- US GDP: Gross domestic product increased at a 2.4% annualised rate last quarter, the Commerce Department in its advance estimate of second-quarter GDP said today. The economy grew at a 2.0% pace in the January-March quarter.

- The US labour market remained strong with initial claims for state unemployment benefits falling for the second week in a row to a seasonally adjusted 221,000 for the week ended 22 July.

- Inflation continued to decline, with US headline inflation falling to 3% in June, down from May’s 4%.

- The Conference Board Consumer Confidence Index rose again in July to 117.0, up from 110.1 in June.

- Flash PMIs in the US, UK and Eurozone were softer in July. In the US the S&P Global US Composite PMI declined to 52.0 in July 2023, down from 53.2 the previous month. In the UK the S&P Global/CIPS Flash UK Composite Output Index showed business activity falling to 50.7 in July 2023, down from 52.8 in June. In the Eurozone the HCOB flash Composite PMI for the Eurozone dropped to 48.9 in July from 49.9 in June.

Yield curves

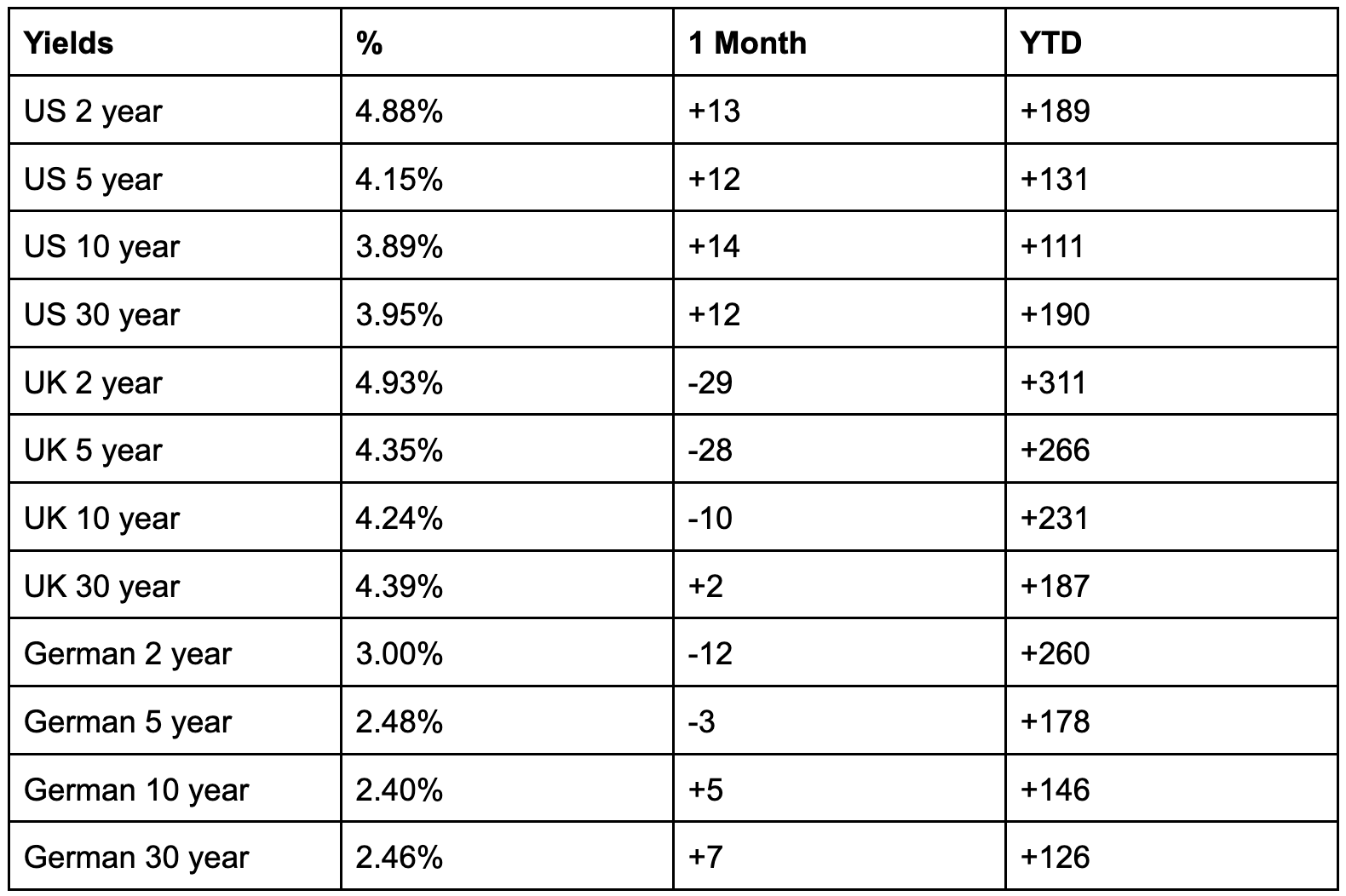

Rates across the US Treasury yield curve were up in July. The yield on the 2-year Treasury note, which is highly sensitive to expectations for the Fed Funds rate, is at 4.88%, up from 4.4% at the start of the year. The benchmark 10-year US Treasury note yield is at 3.89%, while the yield on the 30-year bond is at 3.95%.

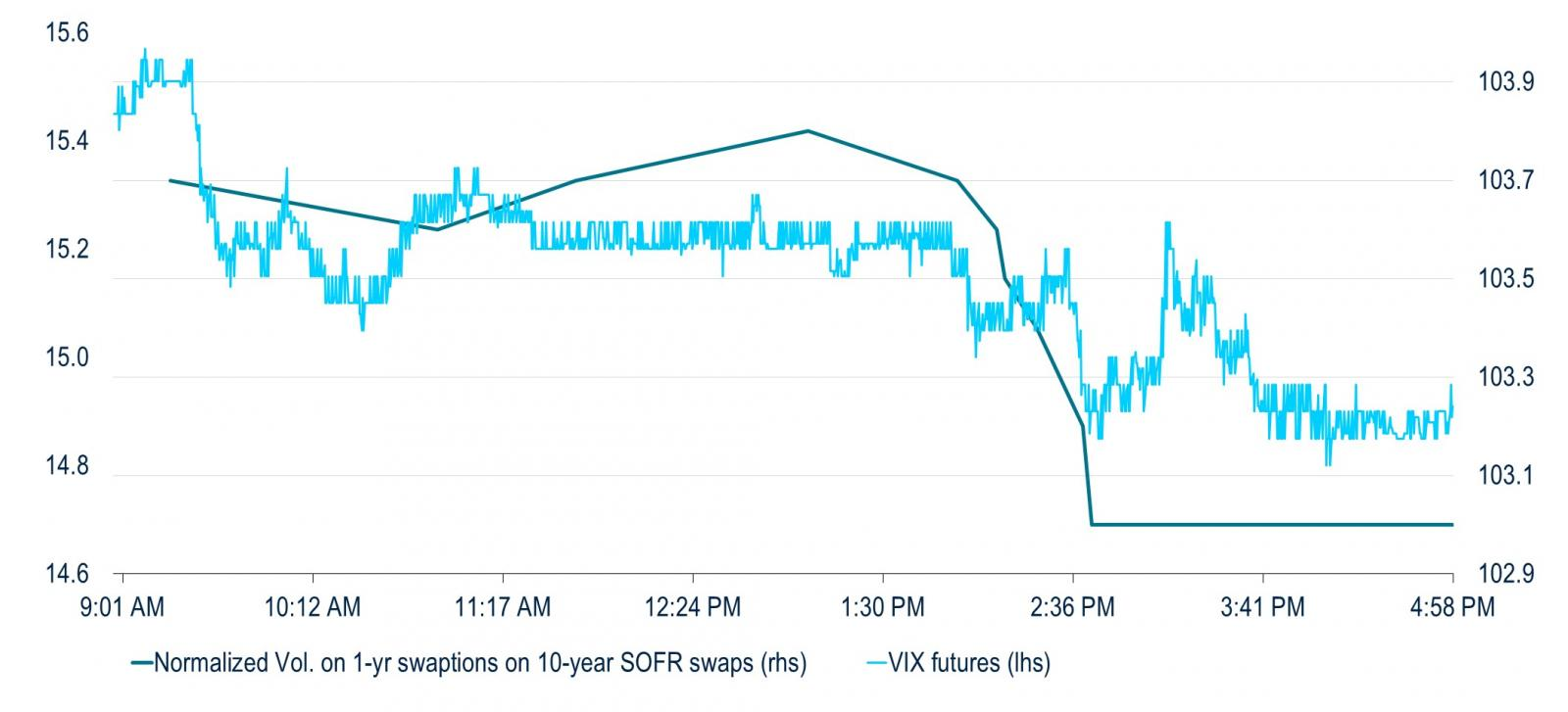

US yields have been reacting to mixed data in July: jobless claims fell to a two-month low but housing market data was softer, with new starts, building permits and existing home sales declining. Retail sales were mixed with “core” retail rising 0.6% month-over-month. Yields are expected to continue to climb following a higher than expected Q2 GDP of 2.4%. Fed Chair Jerome Powell indicated that the central bank would be data dependent moving forwards after raising rates by 25 basis points on 26 July. The immediate response to the rate rise was a drop in yields as Powell said the Federal Reserve hasn’t made a decision to hike at every other meeting, raising hopes that the Fed could skip a rate increase in September.

Source: PGIM Fixed Income

While the US growth outlook remains positive but somewhat subdued due to the full impact of tightening credit conditions still emerging, the IMF, in its July update, noted that the excess savings from the pandemic-related transfers which helped households weather the cost-of-living crisis are all but depleted. However, a still tight labour market means that the US is likely to maintain its growth momentum. Yields are likely to start to flatten out as the central banks get towards their peaks, with volatility in fixed income markets likely to fall as a consequence.

Source: Bloomberg 9:40 am EDT 27 July 2023

Global Economic and Market Review

In the UK, the inflation story finally took a positive turn in July as inflation came in below expectations. UK CPI rose by 7.9% in the 12 months to June, its lowest level in 15 months, and down from May's 8.7%. This reflected a drop in motor fuel costs, although food prices moderately rose. Despite a slowdown in inflation, economic growth has decelerated and the UK labour market remains tight – insufficient conditions for the Bank of England to take its foot off the monetary policy pedal.

The ECB, as expected, raised rates by another 25 basis points at its meeting on 27 July despite signs of slowing growth in the Eurozone. However, Eurozone bonds have been falling through July. Despite the ECB refusing to give any guidance on the future direction of rates, insisting that further actions will be data dependent, markets are now anticipating that the ECB is near the peak of its tightening cycle. However, there are potential headwinds including a rise in food and energy inflation due to geopolitical events, namely the war in Ukraine, and global weather conditions. According to Worldgovernmentbond.com, the spread between Germany’s 10 Year and Italy’s 10 year is 163, down 1.3 basis points this month. Germany’s spread vs the US is -151.8 basis points.

It is clear that differences in domestic interest rate paths that may emerge in September will continue to drive yields. The ECB and the BoE continue to face stickier inflation, so despite slowing growth, may be more likely to sustain their hiking cycle into the Autumn. Rate hikes are expected to outpace the US over the coming months, helping boost the value of European and UK currencies at the expense of the USD.

Key risks

Markets are still hoping for rate cuts early next year. Short-dated government bonds, which are subject to higher levels of volatility, are offering higher yields, which, if interest rates stay in line with expectations over the next couple of months, should offer attractive income with limited risk. However, if inflation, particularly in Europe, remains stubbornly high, bond prices could still weaken. However, if inflation continues to decelerate in line with ECB and Fed projections, the middle area (five to 10 years) of the curve may become more attractive due to the consequent expectation of the interest rate cycle.

- Inflation fails to moderate as expected, weighing on asset prices. US core inflation continues to remain above target through August and into September. This will likely cause interest sensitive stocks in the technology sector, financials, telecommunications, and infrastructure to decline.

- Policymakers actions lead to over tightening credit conditions.

- Geopolitical flare-ups and Climate change. The withdrawal of Russia from the Black Sea Grain agreement and threats to bomb boats emerging from Ukrainian ports have resulted in higher wheat prices. Europe, China and across the US have experienced unusually high temperatures this summer which may negatively impact food harvests, hitting consumers in the Autumn.

DISCLAIMER: While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here.