Will IPOs trigger a rotation out of mega-cap tech?

Key data to move markets today

EU: Eurozone, Spanish, Italian, French and German HCOB Composite and Services PMIs, Eurozone PPI and speeches by ECB Executive Board Members Frank Elderson and Piero Cipollone

UK: BoE Monetary Policy Report Hearings and S&P Global Composite and Services PMIs

US: ADP Employment Change, S&P Global Composite and Services PMIs, Factory Orders, ISM Services PMI, ISM Prices Paid, ISM Employment Index, ISM New Orders Index, Fed’s Beige Book and a speech by Fed Governor Michael Barr

JAPAN: A speech by BoJ Governor Kazuo Ueda

Global Macro Updates

April job openings exceeded expectations, while the quits rate edged lower. April JOLTS job openings rose to 7.618 million, above consensus expectations of approximately 6.850 million and up from the prior 6.887 million, which was revised higher from 6.866 million. Hires declined to 5.116 million from 5.535 million, while the quits rate eased to 1.9% from 2.0% in March. Pre-release commentary had generally anticipated little month-over-month change, based on online job-posting trends and relatively stable jobless claims.

The JOLTS report marks the first release in a busy week for labour-market data. The May ADP private payrolls report, due today, is expected to show job growth of 125,000 following April’s increase of 109,000. Analysts have also highlighted strength in ADP’s preliminary weekly job-growth data, with the latest release estimating average private-sector job creation of 35,750 per week over the four weeks ended 9 May.

Attention will then turn to the May nonfarm payrolls report, scheduled for release on Friday at 8:30 am ET. Consensus expectations call for an increase of approximately 90,000 jobs, with the unemployment rate holding steady at 4.3% and average hourly earnings rising 0.3%, following a 0.2% increase in April.

Preview commentary has pointed to low and relatively stable jobless claims, supportive signals from ADP’s weekly releases and likely weather-related benefits for several industries. At the same time, some analysts have cautioned that recent payroll strength could ultimately be revised lower.

Equity supply is drawing increased scrutiny ahead of upcoming IPOs. With several IPOs on the horizon and Alphabet’s proposed $80 billion equity offering in the pipeline, market commentary has increasingly focused on the implications of positive net equity supply after several years of de-equitisation.

Rising equity supply could place pressure on market return on equity, which is currently near a record twenty percent. Additionally, an issuance on the scale of Alphabet’s proposed $80 billion raise would have shifted net equity supply in Q4 2025 from negative $44 billion to positive $40 billion.

Another point of focus is whether investors will fund upcoming IPO participation by rotating out of large-cap technology shares. Bank of America strategists have argued that increased IPO activity could absorb available capital and prompt investors to sell recent winners in order to buy newly issued shares.

Goldman Sachs strategists recently raised their 2026 IPO volume forecast to $225 billion from $160 billion and also pointed to an additional $500 billion in supply from expiring lockups. Even so, they argued that equity demand should remain strong enough to absorb new issuance, citing recent IPO performance, supply that remains below the longer-term average relative to overall market size and still-elevated corporate repurchase demand. Their 2026 forecasts call for $1.3 trillion in buybacks versus $1.1 trillion in issuance.

As noted by CNBC, Oppenheimer analysts added that the decision to pursue an equity raise rather than debt financing may indicate that markets are becoming less accommodating toward AI data-centre funding. In their view, this could encourage weaker-positioned companies, including Meta Platforms, to reassess or rationalise spending plans.

US Stock Indices

Dow Jones Industrial Average +0.45%

Nasdaq 100 +0.48%

S&P 500 +0.13%, with 7 of the 11 sectors of the S&P 500 up

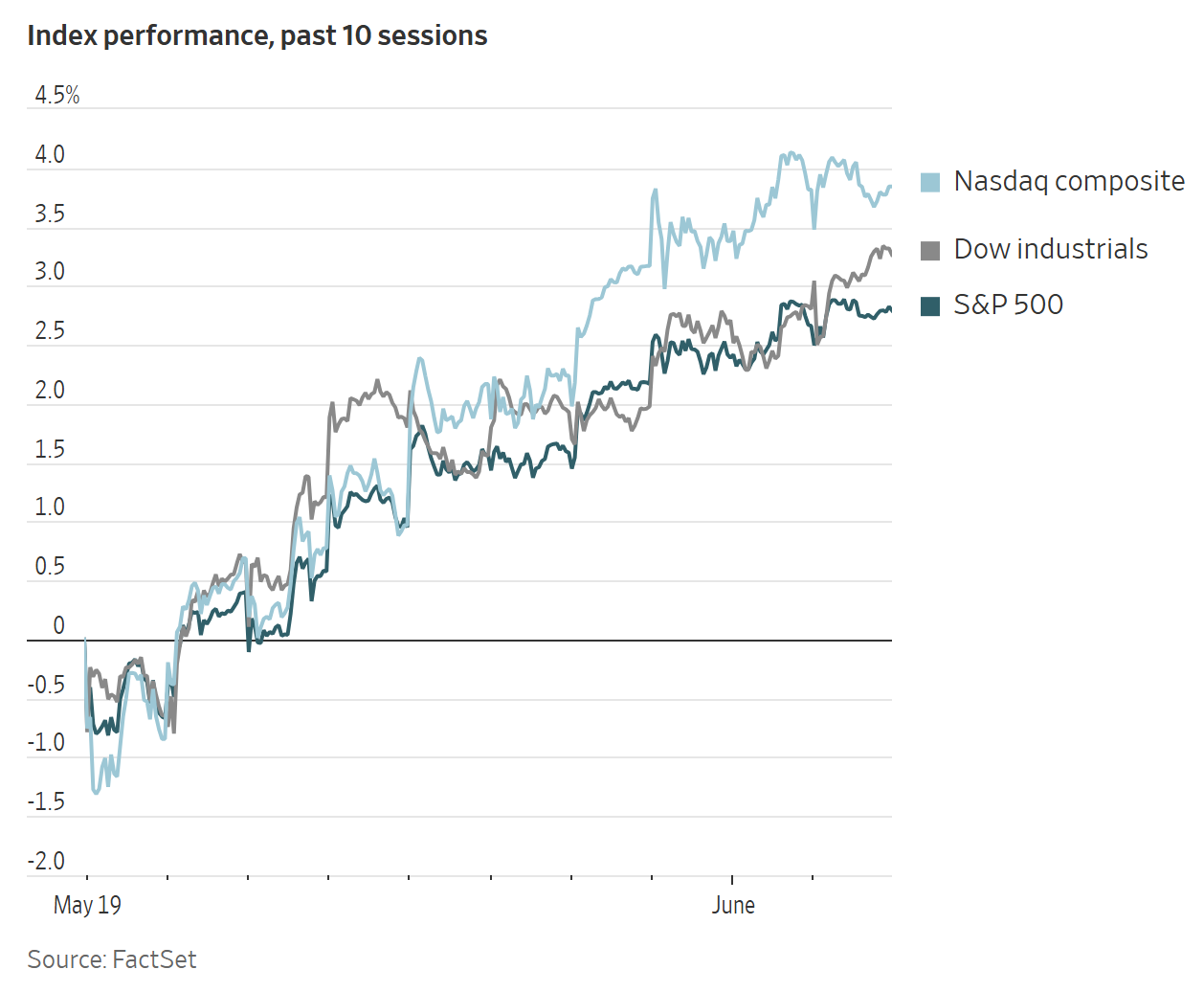

AI-related developments helped lift the S&P 500 to a ninth straight day of gains on Tuesday, marking its longest winning streak since early May 2025.

The S&P 500 rose +0.13% to a record 7,609.78, finishing above 7,600. The index is now up +2.38% over its nine-day advance. The Dow Jones Industrial Average added 228.91 points, or +0.45%, to reach a fresh record high, while the Nasdaq Composite edged up +0.03%.

All three major indices have now posted record closes for five straight sessions, the first time that has happened since February 2017.

In company news, Microsoft unveiled an updated quantum-computing chip, signalling its ambition to build a commercially viable machine by 2029.

OpenAI is broadening its AI coding agent beyond software engineering into additional professions, as it looks to compete more aggressively with rivals such as Anthropic PBC for enterprise customers.

Victoria’s Secret exceeded earnings expectations and raised its outlook, reinforcing signs of progress in CEO Hillary Super’s turnaround effort.

Shares of Marvell Technology rose more than thirty percent on Tuesday after Nvidia CEO Jensen Huang said the company could become the next trillion-dollar business, citing strong demand for AI hardware.

S&P 500 Best performing sector

Utilities +1.93%, with NRG Energy +3.12%, Dominion Energy +2.88% and Eversource Energy +2.85%

S&P 500 Worst performing sector

Communication Services -2.61%, with Match Group -3.92%, Alphabet -3.81% and Netflix -2.94%

Mega Caps

Alphabet -3.81%, Amazon -1.81%, Apple +2.90%, Meta Platforms -0.47%, Microsoft -4.17%, Nvidia -0.69% and Tesla +1.89%

Information Technology

Best performer: Hewlett Packard Enterprise +19.47%

Worst performer: Palo Alto Networks -1.10%

Materials and Mining

Best performer: Freeport-McMoRan +6.98%

Worst performer: FMC -1.57%

Corporate Earnings Reports

Posted on Tuesday, 2 June from The Pulse, our real-time AI-driven news tool. Available exclusively on the EXANTE Web Platform

Dollar General reported first quarter results with EPS of $2.00 vs consensus estimates of $1.89 to $1.90 and net sales of $10.79 billion to $10.8 billion vs estimates of $10.82 billion to $10.83 billion. Comparable sales grew +2% vs an expected +2.09%. The company guided full year EPS to a range of $7.20 to $7.45 vs a consensus of $7.25 and comparable sales growth of +2.2% to +2.7%. The chief financial officer stated the company was pleased with first quarter EPS performance which exceeded expectations and noted positive customer traffic along with balanced category growth.

Palo Alto Networks reported Q3 FY26 results with revenue reaching $3.0bn, up +31% y/y and beating estimates by $0.1bn. Non-GAAP EPS was $0.85, ahead of expectations by $0.05. Remaining performance obligations stood at $18.4bn, up +36% y/y, while next-generation security ARR rose +60% y/y to $8.1bn. The company raised full-year revenue guidance to $11.4bn. CyberArk and Chronosphere contributed $388mn in revenue and $1.6bn in NGS ARR. Palo Alto CEO stated that Q3 was a standout quarter with accelerating organic bookings growth as customers turn to the firm to secure AI deployments at scale.

GitLab reported first-quarter results with revenue reaching $264mn vs $255mn expected, rising +23% y/y. EPS was $0.23 vs $0.21 expected. Remaining performance obligations stood at $1.1bn and the dollar-based net retention rate was 117%. The firm raised its full-year revenue outlook to $1.11bn-$1.118bn and EPS guidance to $0.79-$0.82. It announced a workforce reduction affecting 14% of global employees, equivalent to 350 team members, exiting 22 countries with restructuring charges of $30mn-$35mn expected. GitLab's CFO stated that the team delivered a strong first quarter with 23% revenue growth and 2 points of operating margin expansion.

Ulta Beauty reported Q1 2026 with revenue reaching $3.16bn vs $3.11bn expected, up +11.1% y/y. EPS was $7.74 vs $6.87 expected, up +15.5% y/y. Comparable sales rose +5.3% while operating income increased +11.6% y/y. The company repurchased $555mn of shares. Full-year guidance showed net sales growth of +6% to +7%, comparable sales growth of +2.5% to +3.5% and operating income growth of +6.5% to +9%. Chief executive stated fiscal 2026 is off to a strong start driven by broad-based growth across all channels and major categories.

European Stock Indices

CAC 40 +0.77%

DAX +0.48%

FTSE 100 +0.33%

Commodities

Gold spot -0.10% to $4,487.70 an ounce

Silver spot +0.41% to $75.11 an ounce

West Texas Intermediate +0.99% to $93.39 a barrel

Brent crude +0.51% to $95.82 a barrel

Gold held steady on Tuesday as market participants focussed on developments in the Middle East and upcoming US economic data to gauge their impact on monetary policy.

Spot gold was -0.10% lower at $4,487.70 per ounce after falling as much as two percent on Monday.

Data due this week include the ADP employment report today and Friday’s nonfarm payrolls report. Markets will scan the data for cues on the Fed's policy path.

Spot silver rose +0.41% to $75.11 per ounce.

Oil prices more than 0.5 percentage points to a one-week high in volatile trade on Tuesday as the market waited for news on the Iran war, with Tehran reviewing a proposed agreement with the US to halt the conflict.

Brent futures rose $0.49, or +0.51%, to settle at $95.82 a barrel, while US WTI crude rose $0.92, or +0.99%, to settle at $93.39. Those were the highest closes for both benchmarks since 26 May.

Israel continued its strikes in southern Lebanon on Tuesday, extending its campaign against Hezbollah a day after Trump urged Netanyahu not to target Beirut in order to avoid further escalation in the three-month conflict.

Fars News reported that exchanges between Tehran and Washington on a proposed MOU had stopped several days earlier after Israel threatened to bomb Beirut. US Secretary of State Rubio said that, although Iran no longer has a navy, it still has significant drone capabilities. He added that the initial understanding with Iran was that if it reopened the strait, the blockade would be lifted.

Additionally, Secretary of State Rubio told lawmakers on Tuesday that Iran had agreed to discuss parts of its nuclear programme it had previously refused to address, while cautioning that this did not ensure a final agreement.

Russian crude exports from western ports rose 15.0% m/o/m in May to 2.5 million barrels per day (bpd), the highest monthly average since Sept-2025, as Ukrainian strikes on refineries left more crude available for export. Ukraine has hit at least 16 refineries since May, the highest monthly total since the war began. It has hit two more so far this month. Reports on Monday pointed to gasoline shortages in and around Moscow. Russia’s Energy Ministry said it is developing additional measures to ensure stable domestic gasoline supplies.

Brazil’s oil output reached a record 4.334 million bpd in April, up 2.2% m/o/m and more than 19.0% y/o/y, according to ANP.

Speaking at an S&P Global event in London, Vitol Managing Director Tom Baker said the oil market is underpricing war-related risks. He noted that China’s imports are down by nearly 5.0 million bpd and said that volume would eventually need to return.

Iraq has joined other Gulf countries seeking to reduce reliance on the Strait of Hormuz, announcing plans to raise pipeline exports to 770,000 bpd within three months from about 225,000 bpd currently.

Note: As of 4 pm EDT 2 June 2026

Currencies

EUR -0.05% to $1.1628

GBP +0.04% to $1.3460

Bitcoin -4.90% to $67,477.28

Ethereum -0.75% to $1,897.74

The dollar traded within a tight range on Tuesday, with the dollar index up +0.03% at 99.21. Since 15 May, it has remained confined to a 98.90 – 99.50 range.

The euro slipped -0.05% to $1.1628, while sterling edged up +0.04% to $1.3460.

Japan’s Finance Minister Satsuki Katayama said authorities stand ready to act in currency markets if needed, but declined to comment on recent moves.

The yen weakened -0.19% to ¥159.91 per dollar on the day.

Investors are now focused on a speech later today by BoJ Governor Kazuo Ueda for signals on whether the central bank will raise rates next week.

Fixed Income

US 10-year Bond -0.7 basis points to 4.446%

German 10-year Bund -2.6 basis points to 2.981%

UK 10-year gilt -3.3 basis points to 4.865%

US Treasury yields edged lower on Tuesday, reflecting a modest pullback following recent upward pressure.

The yield on the 10-year US Treasury note declined by -0.7 bps to 4.446%, after having reached a 16-month high of 4.687% on 19 May.

The 30-year Treasury bond yield also moved lower, falling by -1.2 bps to 4.959%.

Cleveland Fed President Beth Hammack stated on Tuesday that the Fed may need to raise interest rates in the near term to address inflationary pressures that remain elevated and continue to trend in a concerning direction.

The spread between the 2-year and 10-year US Treasury yields narrowed to 39.5 bps, 2.3 bps tighter than Monday’s level.

The 2-year US Treasury yield, sensitive to Fed fund rate expectations, fell by -1.6 bps to 4.051%.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing 15.1 bps of rate hikes in 2026, lower than the 16.6 bps priced in a week ago. Fed funds futures traders are now pricing in a 1.4% probability of a 25 bps rate cut at June’s FOMC meeting, compared to a 1.3% probability of a rate hike last week.

In the euro area, government bond yields also declined on Tuesday, partially reversing Monday’s sharp rise amid continued uncertainty over the macroeconomic outlook.

Germany’s 10-year Bund yield fell -2.6 bps to 2.981%, after climbing +6.5 bps on Monday. On the long-end of the maturity spectrum, the 30-year yield declined by -1.9 bps to 3.524%.

By contrast, Germany’s 2-year yield, sensitive to ECB policy-rate expectations, rose by +0.7 bps to 2.634%, following a +7.4 bps increase in the previous session.

Money markets continued to price in a 25 bps rate increase at next week’s ECB meeting as highly likely, with two such hikes expected this year and a possibility of a third.

Italy’s 10-year yield declined -4.5 bps to 3.691%, partially reversing Monday’s +8.3 bps increase. The spread between Italy’s 10-year BTP and the 10-year Bund narrowed to 71.0 bps, down 1.9 bps from Monday’s 72.9 bps.

Note: As of 4 pm EDT 2 June 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

本文提供给您仅供信息参考之用,不应被视为认购或销售此处提及任何投资或相关服务的优惠招揽或游说。金融工具交易存在重大亏损风险,未必适合所有投资者。过往表现并非未来业绩的可靠指标。

由专业人士创建。 为专业人士。