Is the tech rally over?

Key data to move markets today

EU: German Factory Orders and Eurozone Sentix Investor Confidence

JAPAN: GDP and Current Account

Global Macro Updates

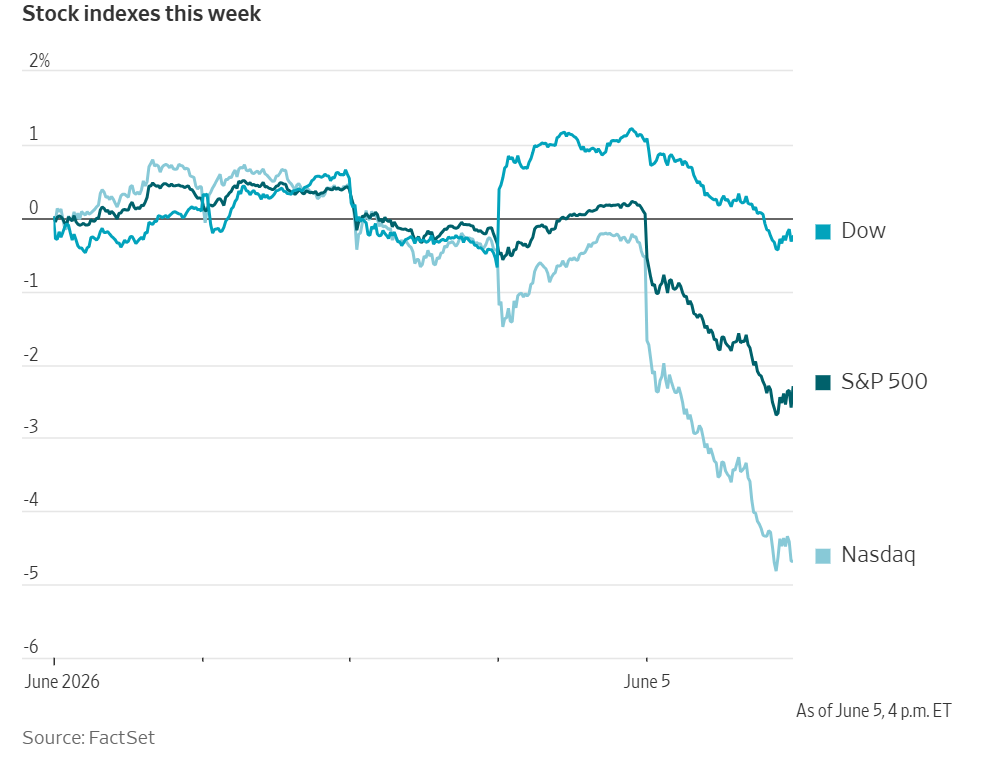

The US labour market’s surprise causes an AI tumble. The US economy posted another month of strong employment gains in May on Friday, raising the likelihood of the Fed keeping interest rates higher for longer or even raising rates, amid rising inflation stemming from the war with Iran. A high interest rate environment makes it more expensive for Big Tech companies that are investing heavily in AI to raise capital in bond markets. The impact on equities markets was clear: US tech stocks fell by the most since the “liberation day” tariff announcements in April 2025. The Nasdaq plunged over 4% as shares in chipmakers sold off sharply and the S&P fell almost 2.6%, ending a nine-week winning streak.

Nonfarm payrolls increased by 172,000 jobs last month after rising by an upwardly revised 179,000 in April. The Street expectations were of a rise in the 85,000–90,000 range after a previously reported 115,000 rise in April. The economy added 93,000 more jobs in March and April than previously estimated. The payrolls count for March was revised up by 29,000 jobs to 214,000. Friday’s results now mean that payroll growth has now averaged 188,000 jobs per month over the past three months, nearly triple the comparable figure for the same period in 2025. May’s gains were broad, with the leisure and hospitality sector adding 70,000 positions, well above the average monthly gain of 14,000 over the past 12 months. Jobs at restaurants and bars rose by 48,000 jobs, although this may be temporary and attributable to the US hosting the World Cup. Local government employment increased by 55,000 jobs, while Federal government payrolls rose by 1,000. The Healthcare sector added 35,000 jobs and construction jobs increased by 17,000. Financial services jobs fell by 22,000 jobs and are down by 107,000 since May 2025.

The unemployment rate held at 4.3% for a third consecutive month. This solid run of strong employment gains suggests the labour market may no longer be in a "slow-hire, slow-fire" equilibrium. However, the number of people unemployed for 27 weeks and more increased by 155,000 to 1.988 million, the highest level since December 2021. The median duration of unemployment rose to 11.6 weeks, the longest since November 2021, from 11.0 weeks in April. This suggests that the unemployed are struggling to get hired. This particularly appears to be the case with young, educated workers who, despite still looking for jobs, are finding themselves increasingly competing with AI which is absorbing the task-driven workflows traditionally assigned to entry-level staff.

However, the labour force participation rate was also unchanged, remaining at a 4.5-year low of 61.8%. The labour force has shrunk by about 1.4 million since December 2025. The demographic challenge is forecast to get worse as more Baby boomers retire. This creates a shrinking tax and production base just as the cost of supporting an aging population is expected to soar over the next decade.

Eurozone: trouble ahead? Eurozone GDP fell for the first time in over a year in Q1 with Ireland seeing the biggest drop. According to a final estimate published on Friday by Eurostat, the eurozone economy contracted by 0.2% in the first three months of 2026. This marked a sharp deterioration from the 0.1% expansion indicated in earlier flash readings and a reversal of the 0.2% growth recorded in Q4 2025. On a y/o/y basis, the eurozone only grew 0.3%, down from 1.2% last year. This deceleration can be attributed to the surge in energy prices following the outbreak of the US-Israeli-led war with Iran and the consequent negative effect on business and consumer confidence.

The biggest drop in growth was reported by Ireland, which saw a 12.1% q/o/q contraction and a 16.8% decline compared with the same period a year earlier. However, Ireland's Central Statistics Office has previously noted that such swings are typically driven by the multinational-dominated industrial sector rather than domestic economic conditions. As noted by euronews, Germany, the bloc's largest economy, grew by 0.3% in the first quarter after two years of chronic underperformance. Italy expanded by 0.3%, while Spain saw 0.6% growth. However, in a continuation of pre-Iran war weakness, France contracted by 0.1%.

According to Eurostat, eurozone inflation is expected to be 3.2% in May, up from April’s 3.0%. The unemployment rate edged up to 6.3% in April from 6.2% in March. The ECB is widely expected to raise rates at its meeting this week, but with inflation rising and growth slowing, the ECB may increasingly find itself balancing between managing the after-effects of a supply-side energy shock and preventing inflation expectations from de-anchoring.

US Stock Indices

Dow Jones Industrial Average -1.35%

Nasdaq 100 -4.77%

S&P 500 -2.64%, with 6 of the 11 sectors of the S&P 500 down

There was a sharp selloff in chip and memory stocks on Friday after a better-than-expected jobs report raised concerns about higher interest rates. Chip stocks lost about $1.3 trillion in market value with the PHLX chip index slumping 10.3% in its deepest one-day loss since the beginning of the Covid pandemic in March 2020. The S&P 500 broke a streak of nine straight weekly gains, while the Nasdaq had its worst week since the 24 April Liberation Day selloff. The Dow Jones Industrial Average fell 695.15 points, or -1.35%, to 50,866.78, while the S&P 500 dropped 200.57 points, or -2.64%, to 7,383.74. The Nasdaq Composite plunged 1,121.53 points, or -4.18%, to 25,709.43, its largest one-day percentage loss since last year.

In company news, Lululemon Athletica shares fell after the athletic apparel maker cut its annual profit forecast and projected second-quarter earnings well below Wall Street estimates.

Bloomberg news reported that Alphabet’s Google has agreed to pay Elon Musk’s SpaceX $920 million a month for computing power as part of a cloud services deal that runs through mid-2029, its second such agreement with an AI competitor in a matter of weeks.

S&P 500 Best performing sector

Consumer Staples +1.64%, with Kimberly-Clark +6.28%, Clorox +5.03% and Kenvue +4.92%

S&P 500 Worst performing sector

Information Technology -5.78%, with Micron Technology -13.25%, Teradyne -12.03% and Sandisk -11.39%

Mega Caps

Alphabet -0.98%, Amazon -3.06%, Apple -1.18%, Meta Platforms -5.51%, Microsoft -2.66%, Nvidia -6.19% and Tesla -6.56%

Information Technology

Best performer: Tyler Technologies +1.27%

Worst performer: Micron Technology -13.25%

Materials and Mining

Best performer: Sherwin-Williams +1.74%

Worst performer: Freeport McMoRan -9.07%

According to LSEG I/B/E/S data, Q1 2026 y/o/y earnings are expected to be 29.4%. Excluding the Energy sector, the y/o/y earnings estimate is 30.9%. Of the 493 companies in the S&P 500 that have reported earnings by 5 June, 84.2% reported above analyst expectations. This compares to a long-term average of 67.4% and the prior four quarter average of 78.1%. The Q1 2026 y/o/y blended revenue growth is expected to be 11.4%. Excluding the Energy sector, the growth estimate is 12.0%. Of the companies that have reported Q1 2026 revenue, 79.7% have reported revenue above analyst expectations. This compares to a long-term average of 62.7% and an average over the past four quarters of 72.8%.

For 26Q2, there have been 53 negative EPS preannouncements issued by S&P 500 corporations compared to 59 positive EPS preannouncements. By dividing 53 by 59 the N/P ratio is 0.9 for the S&P 500 Index. The forward four-quarter (26Q2– 27Q1) P/E ratio for the S&P 500 is 21.6.

Six companies are expected to report quarterly earnings during the week of 8 June.

European Stock Indices

CAC 40 -0.32%

DAX -0.75%

FTSE 100 +0.07%

According to LSEG I/B/E/S data, first quarter earnings are expected to increase 11.8% from Q1 2025. Excluding the Energy sector, earnings are expected to increase 7.1%. First quarter revenue is expected to decrease 0.4% from Q1 2025. Excluding the Energy sector, revenues are expected to decrease 0.7%. Of the 289 companies in the STOXX 600 have reported earnings by 4 June for Q1 2026, 58.1% reported results exceeding analyst estimates. In a typical quarter 54% beat analyst EPS estimates. Of the 348 companies in the STOXX 600 have reported revenue tby 4 June for Q1 2026, 53.2% reported revenue exceeding analyst estimates. In a typical quarter 58% beat analyst revenue estimates.

Commodities

Gold spot –3.38% to $4,322.85

Silver spot -7.86% to $68.16 an ounce

West Texas Intermediate -2.69% to $90.54 a barrel

Brent -2.0% to $ 93.09 a barrel

Gold fell on Friday as better than expected nonfarm payroll numbers suggested that the Fed would keep interest rates higher for longer.

Spot gold fell -3.38% to $4,322.85 an ounce. Spot silver was also down, falling -7.86% to $68.16 per ounce.

Oil prices fell again on Friday after Oman said operations at Mina al Fahal port were proceeding normally following a Reuters report that oil loadings had been suspended after an explosion.

Brent crude futures were down -2.0% to settle at $93.09 a barrel, while US WTI declined -2.69% to $90.54 per barrel.

On Friday, Iran reaffirmed its support for Hezbollah and demanded that Israel withdraw its troops from southern Lebanon, further complicating efforts to secure a near-term peace deal that would include the resumption of traffic through the crucial strait. Although President Trump's administration has negotiated three truces, and, while fighting has been greatly reduced, the two sides continue to trade airstrikes.

Over the weekend Israel struck the Iran-backed Hezbollah militant group in Beirut. On Sunday, Iran fired ballistic missiles at Israel in retaliation. It was the first time Iran has fired ballistic missiles at Israel since the ceasefire was announced in April. However, in an interview with the Financial Times on Sunday, President Trump said that Israeli Prime Minister Benjamin Netanyahu will have no choice but to accept any deal the US negotiates with Iran, because the US president “calls the shots”. He told Fox News and Axios he would press Netanyahu not to retaliate against Tehran.

Note: As of 4 pm EDT 5 June 2026

Currencies

EUR -0.73% to $1.1524

GBP -0.63% to $1.3336

Bitcoin -3.88% to $61,156.75

Ethereum -9.85% to $1,598.01

The dollar rose on Friday after better than expected jobs data reinforced expectations that the Fed would keep interest rates higher for longer. The dollar Index ended the day +0.64% to 100.05 . The euro was down -0.73 to $1.1524, while the British pound weakened -0.63% to $1.3336.

The Japanese yen was -0.11% against the dollar to ¥160.19 per dollar as Japanese officials increased warning around the yen, implying possible further intervention from Tokyo. Data on Friday showed Japan's foreign reserves fell by $77 billion in May.

Fixed Income

US 10-year Bond +7.1 basis points to 4.544%

German 10-year Bund +1.8 basis points to 3.039%

UK 10-year gilt -0.2 basis points to 4.909%

US Treasuries rallied on Friday after stronger than expected nonfarm payrolls led to curve flattening. Consensus estimates were 85 - 90,00 new jobs created, however, May’s nonfarm payrolls came in at 172,000 jobs after rising by an upwardly revised 179,000 in April. with inflation remaining at the 4.3% level. This strong job growth combined with elevated oil prices, driven by supply disruptions from the war with Iran, is increasing concerns that fears that inflation could become entrenched in core consumer prices — the measure the Fed watches most closely when setting policy

The 2-year note yield, which typically moves in step with Fed interest rate expectations, jumped +11.3 basis points to 4.160%, the highest since February 2025. The yield on the benchmark 10-year notes rose +7.1 basis points to 4.544%. At the long end, the 30-year Treasury bond yield +3.2 bps to 5.009%

The yield curve between 2- and 10-year notes flattened to 38.4 basis points.

According to CME Group's FedWatch Tool, Fed funds futures traders are now pricing in a 4% probability of a 25 bps rate cut at June’s FOMC meeting, compared to a 0.4% probability last week.However, Friday’s strong payrolls pushed expectations of a Fed rate rise to 69% by December, up from 46% before the data was released.

Investors will be looking to May’s CPI report, due next Wednesday, for further indications of the Fed rate policy path. The data is expected to show core gaming 0.3% m/o/m and 2.9% annualised, while headline inflation is expected to rise 0.5% m/o/m and 4.2% annualised.

In the euro area, government bond yields ticked higher on Friday for their first weekly rise since mid-May, as investors grew more cautious about the prospects for reopening of the Strait of Hormuz and reacted to stronger than expected US jobs data.

Germany's two-year yield, more sensitive to expectations for policy rates, rose +2.8 basis points to 2.684%. Germany's 10-year government bond yield, the eurozone benchmark, was up +1.8 bps at 3.039%. At the long end, Germany’s 30-year yield was +1.8 bps to 3.579%.

Attention remains on this week's ECB policy meeting, with investors watching for signals about the future path of rates. Money markets are pricing a European Central Bank deposit rate of around 2.65% by December, implying two 25-bp hikes and a 60% chance of a third move. They also see more than a 90% chance of a first rate rise this month, followed by another in September.

Italy's 10-year government bond yield climbed +2.8 bps to 3.792%.

The spread between Italy’s 10-year BTP and the 10-year Bund rose to 75.3 bps, +1 bp from Thursday’s 74.3 bps.

Note: As of 4 pm EDT 5 June 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

Tento článek je poskytován pouze pro informační účely a neměl by být považován za nabídku nebo výzvu k nákupu nebo prodeji jakýchkoli investic nebo souvisejících služeb, jejichž odkazy se v něm můžou vyskytovat. Obchodování s finančními nástroji je spojeno se značným rizikem ztráty a nemusí být vhodné pro všechny investory. Dřívější produktivita není spolehlivým ukazatelem budoucí produktivity.

Přihlásit se k odběru přehledů trhu

Přihlásit se k odběru

přehledů

trhu

Předplaťte si nyní

Založeno profesionály. Pro profesionály.