Will the US consumer be okay?

Key data to move markets today

EU: EU Financial Stability Review and a speech by ECB Chief Economist Philip Lane

UK: A speech by BoE Deputy Governor Clare Lombardelli

US: ADP Employment Change 4-week Average and speeches by Minneapolis Fed President Neel Kashkari, Dallas Fed President Lorie Logan, Chicago Fed President Austan Golsbee and Fed Governors Lisa Cook and Philip Jefferson

Global Macro Updates

Consumer confidence topped expectations in May, while regional manufacturing showed a tentative improvement. The Conference Board’s Consumer Confidence Index edged down to 93.1 in May, but still came in above expectations of 92.0. April was revised higher to 93.8 from 92.8. The report noted that consumers remained increasingly concerned about prices and oil and gas for a second consecutive month, while references to geopolitical risks and their inflationary implications also stayed elevated.

Within the details, the Present Situation Index fell 3.2 points to 121.2 as assessments of both business conditions and the labour market softened. By contrast, the Expectations Index rose 1.0 point to 74.4, reflecting a modest improvement in views on business and labour market conditions over the next six months, although household income expectations weakened.

The labour market differential, which measures the share of consumers who say jobs are plentiful less those who say jobs are hard to get, narrowed by 0.6 points to 6.9.

Consumers’ 12-month inflation expectations eased modestly in May but remained elevated, while nearly half of respondents continued to expect interest rates to be higher over the next year.

Buying intentions were mixed. Fewer consumers said they planned to purchase big-ticket items, although homebuying intentions improved slightly. At the same time, plans to spend on services weakened and roughly two-thirds of respondents said they intended to cut back on spending because of rising prices.

The Dallas Fed manufacturing index rose to 0.4 in May from -2.3 in April, returning modestly to expansion territory. The employment index also improved to 0.2 from -0.9. However, price pressures remained firm, with the raw materials prices index rising six points to 42.7, its highest level in eight months, even as the finished goods prices index fell nine points to 18.9.

US Stock Indices

Dow Jones Industrial Average -0.23%

Nasdaq 100 +1.76%

S&P 500 +0.61%, with 6 of the 11 sectors of the S&P 500 up

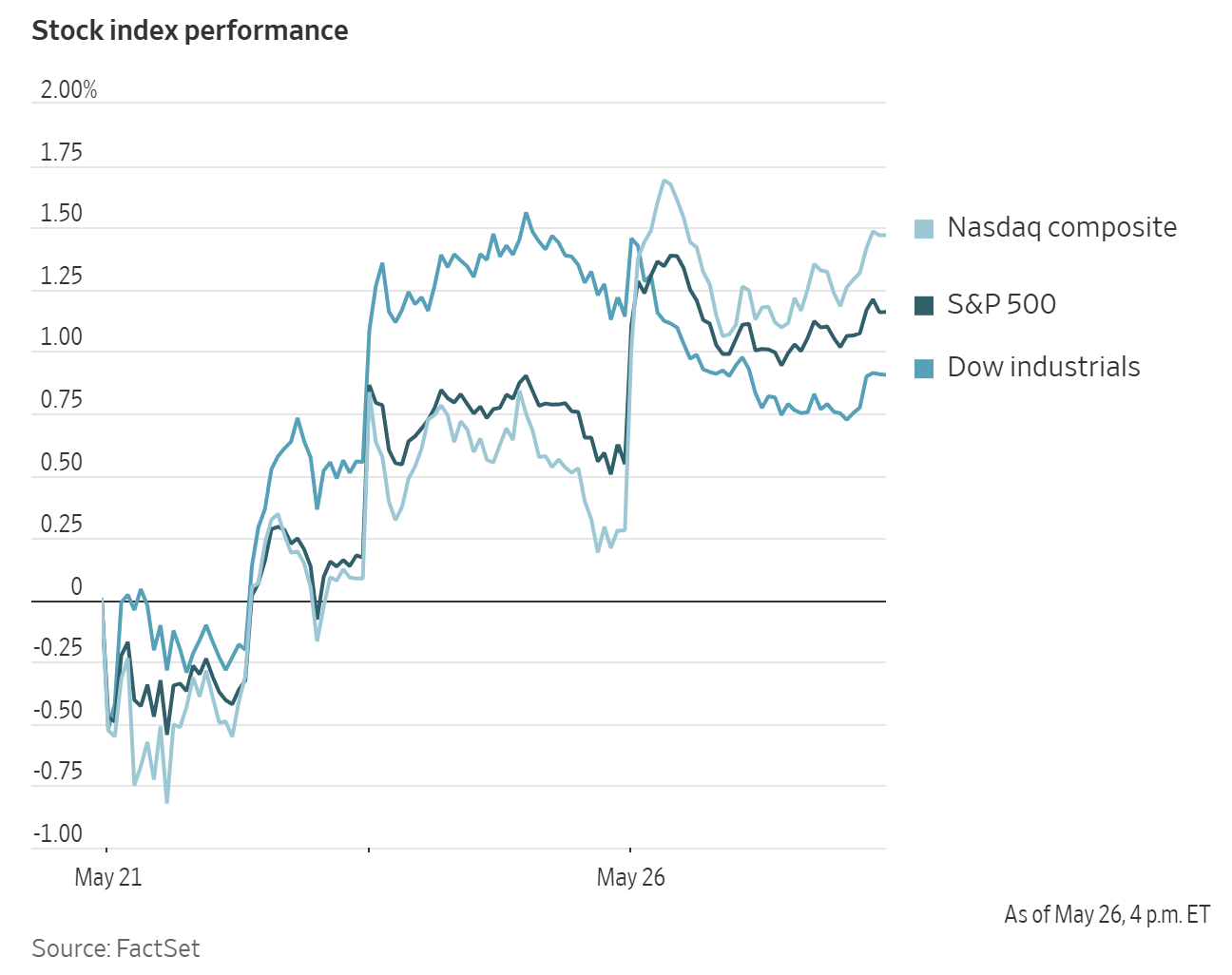

US equities advanced on Tuesday, with the Nasdaq Composite and the S&P 500 closing at record highs after the Memorial Day holiday weekend, supported by renewed strength in chipmakers and memory-related stocks.

The Nasdaq Composite was +1.19%, or 312.21 points to 26,656.18 on Tuesday. The S&P 500 was +0.61%, or 45.65 points to 7,519.12. The Dow Jones was -0.23%, or 118.02 points lower, to 50,461.68.

In corporate news, Ferrari, Europe’s most valuable automaker, unveiled its first electric vehicle on Sunday. The model, priced at $640,000 and developed in partnership with former Apple designer Jony Ive, was poorly received by investors, sending the company’s Milan-listed shares down by more than eight percent.

Eli Lilly announced agreements to acquire three vaccine developers in transactions with a combined potential value of nearly $4 billion.

Oklo, a nuclear technology company, said it had been selected by the US Department of Energy for advanced negotiations on the use of surplus plutonium as fuel for its reactors.

Qualcomm reached an agreement with TikTok owner ByteDance to supply chips for AI data centres, according to people familiar with the matter, marking an important step in the company’s effort to expand beyond smartphone processors into AI infrastructure.

BP unexpectedly dismissed Chairman Albert Manifold only months after his appointment, citing serious concerns over governance standards, oversight and conduct.

S&P 500 Best performing sector

Information Technology +1.69%, with Micron Technology +19.29%, ON Semiconductor +9.29% and Teradyne +8.56%

S&P 500 Worst performing sector

Consumer Staples -1.74%, with Kroger -4.01%, Philip Morris International -3.95% and Lamb Weston Holdings -3.75%

Mega Caps

Alphabet +1.44%, Amazon -0.39%, Apple -0.16%, Meta Platforms +0.34%, Microsoft -0.61%, Nvidia -0.22% and Tesla +1.78%

Information Technology

Best performer: Micron Technology +19.29%

Worst performer: Intuit -4.87%

Materials and Mining

Best performer: Martin Marietta Materials +4.56%

Worst performer: CF Industries -2.09%

Corporate Earnings Reports

Posted on Tuesday, 26 May from The Pulse, our real-time AI-driven news tool. Available exclusively on the EXANTE Web Platform

Zscaler reported fiscal Q3 2026 results after the close. Revenue reached $850 mn vs the $836 mn estimate while EPS was $1.08 against $1.01 expected and operating income totalled $196 mn vs $188 mn consensus. ARR stood at $3.53 bn compared with the $3.51 bn projection. The company guided Q4 revenue to $877 mn vs $879 mn expected. EPS to $1.09 against $1.04 and operating income to $207 mn compared with $205 mn. CEO stated that the firm delivered strong Q3 fiscal 2026 results with record profitability. Separately Zscaler announced the planned acquisition of Symmetry Systems to enhance its AI security and Zero Trust platform capabilities.

European Stock Indices

CAC 40 -1.03%

DAX -0.80%

FTSE 100 +0.24%

Commodities

Gold spot -1.38% to $4,507.34 an ounce

Silver spot -1.48% to $76.92 an ounce

West Texas Intermediate +3.68% to $93.62 a barrel

Brent crude +3.44% to $99.61 a barrel

Gold prices fell by more than one percent on Tuesday amid a volatile trading session.

Spot gold declined -1.38% to $4,507.34 per ounce, while spot silver fell -1.48% to $76.92 per ounce.

Oil markets also reacted sharply. Brent crude futures rose by more than three percent on Tuesday after the US military conducted strikes in Iran, undermining hopes that Washington and Tehran were close to an agreement that could end the three-month conflict and reopen shipping through the Strait of Hormuz.

Brent increased by $3.31, or +3.44%, to settle at $99.61 per barrel, while US WTI crude moved $3.32 higher, or +3.68%, to $93.62, its lowest since 22 April.

US gasoline futures fell more than six percent and US diesel declined four percent, marking their weakest close in five weeks.

US officials have repeatedly indicated that they were close to reaching an agreement with Iran to end the conflict. However, no arrangement has been secured beyond a temporary ceasefire that has reduced attacks to a minimum.

Secretary of State Marco Rubio said negotiations with Iran to extend the ceasefire and reopen the Strait of Hormuz would require several more days because of unresolved language in the draft agreement. He added that the targets struck in Iran were defensive in nature and included vessels allegedly attempting to lay mines, as well as missile launch sites.

The US strikes took place while Iran's top negotiator and foreign minister were in Doha for talks with Qatar's prime minister aimed at securing the agreement.

Reports circulated at midday that the US Navy had resumed assisting vessel crossings through the Strait of Hormuz, but US Central Command quickly denied those claims.

The UAE and Iraq are reportedly considering further expansion of pipeline export capacity in an effort to reduce reliance on the Strait of Hormuz.

Russian authorities are also reportedly considering restrictions on diesel exports. Russia has previously limited gasoline exports, which averaged around 100,000 barrels per day. Restrictions on diesel would carry greater significance for global markets given that diesel exports exceed 800,000 barrels per day.

Separately, the UK Maritime Trade Operations reported on Tuesday that a tanker had experienced an external explosion on its port side, close to the waterline, approximately 60 nautical miles off Muscat, the capital of Oman.

Pakistan, meanwhile, plans to expand domestic storage capacity for crude oil and refined products to strengthen energy security, according to a government document shared with oil producers and several leading global trading firms.

Note: As of 4 pm EDT 26 May 2026

Currencies

EUR -0.15% to $1.1624

GBP -0.46% to $1.3441

Bitcoin -1.64% to $76,027.54

Ethereum -1.83% to $2,075.90

The US dollar strengthened modestly against major currencies on Tuesday, including the euro and the yen. The dollar index rose +0.18% to 99.15, following a -0.35% decline in the previous session.

The euro declined -0.15% against the dollar to $1.1624. Sterling fell -0.46% to $1.3441.

The shift in sentiment also weighed on the Japanese yen, pushing it closer to the ¥160-per-dollar level that market participants view as a potential threshold for intervention by Tokyo.

The yen weakened -0.22% against the dollar to ¥159.29 per US dollar.

Fixed Income

US 10-year Bond -7.1 basis points to 4.492%

German 10-year Bund +3.2 basis points to 2.980%

UK 10-year gilt -3.3 basis points to 4.878%

US Treasury yields fell again on Tuesday.

The yield on the US 10-year Treasury note fell -7.1 bps to 4.492%, while the yield on the 30-year bond declined -4.7 bps to 5.021%. The two-year US Treasury yield, which closely tracks expectations for the Fed funds rate, fell -9.0 bps to 4.042%.

The US Treasury yield curve, measured by the spread between two-year and 10-year Treasury yields, stood at 45.0 bps, up 1.9 bps from the previous session.

A $69 billion auction of two-year notes reflected solid investor demand, with the bid-to-cover ratio coming in slightly above average at 2.64x.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing 16.0 bps of rate hikes in 2026, lower than the 20.8 bps priced in a week ago. Fed funds futures traders are now pricing in a 0.8% probability of a 25 bps rate hike at June’s FOMC meeting, compared to a 1.0% probability of a rate cut last week.

German 10-year bond yields moved modestly higher on Tuesday, rebounding from seven-week lows.

Germany's 10-year Bund yield rose +3.2 bps to 2.980%, after falling 9.5 bps on Monday to 2.948%, its lowest level since 8 April.

The 30-year yield increased +2.2 bps to 3.518%, after touching 3.484% on Monday, its lowest level since 9 April. At the front end of the curve, the two-year Schatz yield, sensitive to monetary policy expectations, rose +3.6 bps to 2.592%. It had fallen -9.1 bps on Monday to 2.556%, its lowest level since 7 May.

Money markets are pricing in roughly a 90% probability of an ECB rate increase at the June meeting, with 57 bps of tightening priced in by year-end, implying at least two quarter-point hikes.

June ECB hike looks increasingly likely, but the path beyond remains open. ECB Executive Board Member Isabel Schnabel delivered one of the clearest signals yet that a rate increase at the 11 June meeting is highly likely. As reported by Bloomberg news, she argued that a hike would be warranted even if a US-Iran peace agreement were reached before then, on the grounds that the energy shock has already caused lasting damage to infrastructure and supply chains that monetary policy cannot ignore.

She also pointed to early signs that second-round effects may be feeding into broader consumption. That assessment contrasts with the view of Banque de France Governor François Villeroy de Galhau, who has said such spillovers have not yet become evident, while stressing that the ECB remains extremely vigilant.

The case for a June move has also been reinforced by other policymakers and recent data. ECB President Christine Lagarde has confirmed that the March inflation forecast of 2.6% will be revised higher. Austria’s central bank Governor Martin Kocher has said that holding rates unchanged through year-end would be difficult if price developments fail to improve, even while maintaining that decisions will be taken meeting by meeting. Central Bank of Malta Governor Alexander Demarco has likewise indicated that June is the more natural horizon for judgment. Energy inflation is already running at 11.9% y/o/y, while the May flash PMI pointed to the strongest input-cost inflation in three and a half years, even as business activity contracted sharply.

The more difficult question is what follows after June. Financial markets are pricing in three 25 bps rate increases over the next year, yet some ECB sources suggest that policymakers may choose to pause in July and wait for updated projections in September. Even Schnabel has stopped short of committing to a path beyond the next meeting. Meanwhile, Villeroy de Galhau has noted that negotiated wage growth eased to 2.5% in Q1, giving more dovish policymakers grounds to argue that second-round effects remain contained for now. Taken together, the debate suggests that while a June hike is increasingly well supported, the pace of any further tightening will remain data-dependent rather than pre-committed.

Note: As of 4 pm EDT 26 May 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

本文提供給您僅供資訊參考之用,不應被視為認購或銷售此處提及任何投資或相關服務的優惠招攬或遊說。金融商品交易涉及重大損失風險,可能不適合所有投資者。過往績效不代表未來表現。

由專業人士建立。為專業人士打造。