¿Está el mercado descontando la permanencia en una paz frágil?

Datos clave que moverán los mercados hoy

UE: producción industrial y balanza comercial de la eurozona, y discursos de la presidenta del BCE, Christine Lagarde, del presidente del Bundesbank, Joachim Nagel, y del miembro del Comité Ejecutivo del BCE, Piero Cipollone

EE. UU.: índice manufacturero Empire State de Nueva York y producción industrial

Japón: decisión sobre tipos de interés del BoJ y declaración de política monetaria

Actualizaciones macroeconómicas mundiales

El acuerdo de paz ya ha llegado. EE. UU. e Irán han confirmado que han alcanzado un acuerdo para poner fin al conflicto, con una ceremonia de firma prevista para el 19 de junio en Suiza. Esta semana tendrán lugar en Doha reuniones preparatorias con cada parte, antes de la firma oficial en Suiza y del inicio de las conversaciones técnicas. En virtud del acuerdo, se espera que el estrecho de Ormuz reabra una vez firmado el texto, aunque el presidente de EE. UU. ha indicado que será necesario un tiempo adicional para retirar las minas antes de que la navegación pueda reanudarse con normalidad. También ha señalado que el tráfico marítimo se reanudaría sin peajes y que EE. UU. levantará de inmediato su bloqueo naval. Aun así, sigue habiendo incertidumbre sobre cómo se compatibilizará la reapertura del estrecho con la reiterada reivindicación de soberanía de Irán y su autoproclamado derecho a cobrar peajes de tránsito.

Se han facilitado pocos detalles sobre el memorando de entendimiento, que Irán ha afirmado que solo se publicará tras la ceremonia de firma. Según informaciones anteriores de la prensa, el memorando establecería una prórroga de 60 días del alto el fuego, durante la cual continuarán las conversaciones sobre el programa nuclear iraní. Entre las disposiciones del borrador figura, según se ha informado, el compromiso de Irán de no adquirir armas nucleares, mientras que funcionarios estadounidenses han sugerido que el acuerdo podría conducir con el tiempo al desmantelamiento del programa nuclear iraní. El compromiso mínimo sería la dilución in situ de todo el uranio bajo la supervisión del Organismo Internacional de Energía Atómica (OIEA). El marco también aborda los arsenales de uranio, potencialmente mediante la reducción del enriquecimiento del material dentro de Irán bajo supervisión de la ONU. Tal y como ha informado el Financial Times, Irán dispone de un arsenales de más de 9.000 kg de uranio enriquecido, la mayor parte a niveles bajos de enriquecimiento, aunque 440 kg están enriquecidos a niveles cercanos a los necesarios para fabricar armas. El presidente de EE. UU. ha indicado que Washington tratará el tema de los arsenales en los próximos meses, aunque ha matizado que no existe una urgencia inmediata.

El alcance del alivio de las sanciones sigue sin estar claro. Los medios iraníes han afirmado que se liberarían 24.000 millones de dólares a lo largo del período de 60 días, y que la mitad estará disponible antes de que comiencen las conversaciones formales. También se espera que Irán obtenga cierto alivio de las sanciones petroleras. Sin embargo, Trump ha afirmado que Irán no recibirá pagos en efectivo directos, aunque ha reconocido que otras sanciones podrían relajarse. Funcionarios estadounidenses han mantenido que cualquier alivio de las sanciones dependerá del cumplimiento por parte de Irán de sus obligaciones en virtud del acuerdo. Según se ha informado, el acuerdo también incluye un marco de reconstrucción económica valorado en no menos de 300.000 millones de dólares.

El acuerdo se topó, no obstante, con una complicación de última hora cuando un ataque israelí en Beirut provocó amenazas de represalia por parte de Irán, antes de que Trump instara públicamente a Israel a detener sus ataques. El acuerdo incluye asimismo, según se espera, el fin de los combates en el Líbano. Sin embargo, el programa de misiles iraní y su apoyo a grupos afines quedarían fuera del alcance de la agenda de 60 días. Además, se prevé que EE. UU. reduzca su presencia militar en torno a Irán.

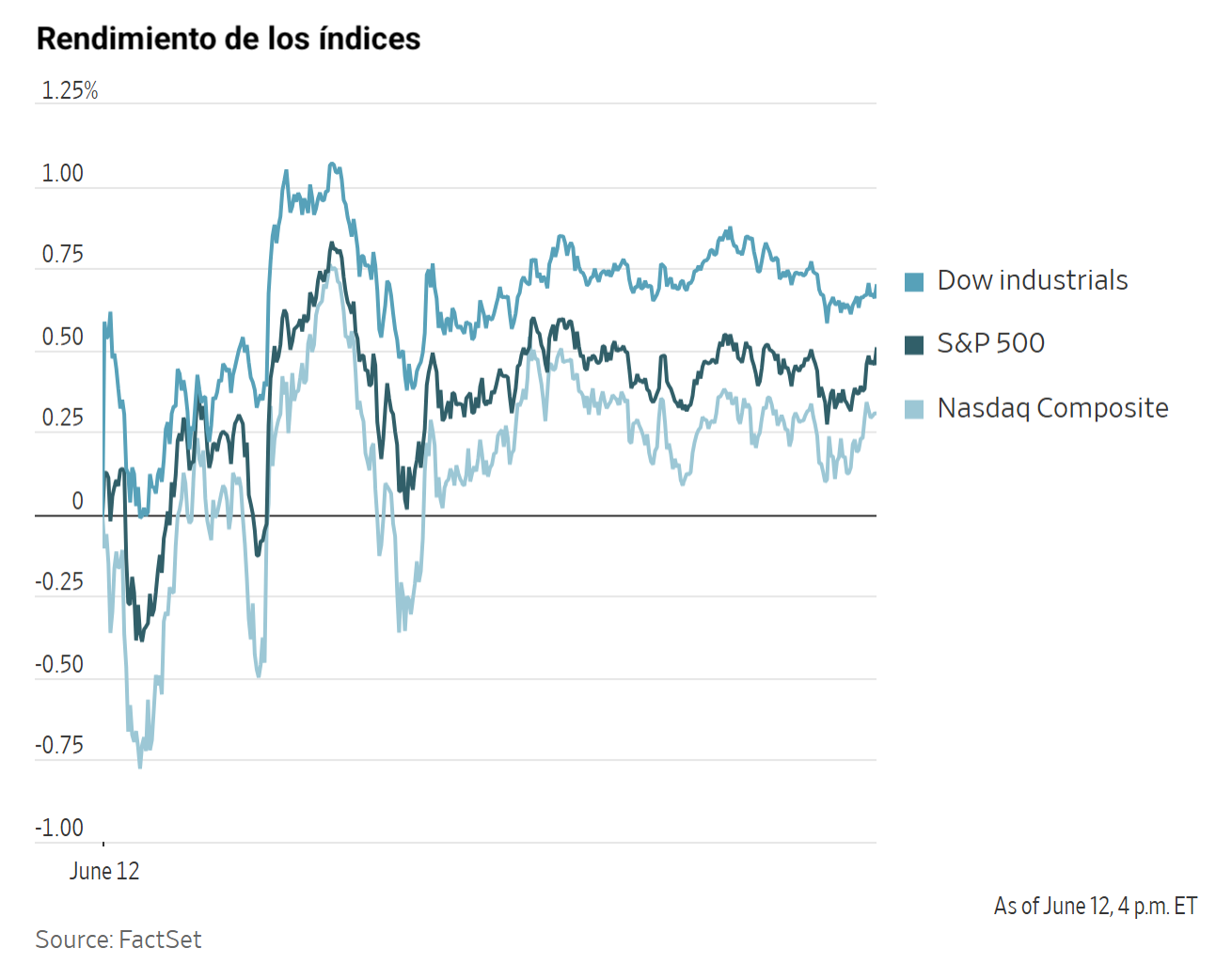

Índices bursátiles estadounidenses

El Dow Jones Industrial Average +0,70 %

El Nasdaq 100 +0,64 %

El S&P 500 +0,50 %, con 10 de los 11 sectores del S&P 500 al alza

Las acciones estadounidenses avanzaron al pesar las esperanzas de un avance diplomático para poner fin al conflicto en Irán sobre los precios del petróleo y mejorar el sentimiento general del mercado. El entusiasmo de los inversores se vio también reforzado por el sólido debut bursátil de SpaceX, que añadió impulso a las ganancias de Wall Street.

Una fuerte subida de los valores financieros contribuyó a elevar el Dow Jones Industrial Average, que ganó 353,46 puntos, o un +0,70 %. El S&P 500 avanzó un +0,50 %, mientras que el Nasdaq Composite subió un +0,31 %.

El Russell 2000 sumó un +0,79 %, alcanzando un nuevo máximo histórico de 2.943,99 puntos.

En términos semanales, el S&P 500 ganó un +0,35 %, el Nasdaq Composite cedió un -0,16 %, el Dow Jones subió un +0,82 % y el Russell 2000 avanzó un +3,10 %.

Las acciones de SpaceX se dispararon en su primer día de cotización, en un debut que superó plenamente las expectativas del mercado. El título se fijó en 135 $ por acción y subió un +19,22 %, para cerrar en 160,95 $. La operación se convirtió en la mayor salida a bolsa de la historia y, al cierre de la sesión, SpaceX se situó como la sexta empresa cotizada más grande de EE. UU. El debut también convirtió a Elon Musk en el primer billonario del mundo.

En cuanto a noticias corporativas, según Bloomberg, Roku estaría estudiando su venta, de acuerdo con fuentes cercanas a la operación.

Exxon Mobil también está evaluando posibles objetivos de adquisición, entre ellos la australiana Woodside Energy Group, en su búsqueda de ampliar su exposición al gas natural licuado y reforzar su posición en los mercados asiáticos, según personas conocedoras del asunto.

Blackstone se encuentra en conversaciones preliminares sobre una posible adquisición de H&R REIT, una empresa canadiense propietaria de edificios de apartamentos y otros activos inmobiliarios.

Flutter Entertainment ha anunciado su intención de abandonar la Bolsa de Londres, aproximadamente dos años después de trasladar su cotización principal a Nueva York. La decisión es un ejemplo más de una empresa que deja el mercado británico para priorizar su actividad en EE. UU.

Sector con mejores resultados del S&P 500

Materiales +1,83 %, donde Mosaic +7,59 %, Albemarle +7,42 % y FMC +5,15 %

Sector con peores resultados del S&P 500

Salud -0,16 %, donde Eli Lilly & Co -2,41 %, Zoetis -2,25 % y Revvity -1,83 %

Empresas de gran capitalización

Alphabet +0,45 %, Amazon -1,23 %, Apple -1,52 %, Meta Platforms -0,36 %, Microsoft +0,10 %, Nvidia +0,16 % y Tesla +1,82 %

Tecnologías de la información

Mejor rendimiento: Seagate Technology +7,25 %

Peor rendimiento: Adobe -6,76 %

Materiales y minería

Mejor rendimiento: Mosaic +7,59 %

Peor rendimiento: Sherwin-Williams +0,13 %

Índices bursátiles europeos

El CAC 40 +1,83 %

El DAX +1,76 %

El FTSE 100 +1,63 %

Materias primas

El oro al contado +0,21 % hasta situarse en 4.218,77 $ la onza

La plata al contado +0,90 % hasta situarse en 67,98 $ la onza

El West Texas Intermediate -2,39 % hasta situarse en 84,29 $ el barril

El crudo Brent -2,63 % hasta situarse en 86,76 $ el barril

El oro cerró el viernes con una subida del +0,21 %, situándose en 4.218,77 $ por onza troy, después de haber tocado el jueves su nivel más bajo desde noviembre, en 4.022 $. En términos semanales, el metal retrocedió un -2,54 %.

Las expectativas de endurecimiento monetario en EE. UU. y la fortaleza del dólar han frenado parte del impulso que venía sosteniendo el rally del oro desde 2023.

El retroceso del oro ha reabierto el debate sobre la duración de su rally récord, incluso cuando los riesgos geopolíticos, los déficits fiscales y las compras de los bancos centrales continúan respaldando su tesis alcista a largo plazo.

Tras marcar un récord de 5.594,82 $ en enero, el oro al contado ha caído un -24,60 %, ya que la guerra con Irán impulsó los precios del petróleo y avivó las apuestas por subidas de tipos.

Los sólidos datos del mercado laboral estadounidense reforzaron las expectativas de subidas de tipos y llevaron al oro por debajo de su media móvil de 200 días por primera vez en dos años y medio.

Este nivel técnico clave, vigilado de cerca y que ahora actúa como resistencia en los 4.446 $, sugiere que la dinámica del mercado podría haber cambiado.

Las salidas de capital de los ETFs respaldados por oro alcanzaron las 16 toneladas en mayo y 7 toneladas en la primera semana de junio.

La plata al contado avanzó un +0,90 % el viernes hasta los 67,98 $. En términos semanales, el metal ganó un +0,24 %.

Los precios del crudo Brent cayeron hasta su nivel más bajo desde principios de marzo, ya que los operadores ganaron confianza en que se podría alcanzar un acuerdo de paz entre EE. UU. e Irán a corto plazo.

Los futuros del Brent cerraron la sesión en 86,76 $ por barril, con una caída de 2,34 $, o un -2,63 %.

El WTI estadounidense terminó la sesión en 84,29 $, un descenso de 2,06 $, o un -2,39 %, que marcó su nivel de cierre más bajo desde el 17 de abril.

En términos semanales, tanto el Brent como el WTI registraron pérdidas del -6,60 %.

El sentimiento se vio influido por la evolución geopolítica, tras la retirada el jueves por parte del presidente de EE. UU. de la amenaza de ataques aéreos contra Irán. Al mismo tiempo, la agencia de noticias iraní Mehr informó de que las negociaciones finales sobre el memorando se centrarían en los asuntos nucleares y económicos, dejando fuera el programa de misiles iraní.

La agencia iraní IRNA también informó de que las conversaciones nucleares tendrían lugar en un plazo de 60 días a partir de la firma del memorando.

Aun así, una limitación clave persiste: los inventarios mundiales y regionales de petróleo siguen siendo bajos y podrían seguir descendiendo. Cualquier acuerdo necesitaría tiempo para traducirse en flujos de suministro ininterrumpidos, lo que limita el potencial bajista inmediato de los precios.

La semana comenzó con una elevada tensión tras el derribo por parte de Irán de un helicóptero y un dron estadounidense no tripulado, así como el lanzamiento de misiles y drones contra bases militares de EE. UU. en países vecinos. Las fuerzas estadounidenses respondieron atacando sistemas de radar y posiciones de misiles iraníes, mientras el presidente de EE. UU. llegó a amenazar con golpear infraestructuras civiles iraníes e invadir la isla de Kharg. Los ataques israelíes en el Líbano también alimentaron el temor de que un posible acuerdo pudiera frustrarse.

Los ataques ucranianos contra refinerías rusas continuaron, con al menos seis instalaciones afectadas durante la semana, lo que llevó la utilización de las refinerías en Rusia a situarse claramente por debajo de los 4,0 millones de barriles diarios. Los ataques a depósitos de petróleo y puertos también han presionado los flujos de exportación. Los envíos desde los puertos occidentales de Rusia apuntan este mes a cerca de 1,7 millones de barriles diarios, aproximadamente 800.000 barriles diarios por debajo de los niveles de mayo.

Informes adicionales indicaron que un número creciente de petroleros apagaron sus transpondedores y lograron atravesar el estrecho. En Asia, las importaciones de crudo de China en mayo cayeron a su nivel más bajo en más de ocho años, en línea con los datos de seguimiento de petroleros publicados anteriormente.

En América del Norte, las interrupciones de producción en Alberta debidas a un incendio en una instalación y condiciones meteorológicas adversas podrían intensificar los descensos en Cushing. Las reservas totales de crudo, productos y reserva estratégica de petróleo de EE. UU. han caído más de 128 millones de barriles, o un 7,6 %, desde la semana terminada el 3 de abril.

Arabia Saudí recortó su precio oficial de venta del Arab Light para Asia en 6,00 $ por barril, mientras que la OPEP-7 elevó los cupos de producción conjuntos en otros 188.000 barriles diarios con efecto desde julio.

Nota: los datos corresponden al 12 de junio de 2026 a las 16.00 EDT

Divisas

El EUR -0,02 % para situarse en 1,1575 $

La GBP -0,10 % para situarse en 1,3402 $

El bitcoin +0,22 % para situarse en 63.478,57 $

El ethereum -0,45 % para situarse en 1.663,44 $

El índice del dólar subió un +0,12 % el viernes hasta 99,81, después de haber tocado el jueves su nivel más bajo en una semana. A pesar de ese rebote, el índice cerró la semana con una caída del -0,20 %.

El euro cedió un -0,02 % hasta 1,1575 $, manteniéndose cerca de su máximo de una semana. No obstante, registró una ganancia semanal del +0,49 % tras la primera subida de tipos de interés del Banco Central Europeo en tres años, anunciada el jueves.

La libra esterlina bajó un -0,10 % el viernes hasta 1,3402 $. Los datos que mostraron una contracción de la economía del Reino Unido en abril tuvieron escaso efecto inmediato sobre la divisa. En el conjunto de la semana, sin embargo, la libra ganó un +0,47 % frente al dólar estadounidense.

El dólar subió un +0,19 % frente al yen japonés hasta los 160,21 yenes, manteniéndose cerca de un nivel que con frecuencia genera inquietud sobre una posible intervención de Tokio. En términos semanales, no obstante, el billete verde cedió un -0,05 % frente al yen.

Renta fija

El bono estadounidense a 10 años +1,7 pb hasta alcanzar el 4,489 %

El bono alemán a 10 años -3,5 pb hasta alcanzar el 3,000 %

El gilt británico a 10 años -7,0 pb hasta alcanzar el 4,837 %

Los rendimientos del Tesoro estadounidense subieron desde mínimos de una semana el viernes, ya que los inversores dirigieron su atención a la reunión de política monetaria del FOMC de esta semana, la primera presidida por Kevin Warsh.

El rendimiento del bono del Tesoro a dos años, que suele moverse estrechamente ligado a las expectativas sobre los tipos de los fondos federales, subió +2,1 pb hasta el 4,093 %.

El bono estadounidense a 10 años avanzó +1,7 pb hasta alcanzar el 4,489 %, mientras que en el extremo largo de la curva el rendimiento a 30 años subió +1,4 pb hasta el 4,973 %.

El diferencial entre los bonos del Tesoro a dos y diez años se amplió 2,9 pb durante la semana hasta los 39,6 pb, frente a los 36,7 pb de la semana anterior.

En términos semanales, el rendimiento a dos años cayó -6,2 pb, el de diez años retrocedió -3,3 pb y el de treinta años cedió -2,6 pb.

Se espera de forma generalizada que el FOMC mantenga los tipos de interés sin cambios el miércoles. Sin embargo, los inversores estarán pendientes de cualquier señal de que el comité pueda eliminar su sesgo acomodaticio de la declaración, especialmente en un contexto de fortaleza reciente del mercado laboral y una inflación que se mantiene muy por encima del objetivo del 2,0 % de la Fed. Cualquier debate sobre la reducción del balance también es probable que centre la atención del mercado.

Los mercados seguirán de cerca asimismo la comunicación de Warsh durante la rueda de prensa. Jerome Powell continuará en la Fed como gobernador y seguirá votando en las decisiones sobre tipos de interés.

Según la herramienta FedWatch de CME Group, los operadores de futuros de fondos federales descuentan subidas de tipos de 20,0 pb en 2026, por debajo de los 25,8 pb descontados hace una semana. Asimismo, descuentan ahora una probabilidad del 1,5 % de que se produzca un recorte de tipos de 25 pb en la reunión del FOMC de junio, frente al 2,8 % de la semana anterior.

Los rendimientos de los bonos soberanos de la eurozona bajaron el viernes.

Los bonos de vencimiento más corto, habitualmente más sensibles a la política de los bancos centrales, lideraron el avance. El rendimiento alemán a dos años cayó -6,0 pb hasta el 2,638 %, después de haber tocado anteriormente su nivel más bajo en diez días, en el 2,581 %. En el extremo largo de la curva, el rendimiento a 30 años retrocedió -1,6 pb.

El rendimiento del Bund alemán a 10 años cayó -3,5 pb hasta el 3,000 %. El BTP italiano a 10 años cedió 6,1 pb, dejando el diferencial sobre los Bunds en 73,5 pb, 2,0 pb menos que los 75,5 pb de la semana anterior. En el conjunto de la semana, el rendimiento del BTP a 10 años cayó -6,9 pb.

En términos semanales, la curva alemana también mostró un patrón de pendiente alcista, ya que los rendimientos a corto plazo cayeron con más intensidad que los de largo plazo. El rendimiento del Schatz alemán a dos años descendió -6,9 pb, el del Bund a 10 años cayó -4,9 pb y el rendimiento a 30 años retrocedió -2,8 pb.

Los mercados de renta fija han continuado reaccionando estrechamente a los titulares relacionados con la guerra, ya que los inversores valoran el riesgo de un cierre prolongado del estrecho de Ormuz. Una interrupción sostenida y unos precios del petróleo más altos podrían alimentar presiones inflacionistas más amplias y obligar a los bancos centrales a mantener o endurecer aún más su política monetaria.

Ese riesgo se vio reforzado por la subida de tipos del BCE el jueves, cuyo objetivo fue contener la inflación antes de que el encarecimiento de los combustibles se trasladara de forma más generalizada a la economía.

En su rueda de prensa posterior a la decisión, la presidenta del BCE, Christine Lagarde, ofreció escasas precisiones sobre la senda futura de la política monetaria, reiterando que el banco central seguiría dependiendo de los datos y actuando reunión a reunión.

Los mercados monetarios descuentan actualmente una probabilidad de alrededor del 30 % de una nueva subida de tipos del BCE en julio, mientras que un movimiento en septiembre se da por casi descontado.

Nota: los datos corresponden al 12 de junio de 2026 a las 16.00 EDT

Aunque se han hecho todos los esfuerzos posibles para verificar la exactitud de esta información, EXT Ltd. (en adelante, "EXANTE") no se hace responsable de la confianza que cualquier persona pueda depositar en esta publicación o en cualquier información, opinión o conclusión contenida en ella. Las conclusiones y opiniones expresadas en esta publicación no reflejan necesariamente la opinión de EXANTE. Cualquier acción realizada sobre la base de la información contenida en esta publicación es estrictamente bajo su propio riesgo. EXANTE no se hará responsable de ninguna pérdida o daño relacionado con esta publicación.

Este artículo se presenta a modo informativo únicamente y no debe ser considerado una oferta ni solicitud de oferta para comprar ni vender inversión alguna ni los servicios relaciones a los que se pueda haber hecho referencia aquí. Operar con instrumentos financieros implica un riesgo significativo de pérdida y puede no ser adecuado para todos los inversores. Los resultados pasados no garantizan rendimientos futuros.

Regístrese para recibir perspectivas de los mercados

Regístrese

para recibir perspectivas

de los mercados

Suscríbase ahora

Artículos relacionados

La factura del acceso: EE. UU. recurre a la Sección 301Diarias27 jul 2026

La factura del acceso: EE. UU. recurre a la Sección 301Diarias27 jul 2026 El BCE mantiene su postura, pero los riesgos van en aumentoDiarias24 jul 2026

El BCE mantiene su postura, pero los riesgos van en aumentoDiarias24 jul 2026 ¿Podrá el Banco de Inglaterra relajar realmente su política?Diarias23 jul 2026

¿Podrá el Banco de Inglaterra relajar realmente su política?Diarias23 jul 2026 ¿Está mejorando el sentimiento alemán gracias al optimismo reformista?Diarias22 jul 2026

¿Está mejorando el sentimiento alemán gracias al optimismo reformista?Diarias22 jul 2026

Creado por profesionales. Para profesionales.