Fixed Income Briefing May 2026

Renée Friedman, Global Head of Research

Economic and US Treasury Market Review

▪ The dollar has risen more than 1% MTD in May thanks to geopolitical safe haven demand due to continuing geopolitical tensions in the Middle East and higher than expected inflation, with CPI and PPI both exceeding expectations. These factors have prompted bond markets to price out earlier expectations of Fed interest rate cuts.

▪ US economic data gave a somewhat mixed picture. According to the US Bureau for Labor Statistics, the US labour market in April 2026 showed continued resilience, with the economy adding 115,000 nonfarm payroll jobs. The national unemployment rate stands at 4.3%. Average hourly earnings rose by 3.6% y/o/y, but real average hourly earnings for all employees decreased 0.5 percent from March to April this year. Initial jobless claims are holding steady, with the four week moving average for initial jobless claims for the week ending 16 May coming in at 202,500, a decrease of 1,500 from the previous week's revised average, while the weekly initial jobless claim rate fell 3,000 to 209,000; layoffs remain low despite high-profile tech job cuts.

▪ On the growth front, business activity has held steady in May, with the S&P Global Flash US Composite PMI coming in at 51.7, unchanged from April. The Flash Services PMI came in at 50.9, edging down from April’s 51.0. However, the Flash Manufacturing PMI rose to 55.3 from April’s 54.5, a 48-month high on temporary stock building. As noted by S&P, surging input costs, which jumped in May at the steepest rate since late-2022 on the back of rising war- related supply constraints and steep energy cost increases, were not only cited as causing lower sales, but also contributed to increasing job losses and a further rise in selling price inflation to its highest since August 2022.

▪ On the consumer side, the Conference Board’s Consumer Confidence Index edged down to 93.1 in May but still came in above expectations of 92.0. April was revised higher to 93.8 from 92.8. The report noted that consumers remained increasingly concerned about prices and oil and gas for a second consecutive month, while references to geopolitical risks and their inflationary implications also stayed elevated. The Present Situation Index fell 3.2 points to 121.2 as assessments of both business conditions and the labour market softened. In contrast, the Expectations Index rose 1.0 point to 74.4, reflecting a modest improvement in views on business and labour market conditions over the next six months. However, household income expectations weakened. The labour market differential, which measures the share of consumers who say jobs are plentiful less those who say jobs are hard to get,narrowed by 0.6 points to 6.9. Consumers’ 12-month inflation expectations eased modestly in May but remained elevated, while nearly half of respondents continued to expect interest rates to be higher over the next year. The May reading of the University of Michigan confidence survey indicated that US consumer sentiment fell for the third straight month as supply disruptions in the Strait of Hormuz continue to boost gasoline prices. Sentiment is now just below the previous historical trough seen in June 2022. It fell to 44.8 from April’s 49.8. The cost of living continues to be a first-order concern, with 57% of consumers spontaneously mentioning that high prices were eroding their personal finances, up from 50% last month. Year-ahead inflation expectations edged up from 4.7% in April to 4.8% in May. This substantially exceeds the 3.4% reading seen in February 2026 prior to the start of the Iran conflict. Long-run inflation expectations climbed from 3.5% in April to 3.9% in May, notably higher than the 2.8% to 3.2% range seen in 2024.

▪ Annualised headline inflation rose to 3.8% in April 2026, up from 3.3% in March, according to the Bureau of Labor Statistics. It was +0.6% on a seasonally adjusted basis m/o/m after rising 0.6% in March. Core annualised CPI was +2.6% y/o/y and 0.2% m/o/m. However, the Fed's favoured inflation measure, the core PCE price index, was 2.8% in April, with monthly core PCE rising 0.4% in April, following a 0.3% increase in March. Energy costs surged 17.9% y/o/y, the steepest increase since September 2022. Fuel oil jumped 54.3% and gasoline rose 28.4%.

Yield swings

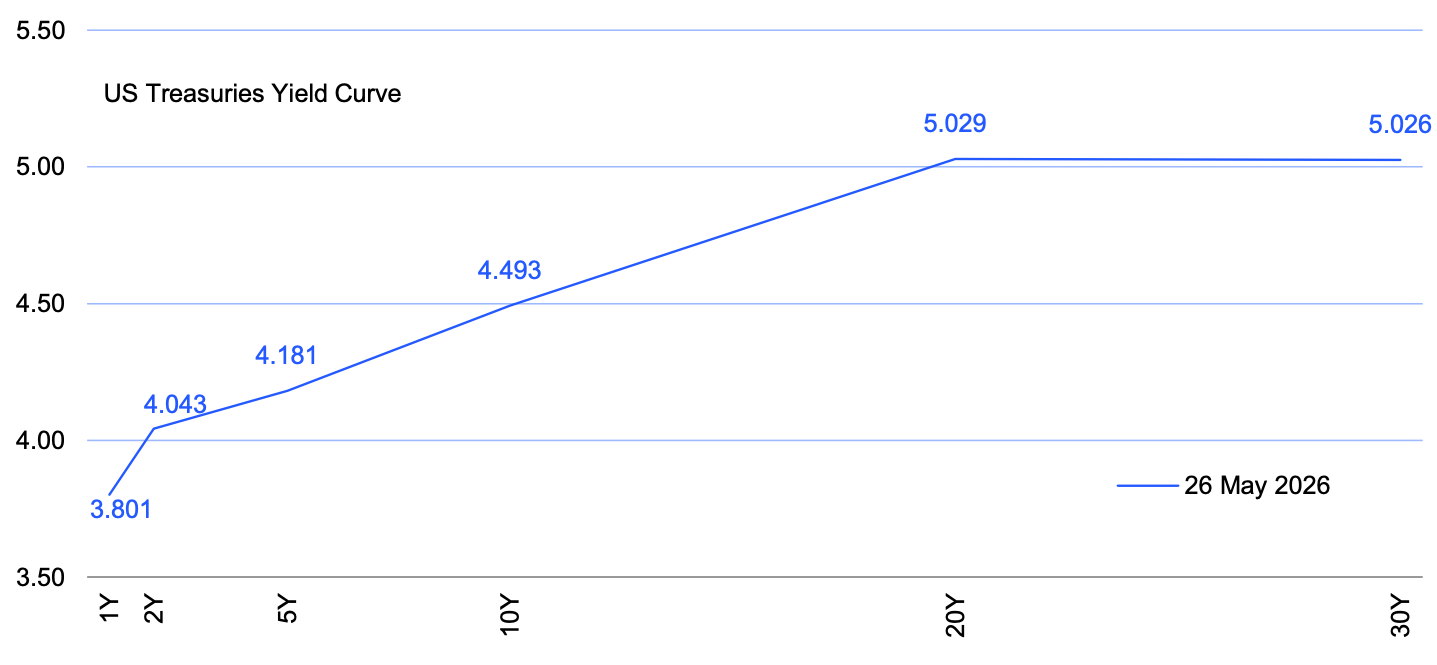

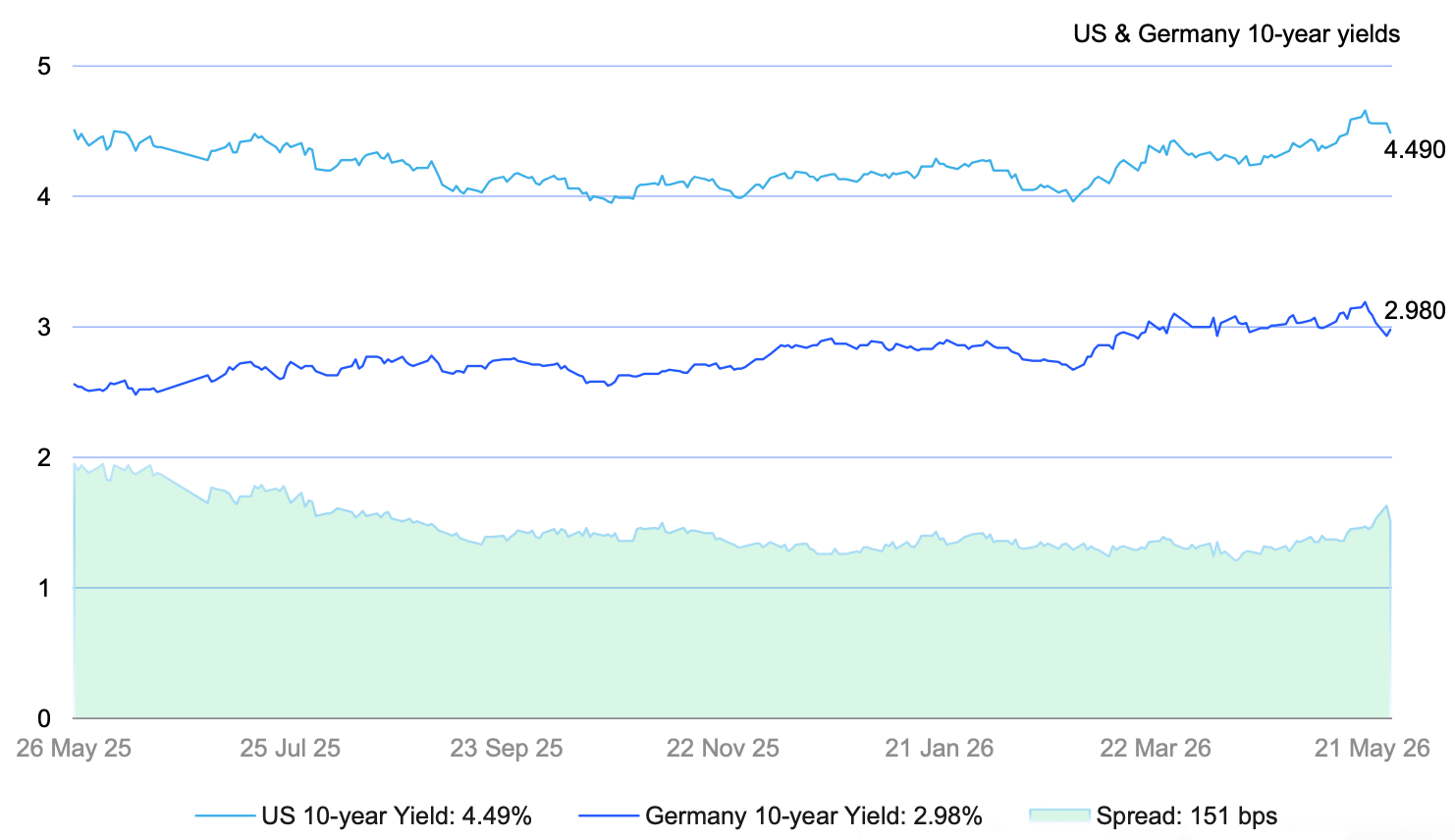

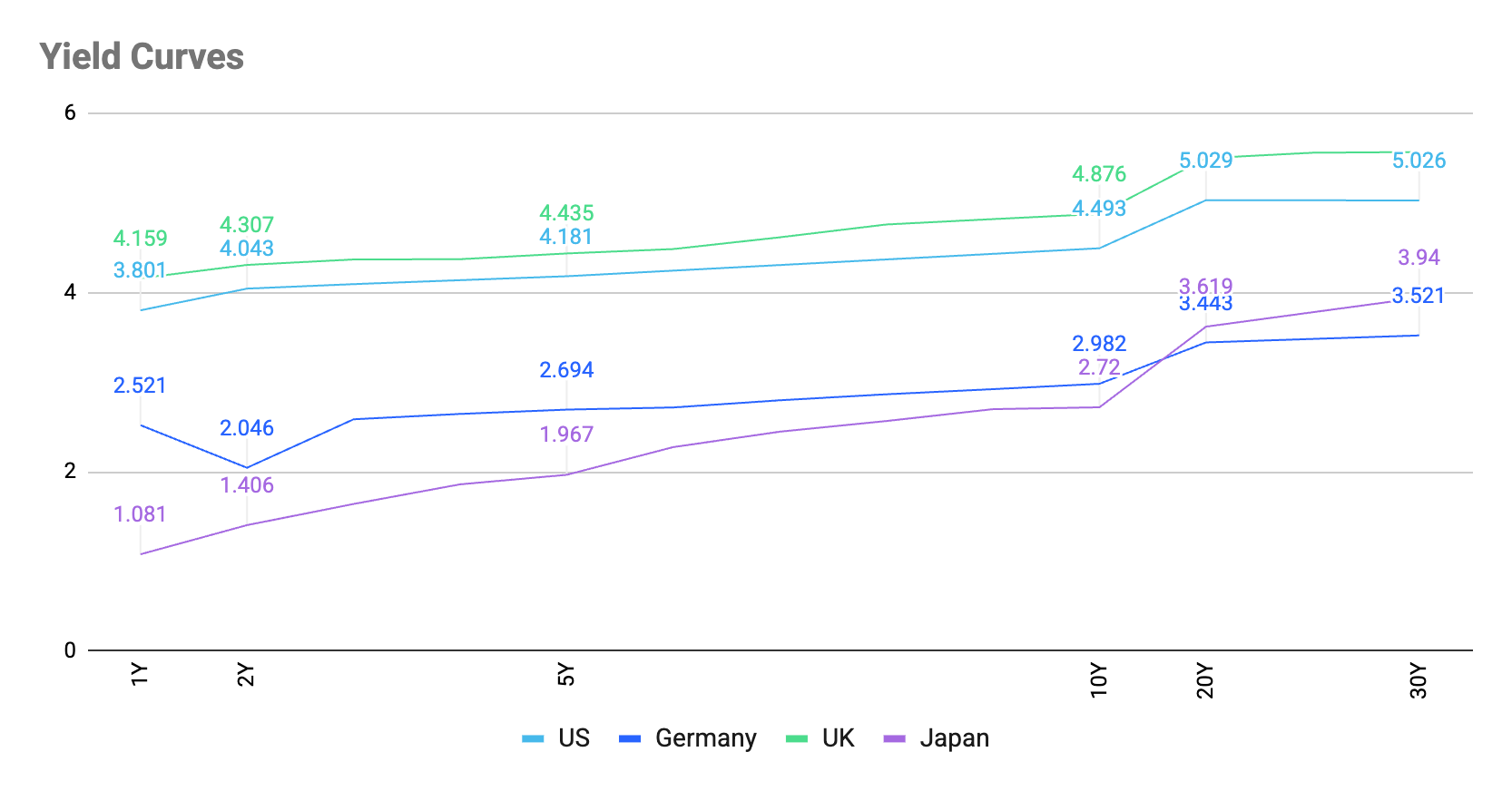

May has been a volatile month for bonds. The yield curve has steepened with yields on US Treasuries having broadly risen over May, particularly along the longer end (10-30 years), while short-term yields have remained relatively stable. In the UK, gilt yields spiked early in the month following weaker economic data, hawkish comments from the Bank of England and rising domestic political uncertainty after the Labour government suffered huge losses in local elections, putting the Prime Minister’s premiership in doubt. Short-dated yields, those in the 2-5-year range, jumped more than longer maturities, flattening the curve. It was a different situation in Germany in May. German bund yields have only risen moderately, reflecting the ECB’s expected tightening cycle, but remain lower than US and UK yields due to more stable inflation readings. The German yield curve has steepened, with longer maturities outperforming.

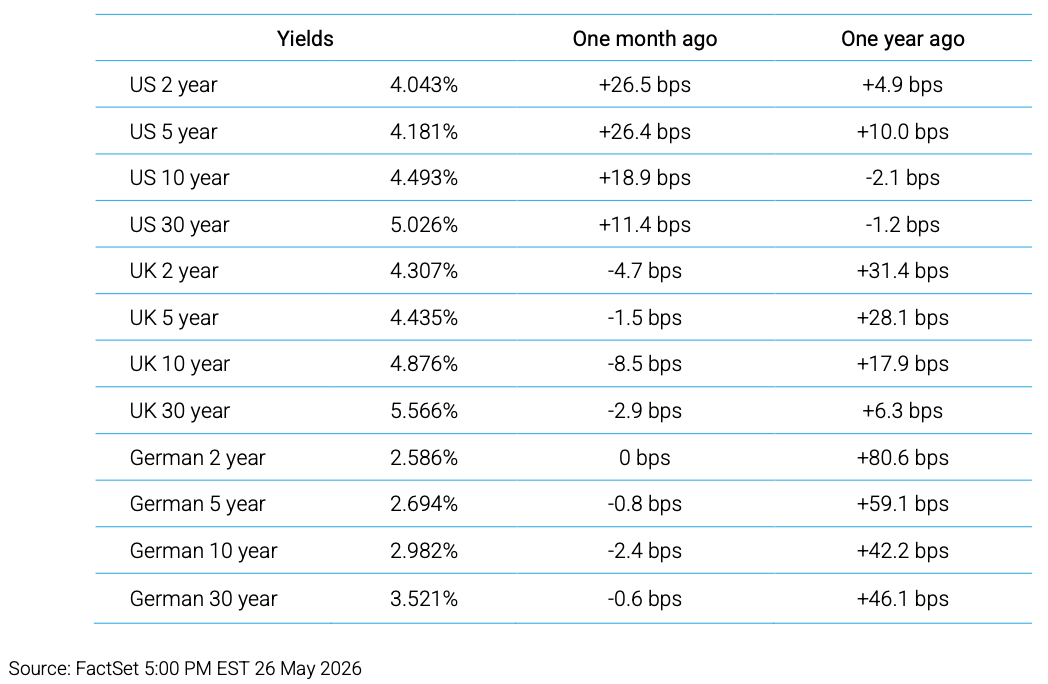

The US 10-year yield is +18.9 basis points (bps) from a month ago. The 10-year German Bund is -2.4 bps. The spread between the two has widened from 129 bps a month ago to 151 bps. On the long-end of the curve, the US 30-year yield is +11.4 bps from a month ago, while the German 30-year yield is -0.6 bps from a month ago.

Global Economic and Market Review

Eurozone headline inflation rose 3.0% in April 2026, up from 2.6% in March. This marked the highest rate since September 2023, largely driven by a sharp 10.9% surge in energy costs due to Middle East supply constraints. The S&P Eurozone Flash Composite PMI for May fell to 47.5, down from April’s 48.8 and a 31-month low. The Flash Services PMI came in at 46.4, down from April’s 47.6 and a 63-month low. The Flash Manufacturing PMI also fell, coming in at 51.4, down from April’s 52.2 and a 3- month low. The rate of input cost inflation rose for the seventh consecutive month in May, hitting a three-and-a-half year high. Steep rises were seen across both the manufacturing and services sector. Average prices charged for goods and services rose at the fastest pace in 38 months, but the pace of inflation quickened only fractionally from that seen in April.

However, European consumers are not in a complete state of despair. According to the European Commission, the flash estimate of the consumer confidence indicator showed a slight rebound in the EU, +1.7 percentage points compared with April, to - 19.0 from -20.6 in April. Nevertheless, consumer confidence remains well below its long-term average and below the level observed before the outbreak of the war with Iran.

In the first quarter of 2026, seasonally adjusted GDP increased by 0.1% in the euro area compared with the previous quarter, according to Eurostat. The seasonally adjusted GDP increased by 0.8% in the euro area on a y/o/y basis. In the fourth quarter of 2025, GDP had increased by 0.2%. In addition, the ECB’s wage tracker indicates negotiated wage growth with smoothed one-off payments of 3.2% in 2025 and 2.3% in 2026. The headline ECB wage tracker averaged 1.8% in the first quarter, 2.1% in the second quarter, and 2.6% in the third and fourth quarters.

In the UK, the economy appears to be coming under increasing strain. Business activity at UK private sector firms decreased in May, ending a 12-month period of expansion. The S&P Global Flash Composite PMI fell to 48.5, down from April’s 52.6 and a 13-month low. The Flash Services PMI fell to 47.9, a significant drop from April’s 52.7 reading and a 64-month low. The Flash Manufacturing PMI was unchanged from April’s 53.7. The May data highlighted that private sector payroll numbers fell for the twentieth successive month, largely due to a faster pace of job shedding in the service economy. Backlogs of work also decreased again, suggesting a lack of pressure on business capacity. Input price inflation had eased slightly since April, but remained well above its long-run average. According to S&P, around 66% of manufacturing companies and 51% of service providers indicated an increase in their average cost burdens during May. This was overwhelmingly linked to rising oil prices and transportation bills, alongside higher energy and raw material costs.

Headline inflation in the UK fell to its lowest in more than a year in April, surprisingly falling to 2.8% in April, down from March’s 3.3%. The drop was largely attributed to an energy price cap introduced by the energy regulator on 1 April. Core inflation was 2.5% in April 2026 and rose by 0.7% m/o/m in April 2026, accelerating from March’s 0.4% m/o/m increase. However, this is expected to be only a temporary reprieve as consumer prices are expected to increase as higher energy costs due to the Iran war continue to filter through. According to the Office for National Statistics (ONS) May 2026 release, the UK economic inactivity rate rose by 0.1 percentage points to 20.9%. The ONS reported that the headline unemployment rate sat at 4.9% for the February- April period, though for the quarter ending in March, unemployment rose slightly to 5.0%. The number of payrolled employees dropped by 100,000 in April following a 28,000 decline in March. The labour market is becoming increasingly fragile with job vacancies being the lowest since 2021.

Things to think about

The lack of a definitive resolution to the war with Iran including the potential timing of the reopening of the Strait of Hormuz continues to weigh on markets. Though stockpiles and other measures have partly prevented problems thus far, at current drawdown rates, commercial oil stocks could reach critically low levels by June. Even if there is an immediate cessation of hostilities, energy production, due to shutdowns and damage to infrastructure facilities, will take many months to repair. It will also take time to reposition and offload ships currently in the Strait as demining activities will have to take place first. The market is pricing in interest rates rises as investors consider ongoing and future geopolitical disruptions. The competition for capital will remain strong as governments in the US, UK, Europe and Japan will continue to issue debt to finance deficits, putting additional upward pressure on yields as will the growing issuance from corporate bonds related to AI investment. In the US, new Fed Chair, Kevin Warsh, and other FOMC members have signalled that the Fed is likely to maintain a cautious approach to rate hikes amid moderate economic growth but persistent inflationary pressures.

With inflation expected to rise as secondary effects from the energy surge play out and credit expected to remain tighter for longer, the eurozone is likely to focus on gradual tightening given the growth slowdown risks amid geopolitical tensions. The Fed is likely to remain on pause in June and any rate hikes will be slow as Warsh leadership of the Fed will be under intense scrutiny. The Bank of England will remain data- dependent. It may be forced to hike if inflation persists, but it will also be mindful of contraction risks. Investors are still likely to be worried by high government borrowing, rising debt levels in developed markets, particularly in the US which has been accused of weaponising the dollar.

Risk premiums should be expected to widen further as policy divergence emerges. Investors may wish to consider selective yield-spread targeting, diversifying across geographies to reduce country-specific risks in addition to potentially extending duration. However, they should also consider maintaining some allocation to short- duration bonds to preserve liquidity and reduce volatility. Additionally, they may wish to use inflation-protected securities (e.g., TIPS) to hedge inflation risk.

Key risks

▪ Inflation risks continue to rise, further undermining consumer and business confidence. The full second order impacts from the war with Iran are yet to be felt. Tariffs also remain unresolved and this could also feed through to inflation. Persistently high inflation could force aggressive rate hikes; conversely, a sudden disinflation may lead to policy easing or risk of recession.

▪ Policy uncertainty. The central banks may get the timing of rate hikes wrong or we may see a faster divergence in policy than currently considered. Fiscal stimulus changes and political pressures, especially on the Fed, may create volatility. Uncertainty over policies to deal with the “K-shaped” economy may result in uneven economic outcomes and may lead to credit risks in certain sectors or regions.

▪ Geopoliticaltensions, re-alignments and events. Conflictsorre-alignments in Europe and/or Asia over trade or other policy measures can quickly shift safe-haven demand and risk premiums. Geopolitical concerns such as the Iran war, the threat to Taiwan from mainland China, the increase in military exercises by the Chinese navy in the South China Seas, the potential takeover of Cuba by the US and continued expansion of US military and political activities in Latin America, and the ongoing war in Ukraine, have all increased risk aversion, supporting demand for Treasuries as a safe haven.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.