Have bonds overreacted?

Key data to move markets today

EU: German Retail Sales, Unemployment Change and Unemployment Rate, French and Italian CPIs, Eurozone Harmonised Index of Consumer Prices and Core Harmonised Index of Consumer Prices and a speech by Dutch Central Bank Governor Olaf Sleijpen

UK: GDP

US: Chicago PMI, Consumer Confidence, Housing PRice Index, JOLTS Job Openings, and speeches by Chicago Fed President Austan Golsbee, Kansas City Fed President Jeff Schmid, and Fed Governors Michael Barr and Michelle Bowman

JAPAN: Tankan Large’s Manufacturing Index, All Industry Capex and Outlook

CHINA: RatingDog Manufacturing PMI

Global Macro Updates

Fed Chair Powell speech. Fed Chair Jerome Powell, speaking at Harvard University on Monday, expressed a measured approach in response to the ongoing conflict in Iran. He emphasised that the Fed's monetary policy tools have limited effectiveness in mitigating the effects of supply shocks, such as those arising from oil price disruptions, and noted that inflation expectations remain anchored.

Powell further highlighted the persistent tension between the Fed’s dual mandate of promoting maximum employment and stable prices. He characterised tariff-influenced price increases as predominantly one-off events, estimating their contribution to inflation at approximately 0.5% to 1.0%.

Addressing developments in the private credit sector, Powell asserted that he does not foresee a risk of contagion, observing that private credit constitutes a relatively small fraction of the broader asset landscape.

Powell also acknowledged that the labour market faces enduring structural challenges, but pointed to the potential for productivity improvements driven by artificial intelligence. He conveyed an optimistic outlook for the US economy, both in the medium and long term.

Eurozone sentiment falls as inflation pressures intensify. The eurozone Economic Sentiment Indicator (ESI) declined in March, dropping to 96.6 compared to the consensus estimate of 96.0 and the previous reading of 98.3. Industry confidence registered at -7.0, outperforming the forecast of -9.3 but slightly lower than the prior figure of -7.1. Services confidence stood at 4.9, above the consensus of 2.0, yet marginally below last month’s 5.0. The most pronounced deterioration was observed in the consumer confidence index, which fell to -16.3 from -12.2, accompanied by a two-point reduction in retail confidence. Among eurozone countries, France saw the steepest decline in its ESI (-3.7), followed by Spain (-2.4). The employment expectations indicator decreased by 1.3 points to -97.3, with downward revisions across retail trade, services and industry sectors. These trends closely mirror last week’s S&P Global Flash eurozone PMI release, which showed a sharp rise in selling price expectations across all four business sectors. The composite PMI reached a ten-month low at 50.5, indicating a slowdown in activity and the fastest increase in input costs in three years. Additionally, the ESI breakdown revealed a surge in consumer price expectations amid higher inflation, as well as a marked increase in economic uncertainty, particularly within the industry and retail trade sectors, due to concerns about future business conditions.

In Germany, CPI accelerated to 2.8% y/o/y in March, marking the fastest pace in over twelve months. This increase was largely attributed to the Iran conflict, which propelled energy prices 7.2% higher compared to the previous year, according to preliminary data from DeStatis. The result was in line with analyst expectations and reversed the disinflationary trend observed last year, with core inflation remaining steady at 2.5%. The surge in energy-related prices parallels a more pronounced rise in Spain, where flash HICP inflation climbed to 3.3% y/o/y, despite fiscal measures aimed at moderating the effect. Analysts indicate that the concurrent movements in German and Spanish inflation support an anticipated eurozone headline inflation rate of approximately 2.6%.

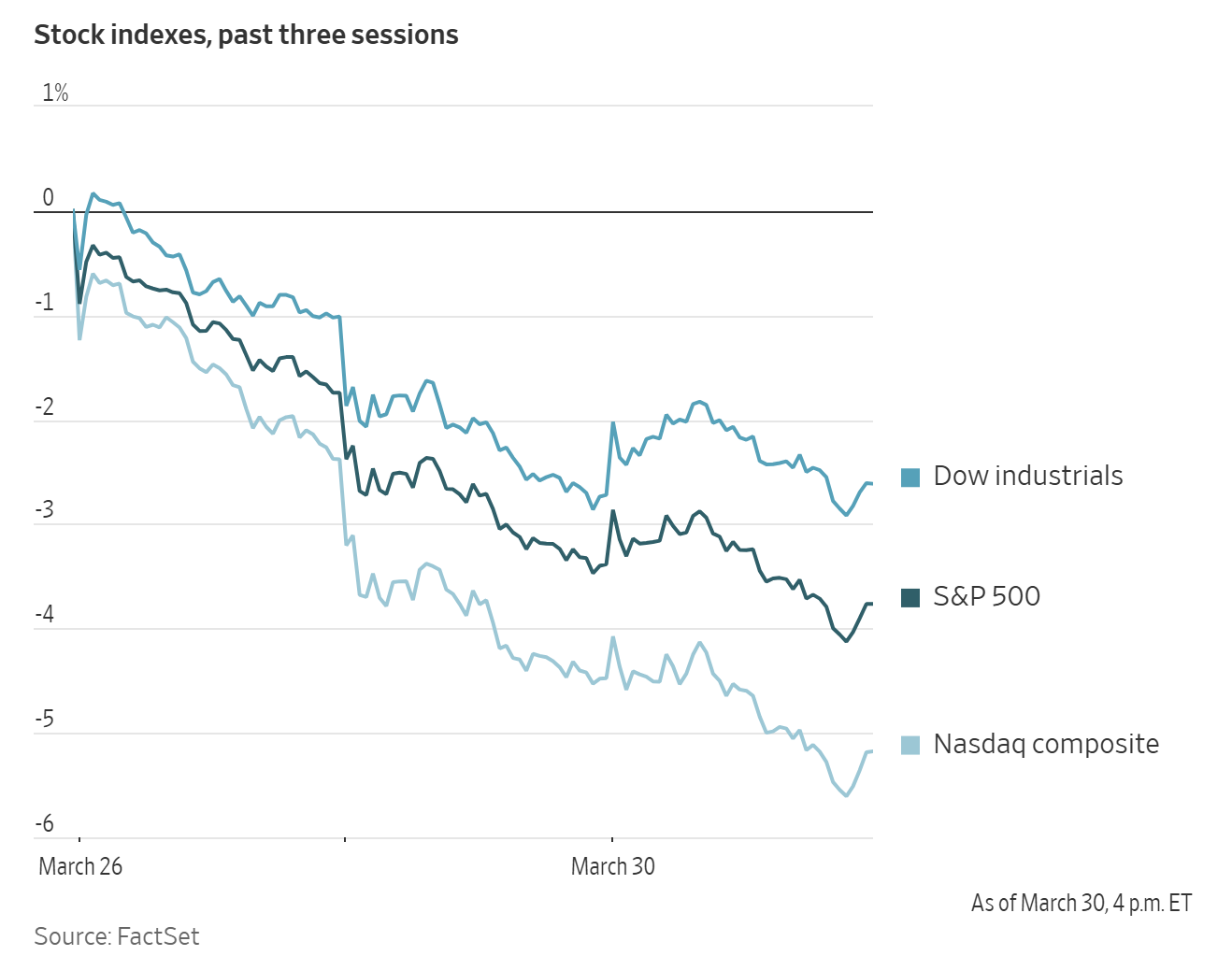

US Stock Indices

Dow Jones Industrial Average +0.11%

Nasdaq 100 -0.78%

S&P 500 -0.39%, with 3 of the 11 sectors of the S&P 500 down

Equity markets have experienced consecutive weeks of losses since the US initiated military action against Iran at the end of February. As a result, the S&P 500 is currently poised for its weakest monthly performance since September 2022.

On Monday, the S&P 500 declined for the third consecutive session, ending the day down -0.39%. The Nasdaq Composite also fell by -0.73%, marking its third straight loss and reaching its lowest closing level since early August. Conversely, the Dow Jones Industrial Average edged higher by +0.11%, gaining 49.50 points.

The Russell 2000, which serves as a benchmark for small-cap stocks, is on course for its most significant monthly point decline since the onset of the Covid-19 pandemic in March 2020. The index is down -8.30% so far in March.

In corporate news, shares of Alcoa surged more than eight percent following reports that two Middle Eastern competitors were targeted by Iranian attacks.

Air Canada announced that its CEO will retire amid political criticism regarding his inability to communicate in French, following a fatal runway collision.

Sysco has agreed to acquire the family-owned Jetro Restaurant Depot in a transaction valued at approximately $29 billion.

Eli Lilly has entered into a drug-discovery partnership with InSilico, a Hong Kong-listed company, which could be worth up to $2.75 billion according to InSilico.

S&P 500 Best performing sector

Utilities +0.66%, with Edison International +2.19%, PG&E +1.81% and Exelon +1.63%

S&P 500 Worst performing sector

Industrials -1.61%, with Generac -4.85%, GE Vernova -4.20% and Caterpillar -4.02%

Mega Caps

Alphabet -0.23%, Amazon +0.81%, Apple -0.87%, Meta Platforms +2.03%, Microsoft +0.61%, Nvidia -1.40% and Tesla -1.81%

Information Technology

Best performer: ServiceNow +5.59%

Worst performer: Micron -9.88%

Materials and Mining

Best performer: FMC +6.66%

Worst performer: Smurfit Westrock -2.94%

European Stock Indices

CAC 40 +0.92%

DAX +1.18%

FTSE 100 +1.61%

Commodities

Gold spot +0.40% to $4,510.24 an ounce

Silver spot +0.68% to $70.06 an ounce

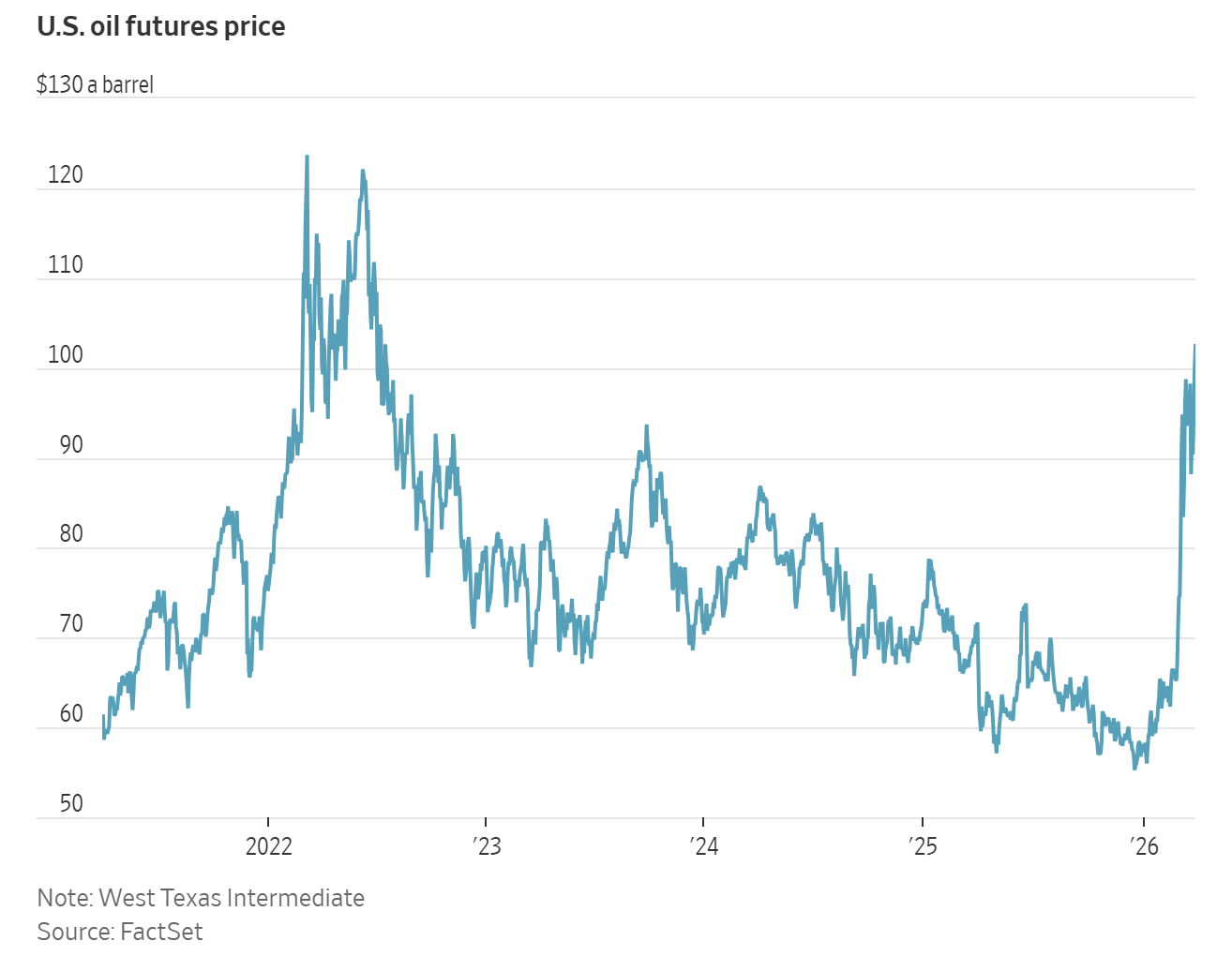

West Texas Intermediate +6.00% to $105.62 a barrel

Brent crude -0.04% to $114.52 a barrel

Gold advanced for the second consecutive session on Monday, supported by increased safe-haven demand amid market uncertainty.

Spot gold climbed +0.40% to $4,510.24 per ounce, rebounding after reaching its lowest point since November earlier last week.

However, gold has declined -14.84% so far in March, positioning the metal for its most significant monthly loss since 2008.

Spot silver also moved higher, rising +0.68% to $70.06 per ounce.

US crude futures surged by more than five percent on Monday, reflecting heightened supply concerns as the conflict in the Middle East intensified.

US WTI crude increased by $5.98, or +6.00%, to $105.62 per barrel. It has surged over +56.96% this month, marking its strongest monthly performance since May 2020. Brent crude futures edged lower by 5 cents, or -0.04%, to $114.52 per barrel.

Russia's Baltic Ust-Luga port, a major petroleum export hub, sustained further damage on Sunday following a Ukrainian drone attack that ignited a blaze, which was subsequently contained, according to Russian officials. This marks the fourth instance in eight days that the port has been targeted by Ukrainian drones.

Iran continued its attacks on Middle Eastern countries on Monday, with explosions reported in Qatar. Saudi Arabia announced it had intercepted several missiles, while Turkey, the UAE and Kuwait were also targeted. Iran denied any attempted attack on a Kuwaiti desalination plant, attributing the incident to Israel. Leaders from Jordan, Qatar and other nations convened in Saudi Arabia for discussions with the Crown Prince regarding the evolving situation in the region.

G7 finance leaders stated that the group stands prepared to take ‘all necessary measures’ to ensure energy market stability following a teleconference held on Monday. Additionally, the EU announced the expansion of its naval operations in the Red Sea.

Note: As of 4 pm EDT 30 March 2026

Currencies

EUR -0.34% to $1.1461

GBP -0.57% to $1.3180

Bitcoin +1.13% to $66,763.48

Ethereum +2.57% to $2,035.40

On Monday the dollar index increased +0.30% to 100.49, reaching as high as 100.61, its strongest point since 19 May.

The euro weakened against the dollar amid concerns regarding the economic impact of a prolonged US-Israeli conflict with Iran. The Japanese yen found support as Japanese officials heightened their rhetoric regarding potential currency intervention.

The euro declined -0.34% to $1.1461, while sterling fell -0.57% to $1.3180, having previously touched $1.3170, its lowest level since 26 November.

The Japanese yen appreciated +0.35% against the dollar to ¥159.75 per dollar, after briefly falling below the significant ¥160 per dollar threshold. This marked its weakest level since July 2024, when Japan last intervened to bolster the currency.

In the most assertive warning yet regarding yen-buying intervention, Japan’s top currency diplomat, Atsushi Mimura, stated on Monday that authorities may be compelled to take ‘decisive’ action should speculative trading persist in the currency markets.

Additionally, BoJ Governor Kazuo Ueda noted that the central bank will monitor movements of the yen closely, as fluctuations impact both the economy and price levels. He indicated that inflationary pressures stemming from a weaker currency could warrant an interest rate increase in the coming months.

Fixed Income

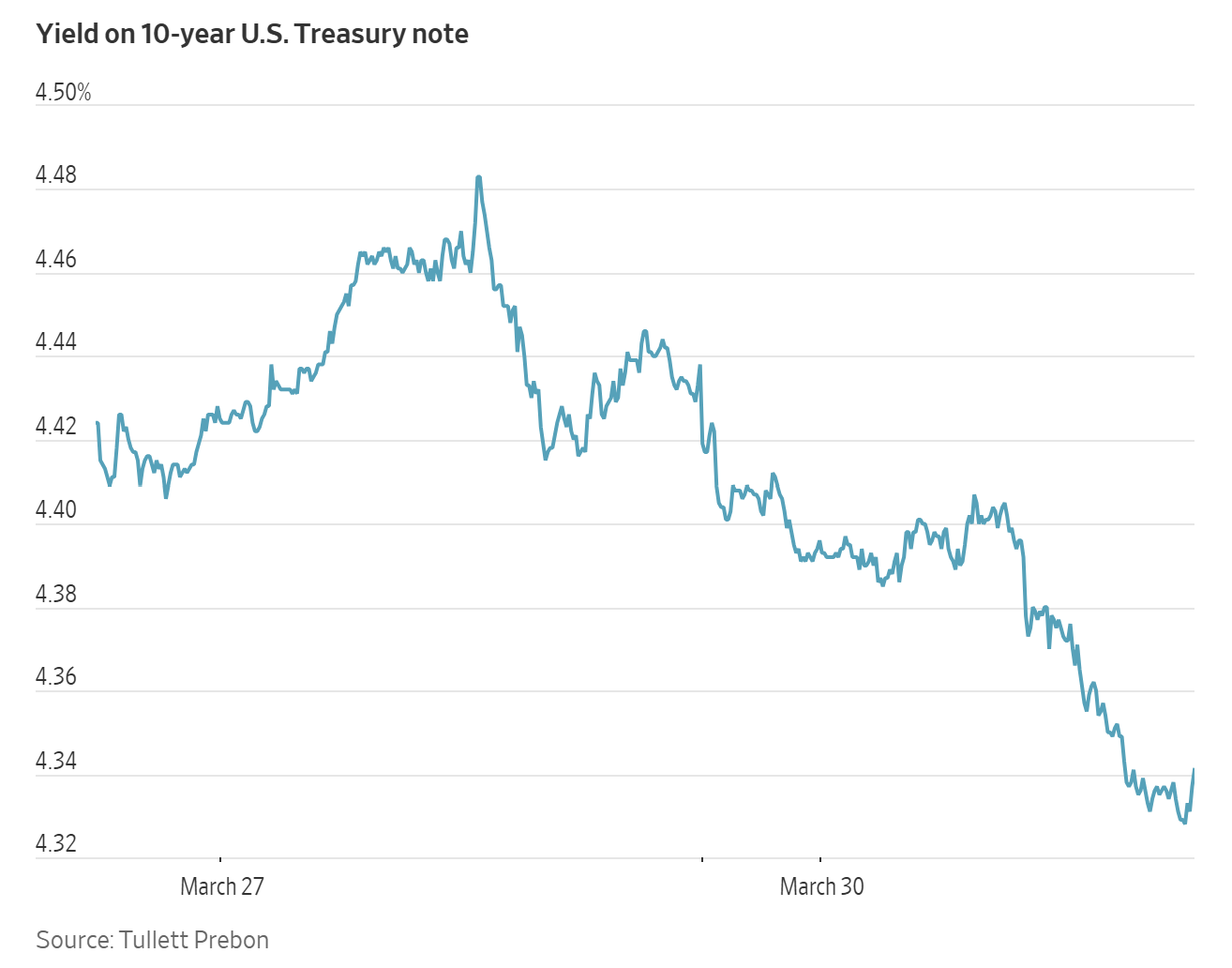

US 10-year Bond -8.2 basis points to 4.356%

German 10-year -6.8 basis points to 3.035%

UK 10-year gilt -4.4 basis points to 4.878%

US Treasuries advanced across the yield curve on Monday, as escalating concerns about global economic growth overshadowed inflation risks. Investors grew increasingly apprehensive about the ongoing conflict, now entering its fifth week with no clear resolution in sight.

The US 10-year yield declined for the first time in three sessions, dropping -8.2 bps to 4.356%. This marked its most significant daily decrease since early August.

On the short end, the US two-year yield, which reflects expectations for interest rates, fell -8.4 bps to 3.844%. This was the largest one-day drop since late August. At the long end, the 30-year yield retreated -5.5 bps to 4.917%, representing its most substantial daily pullback since 12 February.

Treasuries continued to strengthen following remarks from Fed Chair Jerome Powell, who stated that longer-term inflation expectations remain ‘well-anchored’ despite elevated oil prices.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing in 2.7 bps of rate cuts in 2026, higher than the 2.3 bps priced in the previous week. Fed funds futures traders are now pricing in a 1.6% probability of a 25 bps rate hike at the 29 April FOMC meeting, compared to last week’s 6.2% probability.

Eurozone bond yields also decreased from recent multi-year highs on Monday, as investors evaluated the risks posed by the Iran conflict to inflation and economic growth.

The German 10-year bund yield was -6.8 bps lower at 3.035%, after reaching 3.130% on Friday, their highest level since May 2011.

The German two-year bund yield declined -6.9 bps to 2.622%. On the long end, the 30-year yield fell by -5.6 bps to 3.501%.

Money markets are pricing in approximately 66.7 bps of rate hikes from the ECB this year, a decrease from nearly 90 bps at one point on Friday.

The Italian 10-year BTP yield declined -8.7 bps to 3.983%, having climbed above 4.140%, its highest since mid-2024, on Friday. The spread over Bunds narrowed to 94.8 bps, 1.9 bps lower than the previous session.

Note: As of 4 pm EDT 30 March 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

本文提供给您仅供信息参考之用,不应被视为认购或销售此处提及任何投资或相关服务的优惠招揽或游说。金融工具交易存在重大亏损风险,未必适合所有投资者。过往表现并非未来业绩的可靠指标。

由专业人士创建。 为专业人士。