Corporate Earning Calendar 6 March - 12 March 2025

Thursday: JD.com, Broadcom, Costco Wholesale, Hewlett Packard Enterprise, Kroger

Monday: Oracle

Tuesday: Dick’s Sporting Goods

Wednesday: Adobe, UiPath, Analog Devices, Crown Castle, Williams-Sonoma

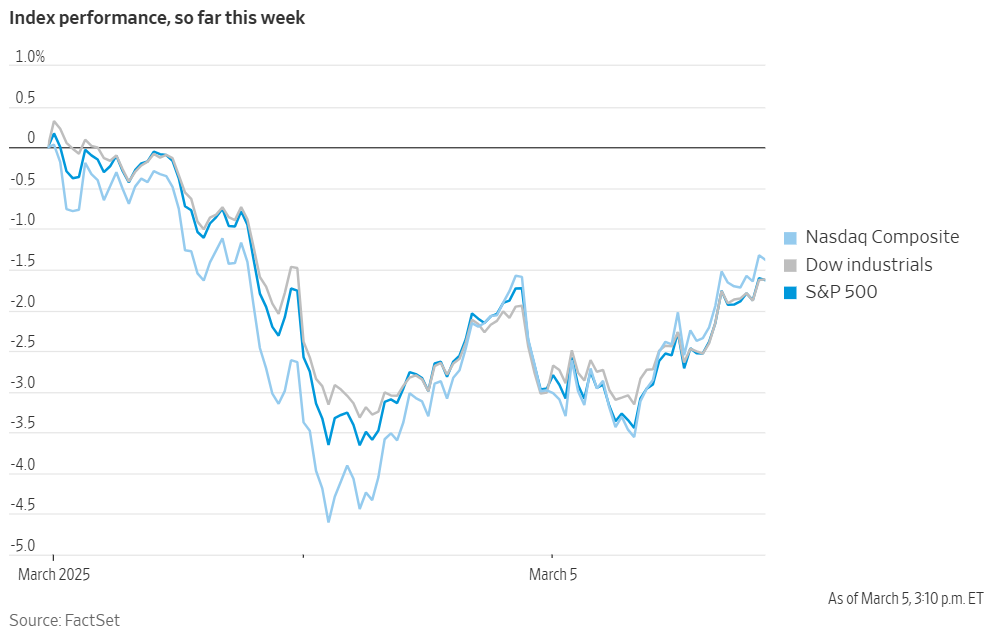

Global market indices

US Stock Indices Price Performance

Nasdaq 100 -1.23% MTD and -1.83% YTD

Dow Jones Industrial Average -1.90% MTD and +1.09% YTD

NYSE -1.37% MTD and +3.44% YTD

S&P 500 -1.88% MTD and -0.66% YTD

The S&P 500 is -0.89% over the past week, with 9 of the 11 sectors down MTD. The Equally Weighted version of the S&P 500 is -1.59% this week. Its performance is -1.77% MTD and +0.79% YTD.

The S&P 500 Real Estate sector is the leading sector so far this month, up +0.56% MTD and +6.50% YTD, while Energy is the weakest at -5.79% MTD and -0.75% YTD.

This week, Real Estate outperformed within the S&P 500 at +1.77%, followed by Health Care and Consumer Staples at +1.24% and +0.58%, respectively. Conversely, Information Technology underperformed at -4.27%, followed by Energy and Utilities, at -3.89% and -3.02%, respectively.

On Wednesday US equities experienced a late-session surge, concluding another volatile trading day for global markets characterised by significant fluctuations in European bonds and equities. Geopolitical developments remained a central driver of market sentiment, notably the White House's decision to postpone the implementation of auto tariffs on Canada and Mexico.

All three major US equity indices registered gains, with the S&P 500 +1.1%, the Nasdaq 100 +1.4%, and the Dow Jones Industrial Average +1.1%.

Market volatility persists, and traders anticipate continued fluctuations as they assess the latest developments in trade policy and await the release of the US nonfarm payrolls report on Friday. Options trading activity suggests a move of 1.3% in either direction for the S&P 500, which would represent the most significant movement on a jobs day since the regional bank turmoil in March 2023.

In corporate news, Novo Nordisk is emulating its competitor, Eli Lilly & Co, by offering its highly successful weight-loss medication, Wegovy, directly to US patients at a discounted price.

Microsoft’s $13 billion investment in OpenAI received approval from the UK's antitrust authority, resolving months of uncertainty surrounding the transaction.

Abercrombie & Fitch is facing challenges in meeting elevated investor expectations. The retailer projected revenue growth of 3% to 5% for the current year, falling short of the average Wall Street estimate of $5.2 billion in annual sales, which would represent growth of approximately 5.5%.

Phillips 66 is actively opposing activist investor Elliott Investment Management, as outlined in a letter to shareholders issued on Wednesday, as reported by Bloomberg news.

Mega caps: The Magnificent Seven had a mostly negative performance this week with Microsoft +0.32%, and Alphabet +0.17%, while Apple -1.92%, Meta Platforms -2.56%, Amazon -2.79%, Tesla -4.02%, and Nvidia -10.65%.

Energy stocks had a negative performance this week, with the Energy sector itself -3.89% due to expectations of subdued demand amidst trade policy uncertainty and potential relief of sanctions on Russian supply. WTI and Brent prices fell this week by -3.02% and -4.74%, respectively. Over the week Baker Hughes -2.73%, Chevron -2.79%, Hess -2.84%, ExxonMobil -3.67%, Shell -4.48%, Phillips 66 -4.54%, BP -5.27%, Energy Fuels -6.14%, Occidental Petroleum -6.26%, Halliburton -6.67%, ConocoPhillips -7.54%, Marathon Petroleum -7.64%, and Apa -15.77%.

Materials and Mining stocks had a mixed performance this week, with the Materials sector -0.74%. Sibanye Stillwater +3.75%, Newmont Corporation +0.62%, and Freeport-McMoRan +0.55%, while Nucor -1.55%, CF Industries -1.89%, Yara International -2.94%, Albemarle -4.28%, and Mosaic -4.32%.

European Stock Indices Price Performance

Stoxx 600 -0.20% MTD and +9.55% YTD

DAX +2.35% MTD and +15.93% YTD

CAC 40 +0.77% MTD and +10.74% YTD

IBEX 35 -1.00% MTD and +13.96% YTD

FTSE MIB -2.38% MTD and +10.38% YTD

FTSE 100 -0.61% MTD and +7.13% YTD

This week, the pan-European Stoxx Europe 600 index was -0.64%. It was +0.91% on Wednesday, closing at 556.09.

So far this month in the STOXX Europe 600, Construction and Materials is the leading sector, +3.32% MTD and +12.68% YTD, while Oil & Gas is the weakest at -4.39% MTD and +2.33% YTD.

This week, Construction and Materials outperformed within the STOXX Europe 600 with a +3.29% gain, followed by Industrial Goods & Services and Banks at +2.42% and +1.14%, respectively. Conversely, Autos & Parts underperformed at -6.07%, followed by Oil & Gas and Retail, at -4.49% and -4.43%, respectively.

Germany's DAX index was +3.38% on Wednesday, closing at 23,081.03. It was +1.26% for the week. France's CAC 40 index was +1.56% on Wednesday, closing at 8,173.75. It was +0.37% for the week.

The UK's FTSE 100 index was +0.28% this week to 8,755.84. It was -0.04% on Wednesday.

Within the Stoxx Europe 600, the Construction & Materials sector exhibited a leading performance, propelled by the agreement among German political parties to establish a €500 billion infrastructure fund. In corporate news, Best Buy's British division announced that CEO Quinn will retire later this year, with Philip Hoare slated to assume the role in September. The Banking sector also outperformed, benefiting from the strengthened European and German defence and infrastructure initiatives, which contributed to rising bond yields.

The Industrial Goods & Services sector experienced gains, particularly within the aerospace and defence segments, as analysts suggested that Germany's defence spending commitments had raised expectations for other European nations. The Basic Resources sector also saw an increase, driven by new stimulus measures in China and Germany's significant debt changes.

In contrast, the Real Estate sector lagged, primarily due to rising bond yields, despite forecasts from UK building suppliers indicating a sales recovery contingent upon a housing market rebound in 2025. The Utilities sector also underperformed due to its diminished attractiveness in a rising bond yield environment, notwithstanding the sector's dividend yields.

Other Global Stock Indices Price Performance

MSCI World Index -0.73% MTD and +1.88% YTD

Hang Seng +5.54% MTD and +20.70% YTD

This week, the Hang Seng Index was +1.75%, while the MSCI World Index was -1.14%.

Currencies

EUR +4.01% MTD and +4.18% YTD to $1.0791.

GBP +2.50% MTD and +2.96% YTD to $1.2891.

The euro was +2.90% against the USD over the past week, while the British pound was +1.71% against the dollar. The Dollar Index is -2.07% so far this week and -3.79% YTD.

The euro was up against the US dollar on Wednesday, reaching a four-month high, driven by improved growth prospects within the eurozone. It followed the announcement of Germany's proposed €500 billion infrastructure fund, which may mitigate the adverse effects of prevailing global trade tensions. The euro is +2.90% over the past week, positioning it for its strongest performance since November 2022. Against the dollar, it reached its highest level since 8th November, ultimately settling at $1.0791 on Wednesday, a +1.61% increase and marking its most significant daily advance since November 2023. The euro also strengthened against the British pound, the Japanese yen, and the Swiss franc.

The US dollar fell against a majority of major currencies on Wednesday. There are growing concerns around the US economic outlook fueled by anxieties surrounding the potential impact of tariffs on inflation and overall economic stability. Market participants are increasingly factoring in the possibility of a US economic contraction.

The dollar index was-1.19% to 104.27 on Wednesday, reaching its lowest point since 8th November. This is primarily due to tariff uncertainty.

On Tuesday, during the State of the Union address, President Trump reiterated intentions to implement reciprocal tariffs, effective from 2nd April. This followed the implementation of 25% tariffs on imports from Mexico and Canada, alongside the doubling of duties on Chinese goods to 20%. In response, Canada and China promptly implemented retaliatory measures, and the Mexican President pledged to announce countermeasures in a public address on Sunday.

However, on Wednesday, the White House revised certain aspects of its tariff announcements. The administration declared a one-month exemption for automakers from the 25% tariffs on Canadian and Mexican imports, contingent upon compliance with the terms of the USMCA.

The British pound appreciated against the dollar on Wednesday, reaching a four-month high of $1.2899 and ending the day at $1.2891, a +0.81% increase.

The euro rose +0.40% against the pound to 83.35 pence, its highest in a week, marking its third consecutive day of gains. Sterling's fluctuations were influenced by interest rate differentials and increased British government borrowing costs.

Traders are awaiting testimony from BoE Governor Andrew Bailey and other senior bank officials before lawmakers at 14:30 GMT. They will address the February interest rate reduction decision. Interest rate futures currently reflect expectations of two additional quarter-point rate cuts by the BoE this year, with expectations of a third cut diminishing.

Against the Japanese yen, the dollar depreciated by -0.62% to ¥148.81.

Note: As of 5:00 pm EST 5 March 2025

Cryptocurrencies

Bitcoin +8.68% MTD and -1.65% YTD to $90,475.56.

Ethereum +2.29% MTD and -31.46% YTD to $2,238.20.

Bitcoin is +9.40% and Ethereum -1.70% over the past week. On Wednesday Bitcoin was +3.41% and Ethereum +3.25%. This jump in Bitcoin prices this week follows US President Trump’s announcement on Sunday on his Truth Social platform that a US strategic reserve of digital assets would include Bitcoin and Ethereum as “the heart of the reserve”, adding that it would also include Solana, XRP and Cardano. President Trump is set to announce the creation of a US strategic Bitcoin reserve at the White House crypto summit on Friday, according to Commerce Secretary Howard Lutnick. As noted by Yahoo Finance, the attendees are expected to include Coinbase Global (COIN) CEO Brian Armstrong, Strategy’s (MSTR) Michael Saylor, Chainlink Labs CEO Sergey Nazarov, and Exodus CEO JP Richardson. They will be joined by several key members of Trump’s administration, including AI and crypto czar David Sacks and Bo Hines, executive director of a presidential working group on digital assets.

It is not only the potential crypto reserve that is pushing the crypto market higher. As noted by the Financial Times, there are growing expectations by State Street, the world’s largest ETF servicer by assets, that institutional investors will flock to crypto ETFs. According to a State Street report, crypto ETFs AUM will be higher than precious metal ETFs in North America by the end 2025, making them the third-largest asset class in the ETF industry. Spot crypto products will expand to cover the top 10 coins based on market cap. Other large institutional holders of crypto ETFs include BlackRock, which last week said it was including Bitcoin in some of its model portfolios through its $58bn iShares Bitcoin Trust ETF.

Note: As of 5:00 pm EST 5 March 2025

Fixed Income

US 10-year yield +6.1 bps MTD and -29.5 bps YTD to 4.281%.

German 10-year yield +38.0 bps MTD and +42.2 bps YTD to 2.791%.

UK 10-year yield bps +16.3 MTD and +8.0 bps YTD to 4.648%.

US Treasury 10-year bond yields are +2.8 bps over the past week. US Treasury yields demonstrated an upward trend on Wednesday, recovering from earlier declines, as market participants evaluated a combination of economic indicators amidst ongoing uncertainty regarding the US President's tariff policies.

Yields initially decreased on Wednesday following the release of the ADP National Employment Report, which indicated a private payroll increase of only 77,000 jobs in February. This was significantly short of the anticipated 140,000. There was also an upward revision to January's figures which were adjusted to 186,000. However, yields subsequently reversed course after the Institute for Supply Management (ISM) reported that its nonmanufacturing purchasing managers index (PMI) increased to 53.5 in the previous month, surpassing the forecast of 52.6 and January's reading of 52.8. A reading above 50 signifies economic expansion.

The Fed's Beige Book reported that economic activity has exhibited a slight but uneven increase since mid-January. Employment experienced a marginal rise, and prices increased moderately. Business and household entities expressed ongoing optimism, albeit tempered by growing uncertainty regarding the potential impact of US government policies on future growth, labour demand, and price levels.

The yield on the US 10-year Treasury note ended the trading session on Wednesday +3.3 bps to 4.281%, having reached a peak of 4.284%, its highest level since February 27th. This movement positioned the 10-year yield for its most significant single-day increase since February 18th.

On the short end of the curve, the yield on the 2-year Treasury note was -17.7 bps this week to 4.013%. It rose +0.8 bps on Wednesday. On the longer end of the curve, the 30-year yield declined -10.8 bps on the week and settled at 4.575%, after rising by +3.6 bps on Wednesday.

Recent economic data has fueled concerns regarding a potential economic slowdown, leading to increased market expectations for both the timing and magnitude of interest rate reductions by the Federal Reserve this year. Consequently, yields have experienced downward pressure in recent weeks.

Expectations for a Fed rate reduction at its early-May meeting briefly exceeded 50% on Tuesday and settled at 43.4%, an increase from approximately 28% a week prior, as indicated by CME Group's FedWatch Tool. Traders are currently pricing in 69 bps of cuts by the Fed this year, up from previous projections of less than 50 bps, according to data provided by LSEG.

On Wednesday European bond markets were shocked by the incredible surge in the German 10-year yield, +29.7 bps to reach 2.791%, the highest level since mid-March 2020 and its biggest one day jump since March 1990. Germany's two-year bond yield, which is particularly sensitive to anticipated ECB rate expectations, was +21.9 bps at 2.238%, its biggest daily jump since March 2023, and on the longer end of the curve, the Germany's 30-year yield was up +23.1 bps to 3.072% in its biggest daily jump since October 1997.

German long-dated bonds experienced a significant sell-off, the euro surged to a near four-month high, and equity markets rebounded on Wednesday, following the announcement that parties engaged in German government formation talks had reached an agreement to relax fiscal regulations.

The involved German political parties aim to facilitate increased defence and federal state expenditures, as well as establish a €500 billion special fund dedicated to infrastructure development.

Friedrich Merz's conservative party and the Social Democrats (SPD) are scheduled to present their proposals to parliament in the coming week. The Green party, led by parliamentary co-leader Katharina Droege, indicated its intention to engage in rigorous negotiations before potentially endorsing the debt reforms proposed by the conservatives and Social Democrats.

According to LSEG's IFR, Germany was set to issue 5 billion euros in new 30-year bonds on Wednesday.

Money markets subsequently adjusted their expectations of ECB rate cuts, with the projected deposit rate for December shifting to 2.02% from 1.92% on Tuesday.

European Commission President Ursula von der Leyen announced on Tuesday that the EU would activate the escape clause of the Stability and Growth Pact, thereby removing limitations on defence spending. Furthermore, these measures are anticipated to provide future governments with expanded fiscal flexibility beyond military and investment allocations in forthcoming budgets.

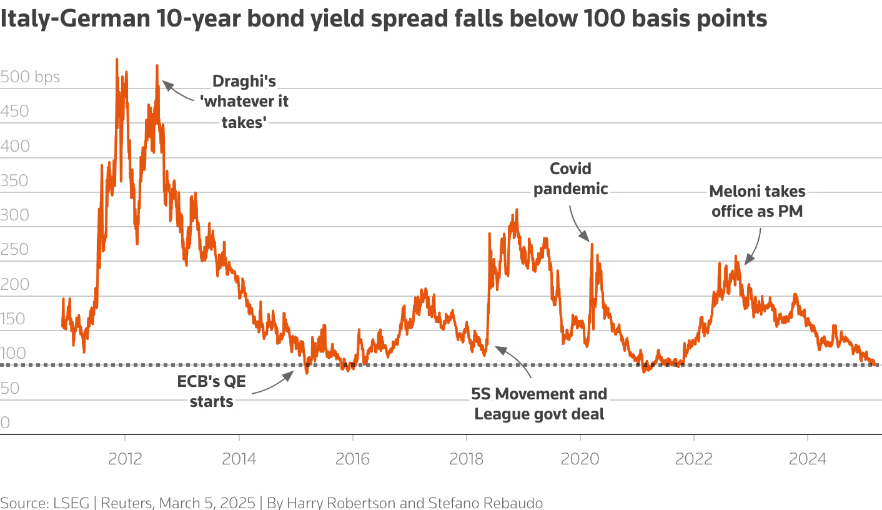

The spread between the risk-free 10-year overnight index swap (OIS) and Bund yields decreased to -23 basis points, reaching its lowest level since August 2010.

Joint European Union borrowing for new investments is deemed crucial to support government bonds in highly indebted member states, such as Italy and France.

The spread between US 10-year Treasuries and German Bunds is now 149.0 bps, 32.3 bps lower than last week.

Italian bond yields, a benchmark for the eurozone periphery, were +14.4 bps this week to 3.916%. Consequently, the yield spread between Italian and German debt remained relatively stable at 112.5 bps after dropping below 100 bps for the first time since 2021 early in the session. Italy's 10-year bond yield was +29.0 bps on Wednesday. The spread between French and German 10-year bond yields declined by 2.3 bps this week, reaching 65.7 bps.

The UK 10-year yield was +14.4 bps over the past 7 days, on Wednesday 10-year British gilt yields reached an intraday peak of 4.708%, their highest level since 16th January, before subsequently receding to 4.648%, representing an overall increase of +14.7 basis points.

Interest rate futures indicated market expectations of approximately 54 bps of reductions to the BoE's Bank Rate by December. This figure represents a decrease from the 61 bps priced in on Tuesday, which had reflected market expectations of slightly more than two quarter-point rate cuts.

Commodities

Gold spot +2.09% MTD and +10.88% YTD to $2,918.24 per ounce.

Silver spot +5.38% MTD and +13.50% YTD to $32.68 per ounce.

West Texas Intermediate crude -4.62% MTD and -5.81% YTD to $66.72 a barrel.

Brent crude -5.09% MTD and -6.56% YTD to $69.36 a barrel.

Gold prices are +0.08% this week. Despite a weakening US dollar, gold prices exhibited minimal fluctuation on Wednesday, as persistent anxieties surrounding trade tensions maintained prices above $2,900 per ounce.

Spot gold experienced a marginal increase of 0.02%, reaching $2,918.24 per ounce. Concurrently, US gold futures settled 0.20% higher at $2,926.

The bullion market displayed relative stability throughout the trading session, notwithstanding a -1.19% decline in the US dollar to a four-month low.

The upward trajectory of gold prices, driven by concerns regarding the US President's tariff policies, has resulted in eleven record highs this year. Gold peaked at $2,956.15 on 24th February, culminating in a YTD gain of +10.88%.

This week, WTI and Brent are -3.02% and -4.74%, respectively.

Oil prices ended Wednesday's trading session with a fourth consecutive decline, influenced by a larger-than-anticipated increase in US crude oil inventories. This development compounded existing market anxieties regarding OPEC+ plans to augment production in April as well as the imposition of US tariffs on Canada, China, and Mexico.

Brent crude futures settled at $69.36 per barrel, representing a decrease of $1.77, or -2.49%. US WTI crude settled at $66.72 per barrel, down $1.14, or -1.68%.

Prices experienced a partial recovery after reaching multi-year lows earlier in the session. Brent crude fell to $68.33, its lowest level since December 2021, while US crude futures touched $65.22, the lowest point since May 2023. This modest rebound followed comments from US Commerce Department Chief Howard Lutnick, who indicated on Bloomberg TV that the US would retain final decision-making authority regarding tariff relief for specific industries.

The increase in US crude oil stockpiles, attributed to seasonal refinery maintenance, exerted downward pressure on prices. Conversely, gasoline and distillate inventories declined due to increased export activity, as reported by the Energy Information Administration. Brent crude prices registered a decline of over $2 following the release of this data.

The implementation of tariffs by the US on China and Canada triggered immediate retaliatory measures from these nations, heightening concerns about a potential slowdown in global economic growth and its subsequent impact on energy demand.

OPEC+'s decision on Monday to increase production for the first time since 2022 further contributed to downward pressure on crude oil prices. The group will implement a modest increase of 138,000 barrels per day from April, representing the initial phase of planned monthly increases aimed at reversing its nearly 6 million barrels per day of production cuts, equivalent to approximately 6% of global demand.

Furthermore, the White House announced on Tuesday the termination of a licencse granted to US oil producer Chevron in 2022, authorizing its operations in Venezuela and the export of its oil. This decision places approximately 200,000 barrels per day of supply at risk.

EIA report: impact of seasonal maintenance on US oil inventories. Data released by the EIA on Wednesday revealed that US crude oil inventories were higher than expected in the preceding week. Concurrently, gasoline and distillate inventories declined, attributed to heightened product export activity amid ongoing refinery spring maintenance.

Crude oil inventories rose by 3.6 million barrels, reaching a total of 433.8 million barrels during the week ending 28th February, according to the EIA's report.

Refinery crude runs decreased by 346,000 barrels per day (bpd), and utiliszation rates fell by 0.6 percentage points, settling at 85.9% of total capacity. Utiliszation rates have remained relatively stable around 85% since mid-January, reflecting typical seasonal maintenance activities.

Refinery utilisation rates on the East Coast experienced a significant decline, reaching their lowest level since July 2020. Rates plummeted to 54.8% of capacity, down from 82.5% in the previous week.

Gasoline inventories decreased by 1.4 million barrels, totaling 246.8 million barrels for the week. However, gasoline inventories in the Midwest region increased to 60.4 million barrels, marking the highest level since February 2024.

Distillate stockpiles, encompassing diesel and heating oil, declined by 1.3 million barrels, reaching 119.2 million barrels for the week.

US product exports exhibited a substantial increase, rising to just over 7 million bpd from 5.4 million bpd in the preceding week, as indicated by the EIA data.

Crude oil inventories at the Cushing, Oklahoma, delivery hub increased by 1.1 million barrels during the week, as reported by the EIA.

Net US crude oil imports decreased by 54,000 bpd in the preceding week, according to the EIA.

Note: As of 5:00 pm EST 5 March 2025

Key data to move markets

EUROPE

Thursday: ECB Rate on Deposit Facility, ECB Press Conference, ECB Monetary Policy Statement, Retail Sales, and a speech by ECB’s President Christine Lagarde.

Friday: German Factory Orders, Eurozone Employment Change and GDP, and speeches by Bundesbank President Joachim Nagel and ECB’s President Christine Lagarde.

Monday: German Industrial Production, Trade Balance, and Eurozone Sentix Investor Confidence.

Tuesday: Eurogroup Meeting.

UK

Friday: A speech by BoE Monetary Policy Committee Member Catherine L. Mann.

Monday: Retail Sales.

US

Thursday: Initial and Continuing Jobless Claims, Nonfarm Productivity, Unit Labor Costs, Philadelphia Fed Manufacturing Survey, and speeches by Richmond Fed President Thomas Barkin, Atlanta Fed President Raphael Bostic, and Fed Governor Christopher J. Waller.

Friday: Nonfarm Payrolls, Unemployment Rate, Average Hourly Earnings, U6 Unemployment Rate, and speeches by Fed Governor Adriana Kugler, Fed Governor Michelle Bowman, New York Fed President John Williams, and Fed Chairman Jerome Powell.

Tuesday: JOLTS Job Openings.

Wednesday: CPI, Core CPI, and a speech by St. Louis Fed President Alberto Musalem.

CHINA

Thursday: Exports, Imports, and Trade Balance.

Saturday: CPI and PPI.

JAPAN

Monday: GDP.

Global Macro Updates

The ongoing tariffs saga. The White House confirmed a one-month delay in the implementation of tariffs for automakers, following appeals from automotive industry executives to administration officials on Tuesday. This potential easing of the tariff policy was previously indicated by Commerce Secretary Lutnick, who informed Bloomberg news that certain sectors, including the automotive industry, might be exempt from the 25% tariff.

Separately, Agriculture Secretary Brooke Rollins revealed to Bloomberg news that the Trump administration is considering specific tariff exemptions and carve-outs for the agricultural sector. Earlier this week, the US President had indicated the potential for tariffs on external agricultural products starting 2nd April, while China announced retaliatory tariffs of 10% - 15% on US food and agricultural imports.

The current sentiment contrasts starkly with the optimism prevalent three months ago. The prevailing notion among market participants was to "take Trump seriously, not literally." While there was enthusiasm for potential tax cuts, deregulation, a favourable cryptocurrency regime, and an anticipated wave of M&A, few anticipated the rapid implementation of such a stringent tariff regime. President-elect Trump had pledged to impose tariffs, but as Joe Weisenthal of Bloomberg's Odd Lots observed, "they didn't take him literally or seriously."

The pursuit of an ‘America First’ policy may be incompatible with booming asset prices. Thus far, stock market volatility has not deterred the White House from pursuing its agenda. However, there are downside risks for the US economy, including a deceleration of real income growth, which could signal potential labour market weakness.

The conventional response to labour market weakness is monetary easing through interest rate cuts. Market expectations for rate cuts have indeed increased, with a 44% probability currently priced in for a Fed rate cut at the FOMC May meeting, up from 25% a week ago. However, the implementation of tariffs introduces uncertainty, potentially delaying the Fed's timing and magnitude of rate cuts.

The US government appears to have recognised that undermining the USMCA is detrimental to the US economy and the manufacturing sector. There are indications that tariffs may be reduced or modified for goods with US content or those meeting USMCA content requirements.

Nevertheless, the specific details of any potential agreement remains unclear. Moreover, the damage to the integrated North American supply chain has already been inflicted. One of the primary benefits of the USMCA was the predictability that fostered long-term cross-border investment, and this episode has significantly undermined that predictability.

The current policy environment presents challenges for businesses in planning, sourcing materials, and forecasting consumer demand and supplier availability. As Rachel Ziemba wrote for Weaponized Economy, "Tariffs are here on the US' largest trading partners, but the way in which they are being applied and changed at the last minute adds to maximum confusion and scrambling. The net result is to send a message that it's no longer safe to assume that North American production integration will continue."

Defence and growth: Germany's bold fiscal shift. The CDU/CSU and SPD parties in Germany reached a significant agreement on Tuesday to increase defence and infrastructure spending, preceding formal coalition talks. Key elements of this agreement include the establishment of a new €500 billion special infrastructure fund over a 10-year period, the exemption of defence spending exceeding 1% of GDP from the constitutional debt brake, and an increase in the permitted structural deficit for states from 0.0% to 0.35% of GDP. Parliamentary votes on these measures are anticipated next week, leveraging the existing majority ratios within the Bundestag.

These proposals necessitate constitutional amendments, requiring a 75% majority vote in parliament. Consequently, the parties will need support from the Green Party. While representing a departure from prior election promises, Merz's commitment to defence suggests potential future spending exceeding 3% of GDP. Utilising the current parliamentary composition strategically avoids potential opposition from Die Linke and AfD parties. Danske Bank estimates that these reforms could stimulate economic growth by 0.2% in 2026, 0.25% in 2027, and 0.20% in 2028.

Analysts project that swift implementation, coupled with rapid increases in defence spending to 3.5% of GDP and a substantial infrastructure boost, could generate annual GDP growth of 0.6% to 1.0%, with a deficit-to-GDP ratio reaching 4.5% by 2027. Conversely, a more gradual approach is estimated to result in annual GDP growth of 0.2% to 0.8% and a deficit-to-GDP ratio of 3.1% by 2027.

Additionally, the European Union is confronting unprecedented security challenges as leaders convene in Brussels on Thursday. Amid concerns over diminishing US support under the Trump presidency, the EU is urgently seeking to enhance its defence capabilities and provide support to Ukraine. European Commission President von der Leyen has proposed a substantial increase in defence spending, but internal disagreements, particularly with Hungary, are hindering efforts to deliver military aid to Ukraine, as reported by EurActiv.

Furthermore, Eurointelligence highlights that the onus of securing necessary funding rests on individual member states. Consequently, the relaxation of EU fiscal rules may not offer immediate relief to countries already facing budgetary constraints. Additionally, the procurement process for military equipment could result in a delay of up to a year before funds reach recipient countries. The French approach underscores this fiscal reality, as the government is considering the implementation of taxes targeting wealthy households and the establishment of defence-related investment funds accessible to private investors.

ECB preview. The ECB is poised to implement a 25 bps reduction to its key interest rates today, lowering the deposit rate to 2.5%. This action would represent the fifth consecutive rate cut and the sixth instance of monetary easing since June of 2024. The decision is anticipated to be unanimous, with support from a majority of hawkish officials. However, increased uncertainty regarding future policy actions is expected from April onward.

As the ECB's policy rate approaches the neutral rate, estimated by staff to be between 1.75% and 2.25%, policy divisions within the Governing Council could widen. There is speculation that the ECB may modify its policy statement and remove references to policy being restrictive, although the longstanding preference has been to maintain flexibility.

Macroeconomic forecasts are likely to lead to an upward revision of near-term inflation projections, with minimal changes to the longer-term outlook. Inflation risks are viewed as balanced. Growth projections are expected to be revised downward, with potential headwinds from tariffs and increased geopolitical uncertainty.

In the longer term, Europe's initiative to substantially increase defence spending could have implications for ECB policy, although these effects are likely to extend beyond immediate policy considerations.

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

本文提供给您仅供信息参考之用,不应被视为认购或销售此处提及任何投资或相关服务的优惠招揽或游说。金融工具交易存在重大亏损风险,未必适合所有投资者。过往表现并非未来业绩的可靠指标。