Is inflation on a glide path lower through 2026?

Key data to move markets today

EU: Eurozone’s Harmonized Index of Consumer Prices and Core Harmonized Index of Consumer Prices and a speech by ECB Board member Piero Cipollone

USA: Building Permits, Housing Starts, Industrial Production, Michigan Consumer Sentiment and Expectations Indices and UoM 1- and 5-year Consumer Inflation Expectations

Global Macro Updates

June retail sales in line with expectations. Headline retail sales rose 0.2% m/o/m in June, matching consensus expectations and following May’s 1.0% increase, which was revised up from 0.9%. Excluding autos, retail sales declined 0.2% m/o/m, compared with consensus expectations for a 0.1% decrease and May’s 1.0% gain, revised up from 0.8%. Control group sales, which feed into GDP calculations, increased 0.5%, above consensus expectations for a 0.4% rise and following May’s 0.8% advance, revised up from 0.7%.

Sales declined at gas stations, health and personal care stores, miscellaneous retailers, clothing and accessories stores and food and beverage stores. Gains were recorded by online retailers, motor vehicle and parts dealers, sporting goods and hobby stores, electronics and appliance stores, building materials and garden suppliers, general merchandise stores and restaurants and bars. Furniture and home furnishing store sales were unchanged.

The report was broadly consistent with economist previews. Lower gasoline prices weighed on headline sales, while stronger motor vehicle spending and online sales linked to Prime Day provided an offset.

The data followed a mixed reading on consumer spending from the prior day. The Fed’s Beige Book noted a slight increase in consumer spending, even as higher fuel prices prompted some consumers to trade down. Separately, Bank of America’s CEO said affordability pressures remain, though resilient consumer spending continues to support economic growth.

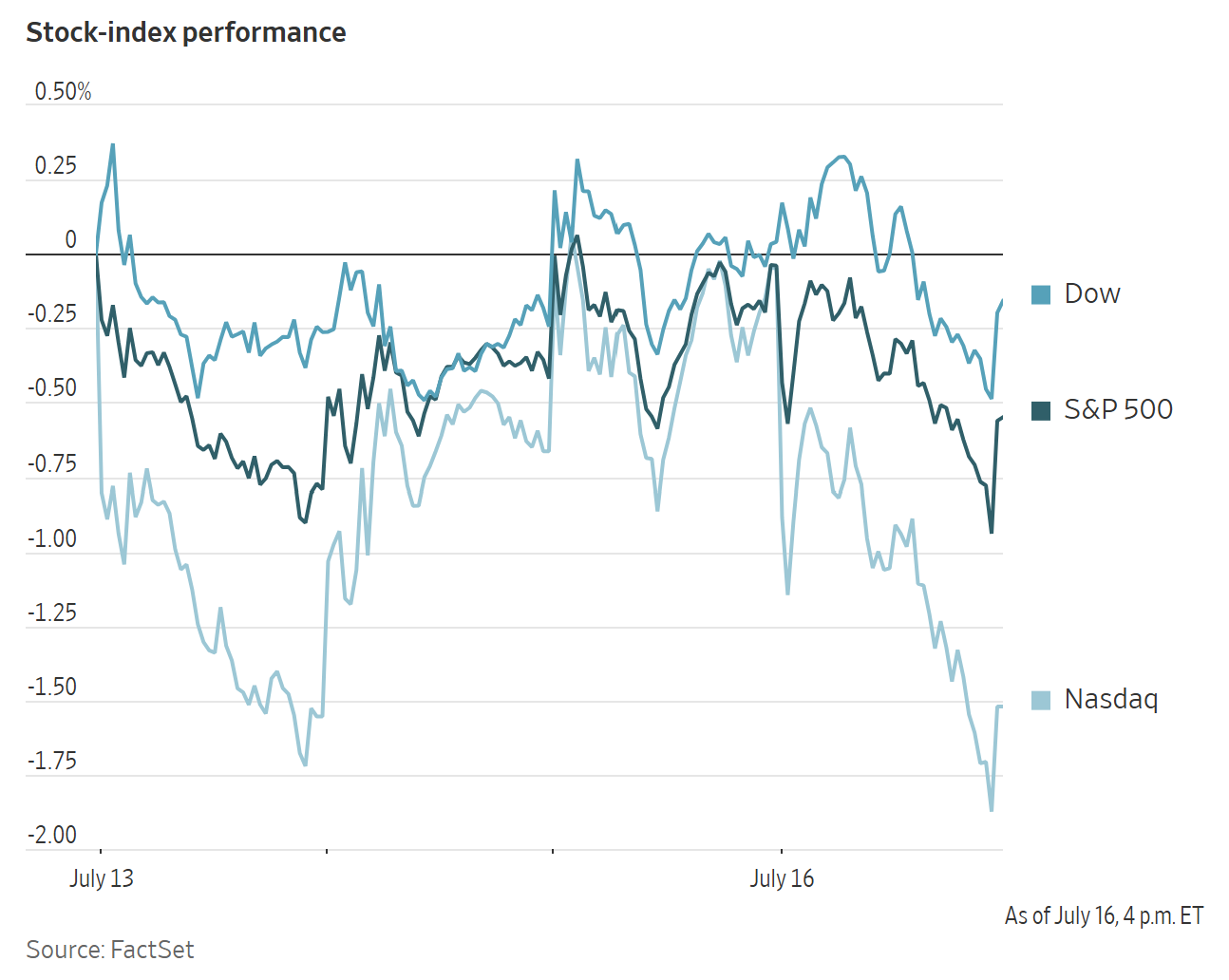

US Stock Indices

Dow Jones Industrial Average -0.20%

Nasdaq 100 -1.62%

S&P 500 -0.51%, with 8 of the 11 sectors of the S&P 500 down

Major US equity indexes declined on Thursday. The Nasdaq Composite lost -1.47%, the S&P 500 declined by -0.51% and the Dow Jones Industrial Average retreated -0.20%, or 105.67 points.

In corporate news, TSMC shares declined by more than 2%, despite the company reporting its fifth consecutive quarter of record earnings.

Eli Lilly agreed to acquire psychedelic drug developer AtaiBeckley for an initial $2.8 billion, only weeks after the Trump administration pledged to accelerate regulatory approvals for mind-altering treatments targeting mental health conditions. The agreement also includes contingent value rights that could lift the total potential transaction value to $3.8 billion, equivalent to $9.25 per share, if AtaiBeckley’s drugs meet specified development and regulatory milestones.

Uber Technologies agreed to acquire Delivery Hero in a transaction valuing the German company at $14.8 billion. Uber offered €41.50 per share and will acquire Delivery Hero’s operations across 50 markets, subject to regulatory approval. The acquisition represents a significant expansion for Uber across Asia, Latin America and the Middle East, increasing its total market presence to 99 markets from 79. Uber plans to finance the transaction with existing cash and new debt.

European Stock Indices

CAC 40 -0.05%

DAX -0.34%

FTSE 100 +0.54%

Commodities

Gold spot -2.10% to $3,972.76 an ounce

Silver spot -3.21% to $55.50 an ounce

West Texas Intermediate -0.82% to $79.58 a barrel

Brent crude -0.86% to $84.90 a barrel

Gold prices fell by more than two percent on Thursday, reaching their lowest level in more than two weeks as investors reassessed positioning across precious metals.

Spot gold was down -2.10% at $3,972.76 per ounce after touching its lowest level since 1 July earlier in the session.

Spot silver declined -3.21% to $55.50 per ounce.

Oil prices settled slightly lower on Thursday but remained close to their highest levels since mid-June, as the escalation of the Iran conflict continued to support risk premia across energy markets.

Brent crude futures declined 74 cents, or -0.86%, to $84.90 per barrel, while US WTI futures fell 66 cents, or -0.82%, to $79.58 per barrel. At their session highs, both contracts had been up by more than one percent.

Late Wednesday, US Central Command said it had completed its latest wave of strikes against positions in Iran, before announcing that another round of attacks began at 14:00 ET yesterday. It also struck an empty VLCC, the Belma, deep within the Persian Gulf near Iran’s key oil export terminal, marking its first attack on a vessel since the US reimposed its blockade on the country’s shipping.

Iran launched attacks against Jordan, Bahrain and Kuwait, and reportedly disrupted oil-loading capabilities at Iraq’s Basra export terminal. Iraq denied that all loadings were offline; however, other updates indicated that the full 2 million bpd of capacity was down. Ship voyages through the Strait of Hormuz fell to only 13 on Wednesday, with most vessels taking the Iranian route.

Crude benchmarks peaked intraday after reports that Iran had asked Yemen’s Houthis to stand ready to close the Red Sea oil route if the US strikes Iranian power infrastructure. Houthi leaders also threatened to target Saudi oil facilities if Riyadh becomes involved in a broader military escalation. Prices briefly rallied again following reports of explosions in downtown Dubai.

Ukraine’s attacks on Russian energy infrastructure continued overnight, with a refinery and two smaller tankers in the Azov Sea hit, while two larger crude carriers in the Black Sea were struck intraday.

Note: As of 4 pm EDT 16 July 2026

Currencies

EUR -0.18% to $1.1442

GBP -0.44% to $1.3473

Bitcoin -1.08% to $64,104.05

Ethereum -2.34% to $1,876.13

The dollar held gains against major peers on Thursday, recovering from a nearly one-month low reached on Wednesday.

The US dollar index rose +0.22% to 100.73, moving off its lowest level since June 18, though it remained on track for a weekly decline.

The euro fell -0.18% to $1.1442, ending a two-day advance. Investors continued to monitor European gas futures, which rose to their highest levels since March, raising concerns that higher energy costs could weigh on the eurozone economy and limit further appreciation of the currency.

The ECB is viewed as more hawkish than the Fed, with markets pricing in two additional rate increases into 2027 and some economists not ruling out an initial move as soon as next week.

Sterling retreated from a nearly two-month high, trading -0.44% lower at $1.3473, as investors anticipated that Britain’s incoming prime minister would appoint a fiscally conservative finance minister.

The dollar rose +0.16% to ¥162.38 against the yen.

Fixed Income

US 10-year Treasury +0.4 basis points to 4.559%

German 10-year Bund +1.3 basis points to 3.163%

UK 10-year Gilt +3.8 basis points to 4.972%

US Treasury yields moved modestly higher on Thursday after consumer and labor-market data did little to alter investor expectations for the near-term path of Fed policy.

The yield on the US 10-year Treasury note rose +0.4 bps to 4.559%. The yield had declined -6.5 bps over the previous two sessions, its largest two-day drop in three weeks.

The yield on the 30-year bond edged up +0.4 bps to 5.086%.

The 2-year note yield, which typically tracks Fed funds-rate expectations, advanced +1.5 bps to 4.158%.

Eurozone bond yields rose across countries and maturities on Thursday. Germany’s 10-year Bund yield increased +1.3 bps to 3.163%, its highest level since 20 May.

Markets currently assign roughly a 90% probability to an ECB rate increase by the September meeting, which would mark the second hike this year after June’s move, while also pricing a meaningful probability of a third increase by year-end.

The 2-year Schatz yield moved broadly in line with the 10-year Bund yield on Thursday, rising +2.1 bps to 2.765%.

The spread between German and US 10-year borrowing costs was last at 139.6 bps, near its lowest level since early June. Eurozone spreads were little changed, with the spread between 10-year Bunds and Italian BTP yields at 77.9 bps.

Note: As of 4 pm EDT 16 July 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

本文提供給您僅供資訊參考之用,不應被視為認購或銷售此處提及任何投資或相關服務的優惠招攬或遊說。金融商品交易涉及重大損失風險,可能不適合所有投資者。過往績效不代表未來表現。

由專業人士建立。為專業人士打造。