¿Qué señales enviará el presidente Warsh?

Datos clave que moverán los mercados hoy

UE: índice armonizado de precios al consumo de la eurozona, índice armonizado de precios al consumo subyacente y discursos del presidente del Banco Central de los Países Bajos, Olaf Sleijpen, y del miembro del Comité Ejecutivo del BCE, Piero Cipollone

Reino Unido: IPC e IPC subyacente, IPP de insumos, de productos y subyacente de productos, e índice de precios al por menor

EE. UU.: decisión de tipos de interés de la Fed, comunicado de política monetaria de la Fed, proyecciones económicas del FOMC, proyecciones de tipos de interés, rueda de prensa del FOMC, ventas minoristas, grupo de control de ventas minoristas, ventas minoristas excluidos los automóviles y ventas de viviendas pendientes

Actualizaciones macroeconómicas mundiales

Avance: reunión del FOMC de junio. La Fed celebra esta semana su reunión del FOMC de junio. Hoy a las 14.00 horas EDT se publicarán el comunicado de política monetaria y el último Resumen de Proyecciones Económicas, seguidos a las 14.30 horas de la primera rueda de prensa del presidente Kevin Warsh. Los analistas han prestado especial atención a los posibles cambios en el comunicado, las proyecciones y el marco de comunicación bajo la nueva presidencia.

No se espera ningún cambio en los tipos de interés en esta reunión y, en general, tampoco se anticipan votos disidentes. Sin embargo, el comunicado podría sufrir revisiones de calado. El lenguaje sobre el mercado laboral podría reforzarse en respuesta a la reciente solidez de los datos de empleo, mientras que se presta especial atención al futuro de las señales de orientación futura. Dado que Warsh ha criticado anteriormente la orientación futura, y a la luz de los comentarios recientes de algunos responsables de política monetaria sobre la eliminación de las señales implícitas, los analistas han apuntado diversas posibilidades que van desde cambios menores en la redacción hasta la supresión completa de la frase sobre "ajustes adicionales". Algunos observadores han planteado también la posibilidad de una revisión más amplia del comunicado, aunque Bank of America ha argumentado que es posible que Warsh no haya tenido todavía tiempo suficiente para llevar a cabo una reforma de tal envergadura.

La mayoría de los análisis previos no esperan cambios significativos en el Resumen de Proyecciones Económicas ni su eliminación en esta reunión, aunque algunos consideran que podrían producirse ajustes en reuniones futuras, habida cuenta de las críticas anteriores de Warsh al marco. Existe división de opiniones sobre si el nuevo presidente incorporará su propia proyección en el diagrama de puntos. Algunos analistas señalan, además, que la Fed completó una revisión exhaustiva de sus comunicaciones el año pasado, por lo que introducir cambios significativos ahora podría interpretarse como innecesariamente disruptivo.

En cuanto a las perspectivas económicas, se espera en general que las proyecciones reflejen un menor crecimiento y unas estimaciones de inflación más elevadas, especialmente para el PCE general. En el gráfico de puntos, la opinión predominante es que podría eliminarse el recorte de tipos para 2026 implícito en la proyección mediana de marzo, mientras que un pequeño número de proyecciones podría desplazarse hacia un endurecimiento adicional. Las expectativas para 2027 siguen siendo dispares, con opiniones divididas entre ningún cambio y un único recorte de 25 pb. Los analistas también están divididos sobre si el tipo de política a largo plazo subirá hasta el 3,250 % o se mantendrá en el 3,125 %.

También existe una considerable especulación sobre cómo gestionará Warsh la rueda de prensa, ya que en el pasado ha criticado la frecuencia de comunicación de la Fed. La expectativa generalizada es que mantenga inicialmente el formato utilizado por Jerome Powell, con una declaración inicial seguida de un turno de preguntas y respuestas. No obstante, podría anunciar ajustes futuros, como el retorno a ruedas de prensa trimestrales. Goldman Sachs ha señalado que podría ser difícil avanzar rápidamente hacia un enfoque de comunicación menos transparente.

Se espera ampliamente que Warsh evite cualquier formulación que pueda interpretarse como orientación futura. Aun así, su tono general podría inclinarse de forma moderada hacia una postura más acomodaticia, haciendo referencia a indicadores como la media recortada del PCE de la Fed de Dallas, las dificultades en la medición de la inflación, la limitada presión inflacionista derivada de los salarios y los posibles beneficios de las ganancias de productividad gracias a la IA. Los analistas también esperan que deba responder a preguntas sobre cómo pretende traducir sus comentarios anteriores sobre el "cambio de régimen" en la Fed en cambios concretos de política monetaria y comunicación.

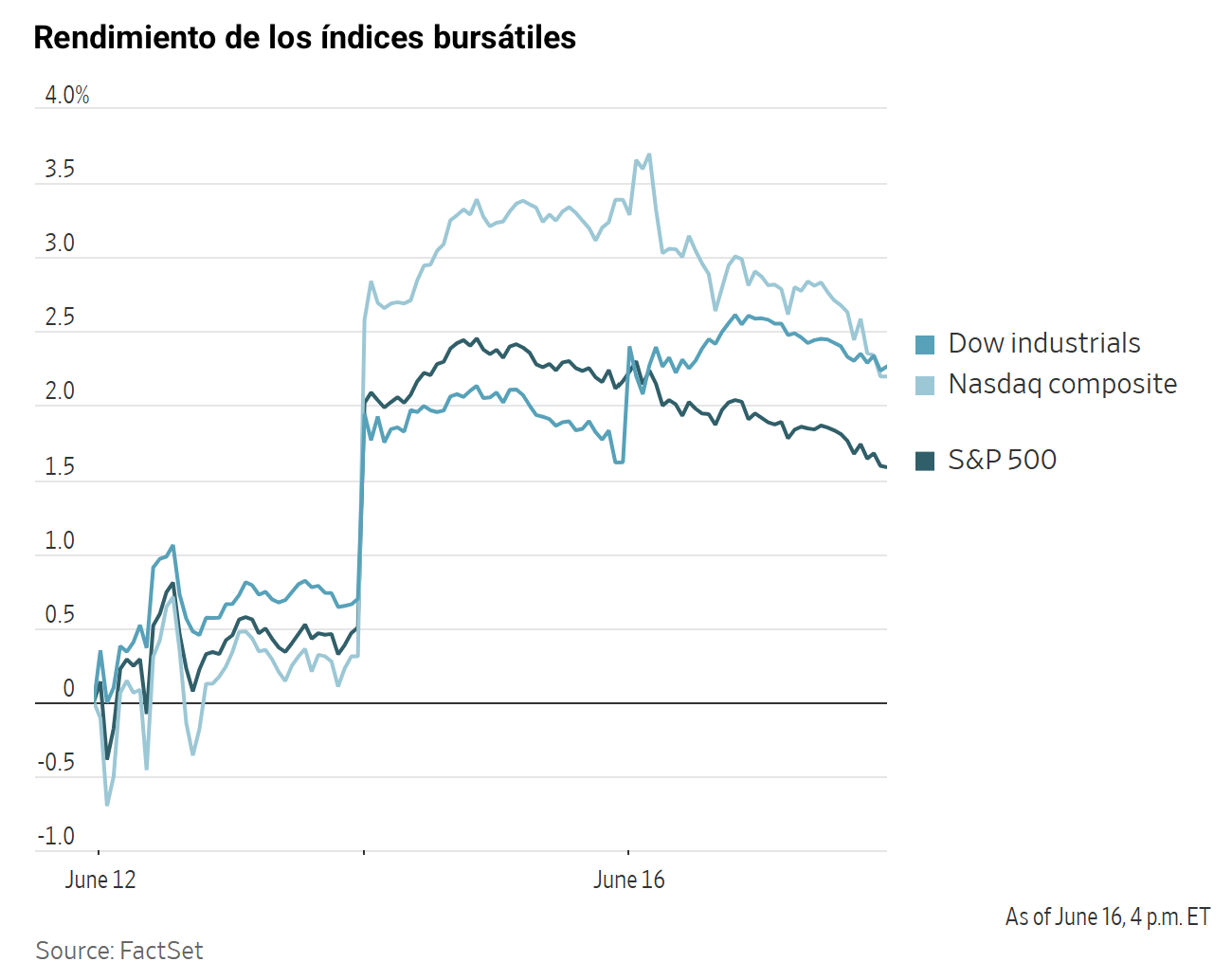

Índices bursátiles estadounidenses

El Dow Jones Industrial Average +0,64 %

El Nasdaq 100 -1,89 %

El S&P 500 -0,57 %, con 4 de los 11 sectores del S&P 500 a la baja

Los índices bursátiles estadounidenses registraron un comportamiento mixto el martes, tras el fuerte repunte del lunes. El Nasdaq Composite cayó un -1,15 %, mientras que el Dow Jones subió un +0,64 % hasta los 51.999,67 puntos, marcando su decimoséptimo cierre récord del año. El S&P 500 retrocedió un -0,57 % hasta los 7.511,35 puntos.

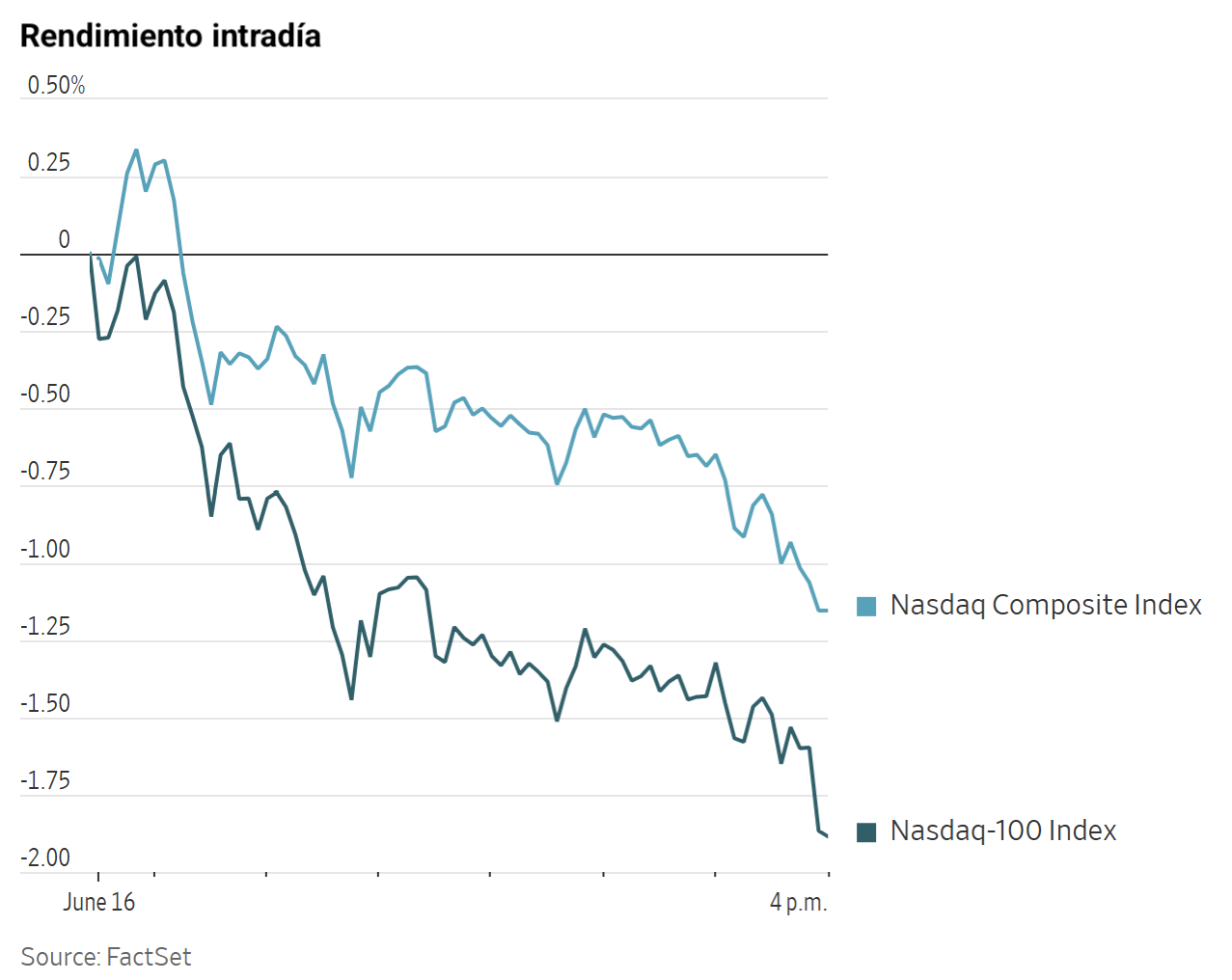

El efecto SpaceX en el Nasdaq. Los dos principales índices de renta variable del Nasdaq incorporarán SpaceX de formas notablemente distintas durante el periodo inicial tras su salida a bolsa. El Nasdaq Composite, que incluye prácticamente todas las empresas cotizadas en el mercado Nasdaq, ya ha añadido SpaceX y le ha asignado una ponderación basada en su capitalización bursátil de casi 2.790 millones de dólares.

De este modo, SpaceX se ha convertido de inmediato en uno de los mayores componentes de este índice de referencia amplio, lo que es coherente con la práctica habitual del Nasdaq de incorporar las empresas recién cotizadas al Composite al segundo día de negociación.

El Nasdaq 100, en cambio, no prevé incorporar SpaceX hasta julio como muy pronto. El índice, que sigue a aproximadamente 100 de las mayores empresas no financieras cotizadas en el mercado, ha acortado recientemente su periodo de espera para los nuevos integrantes, de los tres meses anteriores a 15 días de negociación.

Esta distinción resulta significativa ya que, a diferencia del Nasdaq Composite, que cuenta con más de 3.000 componentes, el Nasdaq 100 es un referente muy seguido por los fondos indexados, entre ellos el ETF QQQ de Invesco, que cuenta con 500.000 millones de dólares bajo gestión.

Incluso cuando SpaceX sea incorporada al Nasdaq 100, su influencia inicial sobre el índice será probablemente bastante limitada, ya que el Nasdaq 100 ajusta las ponderaciones de sus componentes en función del capital flotante, es decir, la proporción de acciones que cotizan libremente en el mercado. Actualmente, menos del 10 % de las acciones de SpaceX están disponibles para el público en general, aunque se espera que esa proporción aumente en los próximos meses a medida que expiren los períodos de bloqueo y los empleados e inversores internos puedan vender sus participaciones.

SpaceX subió un +4,83 % el martes, lo que contribuyó a un claro mejor comportamiento del Nasdaq Composite frente al Nasdaq 100.

En cuanto a noticias corporativas, Microsoft está valorando ofrecer una versión alojada en sus servidores de DeepSeek como opción de modelo de menor coste.

Según informaciones recientes, Netflix estaría estudiando la adquisición de Lionsgate Studios tras perder ante Fox en la pugna por Roku.

SpaceX ha formalizado la adquisición de Cursor por 60.000 millones de dólares, tal y como se esperaba.

Apple tiene previsto lanzar en 2027 su primer dispositivo wearable centrado en la IA, junto con unos AirPods con cámara integrada.

Rivian ha anunciado cientos de despidos en sus áreas de servicio, atención al cliente, ventas y marketing.

Yum! Brands ha puesto a la venta la cadena Pizza Hut por 2.700 millones de dólares; LongRange Capital se hará con el negocio fuera de China.

Sector con mejores resultados del S&P 500

Financiero +1,49 %, donde Fiserv +4,01 %, JPMorgan Chase +3,68 % y Moody’s +3,16 %

Sector con peores resultados del S&P 500

Tecnologías de la información -2,32 %, donde Monolithic Power Systems -9,29 %, Intel -8,45 % y KLA -7,44 %

Empresas de gran capitalización

Alphabet +1,09 %, Amazon -0,04 %, Apple +0,95 %, Meta Platforms +1,13 %, Microsoft -1,48 %, Nvidia -2,37 % y Tesla -1,58 %

Tecnologías de la información

Mejor rendimiento: Western Digital +4,22 %

Peor rendimiento: Monolithic Power Systems -9,29 %

Materiales y minería

Mejor rendimiento: Vulcan Materials +2,68 %

Peor rendimiento: Mosaic -3,69 %

Índices bursátiles europeos

El CAC 40 +0,75 %

El DAX +0,07 %

El FTSE 100 +0,61 %

Materias primas

El oro al contado +0,50 % hasta situarse en 4.330,13 $ la onza

La plata al contado -0,16 % hasta situarse en 69,92 $ la onza

El West Texas Intermediate -5,59 % hasta situarse en 76,62 $ el barril

El crudo Brent -4,78 % hasta situarse en 79,49 $ el barril

El oro avanzó el martes: el metal al contado subió un +0,50 % hasta los 4.330,13 $ por onza, después de haber alcanzado en la sesión anterior su nivel más alto desde el 5 de junio.

La plata al contado, en cambio, cedió un -0,16 % hasta los 69,92 $ por onza.

Los precios del petróleo, por su parte, cayeron por segunda sesión consecutiva el martes, tocando mínimos de tres meses, tras conocerse los detalles de un acuerdo provisional orientado a poner fin a la guerra con Irán y reabrir el estrecho de Ormuz, que incluiría disposiciones que permitirían a Irán reanudar las ventas de crudo.

Los futuros del crudo Brent cedieron 3,99 $, o un -4,78 %, hasta los 79,49 $ por barril, mientras que el WTI estadounidense bajó 4,54 $, o un -5,59 %, para cerrar en 76,62 $ por barril.

Estos niveles representan los cierres más bajos del Brent desde el 2 de marzo y del WTI desde el 4 de marzo. El conflicto entre EE. UU. e Irán se inició el 28 de febrero; el día anterior, el 27 de febrero, el Brent había cerrado en 72,48 $ por barril y el WTI en 67,02 $.

Conforme al acuerdo propuesto, el frágil alto el fuego anunciado en abril se prorrogaría 60 días adicionales y el estrecho de Ormuz volvería a abrirse tras haber sido bloqueado de facto por Irán desde los ataques iniciales de EE. UU. e Israel.

Según los puntos de comunicación del memorando de la Casa Blanca, el marco de paz propuesto permitiría a Irán reanudar de inmediato sus exportaciones de petróleo, flexibilizaría las sanciones bancarias y de transporte para facilitar las transacciones y liberaría 100.000 millones de dólares en fondos congelados. El ministro de Exteriores iraní declaró que las conversaciones formales comenzarían el día en que se firme el memorando, seguidas de 60 días adicionales de negociaciones.

Con todo, la incertidumbre en torno al acuerdo siguió siendo elevada, y se advirtió que los flujos de envíos y las exportaciones energéticas podrían tardar varias semanas en normalizarse. En el Líbano, Hezbolá, que cuenta con el respaldo de Irán, afirmó que no espera que Irán firme un acuerdo nuclear definitivo a menos que Israel se retire del territorio libanés.

Algunos desarrollos se interpretaron de forma constructiva. Según informó Bloomberg, al menos dos grandes petroleros iraníes habrían cruzado la línea de bloqueo de la Marina estadounidense, mientras que Windward señaló que varios petroleros de muy gran tamaño (VLCC, por sus siglas en inglés) indicaban su intención de transitar el estrecho con destino a los Emiratos Árabes Unidos. Al mismo tiempo, el presidente de EE. UU. sugirió que podría permitirse la expiración de las exenciones a las sanciones sobre la energía rusa.

Por otro lado, tras una pausa temporal durante el fin de semana, las fuerzas ucranianas reanudaron los ataques contra infraestructuras energéticas rusas, con impactos en un depósito de petróleo que habrían obligado al cierre de la refinería de Moscú, una de las mayores del país, con una capacidad de 250.000 barriles diarios.

Nota: los datos corresponden al 16 de junio de 2026 a las 16:00 horas EDT

Divisas

El EUR +0,18 % hasta situarse en 1,1606 $

La GBP +0,13 % hasta situarse en 1,3426 $

El bitcoin -0,96 % hasta situarse en 65.709,06 $

El ethereum -0,89 % hasta situarse en 1.794,38 $

El dólar estadounidense se debilitó ayer, aunque se mantuvo cerca del extremo superior de su rango de negociación reciente frente al euro y al yen japonés, en un contexto en el que se espera que los precios de la energía permanezcan elevados durante algún tiempo.

El índice del dólar cayó un -0,11 % hasta 99,56, mientras que el euro ganó un +0,18 % hasta situarse en 1,1606 $.

El yen japonés se depreció de forma marginal, un -0,02 %, hasta los 160,38 yenes por dólar, después de que el BoJ subiera su tipo de interés de referencia en 25 pb hasta el 1,0 %, tal y como se esperaba ampliamente. La medida, que lleva los tipos al nivel más alto desde 1995, refleja los esfuerzos por contener los riesgos inflacionistas vinculados al conflicto con Irán. No obstante, la votación del consejo de 7 a 1 dejó cierta incertidumbre en torno al calendario de futuros endurecimientos.

La libra esterlina subió un +0,13 % frente al dólar hasta 1,3426 $. Los participantes en el mercado esperan que el Banco de Inglaterra mantenga sin cambios los tipos de interés cuando anuncie su última decisión de política monetaria el jueves.

Renta fija

El bono estadounidense a 10 años -3,6 pb hasta alcanzar el 4,445 %

El bono alemán a 10 años -2,3 pb hasta alcanzar el 2,935 %

El gilt británico a 10 años -2,7 pb hasta alcanzar el 4,792 %

Los rendimientos del Tesoro estadounidense bajaron por tercera sesión consecutiva el martes.

El rendimiento del bono a 10 años cayó -3,6 pb hasta el 4,445 %. Una subasta de 13.000 millones de dólares en bonos a 20 años tuvo buena acogida: el rendimiento a 20 años, tras alcanzar un máximo intradía del 4,938 %, se moderó hasta el 4,930 %. El rendimiento del bono a dos años, que es especialmente sensible a las expectativas sobre el tipo de los fondos federales, cedió -1,3 pb hasta el 4,068 %.

En el extremo largo de la curva, el rendimiento a 30 años bajó -3,4 pb hasta el 4,946 %.

El diferencial entre los rendimientos a dos y diez años se estrechó en 2,3 pb hasta los 37,7 pb, lo que apunta a un leve aplanamiento de la curva.

Se da por descontado que la Fed mantendrá los tipos sin cambios el miércoles y podría eliminar cualquier referencia a una orientación hacia la relajación monetaria. Los inversores seguirán de cerca el comunicado de política monetaria, las proyecciones económicas actualizadas y los comentarios del presidente Kevin Warsh en su rueda de prensa posterior a la reunión.

Según la herramienta FedWatch de CME Group, los operadores de futuros de fondos federales están descontando 19,5 puntos básicos de subidas de tipos en 2026, por debajo de los 24,4 puntos básicos de hace una semana. Asimismo, asignan ahora una probabilidad del 0,5 % a una subida de 25 puntos básicos al final de la reunión del FOMC de hoy, frente a una probabilidad del 0,8 % de un recorte de tipos la semana pasada.

Los rendimientos de los bonos soberanos de la eurozona cayeron en todos los países y plazos por cuarta jornada consecutiva el martes, alcanzando mínimos de varias semanas.

El rendimiento del Bund alemán a 10 años retrocedió -2,3 pb hasta el 2,935 %, después de tocar el 2,925 %, su nivel más bajo desde el 8 de abril. El rendimiento del BTP italiano a 10 años cayó -2,4 pb hasta el 3,645 %, tras alcanzar el 3,639 %, su nivel más bajo desde el 18 de marzo, dejando el diferencial frente a los Bunds en 71,0 pb.

El rendimiento alemán a dos años, que es sensible a los cambios en las expectativas sobre los tipos del Banco Central Europeo, bajó -1,0 pb hasta el 2,576 %, después de haber marcado un mínimo de dos semanas en el 2,547 % el lunes. En el extremo largo de la curva, el rendimiento a 30 años cedió -3,0 pb hasta el 3,496 %.

La semana pasada, el BCE se convirtió en el primer gran banco central en endurecer su política monetaria desde el inicio de la guerra con Irán, al que siguió el martes el Banco de Japón.

Aun así, los inversores han recortado las expectativas de nuevas subidas por parte del BCE tras el memorando de entendimiento entre Washington y Teherán, pese a la falta de claridad sobre sus términos. Los futuros sobre el mercado monetario descuentan ahora plenamente 30 pb de endurecimiento adicional para finales de año, lo que implica una subida de un cuarto de punto y una probabilidad de alrededor del 20 % de un segundo movimiento.

En una entrevista con France Culture, la presidenta del BCE, Christine Lagarde, acogió el lunes el acuerdo de alto el fuego entre EE. UU. e Irán, especialmente si se traduce en la reapertura del estrecho de Ormuz. Al mismo tiempo, mantuvo un tono claramente restrictivo en materia de inflación, en un cambio relevante respecto a la rueda de prensa del jueves. Lagarde advirtió de que los elevados precios de la energía están empezando a trasladarse a otras partes de la economía y señaló que el banco central actuaría si los efectos de segunda ronda, como un mayor crecimiento salarial, se hacen más evidentes. También defendió la reciente subida de tipos frente a las críticas sobre su posible impacto en el crecimiento.

Asimismo, Lagarde argumentó que la Unión de Mercados de Capitales, denominada ahora Unión de Ahorro e Inversión, solo podrá tener pleno éxito si cuenta con el respaldo de un instrumento de deuda mutualizado que aporte mayor profundidad y liquidez al mercado. Aunque el alto el fuego ha suscitado esperanzas de una moderación de los costes energéticos, Lagarde y otros responsables de política monetaria, entre ellos el presidente del Bundesbank, Joachim Nagel, indicaron el martes que el BCE sigue dispuesto a endurecer su política si fuera necesario.

El economista jefe del BCE, Philip Lane, afirmó en un evento de Reuters NEXT celebrado el martes que el banco central mantendrá una actitud "proactiva" en sus esfuerzos por contener la inflación, que sigue sin bajar al objetivo del 2 % durante al menos el próximo año. Este indicó que la política monetaria continuará respondiendo en función de cómo evolucionen los riesgos de inflación.

Nota: los datos corresponden al 16 de junio de 2026 a las 16:00 horas EDT

Aunque se han hecho todos los esfuerzos posibles para verificar la exactitud de esta información, EXT Ltd. (en adelante, "EXANTE") no se hace responsable de la confianza que cualquier persona pueda depositar en esta publicación o en cualquier información, opinión o conclusión contenida en ella. Las conclusiones y opiniones expresadas en esta publicación no reflejan necesariamente la opinión de EXANTE. Cualquier acción realizada sobre la base de la información contenida en esta publicación es estrictamente bajo su propio riesgo. EXANTE no se hará responsable de ninguna pérdida o daño relacionado con esta publicación.

Este artículo se presenta a modo informativo únicamente y no debe ser considerado una oferta ni solicitud de oferta para comprar ni vender inversión alguna ni los servicios relaciones a los que se pueda haber hecho referencia aquí. Operar con instrumentos financieros implica un riesgo significativo de pérdida y puede no ser adecuado para todos los inversores. Los resultados pasados no garantizan rendimientos futuros.

Regístrese para recibir perspectivas de los mercados

Regístrese

para recibir perspectivas

de los mercados

Suscríbase ahora

Artículos relacionados

El BCE mantiene su postura, pero los riesgos van en aumentoDiarias24 jul 2026

El BCE mantiene su postura, pero los riesgos van en aumentoDiarias24 jul 2026 ¿Podrá el Banco de Inglaterra relajar realmente su política?Diarias23 jul 2026

¿Podrá el Banco de Inglaterra relajar realmente su política?Diarias23 jul 2026 ¿Está mejorando el sentimiento alemán gracias al optimismo reformista?Diarias22 jul 2026

¿Está mejorando el sentimiento alemán gracias al optimismo reformista?Diarias22 jul 2026 Earnings Scoreboard - Discounting the first derivativeMarcador de resultados21 jul 2026

Earnings Scoreboard - Discounting the first derivativeMarcador de resultados21 jul 2026

Creado por profesionales. Para profesionales.