Can risk appetite return without policy clarity?

Key data to move markets today

EU: Eurogroup meeting and German Trade Balance

UK: A speech by BoE Deputy Governor for Financial Stability Sarah Breeden

USA: Initial and Continuing Jobless Claims, Existing Home Sales and a speech by New York Fed President John Williams

Global Macro Updates

FOMC minutes. The June FOMC minutes did not materially change the policy narrative. At the June meeting, the Fed left rates unchanged, as expected, while the Summary of Economic Projections showed that nine officials continued to anticipate rate increases this year.

The policy outlook remains divided, with officials balancing the prospect of easing inflation against the risk of renewed price pressures. Most participants saw room for inflation to moderate, which could allow rates to remain steady or eventually decline. However, some cautioned that persistent price pressures, potentially linked to AI-driven demand, the Middle East conflict or tariffs, could justify further tightening. Although a few officials favoured a June rate increase, they ultimately supported holding policy unchanged. Views on the outlook remained split, with some expecting rates to finish 2026 at or below current levels and others anticipating higher rates.

Inflation risks remain a central concern for policymakers. Fed staff raised their 2026 and 2027 inflation forecasts from the April outlook, citing the effects of the Middle East war and AI-related investment. Participants broadly continued to see upside risks to price stability.

Labour-market conditions were generally viewed as stable and balanced. Participants described unemployment as steady, with some indicating that the labour market was no longer a significant source of inflation pressure. Most expected conditions to remain steady in the near term.

Growth expectations remained broadly constructive despite a modest downward revision by Fed staff. Participants generally expected GDP growth to stay solid through year-end, supported by AI investment, consumer spending and fiscal policy.

European IPO recovery builds as UK listings lag. European IPO markets are showing signs of a sustained recovery after several subdued years, according to EY Global IPO Trends and PwC IPO Watch. Improving investor confidence and the return of companies that had previously delayed listings have helped revive activity.

However, the recovery remains uneven. IPO windows continue to depend on market volatility, geopolitical developments and valuation expectations, with many companies still waiting for more favourable conditions before launching. EY noted that preparation and flexibility remain critical, as listing opportunities can open and close quickly.

Large transactions continue to underpin global fundraising, including SpaceX’s record listing. Six of the largest global IPOs came from Europe in Q2. PwC estimates that European IPO proceeds rose 76% y/o/y to €7.2 billion in H1 2026. Investors remain selective, favouring companies with strong profitability, resilient earnings and compelling equity stories. Activity has broadened across technology, financials, consumer and real estate.

Nevertheless, UK IPO activity lags continental Europe, with takeover bids worth £59.7 billion far exceeding the £2.2 billion raised through new listings. Although the government and regulators have introduced listing reforms and broader capital markets initiatives, the key challenge remains converting a healthier pipeline into a sustained revival in public offerings. Uncertainty surrounding the UK political backdrop has also contributed to lower IPO activity.

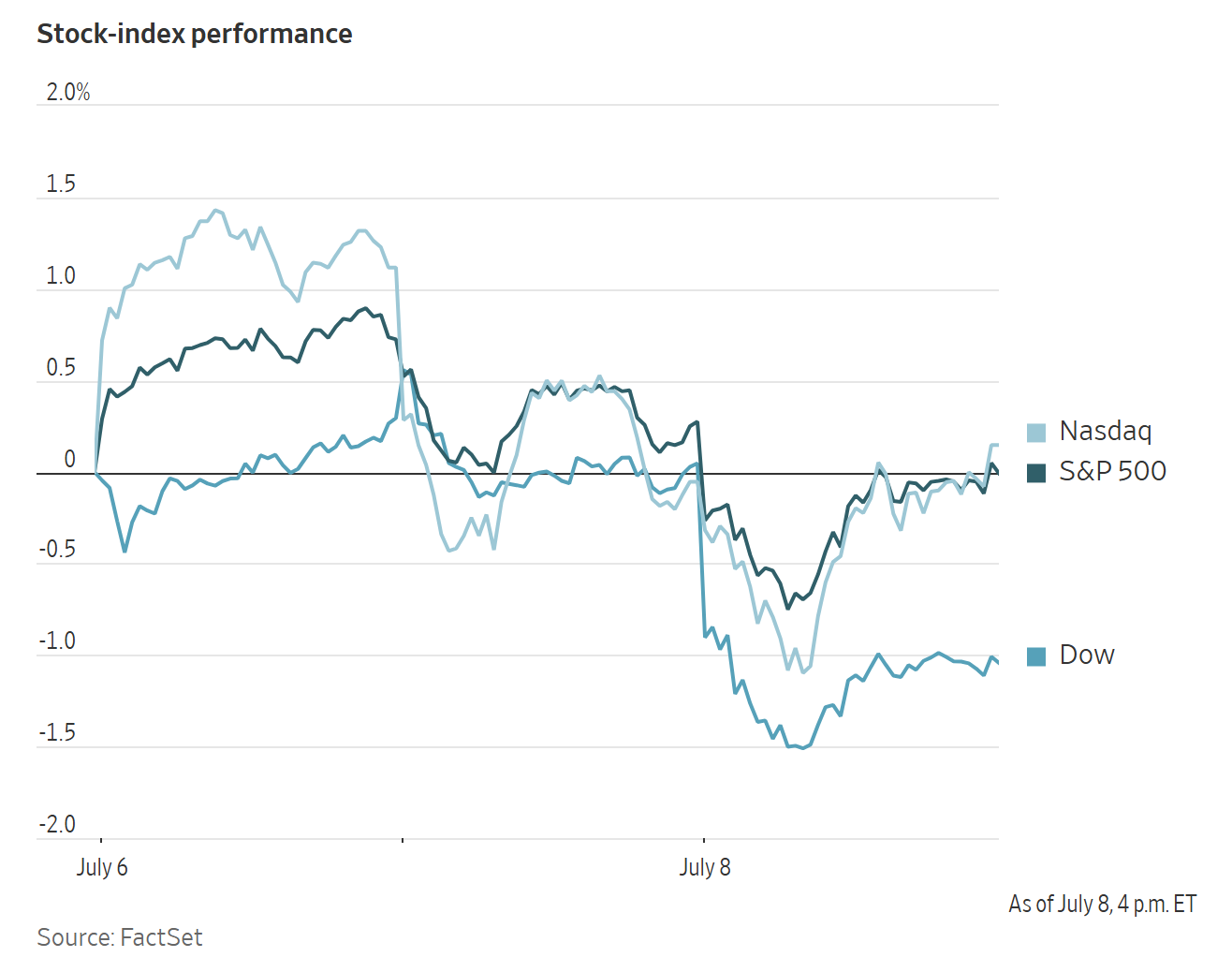

US Stock Indices

Dow Jones Industrial Average -1.09%

Nasdaq 100 +0.27%

S&P 500 -0.28%, with 9 of the 11 sectors of the S&P 500 down

US equities closed mostly lower, with the Dow Jones Industrial Average down 576.76 points, or -1.09%. The S&P 500 fell -0.28%, while the Nasdaq recovered earlier losses to finish slightly higher, up +0.20%.

In corporate news, SpaceXAI introduced a new artificial-intelligence model developed with AI coding startup Cursor. The model is designed to improve performance in finance, legal and coding tasks and provide greater competition to rivals such as Anthropic PBC and OpenAI.

China plans to permit leading AI companies to purchase a limited quantity of Nvidia’s H200 chips, according to The Information.

Apple said its expanded agreement with Broadcom is expected to exceed $30 billion. The partnership includes manufacturing more than 15 billion chips in the US and investing $1.5 billion to help upgrade Broadcom’s Fort Collins, Colorado facility for advanced radio-frequency components used in wireless chips.

Meta Platforms plans to invest about $10 billion in its first Canadian data centre. The Sturgeon County, Alberta facility will have one gigawatt of power capacity. It will rely largely on natural gas-fired power, require 3,000 construction workers and create 300 full-time jobs. Meta expects to use the computing capacity for its AI models and social media apps.

European Stock Indices

CAC 40 -2.18%

DAX -2.23%

FTSE 100 -1.66%

Commodities

Gold spot -0.72% to $4,076.32 an ounce

Silver spot -1.95% to $58.80 an ounce

West Texas Intermediate +3.65% to $74.76 a barrel

Brent crude +4.51% to $79.30 a barrel

Gold prices declined on Wednesday, with spot gold falling -0.72% to $4,076.32 per ounce after touching its lowest level since 1 July earlier in the session.

Spot silver also weakened, dropping -1.95% to $58.80 per ounce.

Crude oil prices settled higher on Wednesday after the US President said an interim agreement signed last month to end the war with Iran was ‘over’ and threatened fresh strikes against Iran following Iranian attacks on US bases in the Gulf and on tankers in the Strait of Hormuz. The president suggested that the US could reimpose a naval blockade on Iranian ports near the Strait of Hormuz.

The comments raised concerns that vessel movements through the Strait of Hormuz could, once again, become disrupted.

Brent futures rose $3.42, or +4.51%, to settle at $79.30 per barrel, their highest level since 19 June. US WTI crude gained $2.63, or +3.65%, to settle at $74.76 per barrel, the highest level since 22 June.

The US military conducted powerful overnight strikes against Iran. Iran’s Revolutionary Guards also stated that they had targeted US military sites in Bahrain and Kuwait.

The US has also revoked a temporary general licence that had authorised the sale and transaction of Iranian oil. Around 63 million barrels of Iranian oil are currently on the water, either in transit or idling, according to Bloomberg news calculations based on Vortexa data.

Reuters reported that at least four oil and gas tankers turned back after attempting to transit the Strait of Hormuz following recent vessel attacks, according to ship-tracking data.

China has reportedly lifted restrictions on refined fuel exports for the remainder of July, with refiners planning to export roughly 3 million metric tonnes of gasoline, diesel and jet fuel this month.

Separately, Reuters reported that Ukrainian drones struck three Russian oil refineries overnight, as well as Russian tankers in the Sea of Azov. Continued Ukrainian drone attacks on refineries has resulted in Russia banning diesel exports in a bid to support its domestic fuel market amid growing shortages.

In the UAE, Fujairah oil product inventories rose 27% to a three-month high in the week to 6 July, led by a 38% increase in heavy distillates, according to S&P Global. Total inventories reached 10.129 million barrels, the highest level since 6 April.

The DOE Weekly Petroleum Status Report showed a crude build of 3.0 million barrels, alongside a gasoline draw of 1.9 million barrels, a distillate draw of 5.0 million barrels and a Cushing draw of 100,000 barrels.

The EIA reported that US petroleum exports reached a record high in April, as disruptions to international crude oil and refined product flows through the Strait of Hormuz increased global demand for US exports.

Note: As of 4 pm EDT 8 July 2026

Currencies

EUR +0.09% to $1.1414

GBP +0.30% to $1.3389

Bitcoin -1.96% to $62,152.89

Ethereum -1.98% to $1,737.74

The US dollar eased on Wednesday. The dollar index ended the trading day -0.07% to 101.05. It had climbed as high as 101.27 earlier in the session, its highest level in about a week.

The euro gained +0.09% on the day to trade at $1.1414. Sterling rose +0.30% to $1.3389 after reaching a three-week high of $1.3410 earlier in the session.

The dollar strengthened +0.25% against the Japanese yen to ¥162.53. This marked a fourth consecutive daily advance as traders remained alert to the possibility of intervention by Japanese authorities.

Fixed Income

US 10-year Treasury +2.1 basis points to 4.577%

German 10-year Bund +9.6 basis points to 3.095%

UK 10-year Gilt +13.6 basis points to 4.989%

US Treasury yields rose to multi-week highs on Wednesday.

The 10-year yield reached a seven-week peak of 4.597% earlier in the session and was +2.1 bps on the day at 4.577%. The US 30-year bond yield also touched its highest level in seven weeks, and traded +2.2 bps higher on the day at 5.078%.

The two-year yield, which is most sensitive to market expectations for the Fed funds rate, climbed to a two-week high of 4.235% earlier in the session and ended +3.2 bps at 4.229%.

Wednesday’s trading also featured a strong auction of US 10-year notes, following an equally robust sale of three-year notes the previous day.

The 10-year note was awarded at 4.580%. This was below the expected rate at the bid deadline, indicating that investors did not require an additional premium to participate in the auction.

Eurozone bond yields rose sharply on Wednesday, reaching their highest levels in a month as the US - Iran ceasefire collapsed and oil prices rose. Traders increased expectations for further ECB rate hikes this year with money markets pricing in 36 bps of additional ECB tightening by year-end, up from 25 bps on Tuesday.

Germany’s two-year Schatz yield, which is most sensitive to ECB rate expectations, rose +11.9 bps to 2.714%. This is its highest level since 11 June.

Germany’s 10-year bond yield also increased to its highest level since 11 June, rising +9.6 bps to 3.095%.

Italian and French 10-year bond yields also moved higher, rising +13.3 bps and +13.4 bps, respectively.

Note: As of 4 pm EDT 8 July 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

本文提供给您仅供信息参考之用,不应被视为认购或销售此处提及任何投资或相关服务的优惠招揽或游说。金融工具交易存在重大亏损风险,未必适合所有投资者。过往表现并非未来业绩的可靠指标。

由专业人士创建。 为专业人士。