Is AI hurting or helping employees and markets?

Key data to move markets today

EU: Eurozone GDP and Eurozone Employment Change

UK: Speeches by BoE External Member Swati Dhingra and BoE Governor Andrew Bailey

US: Nonfarm Payrolls, Average Hourly Earnings, Labour Force Participation Rate, Unemployment Rate and U6 Underemployment Rate

JAPAN: Labour Cash Earnings

Global Macro Updates

Is AI already replacing workers? US jobless claims rose last week to the highest level since February, increasing 13,000 to 225,000. However, this rise may potentially reflect volatility around the Memorial Day holiday. Nevertheless, the four-week moving average of initial jobless claims increased to 214,750, also the highest since February. Continuing claims dropped 8,000 to 1.777 million. Perhaps more interestingly, given concerns about the impact of AI in the workplace, first-quarter worker productivity growth was revised lower.

The US Bureau of Labor Statistics on Thursday said that nonfarm business sector labour productivity grew at an annualised rate of 0.3% in the first quarter of 2026, a larger-than-expected downward revision from the preliminary estimate of 0.8%. On a positive note, unit labour costs increased at a 1.8% rate last quarter, a downward revision from the 2.3% reported in May and below the 2.5% forecast. This news came as data showed that US technology companies in May announced 38,242 job cuts in May, the most in nearly two years. As noted by Bloomberg news, planned cuts in the industry are up more than 65% so far this year compared to the same period in 2025, according to data from outplacement firm Challenger, Gray & Christmas Inc. However, nonfarm business labour productivity rose 2.8% from a year ago, indicating companies are gradually improving worker efficiency.

Research by S&P indicates that AI adoption remains focussed on productivity and revenue gains, not explicitly on head count reduction. Job cuts remain a secondary consequence, rather than the primary objective of investment. However, that same research also notes that AI's employment impact has turned modestly negative, reversing the more positive picture in 2025. Citing the latest S&P Global Purchasing Managers' Index survey, it shows a global net impact of -5 percentage points over the past 12 months (percentage of businesses increasing workforce due to AI adoption minus percentage decreasing), with a further -2 points net impact forecast for the coming year. This seems to be supported by recent high-profile, AI-related workforce reduction plans announced by companies including Meta Platforms, Intuit and Cisco Systems.

Today’s nonfarm payrolls are expected to show US employers adding 85,000 jobs in May. If this is indeed the case, it would cap the strongest three-month stretch of job gains in more than a year and potentially put aside the worries of a “low-hire, low-fire” economy.

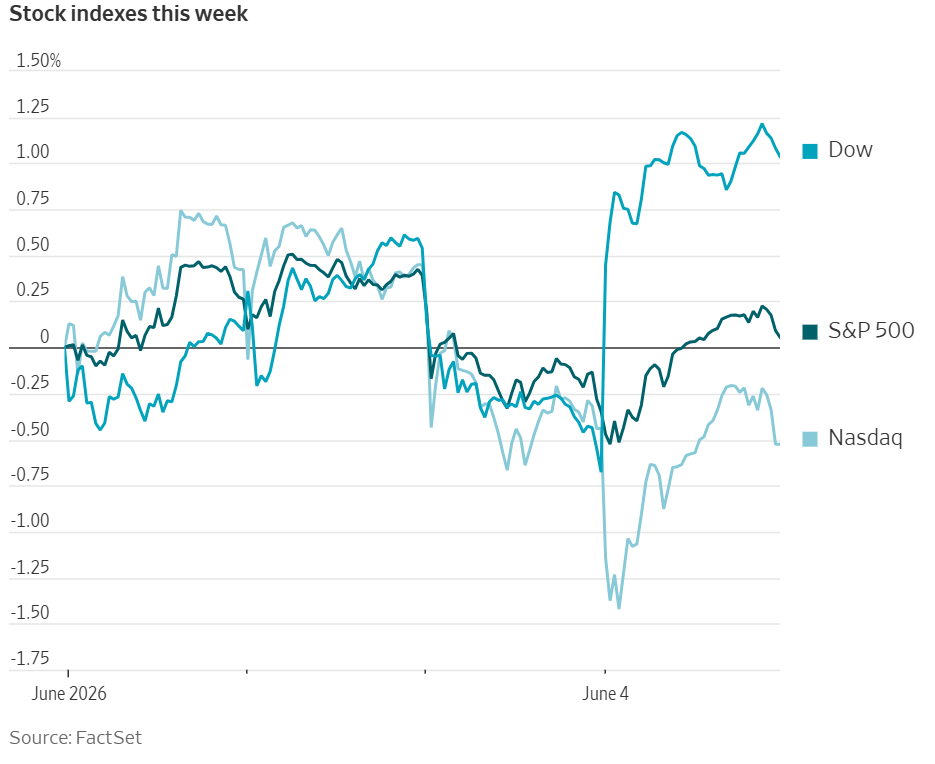

US Stock Indices

Dow Jones Industrial Average +1.73%

Nasdaq 100 -0.53%

S&P 500 +0.41%, with 9 of the 11 sectors of the S&P 500 up

Healthcare and financial stocks pushed the Dow Jones Industrial Average to a record high on Thursday. The Dow Jones Industrial Average rose 874.86 points, or +1.73%, to 51,561.93, while the S&P 500 gained 30.63 points, or +0.41%, to 7,584.31. However, AI tech stocks, led by the 12.59% drop in chipmaker Broadcom’s shares, weighed on the Nasdaq. The Nasdaq Composite was down 23.02 points, or -0.09%, to 26,830.96.

In company news, UnitedHealth, a Dow Jones component, rose 5.2% after Bank of America raised its rating to a ‘buy’.

Blackstone became the latest firm to cap withdrawals after limiting redemptions from its flagship private credit fund for the first time after investors sought to pull 10% of the shares.

In a boost to generic drugmakers, the US Supreme Court, in a 9-0 ruling that overturned a lower court’s ruling, said that drugmaker Hikma's generic version of Amarin's cardiovascular medication Vascepa did not infringe Amarin's patents.

Honeywell’s quantum computing company, Quantinuum, rose 13.3% in their Nasdaq debut, fetching a valuation of $17.63 billion. The stock opened at $68, compared with its IPO price of $60.

S&P 500 Best performing sector

Health Care +3.16%, with Humana +6.80%, Centene +5.29% and Solventum +5.18%

S&P 500 Worst performing sector

Information Technology -1.43%, with Ciena -13.66%, Broadcom -12.59% and Micron Technology -7.74%

Mega Caps

Alphabet +3.68%, Amazon +1.51%, Apple +0.31%, Meta Platforms +0.74%, Microsoft +0.17%, Nvidia +1.94% and Tesla -1.24%

Information Technology

Best performer: Alphabet +3.68%

Worst performer: Ciena -13.66%

Materials and Mining

Best performer: Nucor +1.77%

Worst performer: Dow -1.72%

Corporate Earnings Reports

Posted on Thursday, 4 June from The Pulse, our real-time AI-driven news tool. Available exclusively on the EXANTE Web Platform

Lululemon reported Q1 2026 results with revenue of $2.5bn vs $2.5bn expected and EPS of $1.69 vs $1.69 expected. Revenue rose +4% y/y while comparable sales increased +1%. Americas revenue fell -3% y/y whereas international revenue climbed +22% y/y. Gross margin declined -410 bps y/y to 54.2%. The company lowered full-year guidance to revenue of $11.0bn-$11.15bn and EPS of $10.95-$11.15 from prior ranges of $11.35bn-$11.5bn and $12.10-$12.30 respectively. Q2 revenue guidance was set at $2.450bn-$2.475bn and EPS at $1.76-$1.81 versus $2.69 expected. CEO stated that the company has been navigating headwinds that have led it to adjust its outlook for the full year.

Rubrik reported first-quarter results with revenue $387.1M vs the $366M consensus with subscription revenue of $374.2M up +41% y/y. Adjusted EPS was $0.16 vs the ($0.03) estimate while free cash flow totalled $73.6M. Subscription ARR grew +32% y/y to $1.57B. The company raised full-year fiscal 2027 guidance with revenue of $1.638B-$1.648B, adjusted EPS of $0.25-$0.35 and free cash flow of $293M-$303M. It also issued positive second-quarter guidance. Rubrik joined Anthropic’s Project Glasswing to test AI-driven vulnerability detection and launched a joint Microsoft 365 backup service with Sophos.

Planet Labs reported Q1 results with revenue $94.2mn vs the $90mn estimate, up +42% y/y. Adjusted EPS was -$0.03 vs the -$0.04 estimate. Remaining performance obligations totalled $816mn, up +81% y/y, while backlog stood above $906mn, up +72% y/y. The firm guided FY27 revenue to $425mn-$441mn. It also secured two new NGA contract awards through Planet Labs Federal, including exercise of a $22mn first option year on the Luno B contract for maritime intelligence, plus a Global Monitoring Service agreement. Three Pelican satellites were launched and Pelican-11 was shipped ahead of a forthcoming rideshare mission. Chief Executive Will Marshall stated that Planet delivered record revenue of $94.2mn, accelerating top-line growth to +42% y/y, and that the strong start reflects the mission-critical nature of its data.

DocuSign reported Q1 2027 results with revenue of $830.2mn against consensus of $823.23mn and adjusted EPS of $1.09 vs $1.00 expected. Revenue rose +9% y/y. Full-year guidance showed revenue of $3.49bn-$3.502bn, up +9% y/y, with non-GAAP gross margin of 81.5% to 82.0% and operating margin of 30.5% to 31.0%. Quarterly guidance indicated revenue of $865mn-$869mn, up +8% y/y. The company noted free cash flow of $289.4mn, share buybacks of $317.5mn, IAM at 12.6% of ARR and appointed Graham Sheldon as incoming chief product officer. "We delivered significant innovation this quarter while driving strong financial results through durable revenue growth, substantial free cash flow, and record share buybacks," the company stated.

European Stock Indices

CAC 40 +1.15%

DAX +0.60%

FTSE 100 +0.27%

Commodities

Gold spot +0.95% to $4,473.89 an ounce

Silver spot +1.61% to $73.87 an ounce

West Texas Intermediate -3.10% to $93.04 a barrel

Brent -2.84% to $95.03 a barrel

Gold rose on Thursday primarily due to a weaker US dollar and a drop in oil prices, which were triggered by renewed optimism around a conditional ceasefire between Israel and Lebanon.

Spot gold rose +0.95% to $4,473.89 an ounce. Spot silver rose +1.61% to $73.87 per ounce.

Oil prices fell on Thursday, breaking a three-session streak of gains, after the US House of Representatives passed a measure that would block President Donald Trump from continuing the war with Iran and Israel and Lebanon agreed to a US-mediated ceasefire, one of Iran’s preconditions to a peace deal. However, the truce agreement was rejected by the Iranian-backed Hezbollah and Israel said it would not withdraw troops from the country.

Brent fell -2.84% to settle at $95.03 while US WTI fell -3.1% to settle at $93.04 per barrel after adding nearly 2.5% on Wednesday.

On Thursday, OPEC’s Secretary General, Haitham Al Ghaisthe, speaking at the St Petersburg International Economic Forum, said that OPEC expects robust oil demand growth and is not changing its estimates despite the Middle East conflict and closure of the Strait of Hormuz. He said, “Despite all the commentary out there that oil demand is declining, we have not registered signs of that yet.” He stated that OPEC still forecasts robust demand growth at 1.2 million barrels a day for this year. Despite OPEC’s suggestion of robust demand, there have been suggestions by several oil sector analysts that demand destruction may be taking place, with consumers and industry relying more upon renewable energy sources.

As reported by Reuters, Iranian exports of crude oil and condensate fell to their lowest level in at least six years in May, falling well below 300,000 barrels per day, primarily due to the US naval blockade. Vortex data shows that Iran's exports averaged about 209,000 bpd in May, sharply down from 1.34 million bpd in April and nearly 1.9 million bpd in March, marking their lowest level since late 2019, during President Trump’s first term when he was pursuing a "maximum pressure" campaign against Iran. Data from another firm, Kpler, showed a similar six year low, although it put May exports slightly higher at 260,000 bpd.

Note: As of 4 pm EDT 4 June 2026

Currencies

EUR +0.12% to $1.1609

GBP +0.05% to $1.3424

Bitcoin -2.53% to $63,265.22

Ethereum -2.28% to $1,775.82

The dollar edged down from a two-month high on Thursday due to rising optimism about a ceasefire in Lebanon, one of Iran’s preconditions for a peace deal with the US. The dollar Index ended the day -0.08% to 99.44. The euro was +0.12% at $1.1609, while the British pound was +0.05% to $1.3424.

The yen was +0.02% against the greenback to ¥160.02 per dollar. Chief Cabinet Secretary Minoru Kihara had said in Tokyo he expects the central bank to coordinate its moves with the government after BoJ Governor Kazuo Ueda had given fresh hints that an interest rate hike is in the cards this month.

Fixed Income

US 10-year Bond -1.4 basis points to 4.473%

German 10-year Bund -0.7 basis points to 3.021%

UK 10-year gilt +0.7 basis points to 4.911%

US Treasury yields fell on Thursday after softer than expected labour market data, while oil prices retreated on renewed hopes that a deal to end the US-Israeli war with Iran could be reached.

Initial jobless claims fell while data from the US Labor Department showed worker productivity increased at the slowest pace since the first quarter of 2025 as unit labour costs came in lower than expected.

The yield on the 10-year US Treasury note fell -1.4 bps to 4.473% while the 2-year US Treasury yield, sensitive to Fed fund rate expectations, was -3.0 bps to 4.047%. At the long end, the 30-year Treasury bond yield declined -1.1 bps to 4.977%. The gap between yields on two- and 10-year Treasury notes, seen as an indicator of economic expectations, was at a positive 42.6 basis points.

In Fed speak on Thursday, San Francisco Fed President Mary Daly said that the US interest-rate path will depend on how the economy evolves and that monetary policy is "in a good place" and the Fed is prepared to respond "either way."

Kansas City Fed President Jeffrey Schmid noted that it was important to get inflation back down to the 2% target, but said he and his colleagues don’t want to push the economy into recession. He said the Fed’s choice now is between being patient and holding interest rates steady or hiking rates to tamp down inflation

Richmond Fed President Tom Barkin said that “the Fed is well positioned to respond as appropriate” as the FOMC evaluates the economic impacts of the Middle East crisis.

According to CME Group's FedWatch Tool, Fed funds futures traders are now pricing in a 3.6% probability of a 25 bps rate cut at June’s FOMC meeting, compared to a 0% probability of a rate hike last week.

In the euro area, investors weighed up renewed violence in the Middle East against a potential new ceasefire agreement between Israel and Lebanon.

Germany’s 10-year Bund yield bps edged down -0.7 bps to 3.021%. Germany’s 2-year yield, sensitive to ECB policy-rate expectations, fell -1.0 bps to 2.656%.

Money markets show traders expect the ECB deposit rate to be around 2.7% by December, which implies two quarter-point hikes and a roughly 65% chance of a third. Markets have almost fully priced in a rate hike next week and another in September.

Italy’s 10-year yield rose +2.4 bps to 3.764%. The spread between Italy’s 10-year BTP and the 10-year Bund rose to 74.3 bps, +3.1 bps from Tuesday’s 71.2 bps.

Note: As of 4 pm EDT 4 June 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.