When will inflation be too uncomfortable for the Fed?

Global macro updates

Growth continues despite inflationary concerns. US services activity continued to pick up in May as businesses strategically placed orders and rebuilt inventories in anticipation of shortages and higher prices because of the war with Iran. On Wednesday, the Institute for Supply Management said the ISM Services Index increased to 54.5 last month from 53.6 in April, marking the 23rd consecutive month in expansion territory. The Business Activity Index increased 1.8 percentage points to 57.7% from April's reading of 55.9%. The New Orders Index came in at 57.3%, 3.8 percentage points above April's figure of 53.5% and 2.6 percentage points higher than its 12-month average reading of 54.7%. However, the Employment Index contracted for the third month in a row; it edged slightly down by 0.1 percentage point to 47.9% from April’s 48% reading. It was also below its 12-month moving average. The survey showed that prices continued to rise, with the Prices Index increasing to 71.3% in May, 0.6 percentage point above April's figure of 70.7%, its highest reading since August 2022. The index has exceeded 60% for 18 straight months. Diesel, gasoline, oil and related commodities were once again most frequently mentioned as up in price in May. The Supplier Deliveries Index came in at 55.2%, 1.6 percentage points lower than April’s 56.8%. May was the 18th consecutive month that the index has been in expansion territory, indicating slower supplier delivery performance. Supplier Deliveries is the only index that is inverse; a reading of above 50% indicates slower deliveries, which is typical as the economy improves and customer demand increases.

Further signs that the economic activity increased in May came from the latest Fed Beige book released on Wednesday, which showed that overall economic activity increased at a slight to moderate pace in 10 of the 12 Fed districts. Most districts described a “low fire, low hire” labour market, with hiring remaining primarily focussed on critical roles or attrition replacement. Additionally, the May ADP JOLTS report indicated that private sector employment increased by 122,000 jobs in May and pay was up 4.4% year-over-year. This was the largest increase in jobs added since January 2025, suggesting that the labour market remains strong despite rising energy and other input costs resulting from the war with Iran. The Beige book also noted that there were inflationary pressures stemming directly from the increase in energy prices as well as secondary effects. However, while growth is so far holding up amid higher costs, businesses expressed concern over deteriorating customer sentiment. US consumers are feeling the pinch, with inflation rising 3.8% in April. So although businesses may be benefitting from a short term strategic order boom, there is an increasing probability that as second round effects from surging energy prices are felt more broadly throughout the economy, it could restrain consumer spending and economic growth this quarter. With mid-term elections only a few months away and polls indicating that Americans are growing frustrated with President Trump’s handling of the economy, there will be even more pressure on the Fed to “do something”. However, the Fed cannot fix a supply shock. The expected response to inflation of a rate rise would not be viewed positively by the President or consumers. All eyes will therefore be on what new Fed Chair Kevin Warsh says during this month’s Fed meeting to keep to the Fed’s dual mandate to control inflation while supporting economic growth.

Trump’s tariff redux. On Wednesday, the Trump administration proposed a new set of tariffs on imports from 60 countries. According to the proposal, a 10% tariff rate would apply to imports from Canada, Mexico, the European Union, Taiwan and the UK, while other countries such as China, India, Japan, South Korea, Brazil and Switzerland would be subject to a 12.5% tariff. The administration claims that these countries have failed to curb trade in goods made with forced labour as they either haven’t banned imports made with forced labour or haven’t properly enforced such bans. The US has prohibited the import of goods made with forced labour since 1930. However, according to Bloomberg news, there would be a special mechanism to “allow for a certain volume of apparel and textile imports from certain economies to enter the United States” at a reduced rate. The levies would be applied at the border, with the rates decided by the US Trade Representative after hearings and public comments. The deadline for these is 7 July.

As noted by Reuters, the proposed duties come from probes launched under a separate legal authority known as Section 301 of the Trade Act of 1974. There is also, as noted by Bloomberg news, a separate raft of 301 investigations including a review of US trading partners’ excess manufacturing capacity, the findings of which may also be released soon. President Trump’s previous tariff regime was ruled illegal by the US Supreme Court in February. President Trump immediately imposed a 10% across-the-board tariff using Section 122 in response to that ruling. However, in May the US trade court found those were also unlawful, although they remain in place during the appeal process. The Section 122 tariffs are due to expire on 24 July.

Global market indices

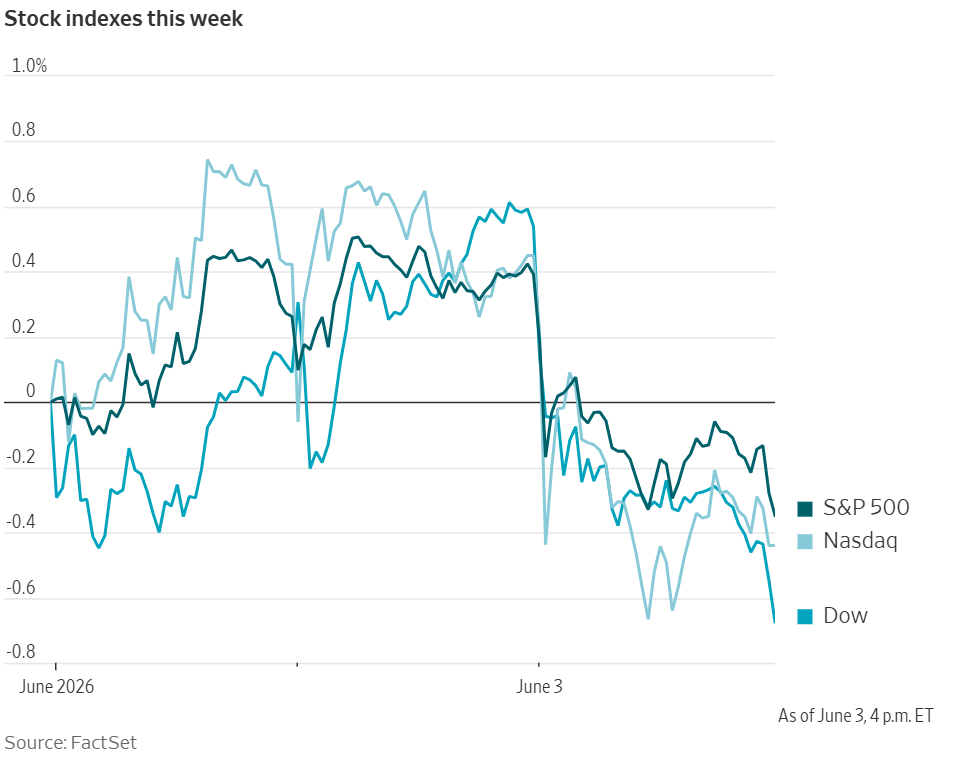

US Stock Indices Price Performance

Nasdaq 100 +0.78% MTD and +21.07% YTD

Dow Jones Industrial Average +0.54% MTD and +6.75% YTD

NYSE -0.07% MTD and +5.78% YTD

S&P 500 -0.35% MTD and +10.35% YTD

The S&P 500 is +0.44% over the past seven days, with 7 of the 11 sectors down MTD. The Equally Weighted version of the S&P 500 is +0.75% over this past week and +0.15% YTD.

The S&P 500 Energy is the leading sector so far this month, +4.28% MTD and -5.48% YTD, while Consumer Discretionary is the weakest sector at -4.35% MTD and -0.66% YTD.

Over the past seven days, Information Technology outperformed within the S&P 500 at +5.14%, followed by Energy and Materials at +3.03% and +0.67%, respectively. Conversely, Communication Services underperformed at -5.84%, followed by Consumer Discretionary and Utilities at -4.84% and -3.26%, respectively.

The equal-weight version of the S&P 500 was -0.42% on Wednesday, outperforming its cap-weighted counterpart by percentage points.

On Wednesday, the rise in oil prices following an attack on Kuwait and Bahrain by Iran caused oil prices to rise, stoking inflation fears, and leading to profit taking by investors, with markets falling for the first time in 10 sessions. The Dow Jones Industrial Average was -1.21%, or down 620.71points, to close at 50,687.07. The S&P 500 was -0.74%, or down 56.10 points, to 7,553.68. The Nasdaq Composite was -0.89%, or down 239.93 points, to 26,853.98. Over the past seven days, the S&P 500 was +0.44%, the Dow Jones Industrial Average was +0.08% and the Nasdaq Composite was +0.67%.

In corporate news, Alphabet increased its equity raise to $84.75 billion from the $80 billion it announced earlier this week to help fund growing artificial intelligence spending plans.

Meta Platforms announced it is selling businesses access to an AI agent for the first time. The company reportedly announced the new product at the WhatsApp-focused Conversations conference in London. The new product expands on existing business messaging services by enabling "agentic" capabilities in which the assistant can take actions on businesses' behalf, like booking calendar appointments and closing sales.

CrowdStrike Holdings raised its revenue guidance for the year on Wednesday despite mounting concerns around hackers being able to attack industries and governments via AI tools. However, its share price fell around 10% in after-hours trading. As noted by The Wall Street Journal, Its shares had risen 91% since the end of March.

SpaceX publicly set a $135 price for shares in its initial public offering next week. The company is aiming to raise $75 billion, the most ever for an IPO. If it achieves this, it would be valued at $1.75 trillion, immediately placing it among the top 10 most valuable US-listed firms

Mega caps: The Magnificent Seven had a mostly negative performance over the past week. Over the last seven days, Microsoft +3.55% and Nvidia +1.01% while Apple -0.19%, Meta Platforms -1.93%, Tesla -3.78%, Alphabet -7.67% and Amazon -8.03%.

Energy stocks had a largely positive performance this week. The Energy sector itself was +3.03%. WTI and Brent prices are +7.57% and +3.13%, respectively, over the past week. Over the last seven days, Marathon Petroleum +8.16%, BP +6.00%, Phillips 66 +5.76%, Occidental Petroleum +4.83%, Shell +4.76%, APA +4.67%, Chevron +4.01%, Halliburton +3.61%, ConocoPhillips +3.40%, ExxonMobil +3.13% and Baker Hughes +1.69%, while Energy Fuels -0.91%.

Materials and Mining stocks had a mixed performance this week, with the Materials sector itself +0.67%. Over the past seven days, Freeport-McMoRan +11.02%, Celanese Corporation +4.82%, Nucor +4.57%, Yara International +3.12%, CF Industries +0.22%, Yara International +3.12%, CF Industries +0.22% and Newmont Corporation +0.22%, while Mosaic -1.77%, Sibanye Stillwater -4.80% and Albemarle -5.14%.

European Stock Indices Price Performance

Stoxx 600 -0.77% MTD and +4.90% YTD

DAX -1.23% MTD and +1.25% YTD

CAC 40 -0.40% MTD and +0.01% YTD

IBEX 35 -1.02% MTD and +5.02% YTD

FTSE MIB +1.08% MTD and +12.54% YTD

FTSE 100 -0.74% MTD and +4.04% YTD

This week, the pan-European Stoxx Europe 600 index is -1.11%. It was -0.66% on Wednesday, closing at 621.19.

So far this month in the STOXX Europe 600, Technology is the leading sector +4.22% MTD and +24.77% YTD, while Health Care is the weakest at -4.17% MTD and -6.57% YTD.

Over the past seven days, Technology outperformed within the STOXX Europe 600, at +6.14%, followed by Basic Resources and Oil & Gas at +3.22% and +2.31%, respectively. Conversely, Health Care underperformed at -4.72%, followed by Food & Beverages and Insurance at -4.43% and -4.31%, respectively.

Germany's DAX index was -1.31% on Wednesday, closing at 24,795.94. It was -1.52% over the past seven days. France's CAC 40 index was -0.71% Wednesday, closing at 8,150.42. It is -0.70% over the past week.

The UK's FTSE 100 index was -1.64% over the past week to 10,373.51. It was -0.40% on Wednesday.

In European equities, Financial Services underperformed after Partners Group declined on reports that it had restricted redemptions in one of its evergreen private-equity funds following elevated withdrawal requests, reviving concerns over liquidity in private markets. Broader unease regarding private credit exposure and redemption pressures was exacerbated by reports that Cliffwater’s main private credit fund faced an ~17% withdrawal request in Q2. Autos & Parts also underperformed as investors rotated out of cyclical sectors.

Basic Resources lagged despite firmer commodity prices, with profit-taking evident across mining stocks, while Rio Tinto declined following a downgrade by RBC. Chemicals also moved sharply lower, led by Akzo Nobel after Nippon Paint and Sherwin-Williams abandoned efforts to acquire the company, thereby removing a significant takeover premium from the shares. BASF traded lower after the European Commission conditionally approved Carlyle Group’s acquisition of BASF’s coatings business.

Retail outperformed as investors reacted positively to a strong set of consumer updates, led by Inditex after it reported Q1 earnings ahead of expectations and highlighted an encouraging start to summer trading, helping to ease concerns about consumer demand and inflation pressures. B&M European Value Retail shares surged after reporting FY EPS above consensus, while Howden Joinery advanced following its £390 million acquisition of DIY Kitchens.

Oil & Gas also outperformed as Brent crude rose on reports of Iranian missile activity targeting regional assets and amid continued concerns over stability in the Middle East as the US and Iran exchanged fire. BP gained following reports that it had held advanced discussions of a potential £2 billion disposal of North Sea assets to Ithaca Energy. Utilities and Telecom also advanced as investors rotated into more defensive sectors amid renewed geopolitical uncertainty in the Middle East and the Persian Gulf.

Other Global Stock Indices Price Performance

MSCI World Index +0.29% MTD and +10.12% YTD

Hang Seng +1.79% MTD and +0.01% YTD

Over the past seven days, the MSCI World Index and Hang Seng Index are +1.05% and +1.20%, respectively.

Currencies

EUR -0.49% MTD and -1.23% YTD to $1.1599

GBP -0.25% MTD and -0.39% YTD to $1.3417

The US dollar rose on Wednesday to a two month high due to escalating geopolitical tensions in the Middle East and strong domestic labour market data that raised the likelihood of the Fed raising rates sooner rather than later.

The dollar index was +0.31% to 99.53, while the euro fell -0.28% to $1.1599. Over the past week, the dollar index is +0.33%. The euro fell -0.22% over the past seven days. This is despite eurozone inflation rising higher than expected last month to 3.2%, meaning a rate increase next week is almost fully priced in.

Sterling also fell on Wednesday, -0.32% to $1.3417. Over the past week, the pound has edged down -0.05% against the US dollar.

The dollar rose +0.10% against the Japanese yen on Wednesday to ¥160.07 per dollar, the lowest level since April. Over the past week, the dollar has gained +0.35% against the yen. Against the yen, the dollar is +0.50% MTD and +2.17% YTD. With the yen passing the unofficial threshold of ¥160, the BoJ will likely intervene in the foreign exchange market to prevent further depreciation. Traders see roughly a 75% chance of a June rate hike in Japan.

Note: As of 5:00 pm EDT 3 June 2026

Cryptocurrencies

Bitcoin -11.14% MTD and -25.57% YTD to $65,162.73

Ethereum -11.16% MTD and -39.88% YTD to $1,785.11

Bitcoin was -12.37% over the last seven days and Ethereum was -11.72%. On Wednesday, Bitcoin was -2.28% and Ethereum -3.93%. Earlier in the day Bitcoin had fallen 4% to $64,721.39, the lowest since 28 February. The drop in Bitcoin and Ethereum this week was part of a broader cryptocurrency market decline as investors reacted to continued outflows from Spot Bitcoin ETFs and corporate selling, particularly the news that software company and noted Bitcoin holder Strategy, sold 32 Bitcoins between May 26 and May 31 for approximately $2.5 million. High conviction long-term holders of Bitcoin — defined as those who have held onto their coins for at least 155 days — have also started to sell Bitcoin.Escalating geopolitical tensions in the Middle East have also weighed on cryptocurrencies over the past week, with oil prices increasing and the consequent rise in inflationary expectations and higher interest rates, creating a more risk-off environment. One potential support, the passage of the Digital Asset Market Clarity Act in the US, which would create a defined regulatory market structure for cryptocurrencies, looks increasingly unlikely as there are only 8 weeks left before the Senate breaks for the summer. Despite the bill advancing to the Senate, there are still strong objections by some Democrats who are insisting on the inclusion of an ethics provision.

Note: As of 5:00 pm EDT 3 June 2026

Fixed Income

US 10-year yield +5.7 bps MTD and +32.8 bps YTD to 4.500%

German 10-year yield +9.6 bps MTD and +17.8 bps YTD to 3.038%

UK 10-year yield +11.5 bps MTD and +45.8 bps YTD to 4.936%

US Treasury yields moved higher on Wednesday as investors assessed inflation risks linked to the Middle East conflict alongside fresh signals from Fedspeak and the latest Beige Book survey.

The yield on the 10-year US Treasury note rose +5.4 bps to 4.500%, marking its largest daily increase in two weeks, while the 30-year yield advanced +3.4 bps to 4.993%.

The US Treasury yield curve, measured by the spread between yields on two- and 10-year Treasury notes, stood at 41.4 bps, 3.1 bps narrower than the previous week’s 44.5 bps.

The 2-year US Treasury yield, which is particularly sensitive to expectations for the Fed funds rate, rose +3.5 bps to 4.086%.

New York Fed President John Williams reiterated that he does not believe the Fed needs to adjust short-term interest rates at present, despite upside inflation risks stemming from the Middle East conflict and other factors.

The Fed’s Beige Book indicated that economic activity increased modestly in recent weeks, employment was little changed and the effects of higher energy prices linked to the war were evident across the economy.

The US yield curve bear-flattened over the course of the week. At the front-end, the 2-year yield was +4.7 bps higher over the past seven days, the 10-year yield advanced +1.6 bps, and, at the longer end, the 30-year yield traded -2.0 bps lower.

According to CME Group's FedWatch Tool, Fed funds futures traders are now pricing in a 1.6% probability of a 25 bps rate cut at June’s FOMC meeting, compared to 0% from last week. Fed funds futures traders are pricing in 19.0 bps of rate hikes in 2026, higher than the 15.3 bps of rate hikes priced in a week ago.

Across the Atlantic, in the UK, Britain’s 10-year Gilt yield +7.1 bps to 4.936%. On a weekly basis, the 10-year Gilt yield is +9.0 bps.

Euro area government bond yields moved higher on Wednesday as markets increased their expectations for further ECB tightening, with pricing implying a greater than 50% probability of three 25 bps rate hikes by year-end. Money markets currently price the ECB deposit rate at 2.66% by December, implying two further increases and approximately a 65% probability of a third move.

Markets are assigning a 90% probability to an initial 25 bps rate increase to 2.25% at the 11 June meeting, with a further increase likely in September, as policymakers continue to balance persistent energy-driven inflation against signs of economic weakening. Investors remain focused on the ECB’s forward guidance, while the prospect of higher fiscal spending in the future is also drawing close market attention.

Germany’s 2-year Schatz yield, particularly sensitive to expectations for the ECB deposit rate, rose +4.9 bps to 2.683%.

Germany’s 10-year government bond yield increased +5.7 bps to 3.038%. At the long end of the yield curve, Germany’s 30-year bund yield advanced +5.1 bps to 3.575%.

Italy’s 10-year BTP yield rose +8.2 bps to 3.773%, while the spread over German Bunds stood at 73.5 bps, or 2.0 bps higher than last week’s 71.5 bps. Over the past seven days, the 10-year BTP yield has increased +7.8 bps.

Italy’s 10-year BTP yield yield rose +8.2 bps to 3.773%, while the spread over German Bunds stood at 73.5 bps, or 2.0 bps higher than last week’s 71.5 bps. Over the past seven days, the 10-year BTP yield has increased +7.8 bps.

During the past week, the German yield curve bear-flattened as shorter maturities advanced at a higher pace than long-dated maturities. Over the course of the past seven days, the two-year Schatz yield traded +8.6 bps higher, while yield on the 10-year bund increased +5.8 bps. At the longer end, the 30-year German yield moved +4.0 bps higher.

The yield spread between German Bunds and 10-year UK gilts reached 189.8 bps on Wednesday, an increase of 3.2 bps over the past seven days.

The spread between US 10-year Treasuries and German Bunds is now 146.2 bps, reflecting a contraction of 4.2 bps from last week’s 150.4 bps.

Commodities

Gold spot -2.29% MTD and +2.73% YTD to $4,431.78 per ounce

Silver spot -3.39% MTD and +2.02% YTD to $72.70 per ounce

West Texas Intermediate crude +9.62% MTD and +67.57% YTD to $96.20 a barrel

Brent crude +6.39% MTD and +60.88% YTD to $97.87 a barrel

Gold prices declined on Wednesday as expectations that conflict-driven inflation may keep interest rates elevated weighed on sentiment.

Spot gold fell -1.25% to $4,431.78 per ounce. On a weekly basis, spot gold was down -0.57%.

Silver spot prices declined -3.21% to $72.70. It declined -2.55% over the past week.

Oil prices rose more than 2% on Wednesday, building on the previous session’s gains, as renewed Middle East tensions and limited progress in talks between Tehran and Washington supported the market. In addition, US government data published on Wednesday showed total stocks of crude and petroleum products fell to the lowest level since 2004. According to the Financial Times, the US has released about 50mn barrels of crude from the SPR and has authorised the drawdown of 172mn to keep a lid on fast-rising crude and petrol prices.

Brent crude settled up $2.05, or +2.14%, at $97.87 a barrel, while US WTI gained $2.81, or +3.01%, to $96.20. Over the past week, WTI has risen +7.57%, while Brent is up +3.13%.

Overnight, an Iranian missile strike killed one person at Kuwait airport, while two other missiles aimed at Kuwait broke apart mid-flight. US and Bahraini forces intercepted three inbound missiles. The IRGC said it had targeted the US Fifth Fleet and military assets at regional airports, prompting US strikes on targets on Qeshm Island.

Fars reported shortly after 13:00 ET that talks were still underway and no final decisions had been reached. According to the report, Tehran will not accept an agreement that excludes Lebanon, and any eventual deal would be followed by a memorandum of understanding outlining a four-stage implementation process.

Separately, Ukraine struck one of Russia’s largest oil terminals overnight, and the site remains on fire.

Concerns over gasoline inventories also persisted. Vitol said refiners in the Atlantic Basin have made significant progress in easing jet fuel and diesel shortages, but that this has contributed to tighter gasoline supply.

At the port of Fujairah, product stockpiles fell by 307,000 bpd month over month to 5.212 million bpd, marking a new record low.

EIA report. The latest US Energy Information Agency (EIA) report, released on Wednesday, showed that US crude oil refinery inputs averaged 16.9 million barrels per day during the

week ending 29 May. This was 90 thousand barrels per day less than the previous week’s average. Refineries operated at 94.7% of their operable capacity last week. Gasoline production decreased last week, averaging 9.4 million barrels per day. Distillate fuel production increased, averaging 5.2 million barrels per day.

US crude oil imports averaged 6.4 million barrels per day last week. This was an increase of 1.2 million barrels per day from the previous week. Over the past four weeks, crude oil imports averaged about 5.9 million barrels per day. This was 4.5% less than the same four-week period last year. Total motor gasoline imports averaged 780 thousand barrels per day last week and distillate fuel imports averaged 121 thousand barrels per day.

US commercial crude oil inventories (excluding the Strategic Petroleum Reserve) fell by 8.0 million barrels from the previous week. At 433.7 million barrels, US crude oil inventories are about 3% below the five-year average for this time of year. However, total motor gasoline inventories increased by 3.4 million barrels from last week, but are still 5% below the five-year average for this time of year. Both finished gasoline and blending component inventories increased last week. Distillate fuel inventories increased by 1.5 million barrels last week and are about 3% below the five-year average for this time of year. Total commercial petroleum inventories decreased by 2.6 million barrels last week.

Total products supplied over the last four-week period averaged 20.4 million barrels per day. This was up by 3.0% from the same period last year. Over the past four weeks, motor gasoline product supplied averaged 8.8 million barrels per day, up by 0.6% from the same period last year. Distillate fuel product supplied averaged 3.6 million barrels per day over the past four weeks, up by 1.2% from the same period last year. Jet fuel product supplied was up 0.4%

compared with the same four-week period last year.

Note: As of 5:00 pm EDT 3 June 2026

Key data to move markets

EUROPE

Thursday: Retail Sales and a speech by ECB President Christine Lagarde

Friday: Eurozone Employment Change and Eurozone GDP

Monday: German Factory Orders and Eurozone Sentix Investor Confidence

Tuesday: German Industrial Production

UK

Thursday: A speech by BoE Governor Andrew Bailey

Friday: Speeches by BoE External Member Swati Dhingra and BoE Governor Andrew Bailey

Tuesday: BRC Like-for-Like Retail Sales

USA

Thursday: Challenger Job Cuts, Initial and Continuing Jobless Claims, Nonfarm Productivity, Unit Labour Costs and a speech by San Francisco Fed President Mary Daly

Friday: Nonfarm Payrolls, Average Hourly Earnings, Labour Force Participation Rate, Unemployment Rate and U6 Underemployment Rate

Saturday: A speech by Fed Governor Michael Barr

Tuesday: ADP Employment Change 4-week Average and Existing Home Sales Change

Wednesday: CPI and Core CPI

JAPAN

Friday: Labour Cash Earnings

Monday: GDP

CHINA

Tuesday: Exports, Imports and Trade Balance

Wednesday: CPI and PPI

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.