Still the land of opportunity?

Key data to move markets today

EU: Eurozone HCOB Composite and Services PMIs and speeches by ECB President Christine Lagarde and Bundesbank President Joachim Nagel

UK: A speech by BoE Governor Andrew Bailey

USA: Markets closed in observance of Independence Day

Global Macro Updates

June NFP. June nonfarm payrolls increased by 57,000, well below market expectations of 110,000 – 115,000. April and May payrolls were revised down by a combined 74,000, lowering the three-month average from 188,000 in May to 111,000 after Thursday’s report, though still above estimated replacement levels. The unemployment rate unexpectedly fell to 4.2%, its lowest level since July 2025, after holding at 4.3% for three months. Average hourly earnings rose 0.3% m/o/m, matching forecasts and May’s pace.

The report showed fewer unemployed workers month over month, but also a notable drop in labour-force participation to 61.5% from 61.8%, the lowest level since March 2021. Participation remains below pre-Covid levels and has trended lower since mid-2023. Analysts highlighted a sharp decline among workers aged 25 – 34, the largest one-month drop for that group outside the COVID period.

The 61,000 decline in leisure and hospitality jobs drew attention after May’s 70,000 gain. Some analysts had initially linked the May increase to hiring ahead of the World Cup, though yesterday’s commentary has softened that view. In previews, JPMorgan cited the effect of an earlier-than-usual Memorial Day, while Citi suggested early summer hiring could reverse as soon as June. Other sectors continued to add jobs, including professional and business services (+36,000), social assistance (+25,000) and healthcare (+22,000, below recent trends).

Several previews had anticipated renewed m/o/m volatility in job growth, a view that appears to have been confirmed. Recaps generally noted that the slowdown to more moderate growth still points to a broadly healthy labour market, although Citi remained more pessimistic and expects weaker job growth and higher unemployment later this year.

On policy, analysts said the June report may make it harder for the Fed to justify near-term rate hikes, though FedWatch odds still imply a likely 25 bps hike in September. Contained wage growth also supports the view that the labour market is not currently a source of inflation pressure.

US Stock Indices

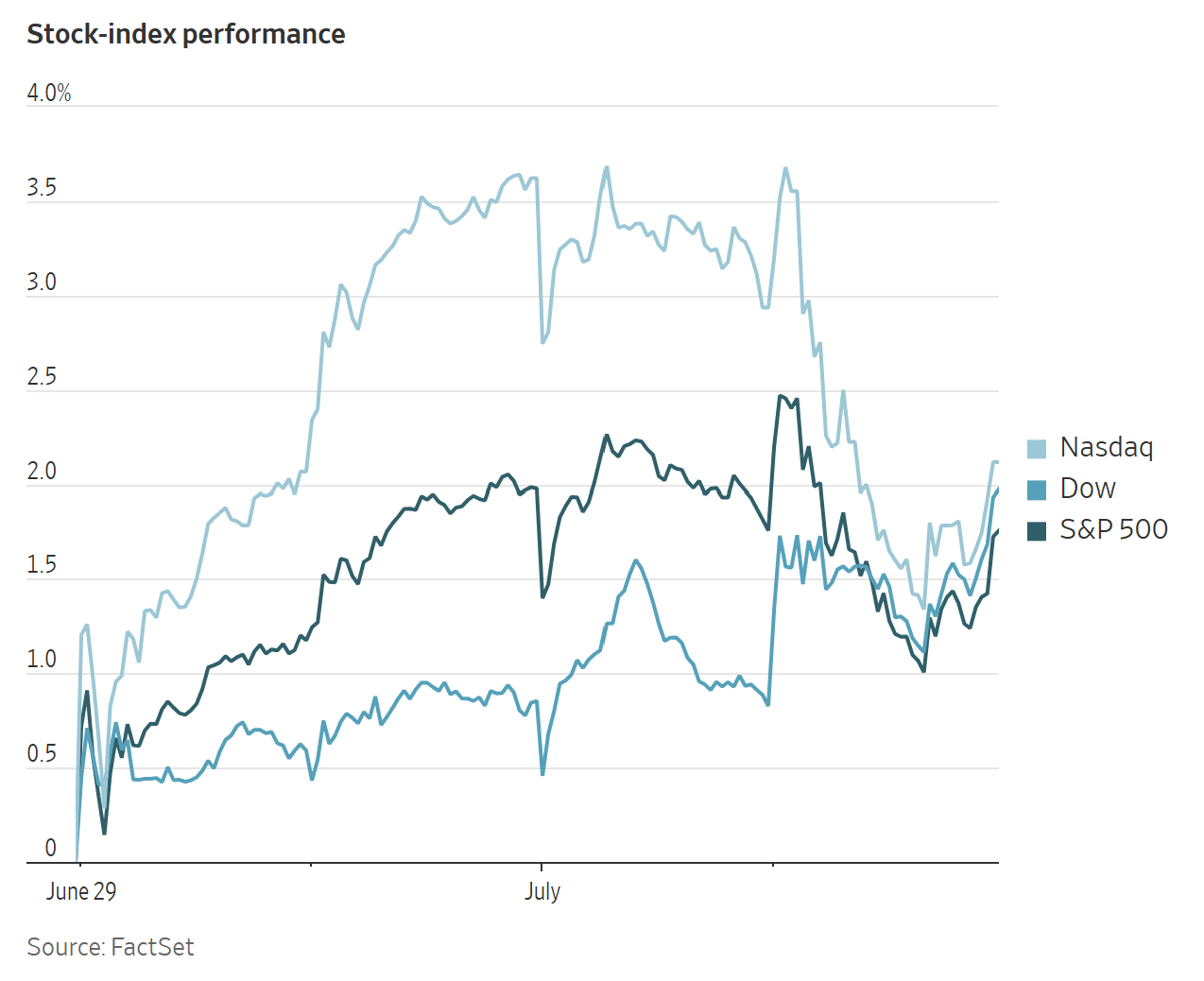

Dow Jones Industrial Average +1.14%

Nasdaq 100 -1.61%

S&P 500 +0.00%, with 8 of the 11 sectors of the S&P 500 up

The labour market appeared weaker than economists had expected, prompting investors to reassess market leadership and rotate into more defensive and previously lagging areas of the equity market.

Investors moved away from the AI-related companies to healthcare, consumer staples and other sectors that had lagged during this year’s chip-stock rally posted gains.

The Dow Jones Industrial Average reached a new record, rising +1.14%, or 594.83 points, while the Nasdaq Composite declined -0.80%. Technology stocks’ weakness also weighed on the S&P 500. Although eight of its 11 sectors advanced, the index finished with a gain of less than one point.

In corporate news, The Information reported that Anthropic PBC is in discussions with Samsung Electronics over a potential manufacturing partnership for a custom artificial-intelligence chip, citing people familiar with the plan.

The Financial Times reported that OpenAI has begun preliminary talks that could give the US government a 5% stake in the ChatGPT developer, citing two people familiar with the discussions.

In private credit, two Blue Owl Capital funds received the industry’s largest redemption requests for a second consecutive quarter, requiring the manager to cap withdrawals again.

Bending Spoons, the Italian technology company that has acquired brands including AOL, Eventbrite and Vimeo, made its stock-market debut Wednesday at a valuation of more than $18 billion. Its shares closed at $40.50, roughly forty percent above the $29 IPO price, giving the company a market value of $25.7 billion.

Mega Caps

Alphabet -0.48%, Amazon +0.40%, Apple +4.84%, Meta Platforms -4.90%, Microsoft +1.62%, Nvidia -1.39% and Tesla -7.49%

European Stock Indices

CAC 40 +1.65%

DAX +2.16%

FTSE 100 +1.67%

Commodities

Gold spot +2.29% to $4,122.80 an ounce

Silver spot +3.25% to $61.06 an ounce

West Texas Intermediate +1.06% to $68.81 a barrel

Brent crude +0.58% to $71.59 a barrel

Gold advanced on Thursday, supported by a weaker US dollar. Spot gold rose +2.29% to $4,122.80 per ounce. The US dollar index declined -0.54%, making dollar-denominated metals more affordable for holders of other currencies.

Spot silver also strengthened, rising +3.25% to $61.06 per ounce.

Oil prices posted modest gains on Thursday as buyers sought to secure supply ahead of the long US Independence Day weekend. Brent futures settled at $71.59 per barrel, up 41 cents, or +0.58%, while US WTI crude finished at $68.81 per barrel, up 72 cents, or +1.06%.

Despite the daily increase, both benchmarks touched their lowest levels since before the US - Israeli-led war with Iran began in late February. Over this week, Brent has declined -1.84%, while WTI has fallen -1.70%.

Officials from the US and Iran held technical talks through mediators in Doha this week, with US envoys and Qatar’s Foreign Ministry describing the discussions as constructive. Key sticking points continue to centre on Iran’s demand to levy charges on ships passing through the Strait of Hormuz.

Tanker traffic through the Strait of Hormuz has recovered after a brief weekend lull, while production has increased across several Gulf countries, including Kuwait, the UAE, Saudi Arabia and Iraq. UAE exports are estimated to have returned to pre-war levels. Bloomberg estimates that Saudi crude exports have also recovered to pre-war levels following the restart of seaborne exports and continued Red Sea flows through the East-West Pipeline. At least six major sell-side firms cut WTI and/or Brent forecasts in response to the recovery in traffic through the strait.

China’s crude imports remain weak, while product inventories appear sufficient after the government lifted limits on petroleum product exports.

Ukraine has struck at least five Russian refineries since last weekend and more than 20 since early June, some multiple times. Gasoline lines in Russia are growing, Moscow is reportedly importing gasoline from countries such as India, and the Kremlin is considering a possible diesel export ban.

Note: As of 4 pm EDT 2 July 2026

Currencies

EUR +0.51% to $1.1433

GBP +0.59% to $1.3347

Bitcoin +1.25% to $61,520.18

Ethereum +4.14% to $1,698.70

The dollar fell sharply on Thursday after the closely watched June employment report showed that US employers added fewer jobs than expected. The Japanese yen surged as traders prepared for possible intervention by Japanese authorities.

The dollar index declined -0.54% to 100.86 after earlier reaching 100.55, its lowest level since 18 June. The move marked the index’s largest one-day decline since 30 April. The euro gained +0.51% to $1.1433 and reached $1.1472 earlier in the session, its highest level since 22 June.

The British pound advanced +0.59% to $1.3347.

The yen rallied sharply against the dollar, recording its largest one-day gain against the dollar since 30 April, as traders assessed a potential shift in the Ministry of Finance’s intervention strategy and speculated whether Tokyo had already acted. Sources told Reuters that Japanese officials were moving away from telegraphing intervention risks and instead signalling a more targeted campaign to pressure speculators and increase the cost of betting against the yen.

Officials also avoided suggesting a specific exchange-rate threshold that would trigger action, reflecting a more aggressive approach intended to keep traders uncertain. The yen gained +0.90% against the dollar to reach ¥161.05 per dollar and reached ¥160.62, its strongest level since 18 June during the trading day.

Fixed Income

US 10-year Bond +0.5 basis points to 4.490%

German 10-year Bund +2.3 basis points to 2.907%

UK 10-year Gilt +1.5 basis points to 4.774%

US Treasury yields eased from earlier highs on Thursday. The Treasury market closed at 2 pm ET and will remain closed on Friday in observance of the US Independence Day holiday.

The yield on the US 10-year Treasury note edged up +0.5 bps to 4.490% after earlier climbing to 4.505%, its highest level since 23 June. The yield is up +10.3 bps on the week, ending a three-week decline and recording its largest weekly gain since mid-May.

The US Treasury yield curve, measured by the spread between two- and 10-year Treasury yields, stood at a positive 30.9 bps.

The two-year US Treasury yield, which typically moves in line with expectations for Federal Reserve policy, fell -0.2 bps to 4.181%, ending a three-day streak of gains. The yield is up +6.4 bps on the week.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing 29.7 bps of rate hikes in 2026, higher than the 33.3 bps priced in a week ago. Fed funds futures traders are now pricing in a 17.6% probability of a 25 bps rate hike at July’s FOMC meeting, compared to 32.1% last week.

Short-dated eurozone government bond yields drifted lower on Thursday as investors reduced expectations that the ECB would raise interest rates aggressively this year.

Two-year German Schatz yields, which are highly sensitive to shifts in rate and inflation expectations, were down -0.8 bps on the day at 2.512% after touching their lowest level since mid-April. They have fallen -1.4 bps this week.

Ten-year Bund yields rose for a fourth consecutive day, trading +2.3 bps higher at 2.907%. It has advanced +5.1 bps so far this week.

Note: As of 4 pm EDT 2 July 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.