¿Puede la IA compensar la incertidumbre macroeconómica?

Qué debemos observar hoy

Empresas que presentan sus informes de resultados hoy lunes, 27 de abril: Verizon

Datos clave que moverán los mercados hoy

UE: confianza del consumidor de Alemania de GfK y discurso de la miembro del Comité Ejecutivo del BCE, Isabel Schnabel

Actualizaciones macroeconómicas mundiales

Un rally impulsado por la IA. en un contexto macroeconómico cada vez más marcado por la incertidumbre geopolítica, el conflicto en evolución en Oriente Próximo y sus implicaciones para los mercados energéticos, las expectativas de inflación y el sentimiento de riesgo global, la renta variable estadounidense ha encontrado en el sector tecnológico un sólido pilar de resiliencia. La temporada de resultados del primer trimestre ha reforzado esta tendencia, ofreciendo a los inversores un foco de claridad y optimismo en un entorno por lo demás frágil.

El impulso de los beneficios ha sido claramente positivo. La tasa de crecimiento combinada de los beneficios del S&P 500 en el 1T ha subido hasta el 15,1 %, frente al 12,6 % al inicio del periodo de publicación de resultados y el 13,2 % de la semana anterior. El 81,3 % de las empresas ha batido las expectativas de beneficios, con una sorpresa agregada superior al 12,3 %, lo que refleja tanto la solidez operativa del sector como la cautela con que las compañías habían planteado sus perspectivas.

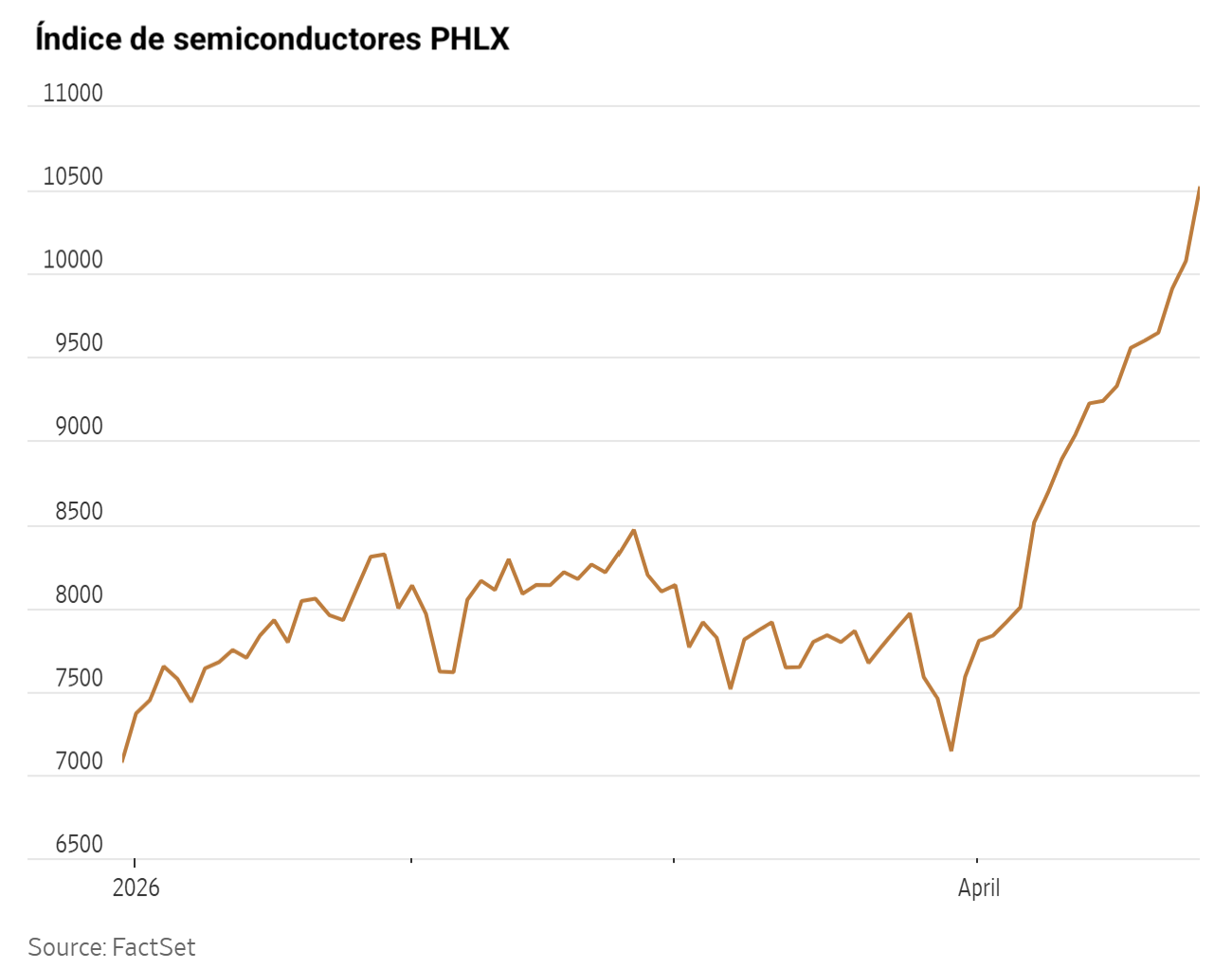

El motor de esta fortaleza es la continua aceleración de la demanda de inteligencia artificial, que se ha consolidado como el gran tema secular de los beneficios empresariales. Las compañías de semiconductores siguen siendo las más beneficiadas, con el índice SOX prolongando un extraordinario rally de varias semanas, aunque la ola alcanza también a empresas de energía, construcción e infraestructuras ligadas al desarrollo de centros de datos. Más allá de los números, esta temporada ha marcado un punto de inflexión en la comunicación corporativa: cada vez más compañías empiezan a cuantificar las ganancias de productividad atribuibles a la IA, lo que refuerza la solidez estructural de la tendencia.

La intensidad de la actividad dentro del ecosistema de IA y semiconductores ha sido especialmente evidente. Los resultados del 1T de Intel, que superaron las estimaciones, y unas perspectivas por encima del consenso han catalizado una brusca revisión al alza de su posicionamiento, con los analistas destacando una fortaleza infravalorada en los precios de las CPU y las capacidades de envasado avanzado. El informe ha reavivado también el impulso en valores expuestos a las CPU como ARM y AMD, a medida que las emergentes cargas de trabajo de "IA agéntica" impulsan un nuevo ciclo de demanda de computación de propósito general. Esta tendencia ha sido validada por compromisos de despliegue a gran escala, incluida la asociación plurianual de Meta con Amazon para desplegar cientos de miles de CPU AWS Graviton.

La asignación de capital en el ecosistema de la IA sigue acelerándose. El plan comunicado por Google de invertir hasta 40.000 millones de dólares adicionales en Anthropic, comenzando con una inversión inicial de 10.000 millones a una valoración de 350.000 millones, pone de manifiesto la escala del capital que se moviliza para asegurar el liderazgo en IA. El compromiso asociado de ampliar la capacidad de computación, con hasta 5 gigavatios en cinco años a través de Google Cloud, subraya la enorme intensidad de infraestructura que sustenta la tendencia.

Al mismo tiempo, las limitaciones de oferta siguen siendo un rasgo definitorio del panorama. Los informes indican que la disponibilidad de GPU en las principales plataformas en la nube podría seguir siendo escasa durante 2026, ya que los grandes proveedores de servicios en la nube priorizan las cargas de trabajo internas y los grandes clientes estratégicos. Esta escasez refuerza el poder de fijación de precios en toda la cadena de valor y subraya el desequilibrio estructural entre una demanda que escala rápidamente y una oferta limitada.

Por último, el panorama competitivo sigue evolucionando a escala global. DeepSeek, la empresa china de inteligencia artificial, ha presentado una versión preliminar de sus últimos modelos insignia, lo que supone un desafío incremental para líderes consolidados como OpenAI, Google y Anthropic, y refuerza la dimensión cada vez más geopolítica del liderazgo en IA.

Índices bursátiles estadounidenses

El Dow Jones Industrial Average -0,16 %

El Nasdaq 100 +1,95 %

El S&P 500 +0,80 %, con 5 de los 11 sectores del S&P 500 al alza

Un vertiginoso rally de las acciones de Intel impulsó al S&P 500 y al Nasdaq a nuevos máximos históricos el viernes, mientras los inversores optaban por ignorar los riesgos geopolíticos imperantes y aumentaban su exposición a los valores tecnológicos.

Intel se disparó un +23,70 %, alcanzando su primer máximo histórico desde el apogeo de la burbuja puntocom en el año 2000, tras anunciar unas ventas más sólidas de lo esperado y una fuerte demanda de sus unidades centrales de procesamiento por parte de los centros de datos.

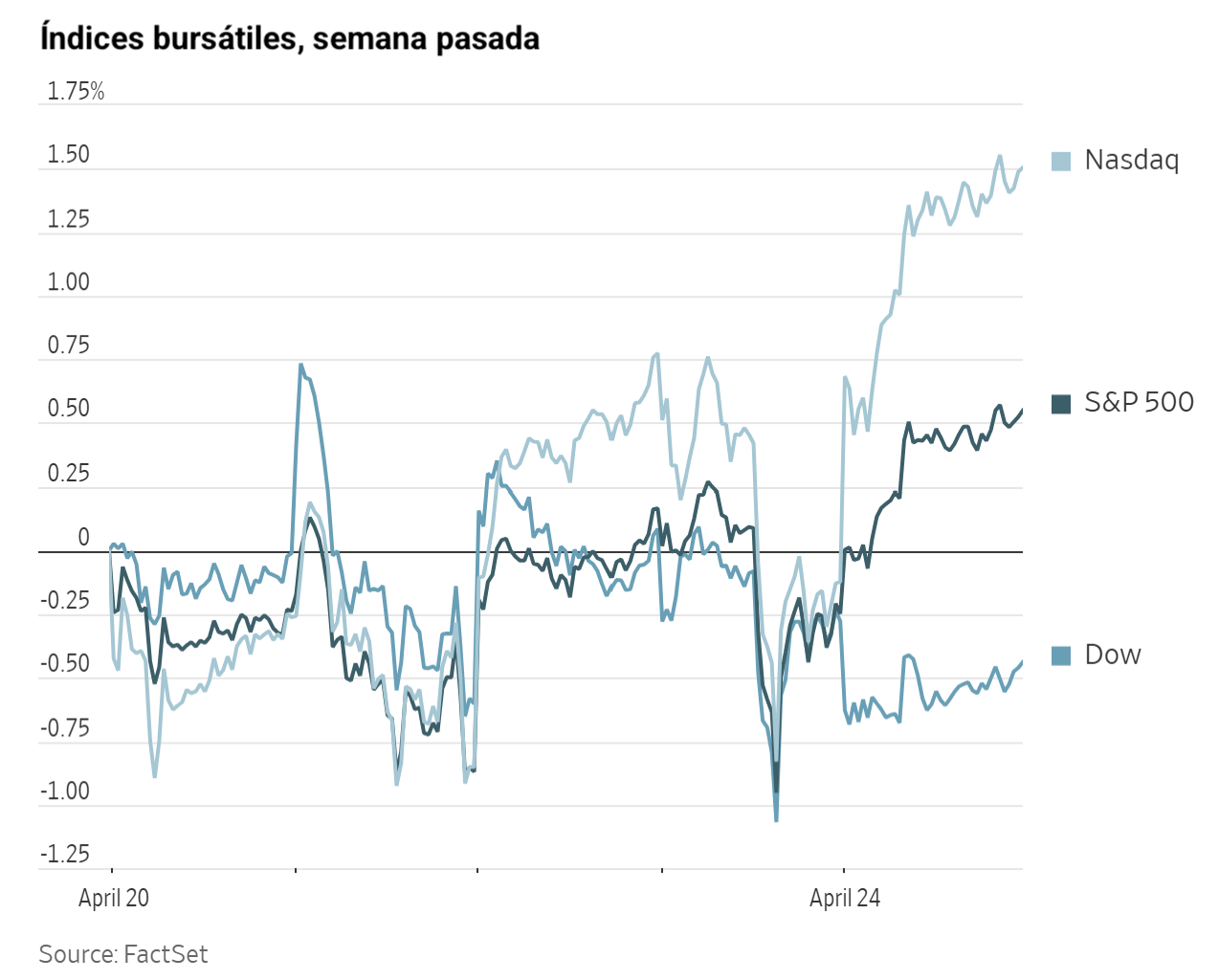

El rally impulsó al Nasdaq un +1,63 %, marcando su quinto máximo histórico del año, mientras el S&P 500 avanzó un +0,80 % hasta su noveno récord en 2026. Al margen de la fiesta tecnológica, el Dow Jones Industrial Average, que retiró a Intel de su composición en 2024, cerró en negativo con una caída del -0,16 %.

Los excepcionales resultados de Intel se enmarcan en una sólida temporada de resultados que ha respaldado la resiliencia del mercado en medio de la volatilidad desencadenada por el conflicto con Irán.

El S&P 500 registró una ganancia semanal del +0,79 %, mientras que el Nasdaq avanzó un +1,77 %, anotando ambos su cuarta semana consecutiva de ganancias. El Dow, sin embargo, cayó un -1,05 % durante la semana.

La confianza de los inversores en el sector tecnológico se extendió al conjunto de la industria de semiconductores, llevando al índice de semiconductores PHLX a su 18ª ganancia consecutiva, su racha más larga en la historia, de acuerdo con datos de Dow Jones Market Data. El índice subió un +10,02 % durante la semana.

Según datos de LSEG I/B/E/S, el crecimiento interanual de los beneficios del S&P 500 en el primer trimestre se proyecta en el +16,1 %, cifra que asciende al +17,2 % excluyendo el sector de energía. De las 139 empresas del índice que han publicado resultados hasta la fecha, el 81,3 % ha superado las estimaciones de beneficios y el 77,4 % ha registrado ingresos por encima de las expectativas. El crecimiento interanual de los ingresos se proyecta en el 9,7 % para el trimestre, aumentando al 10,2 % al excluir el sector de la energía.

Tecnologías de la información y salud, ambos con el 100,0 %, son los sectores con mayor proporción de empresas superando las estimaciones. Materiales, con un factor de sorpresa del 31,6 %, es el sector que más ha superado las expectativas de beneficios. En servicios de comunicación, el 50,0 % de las empresas han publicado resultados por debajo de las estimaciones, siendo este el sector con el factor de sorpresa más bajo, del 0,0 %, igualando de media las estimaciones. El factor de sorpresa del S&P 500 se sitúa en el 9,2 %. La relación precio-beneficio prospectiva a cuatro trimestres del S&P 500 se sitúa en 20,8 veces.

Esta semana está previsto que 178 empresas del S&P 500 publiquen sus resultados del 1T.

En cuanto a noticias corporativas, el nuevo medicamento para adelgazar Foundayo de Eli Lilly & Co. ha tenido un arranque lento, según los últimos datos de prescripción, lo que pone de relieve los retos que la compañía podría afrontar en su pugna con su rival Novo Nordisk.

Newmont, el mayor productor de oro del mundo, ha anunciado un programa de recompra de acciones por valor de 6.000 millones de dólares, aprovechando la histórica escalada de los precios del metal para retribuir a sus accionistas.

Google, de Alphabet, ha anunciado su intención de invertir hasta 40.000 millones de dólares adicionales en Anthropic, en un mes en el que la compañía ha captado compromisos de financiación de hasta 65.000 millones. Cabe recordar que en febrero Anthropic recaudó 30.000 millones y alcanzó una valoración de 380.000 millones de dólares.

Nike ha anunciado una reducción de plantilla de aproximadamente 1.400 empleados, lo que representa cerca del dos por ciento de su plantilla global, como parte de su estrategia de racionalización de operaciones a escala mundial.

Sector con mejores resultados del S&P 500

Tecnologías de la información +2,46 %, donde Intel +23,60 %, Advanced Micro Devices +13,91 % y Qualcomm +11,12 %

Sector con peores resultados del S&P 500

Salud -1,37 %, donde HCA Healthcare -8,77 %, Boston Scientific 5,51 % y Moderna -4,01 %

Empresas de gran capitalización

Alphabet +1,35 %, Amazon +3,49 %, Apple -0,87 %, Meta Platforms +2,41 %, Microsoft +2,13 %, Nvidia +4,32 % y Tesla +0,69 %

Tecnologías de la información

Mejor rendimiento: Intel +23,60 %

Peor rendimiento: Roper Technologies -2,85 %

Materiales y minería

Mejor rendimiento: Newmont +8,68 %

Peor rendimiento: CF Industries -3,71 %

Informes de resultados empresariales

Publicados el viernes, 24 de abril, a través de The Pulse, nuestra herramienta de noticias en tiempo real basada en inteligencia artificial. Disponible en exclusiva en la plataforma web de EXANTE

Procter & Gamble ha publicado los resultados del tercer trimestre de 2026 con un beneficio por acción básico de 1,59 $, por encima de la estimación de 1,56 $, y unas ventas orgánicas del +3 %, superando la estimación del +1,86 %. Las ventas netas se situaron en 19.124 millones de dólares, por debajo de los 20.580 millones estimados, con un margen bruto del 49,5 %. Los segmentos clave superaron las estimaciones: cuidado del bebé, femenino y familiar crecieron un +3 % frente al +1,47 % estimado, y belleza aumentó un +7 % frente al +2,47 % estimado. La compañía mantiene sus previsiones de beneficio por acción básico para el conjunto del ejercicio en el rango de 6,83 a 7,09 $, frente a la estimación de 6,96 $, y de ventas orgánicas del +4 %, frente a la estimación del +1,45 %. El director financiero de la compañía citó los costes de las materias primas como un factor adverso.

Índices bursátiles europeos

El CAC 40 -0,84 %

El DAX -0,11 %

El FTSE 100 -0,75 %

Materias primas

El oro al contado +0,34 % hasta situarse en 4.708,69 $ la onza

La plata al contado +0,84 % hasta situarse en 75,67 $ la onza

El West Texas Intermediate -2,19 % hasta situarse en 94,88 $ el barril

El crudo Brent -0,50 % hasta situarse en 105,90 $ el barril

El oro avanzó el viernes, aunque registró su primera caída semanal en cinco semanas, ya que las persistentes preocupaciones inflacionarias y la incertidumbre en torno al conflicto entre EE. UU. e Irán siguieron perturbando los mercados financieros.

El oro al contado subió un +0,34 % hasta situarse en 4.708,69 $ por onza, tras haber ganado más de un uno por ciento en un momento anterior de la sesión. No obstante, acumuló una caída del -2,48 % durante la semana.

La plata al contado avanzó un +0,85 % hasta los 75,67 $ por onza el viernes, aunque registró una pérdida semanal del -6,33 %.

Los precios del petróleo, por su parte, experimentaron una notable volatilidad el viernes, cerrando finalmente la semana al alza mientras los participantes del mercado sopesaban las perturbaciones de suministro en curso frente a la posible reanudación de las conversaciones de paz entre EE. UU. e Irán.

Los futuros del crudo Brent cerraron a 105,90 $ por barril, con un descenso de 0,53 $, o un -0,50 %. Los futuros del WTI estadounidense cerraron a 94,88 $ por barril, con una caída de 2,12 $, o un -2,19 % durante el día. Pese a estas pérdidas diarias, el Brent subió un +15,12 % durante la semana, mientras que el WTI avanzó un +10,88 %.

A primera hora de la sesión, los precios del petróleo se dispararon un dos por ciento ante la renovación de los temores de escalada militar en la región, tras la difusión por parte de Irán de imágenes de comandos abordando un buque de carga en el estrecho de Ormuz y la falta de avances en la reapertura de esta ruta marítima estratégica.

Las pérdidas acumuladas en la producción mundial de petróleo se estiman en hasta 14 millones de barriles diarios, con las reservas estratégicas en descenso y los retiros de inventarios, tanto en tierra como flotantes, sin dar señales de frenarse.

La diplomacia sigue bloqueada: EE. UU. e Irán no han logrado cerrar un acuerdo de paz permanente, aunque Trump prorrogó el alto el fuego por tres semanas adicionales mientras mantiene el bloqueo naval. Las tensiones no amainan: las amenazas del presidente de EE. UU. contra los buques sospechosos de minar el estrecho, la incautación iraní de al menos dos embarcaciones y los continuos enfrentamientos entre Israel y Hezbolá siguen poniendo a prueba la frágil tregua.

Los informes apuntan a divisiones internas en el liderazgo iraní, especialmente entre la Administración actual y el Cuerpo de la Guardia Revolucionaria Islámica (CGRI), que han obstaculizado las negociaciones de paz. El bloqueo es también considerado por Irán como una violación del alto el fuego. El ministro de Asuntos Exteriores iraní, Araghchi, tiene previsto visitar Pakistán, Omán y Rusia para mantener conversaciones sobre el conflicto.

El impacto se extiende a escala global, con la escasez de combustible de aviación como principal preocupación. Las aerolíneas siguen cancelando vuelos y la UE estudia obligar a sus Estados miembros a mantener reservas o redistribuir suministros para paliar las escaseces regionales. Goldman Sachs ha advertido además de que las existencias visibles de crudo a escala mundial podrían tocar mínimos históricos a finales de esta semana.

En China, las existencias de crudo han caído en menos de un millón de barriles desde el inicio del conflicto, de acuerdo con Energy Aspects, ya que las importaciones de crudo iraní han alcanzado niveles récord. Mientras las principales refinerías estatales chinas han reducido sus operaciones en torno a un 14 % desde febrero, las refinerías independientes, conocidas como "teapot", han incrementado sus tasas de utilización.

En la Cumbre Global de Materias Primas del Financial Times, las grandes firmas de trading dibujaron un panorama sombrío. Gunvor estimó una caída de la demanda de petróleo de un millón de barriles diarios en marzo y de 2,5 millones en abril. Russell Hardy, director ejecutivo de Vitol, cifró las pérdidas acumuladas por el conflicto en entre 600 y 700 millones de barriles, con el riesgo de superar los 1.000 millones si la situación se prolonga, y estimó una merma de cuatro millones de barriles diarios en la demanda mundial. Por su parte, Trafigura Group proyectó un déficit de suministro de 1.000 millones de barriles, que podría escalar hasta los 1.500 millones si continúan las hostilidades.

Los ataques de Ucrania a la infraestructura energética rusa, incluida la terminal de exportación de Tuapse y las refinerías de petróleo rusas, han desestabilizado aún más el mercado. Según fuentes de Reuters, la producción de crudo ruso ha disminuido entre 300.000 y 400.000 barriles diarios este mes como consecuencia de estos ataques.

Nota: los datos corresponden al 24 de abril de 2026 a las 16.00 EDT

Divisas

El EUR +0,17 % para situarse en 1,1705 $

La GBP +0,30 % para situarse en 1,3506 $

El bitcoin -0,45 % para situarse en 77.575,76 $

El ethereum -0,46 % para situarse en 2.315,88 $

El dólar estadounidense cayó el viernes bajo la presión de dos factores: el cierre de la investigación del Departamento de Justicia sobre el presidente de la Fed, Jerome Powell, y el creciente optimismo ante la posibilidad de que se inicien pronto negociaciones para poner fin al conflicto entre EE. UU., Israel e Irán.

El índice del dólar cayó un -0,28 % hasta 98,51, mientras el euro se apreció un +0,17 % hasta 1,1705 $. Durante la semana, el índice del dólar registró una ganancia del +0,29 %, mientras que el euro acumuló una pérdida del -0,48 % en el mismo periodo.

El yen japonés se fortaleció un +0,17 % frente al dólar estadounidense, cerrando en 159,37 yenes por dólar. La libra esterlina avanzó un +0,30 % hasta situarse en 1,3506 $. Durante la semana, sin embargo, el yen cayó un -0,48 % frente al dólar, mientras que la libra se depreció un -0,06 %.

A lo largo del conflicto, el euro ha estado influido por factores contrapuestos: en ocasiones se ha visto impulsado por las esperanzas de un acuerdo de paz a corto plazo y, en otras, ha sufrido presiones vendedoras ante el temor de que una guerra prolongada pueda causar perturbaciones duraderas en los mercados energéticos mundiales.

La atención del mercado se desplaza ahora hacia una agenda cargada de citas con los bancos centrales: la semana que viene traerá decisiones de política monetaria de la Fed, el BoJ, el BCE y el BoE.

Se espera que la Reserva Federal mantenga su actual postura de política monetaria, ya que sus responsables ponderan el riesgo de un repunte de la inflación derivado del conflicto con Irán frente a la resiliencia continuada de la economía estadounidense.

Se espera que el BCE mantenga su tipo de depósito sin cambios en su reunión del 30 de abril; sin embargo, es probable una subida de tipos en junio, ya que los responsables de política monetaria buscan proteger la economía de la zona euro de los impactos energéticos derivados del conflicto.

El Banco de Inglaterra tiene prevista su reunión el jueves. Aunque los mercados descuentan una subida de tipos antes de que acabe el año, no se espera ningún cambio en la próxima reunión.

En Japón, la inflación subyacente del consumidor en marzo se mantuvo por debajo del objetivo del 2 % del BoJ por segundo mes consecutivo. Los analistas anticipan que las presiones inflacionarias se intensificarán en los próximos meses, a medida que las empresas empiecen a trasladar el encarecimiento del combustible relacionado con el conflicto en Oriente Próximo.

El BoJ concluirá el martes su reunión de política monetaria de dos días con el mantenimiento de los tipos como escenario más probable, dado que la incertidumbre sobre la resolución del conflicto sigue enturbiando las perspectivas económicas y de inflación del país. No obstante, se espera que el banco central deje la puerta abierta a un endurecimiento de su política si las presiones inflacionarias se intensifican.

La ministra de Finanzas japonesa, Satsuki Katayama, reiteró el viernes que las autoridades siguen preparadas para tomar medidas "decisivas" contra los movimientos especulativos en el mercado de divisas, tras declaraciones anteriores en las que subrayó la capacidad y voluntad de intervención de Japón cuando sea necesario y destacó la eficacia de las intervenciones anteriores.

Renta fija

El bono estadounidense a 10 años -2,2 pb hasta alcanzar el 4,307 %

El bono alemán a 10 años -1,4 pb hasta alcanzar el 2,997 %

El gilt británico a 10 años -25,3 pb hasta alcanzar el 4,994 %

Los bonos del Tesoro de EE. UU. avanzaron el viernes en una sesión volátil, con Oriente Próximo acaparando la atención tras los informes sobre posibles negociaciones de paz entre Washington y Teherán, que alimentaron el optimismo sobre una pronta resolución del conflicto.

Durante la negociación de la tarde, el rendimiento del bono del Tesoro a 10 años cayó -2,2 pb hasta alcanzar el 4,307 %. No obstante, el rendimiento a 10 años subió +5,6 pb durante la semana, su mayor ganancia semanal desde mediados de marzo.

El rendimiento del bono del Tesoro de EE. UU. a 30 años bajó -0,3 pb durante el día hasta el 4,912 %, sin variación en términos semanales.

En el extremo corto de la curva, el rendimiento del bono del Tesoro a dos años, sensible a las expectativas sobre los tipos de interés, cayó -5,5 pb hasta alcanzar el 3,791 % el viernes, aunque acumuló durante la semana un avance de +7,9 pb, su mayor incremento semanal desde el 16 de marzo.

La curva de rendimiento se aplanó durante la semana, con el diferencial entre los tramos a dos y diez años estrechándose hasta los 51,6 pb desde los 53,9 pb de la semana anterior. El movimiento responde a un aplanamiento bajista: los rendimientos a corto plazo subieron más que los de largo plazo, reflejando las expectativas del mercado de una mayor inflación en el horizonte inmediato.

El archivo de la investigación sobre Jerome Powell despeja el camino para la confirmación de Kevin Warsh como próximo presidente de la Fed. El desbloqueo llega tras la presión ejercida por el senador republicano Thom Tillis, quien instó al Departamento de Justicia a cerrar su investigación sobre el proyecto de construcción de la Fed para permitir que avanzara el proceso de confirmación del candidato de Trump.

De acuerdo con la herramienta FedWatch de CME Group, los operadores de futuros de fondos de la Fed descuentan 5,7 pb de recortes de tipos en 2026, por debajo de los 16,0 pb descontados hace una semana. Asimismo, asignan una probabilidad del 0,0 % a una subida de tipos de 25 pb en la reunión del FOMC de esta semana, inferior al 1,0 % de la semana anterior.

Los rendimientos de los bonos soberanos a corto plazo de la eurozona registraron su mayor subida semanal en más de un mes, ya que el recrudecimiento de las tensiones en el estrecho de Ormuz impulsó los precios de la energía al alza, avivando las preocupaciones inflacionarias y elevando las expectativas de una posible subida de tipos del BCE.

El rendimiento alemán a dos años, que es sensible a las expectativas de política del BCE, bajó -0,7 pb el viernes hasta el 2,551 %, aunque registró una ganancia semanal de +14,1 pb, la más fuerte desde mediados de marzo.

El rendimiento alemán a 10 años también retrocedió durante el día, cayendo -1,4 pb hasta el 2,997 %, aunque avanzó +3,3 pb durante la semana. En el extremo largo de la curva, el rendimiento a 30 años cedió -0,9 pb el viernes, acumulando una caída semanal de -1,8 pb.

El BCE tiene prevista su reunión esta semana y se espera que mantenga los tipos de interés en los niveles actuales. No obstante, los participantes del mercado anticipan que el banco central pondrá un mayor énfasis en contener la inflación, incluso si ello implica un coste para el crecimiento económico a corto plazo.

Como muestra de los retos que afrontan los responsables de política monetaria, los datos publicados el viernes indicaron que el sentimiento empresarial en Alemania cayó más de lo esperado en abril. El conflicto liderado por EE. UU. e Israel con Irán ha incrementado el pesimismo entre las empresas y amenaza la recuperación prevista de la mayor economía de Europa.

Los rendimientos de los bonos soberanos italianos a 10 años subieron +1,9 pb hasta el 3,802 %, contribuyendo a un incremento semanal de +10,8 pb. El diferencial de rendimiento entre los bonos soberanos italianos y los Bunds se amplió hasta los 80,5 pb, su nivel más alto desde el 8 de abril, el día siguiente al anuncio del alto el fuego entre EE. UU. e Irán, y 7,5 pb por encima del nivel de la semana anterior de 73,0 pb.

Nota: los datos corresponden al 24 de abril de 2026 a las 16.00 EDT

Aunque se han hecho todos los esfuerzos posibles para verificar la exactitud de esta información, EXT Ltd. (en adelante, "EXANTE") no se hace responsable de la confianza que cualquier persona pueda depositar en esta publicación o en cualquier información, opinión o conclusión contenida en ella. Las conclusiones y opiniones expresadas en esta publicación no reflejan necesariamente la opinión de EXANTE. Cualquier acción realizada sobre la base de la información contenida en esta publicación es estrictamente bajo su propio riesgo. EXANTE no se hará responsable de ninguna pérdida o daño relacionado con esta publicación.

Este artículo se presenta a modo informativo únicamente y no debe ser considerado una oferta ni solicitud de oferta para comprar ni vender inversión alguna ni los servicios relaciones a los que se pueda haber hecho referencia aquí. Operar con instrumentos financieros implica un riesgo significativo de pérdida y puede no ser adecuado para todos los inversores. Los resultados pasados no garantizan rendimientos futuros.

Regístrese para recibir perspectivas de los mercados

Regístrese

para recibir perspectivas

de los mercados

Suscríbase ahora

Artículos relacionados

¿Sigue siendo la tierra de las oportunidades?Diarias3 jul 2026

¿Sigue siendo la tierra de las oportunidades?Diarias3 jul 2026 June Equity Review - Calibrating the rotation withinRevisión mensual de renta variable2 jul 2026

June Equity Review - Calibrating the rotation withinRevisión mensual de renta variable2 jul 2026 ¿Cuál es el verdadero estado del mercado laboral estadounidense?Diarias2 jul 2026

¿Cuál es el verdadero estado del mercado laboral estadounidense?Diarias2 jul 2026 ¿Cuánta confianza genera realmente el mercado laboral?Diarias1 jul 2026

¿Cuánta confianza genera realmente el mercado laboral?Diarias1 jul 2026

Creado por profesionales. Para profesionales.