Trump’s moves hit markets

Corporate Earnings Calendar

Global market indices

Currencies

Cryptocurrencies

Fixed Income

Commodity sector news

Key data to move markets

Global macro updates

Corporate Earnings News

Corporate earning calendar 23 January - 29 January 2025

Thursday: Intuitive Surgical, GE Aerospace, Texas Instruments, Union Pacific, Freeport-McMoran, Fair Isaac, McCormick & Co., American Airlines, Alaska Air.

Friday: American Express, Verizon Communications, NextEra Energy, Burberry.

Monday: AT&T, Nucor, Ryanair, SoFi Technologies.

Tuesday: Louis Vuitton, SAP, Boeing, Lockheed Martin, Starbucks, Chubb, Royal Caribbean Cruises, General Motors, Kimberly-Clark, JetBlue Airways.

Wednesday: Microsoft, Meta Platforms, Tesla, ASML, Volvo, T-Mobile US, IBM, Caterpillar, Lam Research, General Dynamics, Hess.

Global market indices

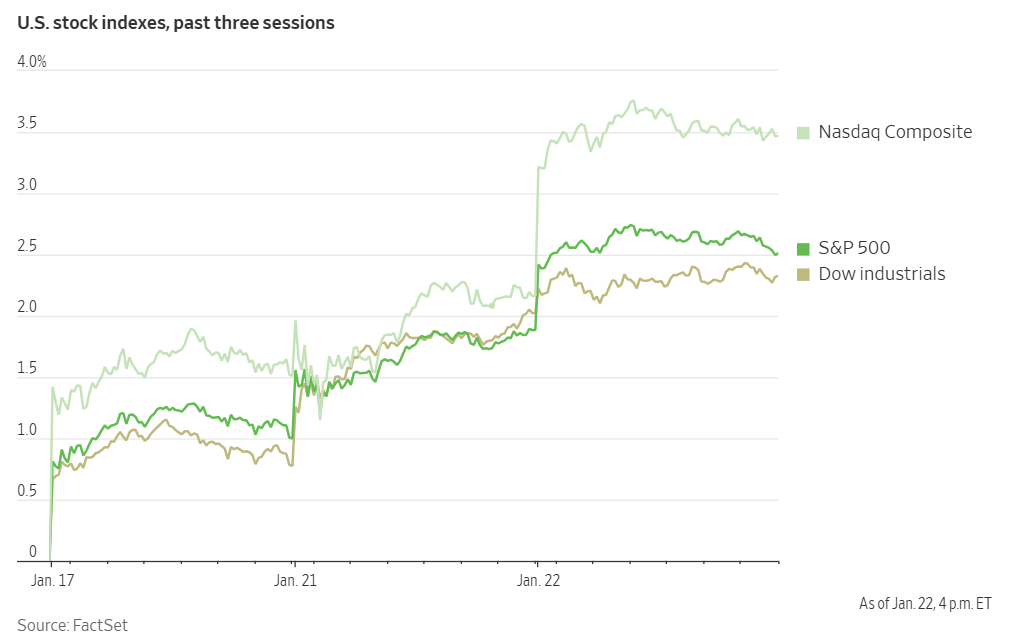

US Stock Indices Price Performance

Nasdaq 100 +3.62% MTD

Dow Jones Industrial Average +3.79% MTD

NYSE +3.83% MTD

S&P 500 +3.48% MTD

The S&P 500 is +2.29% over the past week, with 10 of the 11 sectors up MTD. The Equally Weighted version of the S&P 500 is +2.10% this week, its performance is +3.56% MTD.

The S&P 500 Energy sector is the leading sector so far this month, up +6.58% MTD, while Consumer Staples is the weakest at -0.80% MTD.

This week, Industrials outperformed within the S&P 500 at +3.65%, followed by Information Technology and Real Estate at +3.22% and +2.23%, respectively. Conversely, Energy underperformed at -1.60%, followed by Consumer Staples and Health Care, at +1.07% and +1.13%, respectively.

Investor enthusiasm for AI propelled a stock market rally, driving the tech-heavy Nasdaq Composite up by +1.28%.

Shares of AI-related companies surged following a significant announcement by President Trump: SoftBank, Oracle, and OpenAI pledged a combined $500 billion investment in AI infrastructure within the US. Nvidia, Microsoft, and Arm will also participate in developing this infrastructure for the joint venture, named Stargate.

This news contributed to an extension of this year's market rally, with the S&P 500 briefly surpassing the 6,100 level, and approaching a new record high. However, despite recent attempts to broaden market participation beyond the Magnificent Seven, the majority of companies within the S&P 500 experienced declines on Wednesday.

Overall market performance was mixed. The S&P 500 rose by +0.61%, while the Nasdaq 100 climbed +1.33%. The Dow Jones Industrial Average added +0.30%, but the Russell 2000 was -0.61%. While ongoing developments within the new US administration warrant close observation, investors are advised to remain focused on the underlying economic fundamentals that continue to favour US equities.

In corporate news, Salesforce CEO Marc Benioff expressed optimism for the company's new Agentforce AI product, anticipating ‘thousands’ of deals in Q1 2025.

Samsung Electronics revealed plans to introduce an ultrathin version of its Galaxy S25 phone in H1 2025, aiming to establish a presence in this promising new category ahead of competitor Apple.

Alphabet's Google secured a favourable ruling in a UK court, effectively blocking Russian media firms from seizing the tech giant's global assets. The Russian firms sought to recover court-imposed fines, which have now accrued interest exceeding the combined value of the global economy.

Johnson & Johnson released its Q4 earnings report, causing its shares to fall by as much as -4.1% on Wednesday. The company's 2025 forecast fell short of expectations, primarily due to the adverse effects of a strong US dollar. Johnson & Johnson projected sales of $89.2 billion to $90 billion for the year. Adjusted earnings are expected to be $10.50 to $10.70 per share, a reduction of 25 cents per share attributed to currency fluctuations.

Johnson & Johnson is currently navigating a multibillion-dollar patent cliff as Stelara, its second-biggest drug and a treatment for psoriasis, faces competition from generic alternatives in the US and Europe. The company aims to offset this decline with newer medications, including Darzalex, its leading treatment for blood cancer, and Tremfya, an autoimmune therapy.

Johnson & Johnson's Q4 adjusted EPS were $2.04, with revenue reaching $22.5 billion, both metrics slightly exceeding analyst projections.

Procter & Gamble also reported Q4 earnings. The company's organic sales exceeded estimates, driven by higher sales volume, a departure from previous quarters where growth was primarily attributed to price increases. Organic sales grew by 3% in Q4, representing the most significant increase in three quarters.

Sales were further bolstered by strong performance in P&G's Fabric and Home Care segment, as well as double-digit gains in the Baby, Feminine & Family Care segment. However, the Beauty segment experienced volume declines in Greater China, a region where P&G has acknowledged that lower consumer confidence is impacting business performance.

The company reaffirmed its sales and profit guidance for the current fiscal year, which concludes at the end of June. Procter & Gamble is among the first major US consumer goods companies to report earnings; approximately half of the company's revenue is generated in North America.

US stocks

Mega caps: The Magnificent Seven had a mostly positive performance this week, with the exception of Apple at -10.62%. Alphabet +4.79%, Amazon +7.12%, Meta Platforms +6.49%, Microsoft +5.86%, Nvidia +9.52%, and Tesla +2.79%.

Netflix Q4 earnings. Netflix exceeded expectations in Q4, achieving record subscriber growth. The company added 18.9 million new subscribers, nearly double analysts’ projections and surpassing even the 15.8 million subscribers gained at the onset of the COVID-19 pandemic in early 2020.

Capitalising on this strong performance, Netflix announced price increases across its three US subscription plans. These increases average 13% and include the first-ever price hike for the ad-supported plan, which will rise by $1 from its $6.99 per month launch price in late 2022.

This combination of exceptional subscriber growth and price increases propelled Netflix shares more than +14% in after-hours trading on Tuesday. However, this raises the question of whether Netflix reached its peak performance.

The company has indicated its intention to discontinue reporting subscriber numbers, shifting its focus to revenue and earnings growth as key performance indicators. Netflix attributes this change to the increasing complexity of its business model, which now encompasses advertising and account-sharing options. However, it is also common for companies to cease reporting discretionary metrics when those metrics no longer contribute positively to their growth narrative.

Netflix reported a 16% increase in revenue to $10.2 billion for Q4, marking its strongest gain since Q4 2021. Furthermore, the company anticipates accelerated sales growth in 2025, projecting revenue as high as $44.5 billion, a 14% increase from the previous year, with an operating margin of 29%. For Q1 2025, Netflix forecasts revenue of $10.4 billion and EPS of $5.58, both falling short of analyst's average estimates.

Energy stocks were also mixed this week, as the Energy sector itself was -1.60% due to heightened concerns of US oil production increasing under potential new US energy policies. WTI and Brent prices are down this week, -6.45% and -4.27%, respectively. Over the week Energy Fuels +13.53%, BP +0.77%, Shell +0.54%, Baker Hughes +0.20%, while Phillips 66 -0.38%, Chevron -1.21%, Halliburton -1.49%, ExxonMobil -1.78%, ConocoPhillips -2.41%, Marathon Petroleum -2.70%, Hess -2.76%, Occidental Petroleum -4.74%, and Apa -8.21%.

Materials and Mining stocks had an uneven performance this week, with the Materials sector itself +1.99%. Mosaic +2.89%, Newmont Corporation +0.75%, Yara International +0.73%, while Nucor -0.80%, Sibanye Stillwater -1.90%, Freeport-McMoRan -2.35%, CF Industries -2.97%, and Albemarle -5.15%.

European Stock Indices Price Performance

Stoxx 600 +4.02% MTD

DAX +6.76% MTD

CAC 40 +6.19% MTD

IBEX 35 +2.48% MTD

FTSE MIB +4.88% MTD

FTSE 100 +4.55% MTD

This week, the pan-European Stoxx Europe 600 index was +1.54%. It was +0.39% on Wednesday, closing at 528.04.

So far this month in the STOXX Europe 600, Financials is the leading sector, +7.36% MTD, while Retail is the weakest at -2.47% MTD.

This week, Personal & Household Goods outperformed within the STOXX Europe 600 with a +7.55% gain, followed by Industrial Goods & Services and Financial Services at +4.63% and +3.80%, respectively. Conversely, Utilities underperformed at -0.91%, followed by Oil & Gas and Telecom, -0.40% and -0.01%, respectively.

Germany's DAX index was +1.01% on Wednesday and closed at 21,254.27. It was +2.90% for the week. France's CAC 40 index was +0.86% on Wednesday, closing at 7,837.40. It was +2.65% for the week.

The UK's FTSE 100 index was +1.83% this week to 8,545.13. It was -0.04% on Wednesday.

On Wednesday, in the STOXX Europe 600, the Industrial Goods & Services sector exhibited strong performance. Invisio reported preliminary Q4 revenue that exceeded forecasts, while Alstom announced Q3 revenue of €4.67 billion, also surpassing expectations and reaffirming its full-year guidance.

The Autos & Parts sector also gained, albeit at a more moderate pace compared to the broader market. This more subdued performance is likely influenced by the US President's increasingly hawkish rhetoric towards Europe. Schaeffler released lower-than-expected preliminary full-year 2024 results, primarily due to weak Q4 performance, and issued a profit warning. Porsche confirmed a subdued outlook for 2025, citing anticipated challenges such as sales volume decline resulting from EU model withdrawals, potential supply chain disruptions, and persistent difficulties in the Chinese market.

The Telecom sector experienced weakness, even as Telecom Italia received positive news. An Italian court of appeals confirmed a €1 billion windfall for the company stemming from a 1990s licensing fee dispute, rejecting the government's appeal.

Other Global Stock Indices Price Performance

MSCI World Index +3.52% MTD

Hang Seng -1.40% MTD

This week, the Hang Seng Index was +2.55%, while the MSCI World Index was +2.50%.

Currencies

EUR +0.51% MTD to $1.0408.

GBP -1.60% MTD to $1.2310.

The euro was +1.13% against the USD over the past week, while the British pound was +0.59%. The Dollar Index is -0.73% so far this week and -0.20% MTD.

On Tuesday evening, the President stated that his administration is considering a 10% tariff on goods imported from China, effective 1st February. This follows an earlier announcement suggesting Mexico and Canada could face tariffs of approximately 25% by the same date. Additionally, the President promised tariffs on European imports, though he did not provide specific details. The US dollar index was +0.29% to reach 108.28 on Wednesday after dipping to 107.75 earlier, marking its lowest level since 6th January. This may be attributed to profit taking given the lack of clarity around further tariff measures. However, on Wednesday, the President threatened additional tariffs on Russia if it fails to negotiate an end to its conflict in Ukraine. He also hinted at the possibility of extending such measures to other involved nations.

In addition, compounding trade tensions, the US President on Monday signed a comprehensive trade memorandum, directing federal agencies to conduct thorough reviews of trade-related issues by 1st April. Market participants view this date as pivotal for unveiling the administration's tariff plans.

The euro declined -0.19% to $1.0408 amid comments from several ECB policymakers, who supported further rate cuts. Their statements reinforced market expectations of a reduction at the ECB's policy meeting next week, with a 96% probability of a cut of 25 bps, according to LSEG data. These remarks suggested the ECB may continue easing monetary policy, even as the Fed adopts a more cautious approach.

Sterling fell -0.31% to $1.2310 following a report from the Office for National Statistics, which revealed a larger-than-expected budget deficit in December. The deficit was driven by increased debt interest costs and a one-off purchase of military housing, underscoring the fiscal challenges facing Finance Minister Rachel Reeves.

The euro gained +0.14% against the British pound, reaching 84.50 pence, after hitting a five-month high of 84.73 pence earlier in the week. Investor concerns over Britain's fiscal outlook have contributed to the pound's roughly 2% decline against the euro since the beginning of the year. Markets currently anticipate around 65 bps of rate cuts from the BoE this year.

Against the Japanese yen, the dollar strengthened +0.59% to ¥156.42. Market expectations indicate an 88.3% likelihood of a 25 bps rate hike at the BoJ’s meeting on Friday.

Note: As of 5:00 pm EST 22 January 2025

Cryptocurrencies

Bitcoin +11.39% MTD to $103,829.06

Ethereum -2.36% MTD to $ 3255.30.

Bitcoin is +4.11% and Ethereum -5.65% over the past week. Bitcoin rallied past the $100,000 mark again this week. It spiked to a new all-time high early on Monday of $109,071, but pulled back following the inauguration of President Donald Trump after he did not release any executive orders regarding a Strategic Bitcoin reserve and other crypto positive measures. However, it has recovered since Tuesday after the Securities and Exchange Commission’s (SEC) acting Chairman Mark T. Uyeda announced a new task force, led by Commissioner Hester Peirce, to develop a regulatory framework for digital assets, the first major move by Trump's new administration to overhaul crypto policy. In response, as noted by Coindesk.com on Tuesday, Bitcoin options trading on the Chicago Mercantile Exchange (CME) showed the strongest bullish sentiment since Trump's election victory. Traders scrambled to buy calls, or options offering asymmetric upside exposure, driving the skew higher to 4.4% according to data tracked by digital assets index provider CF Benchmarks.

What also became clearer this week is that institutional investor interest in cryptocurrency remains strong. Speaking at the World Economic Forumin Davos, BlackRock CEO Larry Fink suggested that Bitcoin could reach a price of $700,000 if concerns about currency debasement and economic instability persist. He explained that small investments of 2% to 5% by sovereign wealth funds and asset managers could significantly drive Bitcoin's value. BlackRock’s iShares Bitcoin Trust now holds around 559,262 Bitcoin, valued at around $58.51 billion. This week has seen several companies file cryptocurrency ETF applications including asset managers Osprey Funds and REX Shares for memecoins including Dogecoin and Bonk, in addition to ETFs for Bitcoin, Ethereum, Solana, and XRP.

Note: As of 5:00 pm EST 22 January 2025

Fixed Income

US 10-year yield +4.0 bps MTD to 4.616%

German 10-year yield -0.6 bps MTD to 2.533%.

UK 10-year yield +7.4 bps MTD to 4.642%.

US Treasury 10-year bond yields are -4.1 bps over the past week.

US Treasury yields exhibited a modest increase in subdued trading on Wednesday, lacking a clear directional trend. This muted activity stemmed from growing investor caution as they awaited further policy announcements from the new administration, particularly regarding trade policy, immigration, and fiscal policy.

The uncertainty surrounding potential tariff implementation has left the bond market in a state of flux, with traders exhibiting a general reluctance to make significant investment decisions, ahead of more definitive policy pronouncements from the US administration.

In afternoon trading, the yield on the 10-year Treasury note rose by +3.4 bps to 4.616%. Since hitting its more than one-year high of 4.793% on 14th January, the 10-year yield has retreated more than 17 bps.

Conversely, yields on the 30-year Treasury bond increased by +1.4 bps to 4.817%. At the shorter end of the yield curve, the two-year yield, sensitive to Fed policy expectations, edged up by +1.2 bps to 4.293%.

The US Treasury conducted a successful auction of $13 billion in 20-year bonds on Wednesday. The bonds were priced to yield 4.9%, below market expectations at the bid deadline, signalling robust investor demand. The auction achieved a bid-to-cover ratio of 2.75x, exceeding the average of 2.64x. Following the auction, yields on the 20-year Treasury bond increased by +1.4 bps to 4.889%.

According to the CME Group's FedWatch Tool, there is virtually no chance of a rate cut at the next meeting at the end of this month. Markets are now not expecting the first rate cut, if there is one, until June.

Across the Atlantic, the German 10-year yield was -0.6 bps this week, while the UK 10-year yield was -16.5 bps this week. The spread between US 10-year Treasuries and German Bunds currently stands at 208.3 bps.

Italian bond yields, a benchmark for the eurozone periphery, were -9.1 bps this week to 3.597%. Consequently, the spread between Italian and German 10-year yields is 106.4 bps.

French 10-year government bond yields -16.2 bps to 3.262%. The yield premium over German 10-year yields is 72.9 bps.

Eurozone bond yields largely stabilised on Wednesday, suggesting a tentative sense of relief among investors that the US President has refrained from escalating tariffs during his initial days in office.

Germany's 10-year bond yield edged up by +2.0 bps to 2.533%, while Italy's 10-year yield remained relatively unchanged at 3.597%, registering a marginal decrease of -0.3 bps.

The yield on Germany's two-year bond, which is particularly sensitive to ECB rate expectations, rose by +1.0 bps to 2.228%.

Several ECB officials expressed support for further interest rate cuts on Wednesday, although their remarks had minimal impact on market movements. ECB President Christine Lagarde, speaking to CNBC in Davos, Switzerland, affirmed that the direction of interest rates is "very clear," while seemingly cautioning against overly rapid adjustments.

Bond yields experienced a sharp rise in December and early January, fueled by a sell-off in US Treasuries. This sell-off was driven by investor reactions to robust US economic growth and the potential inflationary impact of tariffs.

Germany's 10-year bond yield reached a seven-month high of 2.629% on 14th January. However, following the release of US CPI data, which reinforced the case for further easing, the 10-year yield has retreated and currently stands 9 bps below its recent peak.

Strong investor demand for eurozone government debt has also contributed to the decline in yields. This was evident in Spain's successful syndication of new 10-year bonds on Wednesday, which attracted record demand exceeding €155 billion. Similarly, France experienced record demand for its syndicated bond sale on Tuesday.

Commodities

Gold spot +5.26% MTD to $2,755.35 per ounce.

Silver spot +7.29% MTD to $30.83 per ounce.

West Texas Intermediate crude +4.78% MTD to $75.26 a barrel.

Brent crude +5.71% MTD to $ 78.97 a barrel.

Gold prices are +2.21% this week. Spot gold was -0.12% on Wednesday, reaching $ 2,755.35 per ounce, its highest point since 6th November. Investors continue to seek safety amidst growing uncertainty surrounding potential US policies.

Additionally, the SPDR Gold Trust GLD, the world's largest gold-backed ETF, reported a decrease in its holdings on Wednesday. The trust's gold reserves were -0.26%, from 871.66 tonnes on Tuesday to 869.36 tonnes on Wednesday. This equates to a reduction from 28,024,618 ounces to 27,950,789 ounces.

This week, WTI and Brent are -6.45% and -4.27%, respectively. Oil prices experienced a continued decline on Wednesday, reaching a new one-week low as market participants assessed the potential impact of the US President's proposed tariffs on global economic growth and energy demand.

Brent crude futures decreased by 41 cents, or -0.52%, settling at $78.97 per barrel. Simultaneously, US WTI crude fell by 63 cents, or -0.83%, to settle at $75.26. This marks the fifth consecutive daily decline for Brent, a trend not observed since September, and the fourth consecutive decline for WTI, a pattern unseen since November. Both benchmarks closed at their lowest point since 9th January for the second consecutive day.

The focus of the oil market is gradually shifting from US sanctions against Russia towards the potential ramifications of the US President's trade policies. The energy complex is facing downward pressure partly attributed to the escalating threat of tariffs.

In Europe, French President Emmanuel Macron and German Chancellor Olaf Scholz met in Paris, striving to present a united front as Europe grappled with formulating a cohesive response to the looming tariffs from the US.

Adding to market uncertainty, the US President indicated that his administration would likely cease oil imports from Venezuela, an OPEC member currently subject to US sanctions. According to data from the US Energy Information Administration (EIA), US oil imports from Venezuela averaged approximately 200,000 barrels per day (bpd) during the first ten months of 2024, an increase from the 2023 average of 100,000 bpd.

Meanwhile, Iran, another OPEC member under US sanctions, conveyed a more conciliatory message at the World Economic Forum in Davos. A high-ranking Iranian official denied the country's pursuit of nuclear weapons and expressed openness to dialogue and potential opportunities.

In other OPEC developments, Saudi Arabia reported a significant increase in crude oil exports in November, reaching an eight-month high.

Market analysts anticipate a decline in US crude stockpiles of approximately 1.6 million barrels last week. Official data from the EIA, originally scheduled for Wednesday, is now expected to be released on Thursday due to the observance of Martin Luther King Jr. Day on Monday.

Note: As of 5:15 pm EST 22 January 2025

Key data to move markets

EUROPE

Thursday: Eurozone Consumer Confidence.

Friday: German HCOB Composite, Manufacturing and Services PMIs, Eurozone HCOB Composite, Manufacturing and Services PMIs, speeches by ECB President Christine Lagarde and Executive Board member Piero Cipollone

Monday: German IFO Business Climate, Current Assessment and Expectations surveys.

UK

Friday: S&P Global/CIPS Composite, Manufacturing and Services PMIs.

Tuesday: ECB Bank Lending Survey.

Wednesday: German GfK Consumer Confidence.

US

Thursday: Initial and Continuing Jobless Claims.

Friday: S&P Global Composite, Manufacturing and Services PMIs. Existing Home Sales Change, Michigan Consumer Sentiment Index, and UoM 5-year Consumer Inflation Expectation.

Monday: New Home Sales Change.

Tuesday: Durable Goods, Nondefense Capital Goods Orders, Housing Price Index, and Consumer Confidence.

Wednesday: Fed Interest Rate Decision, Fed Monetary Policy Statement and FOMC Press Conference.

JAPAN

Thursday: National CPI and core CPI.

Friday: BoJ Interest Rate Decision, Monetary Policy Statement, and Press Conference.

Tuesday: BoJ Monetary Policy Meeting Minutes.

CHINA

Monday: NBS Manufacturing PMI and NBS Non-Manufacturing PMI.

Tuesday: Chinese New Year.

Global Macro Updates

ECB targets neutral rate by summer, Lagarde reiterates confidence in inflation goal. In an interview with CNBC, ECB President Christine Lagarde defended the central bank's gradual approach to monetary policy, emphasising that its earlier start to rate cuts provides the flexibility to assess their economic impact. Lagarde underscored the importance of remaining vigilant regarding tariff developments and responding appropriately. She expressed confidence in achieving the ECB’s inflation target this year and dismissed claims that the bank is falling behind the curve, while acknowledging downside risks to economic growth.

Lagarde indicated that the neutral interest rate lies between 1.75% and 2.25%, aligning with remarks from other policymakers who anticipate at least four rate cuts this year. Officials such as Dutch central bank President Klaas Knot told Bloomberg in an interview in Davos that he supports additional rate cuts over the next two meetings, but noted that committing to further reductions beyond that point is challenging due to prevailing uncertainties. Similarly, Yannis Stournaras, Governor of the Bank of Greece, sees the deposit rate reaching 2%, according to Naftemporiki, though he cautioned that US tariffs could accelerate the pace of rate cuts.

While the ECB has shown reluctance to deviate from its measured approach to rate adjustments, Lagarde clarified that the bank is not bound to 25 bps increments. The ECB is expected to reach the neutral rate by the summer, likely around the 5th June meeting.

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.