What’s the impact of central banks’ divergence?

Key data to move markets today

EU: Italian CPI, German ZEW Surveys on Current Situation and Economic Sentiment and Eurozone ZEW Survey on Economic Sentiment and speeches by Bank of Spain Governor José Luis Escrivá, Dutch Central Bank President Olaf Sleijpen and ECB Chief Economist Philip Lane

US: ADP Employment Change 4-week Average, Building Permits and Housing Starts

JAPAN: BoJ Press Conference, Adjusted Merchandise Trade Balance, Exports and Imports

CHINA: Industrial Production and Retail Sales

Global Macro Updates

BoJ raises OCR and leaves JGB outlook unchanged. The BoJ raised its policy rate as widely expected and did not provide any new indication of further reductions in Japanese Government Bond purchases from April next year.

The central bank increased the unsecured Overnight Call Rate (OCR) by 25 bps to 1.00%, in line with market expectations. The decision was approved by a 7 – 1 vote, with board member Asada dissenting on the view that downside risks to production and employment outweighed upside risks to inflation.

In its policy statement, the BoJ acknowledged headwinds stemming from developments in the Middle East, while noting that the impact of higher oil prices had been offset by strong corporate profits and continued improvement in employment and income conditions. It also indicated that the risk of a significant economic slowdown had diminished, largely because of government support measures and progress in securing alternative supply chains to reduce reliance on the region. At the same time, the statement suggested that inflationary pressures were spreading more rapidly, raising the possibility that underlying inflation could exceed the 2 percent target. The bank further noted that financial conditions remained accommodative and that real interest rates were still negative.

The BoJ guidance reaffirmed that further rate increases would be considered in response to economic and financial developments. It stated that the timing and pace of any future adjustments would be assessed carefully while the effects of conditions in the Middle East continued to be monitored, although the overall guidance was little changed from previous communications.

With regard to Japanese Government Bond (JGB) purchases, the decision confirmed that no interim changes would be made through March 2027, leaving monthly purchases at approximately ¥2 trillion from April 2027. The statement did not set out any specific path for future tapering, implying that the scheduled reductions had come to an end. The bank also reiterated that it would respond flexibly if long-term yields were to rise rapidly and added that there would be no further interim assessments, with any necessary revisions to be decided at future Monetary Policy Meetings.

US data signals softer growth. US macroeconomic data released on Monday painted a mixed picture, with manufacturing activity softening in New York even as labour conditions remained resilient and price pressures stayed elevated.

The June Empire State Manufacturing Index fell to 5.7, below consensus expectations of 12.6 and down from 19.6 in May, marking its lowest reading since March 2026 while remaining in expansionary territory for a third consecutive month. Within the survey, new orders slowed to 3.5 from 22.7, shipments eased to 8.6 from 18.9 and inventories fell to 0.0 from 9.7, indicating a moderation in near-term demand and output.

Even so, employment expanded for a fifth consecutive month, and the average workweek also lengthened. The employment index rose to 9.6 from 8.3, suggesting that labour market conditions in the sector remained comparatively firm. Inflation indicators eased only marginally. The prices paid index slipped to 61.0 from 62.6, while the prices received index edged down to 31.4 from 31.8, pointing to continued cost pressures despite a modest retreat.

Looking ahead, the outlook remained broadly constructive. Forty-four percent of firms expect activity to increase over the next six months, with respondents anticipating stronger new orders and shipments, continued hiring and tighter supply conditions. Price expectations also rose sharply, with the future selling price index reaching its highest level since 2022.

Elsewhere, US industrial production rose 0.1% m/o/m in May, below the 0.3% increase expected by consensus and down from April’s revised 0.9% gain. Capacity utilisation was unchanged from expectations at 76.2%, compared with 76.1% in April.

Housing data also remained soft. The NAHB Housing Market Index came in at 35 in June, below consensus expectations of 37 and unchanged from the prior month. The survey further showed that 35% of builders cut prices in June, up from 32% in May, underscoring persistent pressure on the residential construction sector.

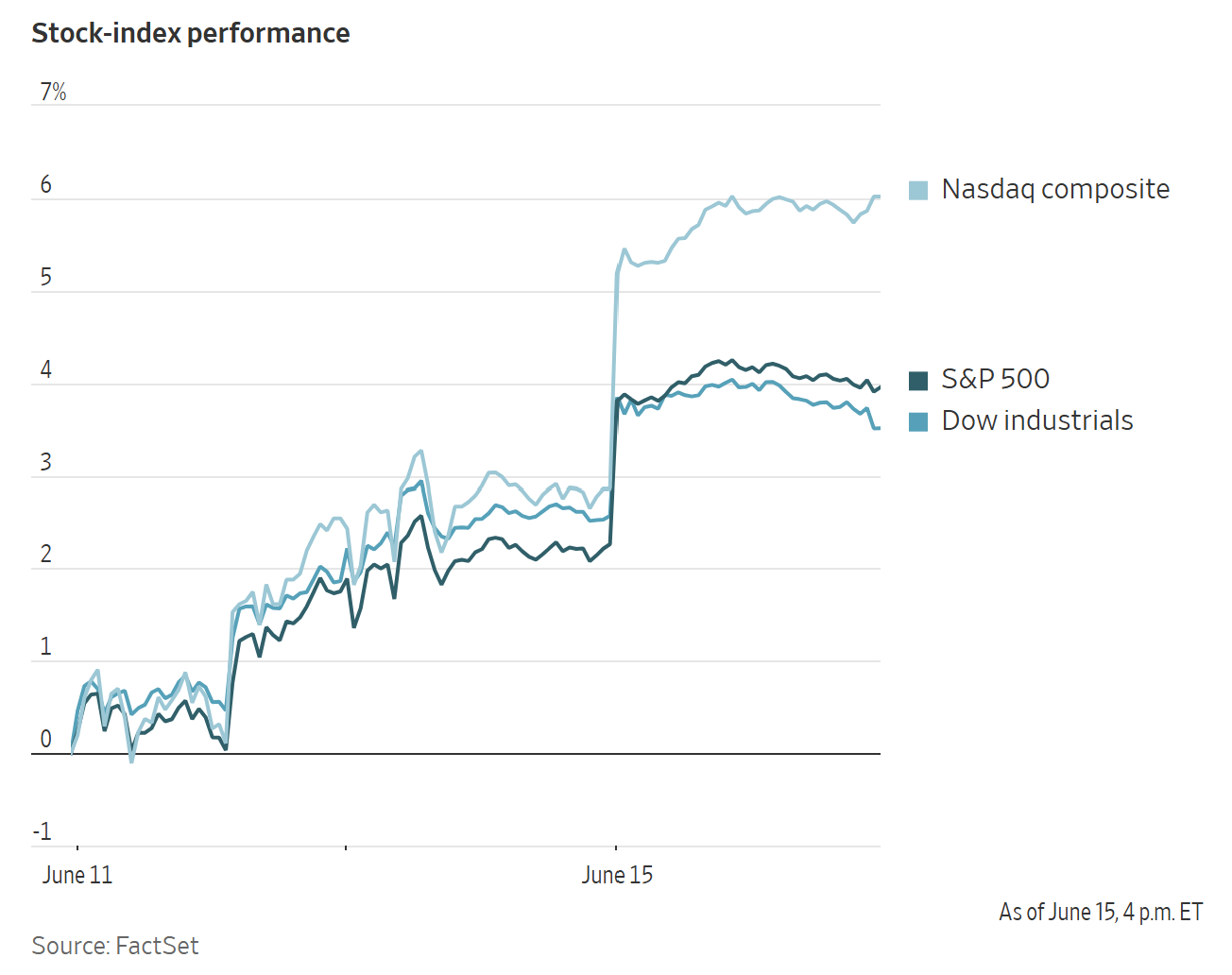

US Stock Indices

Dow Jones Industrial Average +0.92%

Nasdaq 100 +3.06%

S&P 500 +1.65%, with 7 of the 11 sectors of the S&P 500 up

News of a deal to reopen the Strait of Hormuz supported a broad rally in higher-risk segments of US markets on Monday, with equities advancing as oil prices fell on expectations that the conflict may be nearing an end.

The improvement in sentiment lifted the S&P 500 by +1.65%, while the Nasdaq 100 advanced +3.06%. The Dow Jones Industrial Average advanced by 468.77 points or +0.92%, and reached a fresh record high at 51,671.03.

Airline shares outperformed as the decline in oil prices eased concerns over higher jet fuel costs, with United Airlines closing at a record high.

In corporate news, TripAdvisor shares rose after the company announced the sale of its restaurant-reservation platform, TheFork, to American Express for $700 million.

Nvidia drew market attention after issuing $25 billion of high-grade bonds on Monday in its first bond sale since 2021. Demand was strong, with orders reaching as much as $85 billion, prompting an increase from the initial target of about $20 billion. The company issued notes across seven tranches with maturities ranging from two to 30 years. The spread on the longest-dated portion tightened to 0.65 percentage point above Treasuries as investor demand accelerated.

Fox agreed to acquire Roku in a transaction with an Enterprise Value of about $22 billion, marking a significant expansion into ad-supported streaming. The combination would bring together Fox’s sports, news and entertainment channels with Roku’s streaming platform of more than 100 million subscribers, creating the third-largest player in the US television market by share of viewing. Fox said it intends to continue operating Tubi and the Roku Channel as separate offerings, which management described as complementary.

Salesforce agreed to acquire Fin, a developer of AI-powered customer agents, for about $3.6 billion as the company seeks to expand its enterprise AI capabilities and capture additional demand in the sector.

S&P 500 Best performing sector

Information Technology +3.39%, with Western Digital +16.10%, Micron Technology +10.84% and Seagate Technology +9.43%

S&P 500 Worst performing sector

Energy -3.58%, with APA -6.08%, Marathon Petroleum -4.83% and Valero Energy -4.45%

Mega Caps

Alphabet +2.50%, Amazon +3.13%, Apple +1.82%, Meta Platforms +4.67%, Microsoft +2.31%, Nvidia +3.54% and Tesla +1.16%

Information Technology

Best performer: Western Digital +16.10%

Worst performer: Enphase Energy -4.02%

Materials and Mining

Best performer: Newmont +5.56%

Worst performer: Steel Dynamics -3.74%

European Stock Indices

CAC 40 +0.40%

DAX +1.05%

FTSE 100 -0.39%

Commodities

Gold spot +2.13% to $4,308.68 an ounce

Silver spot +3.03% to $70.04 an ounce

West Texas Intermediate -3.71% to $81.16 a barrel

Brent crude -3.78% to $83.48 a barrel

Gold prices rose for a third consecutive session on Monday, reaching their highest level in more than a week.

Spot gold advanced +2.13% to $4,308.68 per ounce after reaching its highest intraday level since 5 June. The move was supported in part by a -0.14% decline in the US dollar index, which made dollar-denominated metals more affordable for holders of other currencies.

Additional support came from policy developments in Singapore, where the deputy prime minister announced plans to establish an over-the-counter gold clearing system and introduce central bank gold-vaulting services.

Spot silver also gained, rising +3.03% to $70.04 per ounce.

Oil prices fell more than 3% on Monday, closing at a three-month low after the US President said the US and Iran had signed a memorandum of understanding intended to end the conflict and reopen the Strait of Hormuz. Brent crude futures settled down $3.28, or -3.78%, at $83.48 per barrel, while US WTI closed at $81.16, down $3.13, or -3.71%.

According to a US official, the memorandum was signed by President Trump, Vice President JD Vance and Iranian Parliament Speaker Mohammad Bagher Qalibaf. Iran’s semi-official Mehr news agency reported that the draft agreement calls for the Strait of Hormuz to reopen within 30 days under Iranian arrangements. Separately, the state-owned National Iranian Oil Company said Iran had lowered the official selling price of its light crude for Asian buyers to $7.15 per barrel above the Oman/Dubai average for July, down from a $13 premium in the previous month.

The memorandum is expected to be formally signed in Switzerland on Friday, followed by a 60-day discussion period covering Iran’s nuclear programme, uranium stockpiles and sanctions relief.

Market participants remain focussed on several unresolved issues beyond the nuclear file, including whether tolls will be imposed on ships transiting the Strait of Hormuz and whether Israel will refrain from attacking Hezbollah positions in Lebanon. Several European leaders attending the G7 meeting have reportedly expressed skepticism that normal traffic through the strait will resume quickly.

Iranian officials said they intend to reinstate service fees for vessels passing through the strait, while US administration officials said they expect toll-free transit to be part of the agreement. Reports also indicated that Israeli Prime Minister Benjamin Netanyahu told President Trump that Israel would not withdraw its troops from Lebanon and did not consider itself bound by the Lebanese provision of the US-Iran agreement.

Both WTI and Brent pared earlier losses beginning around 10:45 ET after reports that an Israeli drone had struck a vehicle in southern Lebanon, killing at least one person. Even so, traders and shipbrokers said it could take weeks before traffic through the Strait of Hormuz recovers meaningfully.

Reuters maritime security sources said that clearance operations using conventional minesweepers and advanced underwater drones could continue for 40 to 50 days before insurers, shipping companies and oil firms regain sufficient confidence to resume transit.

Elsewhere, no attacks on Russian refineries were reported over the weekend, although gasoline shortages in Russia persist. Kommersant reported that some Russian refineries are being allowed to produce fuel under lower environmental standards.

The US Department of Energy said strategic petroleum reserves for the week ended 12 June stood at 340.3 million barrels, down 8.9 million barrels from the previous week and at their lowest level since 1983. The drawdowns are part of a US agreement to release 172 million barrels from the reserve.

Note: As of 4 pm EDT 15 June 2026

Currencies

EUR +0.09% to $1.1585

GBP +0.04% to $1.3408

Bitcoin +4.51% to $66,343.61

Ethereum +8.84% to $1,810.55

The US dollar declined on Monday, falling to a 10-day low against both the euro and sterling as risk sentiment improved.

The dollar index fell -0.14% to 99.67, while the euro rose +0.09% to $1.1585 after earlier reaching $1.1622, its highest level since 5 June.

Sterling also strengthened, gaining +0.04% to $1.3408.

By contrast, the Japanese yen weakened -0.08% against the dollar to ¥160.34 per dollar, reversing earlier gains and remaining near levels that could prompt official intervention.

Attention is now turning to this week’s monetary policy decisions from major central banks, including the Fed, the BoJ, the BoE and the Reserve Bank of Australia.

The Fed is widely expected to leave rates unchanged in the 3.50% to 3.75% range on Wednesday, although it may remove its easing bias. Market participants will also be watching closely for the tone adopted by new Fed Chair Kevin Warsh during the press conference following the statement.

Fixed Income

US 10-year Bond -0.8 basis points to 4.481%

German 10-year Bund -4.2 basis points to 2.958%

UK 10-year Gilt -1.8 basis points to 4.819%

US Treasury yields fell to a one-month low on Monday.

The rally lost momentum during the session as investors concluded that the end of the conflict was unlikely to alter the widely held expectation that the FOMC will keep rates unchanged on Wednesday.

The yield on the 10-year Treasury note fell to 4.419% at one point, its lowest level since 12 May, and settled down -0.8 bps at 4.481%.

The two-year US Treasury yield, which is typically sensitive to expectations for Fed policy, fell -1.2 bps to 4.081%. At the long end of the curve, the 30-year yield rose +0.7 bps to 4.980%.

The US yield curve, measured by the spread between the two-year and 10-year notes, steepened modestly, widening by 0.4 bps to 40.0 bps.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing 18.5 bps of rate hikes in 2026, lower than the 26.4 bps priced in a week ago. Fed funds futures traders are now pricing in a 1.5% probability of a 25 bps rate cut at June’s FOMC meeting, compared to 3.0% last week.

Eurozone bond yields also moved lower on Monday.

Germany’s 10-year bond yield fell to 2.945% at one point, its lowest level since late May, and was down -4.2 bps on the day at 2.958%.

The German two-year Schatz yield, sensitive to expectations for the ECB deposit rate, fell earlier in the session to a two-week low of 2.547% before settling -5.2 bps lower at 2.586%. At the long end, the German 30-year yield declined -2.4 bps to 3.526%.

Money markets were pricing in around 30 bps of additional ECB tightening this year, down from more than 40 bps after the central bank raised interest rates last Thursday.

Italy’s 10-year bond yield fell -6.6 bps to 3.669%, hovering near a two-week low. The spread between Italy’s 10-year BTP yield and German bunds closed at 71.1 bps.

Note: As of 4 pm EDT 15 June 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.