Will Trump and Xi agree?

What to look out for today

Companies reporting on Wednesday, 13 May: Alibaba Group, Cisco Systems, Nebius, Siemens, Takeda Pharmaceutical, Tencent

Key data to move markets today

JAPAN: Current Account

EU: French CPI, Eurozone GDP, Industrial Production and Employment Rate and speeches by ECB Chief Economist Philip Lane and ECB President Christine Lagarde

UK: A speech by BoE MPC member Catherine Mann

USA: PPI and a speech by Minneapolis Fed President Neel Kashkari

Global Macro Updates

US inflation rising leaves the Fed little room for change. April's CPI report landed with more weight than markets had hoped. Headline inflation climbed to 3.8% y/o/y, the highest reading since May 2023, while core CPI came in at 2.8% annually, above both consensus estimates and the prior month, marking its highest level since September 2025. Headline CPI came in at 0.6% m/o/m, while core CPI was +0.4% m/o/m. Energy prices surged 3.8% on the month, accounting for roughly 40% of the headline increase amid ongoing supply disruptions tied to the Iran conflict. Food prices posted their largest monthly gain since August 2022, reflecting elevated fertiliser and energy input costs. While the headline came broadly in line with expectations, the upside surprise in core is the more consequential signal for policy, as it underscores that new Fed leadership won't result in an immediate dovish shift.

The reaction among institutional analysts was notably hawkish. According to Reuters. Goldman Sachs, which had already pushed its first cut call back to December 2026, now projects PCE inflation tracking near 3% through the remainder of the year, above the Fed's 2% mandate. UBS and BofA had previously warned that sticky core services and persistently elevated PCE would likely keep the Fed on hold for longer. Analysts echoed similar caution, noting that underlying inflation dynamics argue against any near-term pivot. However, Citi argued that once transitory distortions, including shelter-related effects tied to last year's government shutdown, are excluded, underlying inflation remains reasonably close to target.

The divisions within the FOMC itself are equally telling. At the 29 April meeting, three Fed governors, Cleveland’s Beth Hammack, Minneapolis’ Neel Kashkari and Dallas’ Lorie Logan, formally dissented against language perceived as signalling an easing bias, each arguing that the next policy move could be a hike rather than a cut. Hammack described inflation pressures as ‘broad based,’ while Kashkari stated that ‘a series of rate hikes could be warranted’ should energy-driven shocks prove persistent. Logan similarly pointed to Middle East supply disruptions as a structural rather than transitory risk. Governor Stephen Miran, the lone dissent in favour of easing, voted for a 25 bps cut, yet even he had tempered his full-year outlook in mid-April, citing ‘less favourable’ inflation developments. With incoming Fed Chair Kevin Warsh inheriting a fractured committee and core inflation still above target, the threshold for policy action has risen considerably.

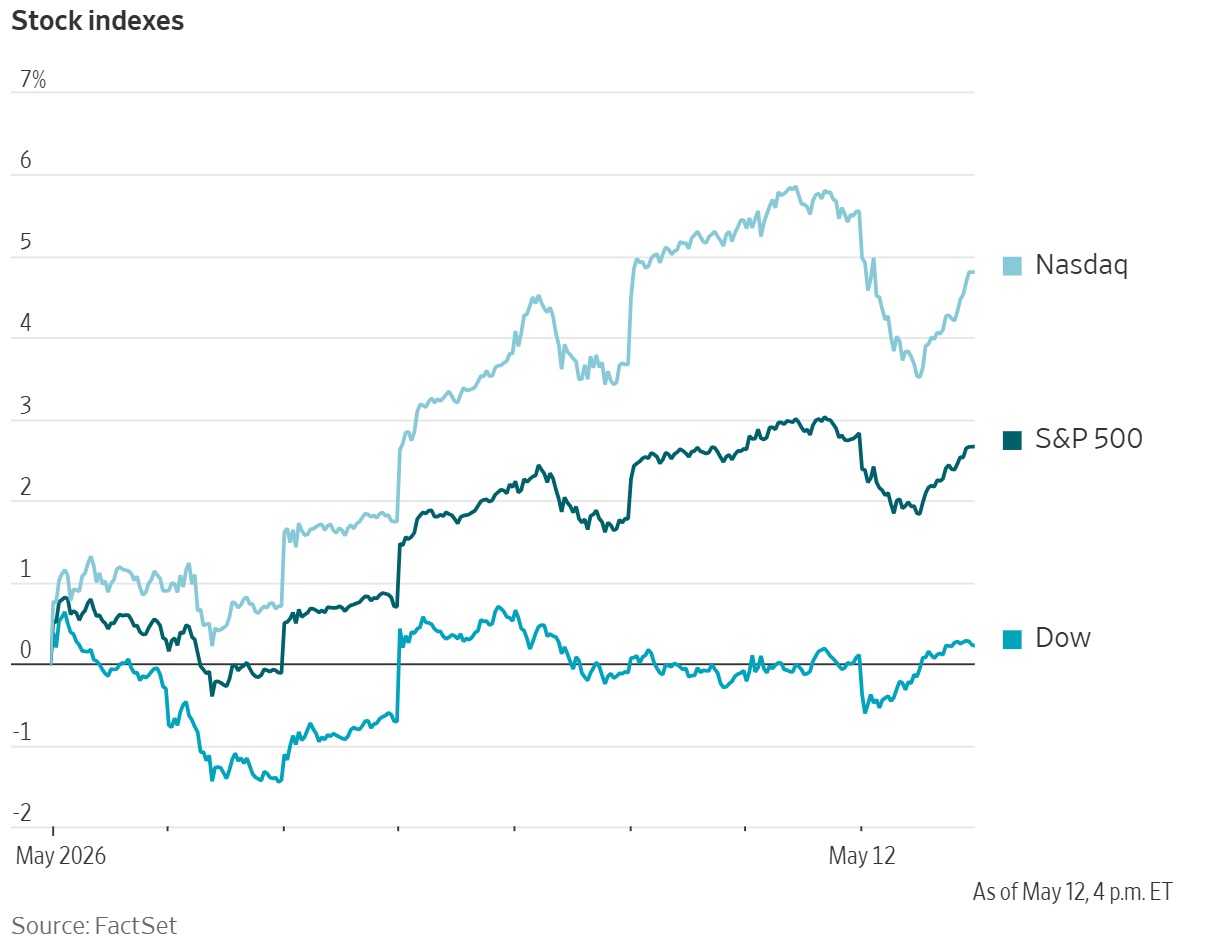

US Stock Indices

Dow Jones Industrial Average +0.11%

Nasdaq 100 -0.87%

S&P 500 -0.16%, with 7 of the 11 sectors of the S&P 500 up

On Tuesday the S&P 500 and the Nasdaq closed lower due to hotter-than-expected inflation data and amid increasing doubts about the US - Iran ceasefire.

The Nasdaq Composite was -0.71%, or -185.92 points to 26,088.20 and the S&P 500 fell -0.16%, or -11.88 points to 7,400.96. However, the Dow Jones rose +0.11%, or 56.09 points, to 49,760.56.

In corporate news, Alphabet’s Google said on Tuesday that it is in talks with Elon Musk’s SpaceX regarding future launches for its Project Suncatcher, an orbital data centre project.

EBay rejected a $56 billion takeover bid from GameStop over financing doubts, calling the proposal "neither credible nor attractive."

S&P 500 Best performing sector

Healthcare +1.93%, with Humana +7.69%, Centene +5.23% and Zimmer Biomet Holdings +4.76%

S&P 500 Worst performing sector

Consumer Discretionary -1.06%, with Norwegian Cruise Line Holdings -3.50%, Carvana -3.29% and Builders FirstSource -2.80%

Mega Caps

Alphabet -0.33%, Amazon -1.18%, Apple +0.72%, Meta Platforms +0.69%, Microsoft -1.18%, Nvidia +0.61% and Tesla -2.60%

Information Technology

Best performer: Zebra Technologies +11.44%

Worst performer: Qualcomm -11.46%

Materials and Mining

Best performer: CF Industries +5.91%

Worst performer: Amcor -2.44%

Corporate Earnings Reports

Posted on Tuesday, 12 May

Qnity Electronics quarterly revenue +18% to $1.32 bn vs $1.27 bn estimate

Adjusted EPS at $1.08 vs $0.94 estimate

Jon Kemp, Qnity’s Chief Executive Officer, said, “Qnity had a tremendous start to the year, outperforming our expectations and delivering our eighth consecutive quarter of strong profitable organic growth with double-digit gains in both segments. These results reflect the strength of our integrated portfolio – spanning advanced chips, advanced packaging and interconnects, and thermal management – as well as our ability to innovate side-by-side with customers to power the next leap in AI and emerging technologies.”— see report

Zebra Technologies quarterly revenue +14.3% to $1.495 billion vs. $1.48 bn estimate

Adjusted EPS at $4.75 vs $4.25 estimate

Bill Burns, Chief Executive Officer of Zebra Technologies, said, “Our strong first quarter results demonstrate the durability of demand for our innovative technology, with organic growth across our segments and regions, led by strength in our manufacturing end market. Elo Touch also contributed solid profitable growth as we begin to drive synergies. These results underscore the value Zebra delivers as the foundation for intelligent operations across the frontline, helping customers operate more efficiently and effectively."— see report

European Stock Indices

CAC 40 -0.95%

DAX -1.62%

FTSE 100 -0.04%

Commodities

Gold spot -0.43% to $4,713.65 an ounce

Silver spot +0.53% to $86.54 an ounce

West Texas Intermediate +3.87% to $102.05 a barrel

Brent crude +2.97% to $107.45 a barrel

Gold prices eased on Tuesday, as heightened uncertainty in the Middle East and stronger-than-expected US inflation data tempered expectations for Federal Reserve rate cuts.

Spot gold fell -0.43% to $4,713.65 per ounce.

India raised import tariffs on gold and silver to 15% from 6%, aiming to curb overseas purchases and alleviate pressure on the country s foreign exchange reserves.

Spot silver rose +0.53% to $86.54 per ounce, after reaching its highest level since 11 March earlier in the session.

Oil prices settled higher for a third consecutive session on Tuesday, as sharp differences between Washington and Tehran over a proposal to end the war in the Middle East heightened concerns that supply disruptions roiling the global oil market could be prolonged.

Brent crude futures gained $3.10, or +2.97%, to settle at $107.45 a barrel, while US WTI futures rose $3.80, or +3.87%, to close at $102.05.

Crude benchmarks advanced on Tuesday afternoon amid escalating Iran-related risks and limited diplomatic progress. President Donald Trump said the US was under no urgency to reach a deal, arguing that the blockade is depriving Iran of funds and reiterating that a nuclear weapon remains unacceptable. Two US officials said Trump is leaning toward military action, with options including resuming Project Freedom (the suspended Strait of Hormuz escort operation) or restarting the bombing campaign against the roughly 25% of targets not yet struck.

Israel is reportedly advocating for a special forces operation to secure Iran’s enriched uranium stockpile, although Trump is said to be hesitant given the associated risks. No action is expected before Trump returns from his China trip (Wednesday through Friday), during which Iran is expected to be discussed with President Xi.

Separately, a senior IRGC Navy officer said Iran has redefined the Strait of Hormuz as a ‘vast operational area,’ with Iranian media reporting that its effective width has expanded from 20 to 30 miles to 200 to 300 miles.

The US Energy Information Administration said on Tuesday that it now assumes the strait will be effectively closed through late May, implying substantially larger losses of Middle Eastern oil and gas supplies than in its previous forecasts. The agency had earlier expected the waterway to remain shut through late April.

The EIA added that, even after flows resume through the Strait of Hormuz, oil output and trade patterns are unlikely to return to pre-conflict levels until at least late 2026 or early 2027.

The EIA estimates that 10.5 million barrels per day (bpd) of output were lost across the Middle East during April due to the strait’s closure, which constrained exports. Other estimates place the supply losses substantially higher.

The prolonged loss of Middle Eastern supply is forcing countries to draw down oil and gas stockpiles. The EIA now expects global oil inventories to decline by about 2.6 million bpd this year, sharply exceeding its prior forecast of a 300,000 bpd drop.

Note: As of 4 pm EDT 12 May 2026

Currencies

EUR -0.39% to $1.1736

GBP -0.51% to $1.3535

Bitcoin -1.51% to $80,565.08

Ethereum -2.36% to $2,284.93

The dollar held near a one-week high on Wednesday as risk sentiment deteriorated.

The euro was down -0.39% at $1.1736, while sterling traded -0.51% lower at $1.3535.

The US dollar index rose +0.39% to 98.29, hovering near its strongest level in a week.

The Japanese yen weakened -0.29% to ¥157.56 per dollar.

US Treasury Secretary Scott Bessent said the US and Japan agree that excessive volatility in currency markets is undesirable, comments viewed as lending some support to Tokyo's recent intervention to bolster the yen.

Fixed Income

US 10-year Bond +5.3 basis points to 4.457%

German 10-year Bund +6.4 basis points to 3.100%

UK 10-year gilt +10.3 basis points to 5.107%

US Treasury yields rose across the curve on Tuesday after CPI came in at 3.8% in April from 3.3% in March.

The 10-year Treasury yield was pushed to its highest closing level since 4 May 2025. The benchmark yield rose +5.3 bps to 4.462%. The 2-year Treasury yield, which typically tracks expectations for the Fed fund rates, was +4.5 bps to 3.994%. The 30-year Treasury yield climbed +4.2 bps to 5.027%.

The Treasury curve spread between 2-year and 10-year yields stood at 46.8 bps, edging up 0.8 bps from Monday’s 46 bps.

A 10-year Treasury auction had lukewarm demand, with a bid-to-cover ratio of 2.4x.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing 9.3 bps of rate hikes in 2026, higher than the 6.1 bps priced in a week ago. Fed funds futures traders are now pricing in a 2.9% probability of a 25 bps rate cut at June’s FOMC meeting, lower than last week’s 5.6% probability.

Germany’s 2-year yield rose +7.2 bps to 2.714%. The 10-year Bund yield was +6.4 bps on the day at 3.100%. At the long end, the 30-year yield increased +5.7 bps to 3.625%.

Italy’s 10-year yield was +8.5 bps at 3.863%, leaving the spread over Bunds at 76.3 bps, 2.1 bps higher than Monday’s 74.2 bps.

UK gilts suffered significant losses as the uncertainty around Sir Keir Starmer’s premiership weighed on markets. The 10-year yield soared +9.7 bps to 5.098%, while the rate sensitive 2-year was +7.5 bps to 4.547%. At the long end, the 30-year rose +8.2 bps to 5.769%.

Note: As of 4 pm EDT 12 May 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.