Is Europe’s AI edge being built underground?

Global Macro Updates

The physical layer: how Europe is playing the AI build-out European software stocks were among Monday's strongest performers, with SAP reaching a 10-week high as a rebound in US software, reportedly driven by short covering, lent support across the sector. Analysts have cautioned, however, that while valuations have reset and management teams are addressing AI-related risks more explicitly, volatility remains elevated. According to FactSet data, the STOXX Europe 600 Technology sector has posted the strongest momentum across the Stoxx 600 since last week, at 2.55 %, outperforming the broader index by 3.63 percentage points.

The underpinnings of this rally are more selective than the headline numbers suggest. Goldman Sachs has argued that the recovery in European equities has been driven primarily by earnings resilience rather than a broad re-rating, with gains concentrated in AI-related names, energy and HALO (Heavy Assets, Low Obsolescence) stocks, groups that together now account for roughly 40 % of European market capitalisation. As that concentration deepens, the region's AI prospects are becoming increasingly anchored to physical infrastructure: data centres, power grids and energy supply chains.

As noted by Reuters, this structural theme finds support in TS Lombard's analysis, which identifies Europe's most credible AI winners as picks-and-shovels infrastructure plays rather than software or platform names. Its semiconductor supply-chain basket, anchored by ASML, Infineon Technologies and STMicroelectronics, has risen approximately twenty percent since early April. The AI infrastructure basket, centred on Schneider Electric and Prysmian, is up roughly twenty two percent over the same period. Together, these two cohorts have accounted for more than two-thirds of the positive performance in European equities over the same period. Goldman Sachs' addition of Siemens Energy to its conviction list reinforced this thesis, complementing Schneider Electric's longstanding presence on that same list.

According to Politico, at the policy level, the EU's forthcoming Chips Act 2.0, being shaped by European Commission Technology chief Henna Virkkunen, signals a strategic pivot. Rather than doubling down on the subsidy-led approach to attracting foreign fabrication, exemplified by Intel's since-cancelled mega-fab in Germany, the revised framework is expected to redirect government procurement toward European semiconductor start-ups. The efficacy of this demand-side shift remains to be tested, yet Goldman Sachs has noted that Europe's quieter leaders in semiconductor equipment and materials, including ASML, BE Semiconductor Industries and Soitec, retain genuine strategic relevance in the global AI race, even absent a leading-edge domestic fabrication base.

US Stock Indices

Dow Jones Industrial Average +0.09%

Nasdaq 100 +0.60%

S&P 500 +0.26%, with 2 of the 11 sectors of the S&P 500 up

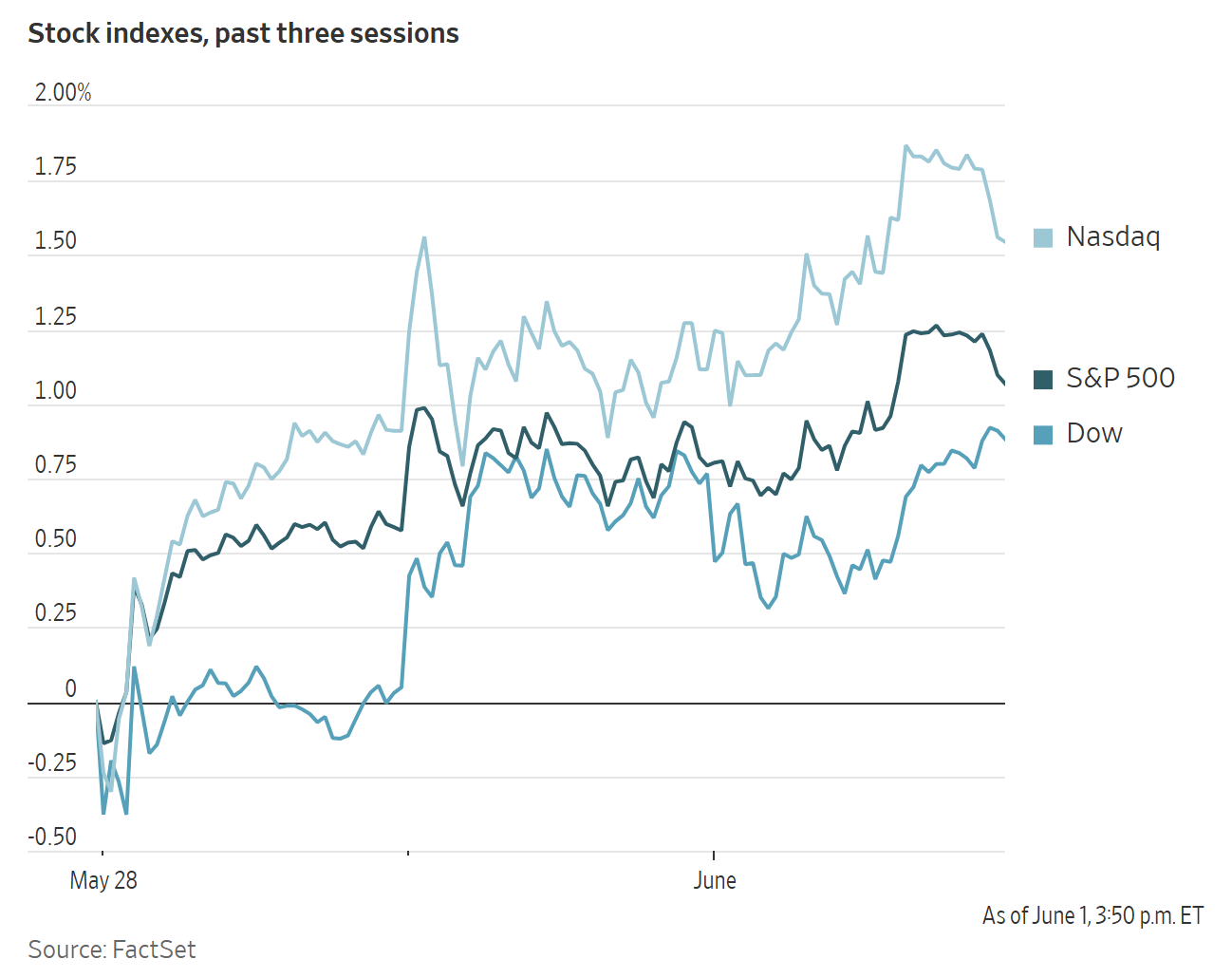

On Monday, all three major US equity indices reached new highs. The Nasdaq Composite was +0.42 %, or 114.19 points to 27,086.81. Although nine of the S&P 500’s 11 sectors closed lower, strong gains in technology and energy helped the index rise +0.26 %, or 19.90 points to 7,599.96, and notched a seven-day winning streak. The Dow Jones was +0.09 %, or 46.42 points higher, to 51,078.88.

In corporate news, Nvidia is moving into the PC market with a new chip designed to challenge Intel’s dominance and help adapt personal computers for the AI era.

Alphabet plans to raise $80 billion in equity, including $10 billion from Berkshire Hathaway, to fund artificial intelligence-related capital spending. Of the remaining $70 billion, $30 billion will be raised through underwritten public offerings, while $40 billion is expected to be sold into the market later this year. Berkshire, now led by CEO Greg Abel, bought nearly 40 million Alphabet shares earlier this year. Alphabet said CapEx could reach as much as $190 billion in 2026 and rise further next year to support AI infrastructure.

Anthropic has confidentially filed draft documents for an IPO, potentially moving ahead of longtime rival OpenAI in reaching the public markets as early as this fall.

Barry Diller’s People, previously known as IAC, has offered to buy the remaining shares of MGM Resorts in a nonbinding proposal that values the company at about $12.4 billion, or $18 billion including debt. People, which already owns 26.1 % of MGM, is seeking to take the company private.

S&P 500 Best performing sector

Information Technology +2.48%, with CDW +12.38%, Gartner +10.72% and Dell Technologies +10.70%

S&P 500 Worst performing sector

Utilities -3.05%, with Constellation Energy -7.66%, Xcel Energy -3.89% and NextEra Energy -3.85%

Mega Caps

Alphabet -1.02%, Amazon -3.47%, Apple -1.84%, Meta Platforms -5.07%, Microsoft +2.28%, Nvidia +6.26% and Tesla -4.57%

Information Technology

Best performer: CDW +12.38%

Worst performer: Qualcomm -8.78%

Materials and Mining

Best performer: Celanese +4.05%

Worst performer: Albemarle -3.00%

Corporate Earnings Reports

Posted on Monday, 1 June from The Pulse, our real-time AI-driven news tool. Available exclusively on the EXANTE Web Platform

Hewlett Packard Enterprise reported second-quarter results with revenue of $10.68bn vs $9.76bn expected and adjusted EPS of $0.79 vs $0.53 expected, up +40% year over year. Cloud and AI revenue reached $7.7bn. The company raised fiscal 2026 guidance to revenue growth of 29% to 33% and adjusted EPS of $3.35 to $3.45. Networking revenue rose +148 % year over year. It also raised its cumulative fiscal 2026 Networks for AI order target to at least $2bn and completed the H3C sale for approximately $3.5bn total pretax consideration. The CEO stated that HPE delivered an exceptional quarter with record-breaking revenue, higher-than-anticipated profitability, and increased free cash flow, reflecting strong execution and healthy demand across the business.

Credo Technology reported Q4 results with revenue of $437mn vs $433mn expected, EPS of $1.16 vs $1.03 estimated, operating income of $217mn vs $204mn estimated, and gross margin of 68% versus 66% estimated. For fiscal 2026, revenue more than tripled to $1.3bn. Q1 guidance showed revenue of $465mn-$475mn vs $465mn estimated and non-GAAP gross margin of 67% to 69%. The company completed the acquisition of DustPhotonics to expand its silicon photonics portfolio for AI infrastructure. Mizuho raised its price target to $260 from $220 while maintaining Outperform. Stifel reiterated Buy and lifted its target to $250 from $200. The chief executive stated that fiscal 2026 marked another defining year for Credo.

European Stock Indices

CAC 40 -0.45%

DAX -0.40%

FTSE 100 -0.68%

Commodities

Gold spot -1.16% to $4,483.29 an ounce

Silver spot -0.60% to $74.81 an ounce

West Texas Intermediate +5.37% to $92.47 a barrel

Brent crude +3.63% to $95.33 a barrel

Gold prices declined on Monday, with spot gold falling -1.16% to $4,483.29 per ounce after reaching a two-week high on Friday.

A firmer US dollar made dollar-denominated metals more expensive for buyers using other currencies.

Spot silver fell -0.60% to $74.81 per ounce.

Oil prices settled more than three percent higher on Monday after Iran’s Tasnim news agency reported that Tehran had suspended indirect negotiations with Washington and that contingency plans were being considered to block the Strait of Hormuz and disrupt other strategic shipping routes. The report intensified market concerns over supply security and added to existing geopolitical risk premiums.

Regional tensions have escalated sharply in recent days. Iran and the US have exchanged strikes, while Israel has ordered troops deeper into Lebanon as fighting with the Iran-backed Hezbollah group intensifies.

Brent crude futures settled at $95.33 per barrel, up $3.34, or +3.63 %, while US WTI futures closed at $92.47 per barrel, gaining $4.71, or +5.37 %. Both benchmarks had risen by more than six percent earlier in the session before trimming gains after the US President said he was unaware of any suspension in talks with Iran and had also received assurances, through intermediaries, that Hezbollah would not launch an attack on Israel.

Earlier gains were driven by a series of military and diplomatic developments. Markets reacted first to reports that Iran had shot down a US MQ-1 drone over international waters, followed by US retaliatory strikes on Iranian radar and drone facilities. Additional support came from reports that Iran had launched missiles and drones toward Kuwait, including an attack affecting a US base, and from Israel’s decision to expand military operations in Lebanon against Hezbollah. Price momentum strengthened further after Tasnim reported that Iran would halt dialogue through intermediaries and, together with allied groups, could move to block the Strait of Hormuz and threaten the Bab el-Mandeb Strait. Sentiment later moderated after the US President stated that talks with Iran were continuing and that hostilities between Israel and Lebanon would cease.

Ukraine continued its attacks on Russian oil refineries, with two additional facilities reportedly targeted since the weekend. Russia has extended its ban on aviation fuel exports through 30 November. Reports also indicate that some cities near Moscow have begun limiting the volume of gasoline and diesel purchases available to consumers.

Russia’s government plans to boost fuel imports from Belarus and tighten controls on gasoline and diesel exports to protect domestic supply, RBC reported on Monday, citing two sources familiar with the matter. The report added that officials are also considering a two-month ban on gasoline exports.

Kazakhstan has restored oil output to 290,000 metric tons per day after earlier disruptions at the Tengiz oilfield, Energy Minister Erlan Akkenzhenov said on Monday.

Venezuela’s oil exports edged up to 1.25 million barrels per day (bpd) in May, marking a third straight monthly increase, driven by higher shipments to the US, India, and Europe, according to shipping data released on Monday.

According to Reuters sources within OPEC+, the group’s seven participating members are expected to raise combined output quotas by 188,000 bpd starting in July when they meet this weekend.

Note: As of 4 pm EDT 1 June 2026

Currencies

EUR -0.21% to $1.1634

GBP +0.00% to $1.3454

Bitcoin -3.24% to $70,957.15

Ethereum -0.75% to $1,992.11

The US dollar strengthened on Monday.

The dollar index rose +0.24% to 99.18, recovering after a -0.38% decline last week.

The euro fell -0.21% to $1.1634, while sterling was flat at $1.3454.

Market attention is firmly focused on a speech by BoJ Governor Kazuo Ueda on Wednesday for guidance on whether the central bank will proceed with a rate increase next week.

Although policymakers have yet to reach a consensus, Reuters reported that a pause in the BoJ’s tapering of government bond purchases is increasingly seen as the preferred option by some officials familiar with the deliberations. The yen weakened -0.21% to ¥159.60 per dollar.

Fixed Income

US 10-year Bond +1.0 basis points to 4.453%

German 10-year Bund +6.5 basis points to 3.007%

UK 10-year gilt +7.7 basis points to 4.898%

US Treasury yields moved higher on Monday, although they retreated from their intraday peaks.

The yield on the US 10-year Treasury note ended the session +1.0 bps to 4.453% after reaching 4.518% earlier in the day.

The yield on the 30-year Treasury bond fell -0.1 bps to 4.971% after earlier touching 5.028%. At the front end of the curve, the two-year Treasury yield, which closely tracks expectations for the Fed funds rate, rose +2.5 bps to 4.035% after reaching 4.090%, its highest level since 22 May.

The spread between two-year and 10-year Treasury yields stood at 41.8 bps.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing 16.4 bps of rate hikes in 2026, lower than the 24.6 bps priced in a week ago. Fed funds futures traders are now pricing in a 1.6% probability of a 25 bps rate cut at June’s FOMC meeting, compared to a 4.0% probability of a rate hike last week.

Euro area government bond yields also rose on Monday.

Germany’s two-year yield, which is sensitive to expectations for the ECB’s deposit rate, rose +7.4 bps to 2.627%.

Money markets were pricing in around 65 bps of ECB tightening this year, up from 55 bps on Friday. Traders also viewed a 25 bps rate increase this month as almost certain. The ECB’s main policy rate currently stands at 2.0%.

Germany’s 10-year government bond yield rose +6.5 bps to 3.007%. Italy’s 10-year BTP yield increased +8.3 bps to 3.736%, leaving the spread over Bunds at 72.9 bps.

At the long end of the German curve, the 30-year yield advanced +4.8 bps to 3.543%.

Note: As of 4 pm EDT 1 June 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.