stockpiles, reaching a two-year low of 210.9 million barrels. This reduction of 2.7 million barrels was driven by a surge in demand, with gasoline supplied climbing to 9.2 million barrels per day (bpd), the highest level observed since early October.

Contrary to expectations, crude oil inventories also experienced a drawdown of 515,000 barrels, settling at 425.5 million barrels. This decline can be attributed to a decrease in net US crude imports, which fell by 605,000 bpd to 1.7 million bpd, coupled with a slight increase in exports. Notably, crude imports from Saudi Arabia plummeted to their lowest point since January 2021, reaching a mere 13,000 bpd. Imports from Canada, Iraq, Colombia, and Brazil also experienced weekly declines.

Despite the heightened demand for gasoline, refinery crude runs decreased by 31,000 bpd, resulting in a 0.4 percentage point reduction in refinery utilisation rates to 89.1% of total capacity. Distillate stockpiles, encompassing diesel and heating oil, also decreased by 1 million barrels, reaching 112.9 million barrels.

Petroleum products supplied, a proxy for demand, rose to its highest level last week since November 2023.

Currencies

The dollar continued to strengthen in October. The dollar index has risen over the month; it is +3.23% MTD +2.66% YTD.

The GBP is -3.12% MTD and +1.78% YTD against the USD. The EUR is -2.50% MTD and -1.61% YTD against the USD.

The US dollar weakened against other major currencies on Wednesday, amidst volatile trading triggered by stronger-than-anticipated US economic data and the release of the UK budget. The ADP National Employment Report revealed a surge in US private payroll growth in October, exceeding expectations and assuaging fears of temporary disruptions caused by hurricanes and strikes. Concurrently, separate data indicated that US GDP grew at an annualised rate of 2.8% in Q3, slightly below the 3% consensus forecast.

The US dollar index, which had risen to 104.43 earlier in the session, subsequently declined by +0.11% to 104.10. This followed a recent peak of 104.63 on Tuesday, its highest point since 30th July.

Sterling fell on Wednesday, falling as much as -0.60% following the delivery of the Labour government's first budget by Chancellor of the Exchequer Rachel Reeves. It ultimately settled at $1.2956, down -0.45%. This budget, the first from the Labour party in 14 years, ended months of speculation regarding the extent of borrowing for infrastructure investment under Reeves and Prime Minister Keir Starmer, and the potential impact on taxpayers.

Gilt yields initially dipped during Reeves' budget presentation but later rebounded. The yield on the 10-year UK government bond rose by +4.2 bps to 4.362%, reaching its highest level since late May as the increase in borrowing and taxes pushed back bets of rate cuts by the BoE.

The euro strengthened against the dollar, rising +0.34% to $1.0857. It was +0.46% against the pound to 83.51 pence, bolstered by a surge in eurozone bond yields. This surge was prompted by stronger-than-expected German growth and regional inflation data, leading traders to reassess their expectations of a significant rate cut by the ECB in December. The eurozone economy expanded by 0.4% in Q3, exceeding economists' projections of 0.2%.

The dollar remained stable against the yen at ¥153.28. Japan's Finance Minister Katsunobu Kato reiterated the government's commitment to closely monitor foreign exchange movements, particularly those influenced by speculative activity.

Measures of anticipated volatility in Sterling increased significantly on Wednesday as investors prepared for the US election on 5th November. The election outcome carries considerable uncertainty and could potentially lead to substantial shifts in trade policy and fluctuations in the dollar.

One-week implied options volatility for the British pound, reflecting the demand for protection against significant currency movements, reached 10.66%, its highest point since March 2023. This represented a substantial overnight increase from 6.33% and marked the largest one-day rise since September 2022, when then-Prime Minister Liz Truss's budget proposals triggered a crisis in UK markets.

Similarly, implied volatility on one-week options for the euro also surged, indicating investor apprehension surrounding the US election and its potential ramifications.

Cryptocurrencies

Bitcoin +14.33% MTD and +72.07% YTD

Ethereum +2.27% MTD and +15.51% YTD

Cryptocurrencies have been on the rise this month as crypto investors look forward to a US election where both candidates appear to be more crypt friendly. Donald Trump has promised to be a “crypto president” while Kamala Harris promised to promote digital asset innovation and protect crypto investors.

Bitcoin was +8.37% on Wednesday to $72,265.00 while Etherium was +5.23% to $2653.40. Bitcoin has also been helped by a rise in daily net inflows into Spot Bitcoin ETFs. BlackRock’s IBIT added $643 million added on Tuesday, contributing to a total of $870 million in daily net inflows — the largest since June and third-largest to date. There are also reports of short-term borrowing rates on institutional crypto lending markets rising as we get closer to the US election.

Note: As of 6:00 pm EDT 30 October 2024

Fixed Income

US 10-year yield +54.9 basis points QTD +42.2 basis points YTD to 4.303%.

German 10-year yield +26.1 basis points QTD +38.7 basis points YTD to 2.396%.

UK 10-year yield +38.3 basis points QTD +82.3 basis points YTD to 4.362%.

US Treasury 10-year bond yields are +42.2 basis points (bps) YTD and +54.9 bps over the past month.

The CME's FedWatch Tool gives a 95.5% probability of a 25 bps cut at the Fed’s 7th November meeting. Swap traders are pricing in a total of about 42.5 bps worth of reductions for the year. However, traders will be looking closely at Friday’s PCE data for further indications of the Fed’s future rate cut policy.

The benchmark German 10-year yield is +26.1 bps in October at 2.396%, while the UK 10-year yield is +38.3 bps at 4.362%. The spread between US 10-year Treasuries and German Bunds increased by 28.8 bps from 161.9 in September to 190.7 bps now.

Italian bond yields, a benchmark for the eurozone periphery, are +17.0 bps this month to 3.629%. Consequently, the spread between Italian and German 10-year yields narrowed by 3.9 bps to 123.3 from 127.2 bps in September.

US Treasury yields experienced mixed movements on Wednesday, with the 10-year yield retracing an earlier decline and shorter-dated yields advancing, fueled by robust economic data preceding Friday's October jobs report. The ADP National Employment Report revealed a notable increase of 233,000 private payroll jobs in October, following an upwardly revised 159,000 gain in September.

This positive employment data aligns with the sustained economic growth observed in Q3, where the US GDP expanded at an annualised rate of 2.8%. Ebbing inflation and robust wage growth have bolstered consumer spending, contributing to this economic performance. The strong economic indicators, including September's better-than-expected jobs report, have fueled market expectations that the Fed will pursue a moderate pace of monetary easing, driving yields higher this month.

The 10-year Treasury yield ultimately settled at 4.303%, a +4.4 bps increase, after reaching a near four-month high of 4.339% on Tuesday. Similarly, the two-year yield was +3.5 bps to 4.154%, having reached its highest level since 1st August at 4.179% on Tuesday.

In line with market expectations, the US Treasury Department announced its intention to maintain the sizes of its coupon-bearing auctions in the upcoming quarter.

Across the Atlantic, shorter-dated eurozone bond yields surged on Wednesday, responding to a series of better-than-expected economic data releases with GDP growing by 0.4 percent in Q3, marking an improvement from the 0.2 percent growth seen in the previous quarter. However, the eurozone's economic outlook remains clouded by potential risks, such as the possibility of increased tariffs under a Republican US presidency. Germany, the region's largest economy, defied recessionary pressures with GDP coming in at +0.2% in Q3 from Q2. German inflation came in at 2.4% from 1.8% in September. Furthermore, preliminary data indicated stronger-than-anticipated economic growth in France, attributed to the impact of the Paris Olympic Games, and Spanish inflation aligned with consensus forecasts.

These positive economic indicators prompted money markets to reassess the likelihood of substantial easing measures from the ECB in December. While a quarter-point rate cut remains fully priced in, the probability of a larger 50 bps cut diminished to approximately 24%, down from around 45% prior to the data releases. Reflecting these shifting expectations, Germany's two-year yield, sensitive to interest rate movements, reached a three-week high of 2.282%, ultimately closing +10 bps higher at 2.271%.

Reinforcing this sentiment, ECB board member Isabel Schnabel acknowledged the recent string of positive economic reports and countered calls for ultra-easy monetary policy. Germany's 10-year yield also climbed, reaching a three-month high before closing at 2.396%, up +6 basis points.

In the UK, Chancellor of the Exchequer Rachel Reeves, presented her inaugural budget, featuring the most substantial tax increases in three decades and outlining a strategy for increased borrowing to support long-term investment. The budget proposal projected an increase in government borrowing of nearly £142 billion over the next five years compared to previous estimates. Consequently, British gilt yields rose across the curve, with the 10-year gilt yield reversing an earlier decline to close at 4.362%, up +4.2 bps. Two-year UK gilt yields also increased by +6 bps to 4.32%, reflecting market anticipation of a more gradual pace of rate cuts by the Bank of England.

Italy's 10-year yield reached an eight-week high of 3.639%, closing at 3.633%, up +6.9 bps. This followed a successful Italian treasury auction, where the maximum planned amount of €9 billion was sold.

Note: Data as of 6:00 pm EDT 30 October 2024

What to think about in November 2024

US elections and global geopolitical risks rising. The US election on 5 November poses risks not just for the citizens of the US but also for its trading partners around the world.

The performance of Emerging Markets (EM) will be significantly influenced by the new administration's trade policy. In the absence of headwinds from escalating tariffs, EM currencies should benefit from a more balanced global growth outlook and accommodative monetary policy by the Fed. Similarly, EM equities are poised to benefit from several supportive factors, including a non-recessionary global growth environment, easing monetary policies by central banks, robust earnings growth, and attractive valuations.

In the event of a comprehensive victory by the Republican party, the potential for increased tariffs and heightened trade tensions could lead to a strengthening of the US dollar, presenting challenges for EM assets. The precise impact, however, would be contingent on the scope of tariff implementation, specifically whether they are applied universally across all trading partners or targeted primarily at China.

Within emerging market currencies, the Chinese Yuan (CNH) would be most directly impacted. Beyond China, the South African Rand (ZAR) and South Korean Won (KRW) exhibit significant vulnerability to US tariff risks. The Taiwanese Dollar (TWD), Thai Baht (THB), and Malaysian Ringgit (MYR) are highly sensitive to fluctuations in the USD/CNH exchange rate. Additionally, the Mexican Peso (MXN), with its high beta to risk sentiment, remains susceptible to deterioration in global risk appetite, even if the US-Mexico trade relationship remains stable.

Within EM equities, North Asian markets (Taiwan and Korea), Mexico, and, to a lesser extent, Brazil appear most exposed to the imposition of higher tariffs. Conversely, equities in India, the Middle East and North Africa (MENA) region, and the CEE-3 (Czech Republic, Hungary, Poland) appear relatively insulated from such trade actions.

For EM assets, in the event of a divided Congress, trade policy would likely resemble that observed under a scenario of unified Republican governance, given the President's considerable independent authority on numerous trade-related matters. However, the scope of tariff increases may be more constrained under divided government, as certain tariff proposals may necessitate legislative approval. This constraint would serve to reduce the probability of extreme, or left tail outcomes characterised by extensive tariff escalation.

The likely preservation of the status quo under a Democrat administration suggests that significant changes to trade policy would be minimal. This outcome would provide a degree of relief to those emerging market currencies and equities most susceptible to tariff-related risks.

Key events in November 2024

The potential policy and geopolitical risks for investors that could negatively affect corporate earnings, stock market performance, currency valuations, sovereign and corporate bond markets and cryptocurrencies include:

5 November US Election. Current Democratic Vice-President Kamala Harris is facing former Republican president Donald Trump. Opinion polls have indicated that they remain virtually tied, including within the “swing” states, with any differentials within the margin of error. The election is likely to be contested in numerous states if the vote is as close as polls are indicating. All 435 seats in the House of Representatives (lower house) and 34 of 100 seats in the Senate (upper house) are also on the ballot. In addition, eleven states will be voting for their governors.

6-7 November US Federal Reserve Monetary Policy Meeting. With inflation having fallen substantially from peak levels and the US economy remaining strong, the Fed is under less pressure to cut rates significantly. However, much will depend on what Friday’s NFP numbers are in order to get a clearer picture of the actual softness in the labour market. Markets are expecting a 25 bps cut at this meeting but job creation weakness might also support further interest rate cuts from Fed in December.

7 November Bank of England Monetary Policy Meeting. The BoE is widely expected to cut rates again during this meeting by 25 bps but further rate cuts may be delayed given the expected increase in borrowing laid out by the Chancellor of the Exchequer during her presentation of the budget on 30 October.

10-16 November Asia-Pacific Economic Cooperation (APEC) Summit 2024, Lima, Peru. APEC Economic Leaders’ Week will bring together heads of state and government officials from member countries to discuss trade, investment, digitalization and sustainable growth.

11-29 November 29th COP Climate Conference, Baku, Azerbaijan. Delegates including heads of state, climate experts and negotiators will meet to try to agree coordinated action to tackle climate change – key negotiations will focus on building momentum on the progress made at COP28. Azerbaijan has been criticised for its potential conflict of interest given the country relied on oil and gas for more than 92.5% of its export revenue last year. Azerbaijan also reportedly has plans to expand its fossil fuel industry.

18-19 November G20 Leaders’ summit, Rio de Janiero, Brazil. Brazil will host the G20 leaders’ summit with the presence of the leaders of the 19 member countries, plus the African Union and the European Union. Brazil has put three main agenda priorities for the G20 dialogue in 2024: social inclusion and the fight against hunger, energy transition and sustainable development in its social, economic and environmental aspects, and reform of the global governance institutions.

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.