Will Nvidia outperform sky-high expectations?

What to look out for today

Companies reporting on Wednesday, 20 May: Nvidia, Intuit, Analog Devices, Hasbro

Key data to move markets today

CHINA: PBoC Interest Rate Decision

EU: German PPI, ECB Non-Monetary Policy Meeting and a speech by Dutch central bank Governor Olaf Sleijpen

UK: CPI, PPI, RPI and Retail Sales

US: FOMC minutes and speeches by Philadelphia Fed President Anna Paulson and Fed Governor Michael Barr

Global Macro Updates

Will the April FOMC minutes signal a policy pivot? The minutes of the April FOMC meeting are due today at 14:00 ET. Economists broadly expect a hawkish tone, noting that the meeting included three dissents over the policy statement's easing bias.

Previews also point to growing support among officials for keeping the possibility of further rate increases on the table. In his post-meeting press conference, Fed Chair Jerome Powell said the centre of the Committee was moving toward a more neutral position and that removing the easing bias had been a closer call than in March. The March minutes had noted that ‘some’ officials saw a strong case for describing future policy decisions as ‘two-sided,’ implying that rate hikes remained a possibility.

Sell-side economists will also be looking for additional commentary on the policy implications of inflationary pressures stemming from the Iran war, including both higher energy prices and their broader pass-through into the economy. Goldman Sachs has estimated that the energy shock could keep core PCE inflation close to 3% this year.

Since the meeting, several economists have pushed back the expected timing of Fed rate cuts. Goldman Sachs now expects the first cut in December rather than September, arguing that a fading oil shock and further labour-market softening are still likely, but will take longer to materialise. Bank of America has taken an even more hawkish view, saying rate cuts are unlikely before July 2027, citing persistent inflation and resilient labour-market data.

BoJ Ueda faces bond market pressure. US Treasury Secretary Bessent said in a post on X that he had met BoJ Governor Kazuo Ueda on the sidelines of the G7 meetings in Paris to discuss Japan's resilient economy and the market outlook. He said he had expressed confidence in Ueda's ability to guide monetary policy successfully, described Japan's fundamentals as strong and reiterated that foreign-exchange volatility is undesirable.

Speaking later at a press conference, Ueda did not elaborate on the meeting, as attention had shifted to weakness in the bond market. He said long-term yields had been rising rapidly, citing inflation concerns linked to developments in the Middle East. He also noted that cost pass-through from upstream sectors into the midstream economy had been relatively swift, particularly in petrochemicals and plastics. Ueda added that there is growing concern that these pressures could affect Japan's economic outlook, prices and both monetary and fiscal policy. He also pledged to coordinate closely with the government in monitoring bond-market developments.

With the BoJ due to conduct an interim review of its JGB purchase-reduction plan at the June Monetary Policy Meeting (MPM), Ueda said the deliberations would take account of recent market developments, market functioning and input from the forthcoming meeting with bond-market participants.

These remarks follow an earlier Nikkei report indicating that people close to Prime Minister Takaichi had been expressing caution towards the BoJ's review. Recommendations issued by the Council on Economic and Fiscal Policy on Monday called for an ‘appropriate monetary policy’ that takes account of trends in the supply and demand for funds. A senior Cabinet Office official said this language implied that both JGB purchases and policy rates were under consideration, and added that the BoJ should remain mindful of the prospect of increased bond issuance going forward.

Council member Aida, a well-known reflationist, argued that the BoJ should maintain monthly purchases at JPY 2.1 trillion, the current target end-point for March 2027, beyond 2027 in order to support stable long-term public and private investment. He also said purchases should remain broadly aligned with nominal GDP growth. However, some within the BoJ are pushing back against that view, arguing that such an approach would amount to debt monetisation and maintaining that the pace of tapering should instead depend on the extent of the improvement in market function.

US Stock Indices

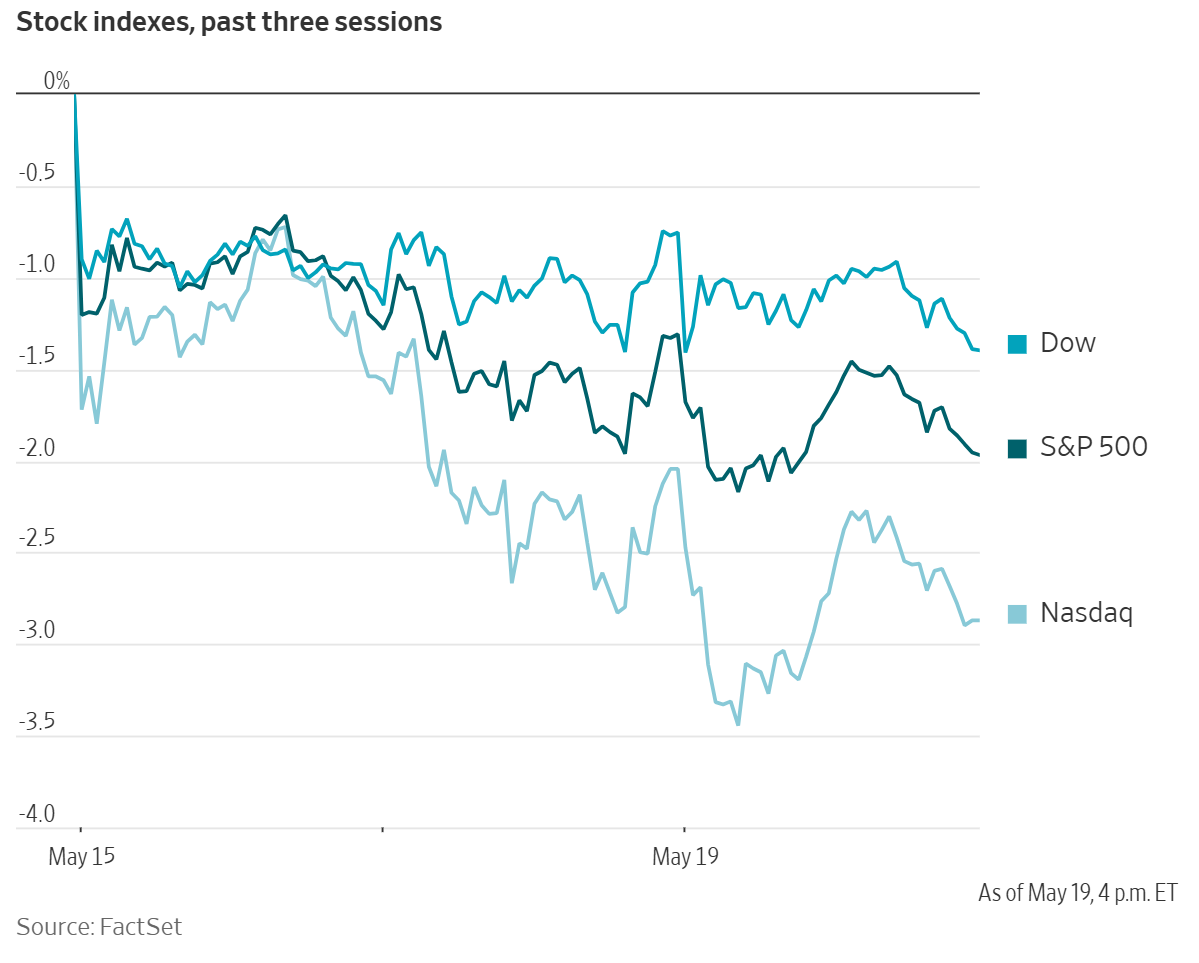

Dow Jones Industrial Average -0.65%

Nasdaq 100 -0.61%

S&P 500 -0.67%, with 6 of the 11 sectors of the S&P 500 down

Major US indices fell on Tuesday as the benchmark 10-year Treasury yield climbed to its highest level in over a year on rising inflation concerns due to elevated energy prices and lack of a peace deal between the US and Iran.

On Tuesday, the Nasdaq and S&P 500 fell for the third session in a row, dragged down by the Technology and Communication Services sectors. The Nasdaq Composite was -0.84%, or down 222.02 points to 25,870.71. The S&P 500 was -0.67%, or down 49.44 points to 7,353.61. The Dow Jones was -0.65%, or down 322.24 points, to 4,363.88.

In corporate news, Cisco Systems’s CFO Mark Patterson warned that the company would see ‘ups and downs’ with its gross profit margin as it pushes further into AI infrastructure.

CoreWeave shares fell after The Wall Street Journal reported that Alphabet and Blackstone were planning to launch an artificial-intelligence cloud company aimed at competing with CoreWeave, using Google's specialised chips. Shares in CoreWeave rival Nebius also moved lower.

ArcelorMittal said it had reduced its stake in Vallourec, a French steel-tube manufacturer.

S&P 500 Best performing sector

Health Care +1.09%, with Eli Lilly +3.37%, Becton, Dickinson and Company +3.23% and Baxter International +3.04%

S&P 500 Worst performing sector

Materials -2.27%, with FMC -5.83%, Smurfit Westrock -4.63% and Newmont -4.33%

Mega Caps

Alphabet -2.34%, Amazon -2.08%, Apple +0.38%, Meta Platforms -1.41%, Microsoft -1.44%, Nvidia -0.77% and Tesla -1.43%

Information Technology

Best performer: Micron +2.52%

Worst performer: Akamai Technologies -6.25%

Materials and Mining

Best performer: CF Industries +2.11%

Worst performer: FMC -5.83%

Corporate Earnings Reports

Posted on Tuesday, 19 May from The Pulse, our real-time AI-driven news tool. Available exclusively on the EXANTE Web Platform

Home Depot reported Q1 results before the open with adjusted EPS of $3.43 vs $3.41 expected and net sales of $41.8bn up 4.8% y/y. Comparable sales rose +0.6% y/y. The company reaffirmed its fiscal 2026 guidance with full-year comparable sales expected at approximately +2%. Home Depot said the core shopper remains resilient despite higher gas prices. CEO stated results were in line with expectations and underlying demand was relatively similar to fiscal 2025 despite greater consumer uncertainty and housing affordability pressure.

European Stock Indices

CAC 40 -0.07%

DAX +0.38%

FTSE 100 +0.07%

Commodities

Gold spot -1.85% to $4,481.01 an ounce

Silver spot -5.18% to $74.78 an ounce

West Texas Intermediate +1.25% to $108.59 a barrel

Brent crude +1.54% to $110.99 a barrel

Gold prices fell by more than one percent on Tuesday on a firmer US dollar and as persistent inflation concerns kept interest rate expectations elevated.

Spot gold was down -1.85% at $4,481.01 per ounce. Earlier in the session, prices fell to their lowest level since 30 March.

Spot silver prices fell -5.18% to $74.78 per ounce, after touching an around two-week low earlier in the session.

Oil prices settled higher on Tuesday, despite US Vice President JD Vance stating that Washington and Tehran had made progress in their talks, reducing immediate concerns about a renewed outbreak of military action.

Brent crude for July delivery settled up $1.68, or +1.54%, at $110.99 a barrel. The US WTI crude contract for June delivery, which expired on Tuesday, increased by $1.34, or +1.25%, to $108.59, while the more actively traded July contract rose $1.58, or +1.54%, to $104.03.

According to Iranian state media, Tehran's latest peace proposal to the United States calls for an end to hostilities across all fronts, including Lebanon, the withdrawal of US forces from areas near Iran and reparations for war-related damage. Washington has consistently rejected these conditions.

The US imposed sanctions on an Iranian foreign-exchange house and, according to US officials, on front companies managing transactions on behalf of Iranian banks. In addition, it blocked 19 vessels allegedly involved in transporting Iranian petroleum and petrochemical products to overseas buyers.

According to consultancy Energy Aspects, Chinese state refiners are processing 8.4 million barrels per day (bpd) of crude this month, down from 8.6 million bpd in April and 9.5 million bpd in March. That compares with roughly 10 million bpd before the US and Israel attacked Iran on 28 February, although companies have since brought forward maintenance schedules. Despite these reductions, Reuters sources said gasoline and diesel inventories in China have risen above average 2025 levels.

Attacks on Russian energy infrastructure also continued on Tuesday. According to Reuters industry sources, a drone strike hit the Yaroslavl-3 oil pumping station, while the Moscow refinery, which was struck on 15 May, has suspended operations.

In the UK, the government announced on Tuesday afternoon that it would permit imports of jet fuel and gasoline produced by third parties from Russian crude.

NATO officials are also reportedly considering the deployment of forces to the Strait to escort vessels if the waterway is not reopened by July.

Separately, The New York Times reported that Tehran is preparing a high-volume campaign targeting energy assets in the Gulf, while the Houthis may attempt to shut down the Bab el-Mandeb Strait, a key route for Saudi exports from the Red Sea.

Note: As of 4 pm EDT 19 May 2026

Currencies

EUR -0.43% to $1.1697

GBP -0.23% to $1.3398

Bitcoin -0.12% to $76,959.43

Ethereum -0.86% to $2,117.89

The US dollar rose to a six-week high against the euro on Tuesday.

The greenback was supported by higher Treasury yields, as inflation concerns and uncertainty over how new Fed Chair Kevin Warsh may respond to sustained price pressures continued to bolster demand for the currency.

The dollar index rose +0.37% to 99.33. The euro fell -0.43% to $1.1607, while sterling weakened -0.23% to $1.3398.

Against the dollar, the Japanese yen slipped -0.15% to ¥159.03 per dollar.

Data released on Tuesday showed that Japan's economy expanded faster than expected in the first quarter, reinforcing expectations of a BoJ rate increase in June.

Markets are also awaiting further details of the government's supplementary budget plan, which could place additional strain on Japan's already weakened public finances and put renewed pressure on the yen.

Japanese Finance Minister Satsuki Katayama said on Monday that Japan remains prepared to respond to excessive currency volatility, while seeking to ensure that any intervention to support the yen does not drive US Treasury yields higher.

Investors have been watching closely for further signs of intervention to support the yen. It remains slightly stronger than it was before last month’s intervention by the Japanese authorities for the first time in nearly two years.

Fixed Income

US 10-year Bond +7.8 basis points to 4.671%

German 10-year Bund +4.1 basis points to 3.193%

UK 10-year gilt +3.7 basis points to 5.129%

The global market selloff continued on Tuesday with yields on longer-dated Treasuries climbing to new highs.

The yield on the 10-year Treasury note surged to as high as 4.687%, its highest level since January 2025, before falling back to end the day +7.8 bps at 4.671%.

The 30-year Treasury bond yield hit its highest in 19 years, ending the trading day at +5.6 bps to 5.183% after hitting an earlier high of 5.197%.

The two-year Treasury note yield, which typically moves in step with interest rate expectations for the Fed funds rate, was +6.8 bps at 4.127% after earlier climbing to 4.139%.

The US Treasury yield curve measuring the spread between yields on two- and 10-year Treasury notes was at 54.4 bps, 1.0 bps wider than Monday.

The Treasury Department is slated to auction 20-year bonds today.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing 18.0 bps of rate hikes in 2026, higher than the 9.6 bps priced in a week ago. Fed funds futures traders are now pricing in a 3.3% probability of a 25 bps rate cut at June’s FOMC meeting, higher than last week’s 1.9% probability.

Eurozone government bonds weakened on Tuesday. Yields remained near the multi-year highs reached in an intraday session the day before as investors continued to price in the risk that sustained energy costs could feed into broader inflation and keep the ECB on a tightening path. As a result, moves at the short end outpaced those further along the curve.

Germany's two-year yield rose +5.5 bps to 2.75% and the 10-year Bund yield rose +4.1 bps to 3.193%, its highest level since 2011. The 30-year yield advanced +2.7 bps to 3.700%.

Italy's 10-year yield increased +3.5 bps to 3.964%, leaving the spread over Bunds at 77.1 bps.

Markets are currently pricing in around an 80% probability of a 25 bps ECB rate increase next month, with two additional 25 bps moves seen as likely by year-end.

UK government bonds also came under pressure on Tuesday, with the 10-year gilt yield rising +3.7 bps to 5.129%.

Note: As of 4 pm EDT 19 May 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.