Are markets underestimating the risks to growth?

Key data to move markets today

EU: Italian CPI, German ZEW Economic Sentiment and Current Situation Surveys, Eurozone Economic Sentiment Survey, and a speech by German Bundesbank President Joachim Nagel

US: ADP Employment Change 4-week Average and Pending Home Sales

JAPAN: Adjusted Merchandise Trade Balance, Exports, Imports, and Merchandise Trade Balance Total

Global Macro Updates

What if Tehran has found its ultimate source of deterrence? The closure of the Strait of Hormuz has precipitated both an immediate crisis and a profound strategic dilemma with global ramifications. The longer the strait remains blocked, the more acute the threat of a worldwide recession, given the waterway's critical role in global energy supply. Iran has now demonstrated that its control over this maritime chokepoint grants it significant leverage over the world economy. Even if Iran were to ease its hold temporarily, it retains the capability, and the incentive, to restrict passage again in the future, effectively using this as a tool of coercion or deterrence.

The reopening of the strait is fraught with significant challenges. Iran does not need to comprehensively halt every vessel; the mere threat, underscored by sporadic attacks, has already dissuaded ship owners, crews, and insurers from risking passage. Military solutions such as the bombing of Iranian infrastructure or a potential US occupation of Kharg Island, crucial for Iran’s oil exports, do not address the core issue. Iran's military capabilities, including deep-sea mines, anti-ship missiles, drones, and other unconventional methods, make any naval effort perilous. Notably, Iran has demonstrated advanced proficiency in drone warfare, as evidenced by its support for Russia’s campaign in Ukraine.

In response, the US has called upon allies, including the UK, EU, and even China, to contribute naval forces to break the impasse. However, these nations are reluctant to endanger their own assets for a crisis they did not initiate, particularly given the risk to vessels and the potential for a protracted conflict. Diplomatic strains, especially after a year of tariffs and rhetoric from the Trump administration, have further eroded the willingness of US allies to participate.

Land-based interventions, such as deploying ground troops, are also fraught with risk, likely resulting in substantial American casualties without guaranteeing the strait’s reopening. Furthermore, the assassination of Iranian leaders and explicit calls for regime change have fundamentally altered Tehran’s strategic calculus. Where Iran once sought to avoid direct confrontation with the US, it now perceives the closure of the Strait as a legitimate survival tactic. This shift has marginalised Iranian moderates and entrenched the regime’s hardline stance.

Looking ahead, the US and its Gulf allies face a stark choice: pursue accommodation with Iran’s current leadership to prevent future closures, or intensify efforts for regime change, accepting the inherent risks of sustained upheaval. Crucially, Iran’s demonstrated ability to close the Strait of Hormuz has established a powerful new deterrent, independent of its nuclear ambitions. If the regime endures, it may emerge from this crisis with enhanced international leverage, having redefined the balance of power in the region.

Trump’s appeal for help in the strait of Hormuz falls on deaf ears. On Monday, UK Prime Minister Sir Keir Starmer insisted that the UK would “not be drawn into the wider war” and refused to send ships while Germany, Japan and France dismissed the prospect of sending vessels to help reopen the Strait of Hormuz. President Trump told the Financial Times that NATO faces a “very bad” future if allies fail to assist the US in opening up the vital waterway, which has been closed by Iran. Germany’s chancellor, Friedrich Merz, said, “There was never a joint decision on whether to intervene. That is why the question of how Germany might contribute militarily does not arise. We will not do so.” In Asia, key US partners including Japan and South Korea have also stopped short of committing ships. This has complicated relations with the US ahead of Prime Minister Sanae Takaichi’s White House visit on Thursday.

This initial refusal came as President Trump admitted on Monday that the US was shocked by the extent of Iran’s firepower. “They hit Qatar, Saudi Arabia, the [United Arab Emirates], Bahrain, Kuwait. Nobody expected that. We were shocked,” he said. However, he still insisted that the US could expand strikes on Kharg Island to target oil infrastructure. The island is Iran’s main export hub.

US Stock Indices

Dow Jones Industrial Average +0.83%

Nasdaq 100 +1.13%

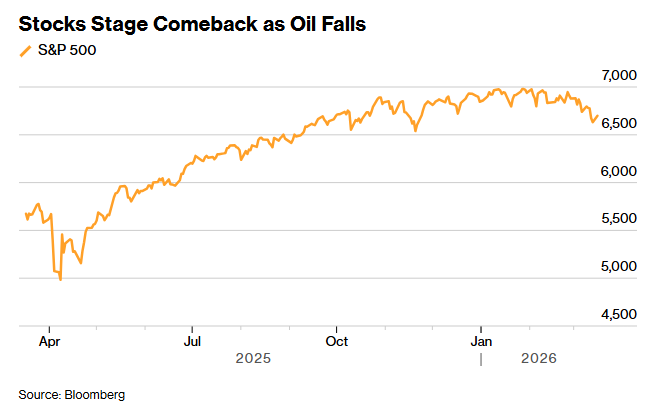

S&P 500 +1.01%, with all of the 11 sectors of the S&P 500 up

On Monday, US equity markets ended sharply higher as oil prices retreated amid ongoing uncertainty about the Middle East conflict and AI related stocks rose. Meta surged +2.33% after Reuters reported that the social media platform plans to shrink its workforce by at least 20% to offset expensive artificial-intelligence infrastructure and prepare for greater efficiency brought about by AI-assisted workers. Nvidia climbed +1.65% after CEO Jensen Huang announced new components at the chipmaker's annual developer conference and said it expects to make at least $1 trillion from artificial-intelligence chips through the end of 2027.

The S&P 500 was +1.01% or 67.19 points to 6,699.38, the Nasdaq Composite was +1.22% or 387.94 points to 22,374.18 points, and the Dow Jones Industrial Average was +0.83% or 387.94 points to 46,946.41 points.

In corporate news, Public Storage has agreed to acquire smaller rival National Storage Affiliates in an all-stock deal valued at about $10.5 billion including debt. Shareholders of National Storage Affiliates will receive 0.14 shares of Public Storage common stock for each share they own, valuing the deal at about $41.68 per share.

S&P 500 Best performing sector

Information Technology +1.39%, with Western Digital +5.11%, Teradyne +4.14%, and Enphase Energy +4.13%

S&P 500 Worst performing sector

Consumer Staples +0.07%, with Molson Coors Beverage -3.46%, Conagra Brands -2.32%, and Brown-Forman Corporation -1.75%

Mega Caps

Alphabet +0.98%, Amazon +1.96%, Apple +1.08%, Meta Platforms +2.33%, Microsoft +1.11%, Nvidia +1.65%, and Tesla +1.11%

Information Technology

Best performer: Western Digital +5.11%

Worst performer: CrowdStrike Holdings -4.06%

Materials and Mining

Best performer: Freeport-McMoRan +2.75%

Worst performer: Mosaic -5.60%

European Stock Indices

CAC 40 +0.31%

DAX +0.50%

FTSE 100 +0.55%

Commodities

Gold spot -0.26% to $5,005.25 an ounce

Silver spot +0.27% to $80.77 an ounce

West Texas Intermediate -5.09% to $94.26 a barrel

Brent crude -2.76% to $101.02 a barrel

On Monday, gold prices declined as apprehensions regarding inflation—driven by the ongoing Middle East conflict and its potential to sustain elevated interest rates—outweighed the positive influence of a weaker dollar and increased safe-haven demand.

Spot gold slipped by -0.26% to $5,005.25 per ounce, marking its lowest point since 19th February earlier in the trading session.

Spot silver rose by +0.27% to $80.77 per ounce.

Oil prices declined on Monday as attacks disrupted Gulf oil production and the US President called for coordinated international efforts to secure the Strait of Hormuz.

Brent crude futures fell by $2.87, or -2.76%, to $101.02 per barrel, while US West Texas Intermediate crude dropped $5.05, or -5.09%, to $94.26 per barrel.

According to sources cited by Reuters, the United Arab Emirates experienced a significant reduction in daily oil output, with production cut by more than half. This decrease was attributed to the ongoing conflict involving Iran and the effective closure of the Strait of Hormuz, which prompted the state oil company ADNOC to implement extensive production shut-ins.

ADNOC suspended crude loading operations at the UAE port of Fujairah following a drone strike that ignited fires at the major export terminal. Although some loading activity at the port has resumed, only two out of its three single point moorings are currently operational.

Fujairah, situated outside the Strait of Hormuz, serves as the outlet for approximately 1 million barrels per day of the UAE’s flagship Murban crude oil, representing roughly 1% of global demand.

The British Prime Minister stated on Monday that Britain would not become involved in a broader conflict but would collaborate with allies to develop a "viable" plan for reopening the Strait of Hormuz.

US Treasury Secretary Scott Bessent told CNBC that the Treasury had not intervened in oil markets, and any potential US action to address rising prices would depend on the duration of the conflict.

The International Energy Agency (IEA) reported on Thursday that the war in the Middle East has led to the largest oil supply disruption in history, as major producers such as Saudi Arabia, Iraq, and the UAE have curtailed output.

Over the weekend, the US President threatened additional strikes on Iran’s Kharg Island, which handles about 90% of the nation’s exports, following earlier attacks on military targets that provoked further retaliation from Tehran.

On Sunday, the IEA announced that more than 400 million barrels of oil reserves would soon be released to the market, marking a record draw intended to mitigate price surges resulting from the ongoing conflict in the Middle East.

The agency further indicated that stocks from Asian and Oceanian countries would be released immediately, while reserves from Europe and the Americas are scheduled to become available at the end of March.

Note: As of 4 pm EDT 16 March 2026

Currencies

EUR +0.78% to $1.1505

GBP +0.73% to $1.3318

Bitcoin +4.64% to $74,412.33

Ethereum +12.27% to $2,361.47

The dollar retreated from its 10-month highs on Monday amid persistent uncertainty stemming from the conflict in the Middle East, as markets prepared for a week marked by significant central bank meetings.

Investors are positioning themselves ahead of key policy decisions scheduled this week from the Fed, the ECB, the BoE, and the BoJ.

The euro reversed its trajectory after reaching a seven-and-a-half-month low earlier in the session, rising +0.78% to $1.1505. Meanwhile, sterling appreciated +0.73% to $1.3318, just above the three-and-a-half-month low recorded on Friday.

The dollar index declined by -0.67% to 99.82, ending a four-day streak of gains; however, it remained near Friday’s 10-month peak of 100.54.

The Japanese yen hovered just below 160 per dollar, marking its weakest level since the BoJ’s last intervention to bolster the currency in July 2024. The yen has faced pressure due to Japan’s substantial dependence on the Middle East for energy supplies, with the ongoing conflict casting uncertainty over the BoJ’s interest rate outlook.

The dollar was down -0.44% to ¥159.01 against the Japanese yen.

Fixed Income

US 10-year Bond -5.8 basis points to 4.224%

German 10-year -3.7 basis points to 2.949%

UK 10-year gilt -5.9 basis points to 4.712%

US Treasuries experienced a rebound on Monday, supported by an improvement in risk appetite.

The 10-year yield fell -5.8 bps to 4.224% after rising for five consecutive sessions, marking its largest single-day decline since mid-February. Yields on two-year Treasury notes, closely tied to interest rate expectations, also decreased by -4.8 bps to 3.686%, registering their most significant daily drop since late February.

Similarly, 30-year Treasury yields declined by -3.4 bps to 4.869%, on track for their sharpest one-day retreat since 12th February.

The yield curve flattened during the session, as the spread between two-year and 10-year yields narrowed by 1.0 bps to 53.80 bps, down from 54.8 bps at the close on Friday.

Investors are now focused on the upcoming FOMC meeting this week, closely monitoring the Fed’s assessment of the economy and its interest rate outlook amid ongoing geopolitical tensions.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing in 25.5 bps of cuts in 2026, lower than the 40.2 bps priced in the previous week. Fed funds futures traders are now pricing in a 0.9% probability of a 25 bps rate cut at the FOMC meeting this week, down from 1.6% a week ago.

German Bund yields declined on Monday, retreating from their highest levels in nearly two and a half years.

The yield on Germany’s 10-year government bond fell by -3.7 bps to 2.949%, after reaching 2.994% on Friday, the highest since October 2023.

Italy’s 10-year government bond yield decreased by -5.4 bps, settling at 3.732%.

Money markets are currently fully pricing in one ECB rate hike by July, with an approximately 80% probability of a second increase by the end of the year.

While market participants anticipate a proactive and resolute ECB, prepared to prioritise inflation control over economic growth, most economists do not expect the Governing Council to support a near-term rate hike.

The ECB, alongside the BoE and the BoJ, is scheduled to announce its monetary policy decisions on Thursday.

Although central banks are widely expected to keep interest rates unchanged this month, investors will closely monitor any indications regarding policymakers’ responses to the economic repercussions of the ongoing conflict in the Middle East.

Germany’s two-year yield, highly sensitive to policy rate expectations, declined by -5.5 bps on Monday to 2.401%, after peaking at 2.476% last week, its highest level since August 2024.

Despite German government bonds losing some of their traditional safe-haven appeal, yield spreads have widened during periods of heightened geopolitical tensions, with the magnitude of these movements influenced by individual countries’ reliance on oil and LNG imports from the Strait of Hormuz.

The yield spread between Italian 10-year government bonds and German Bunds widened to 78.3 bps, compared to 69.4 bps prior to the escalation of hostilities involving the United States, Israel, and Iran.

Meanwhile, French 10-year bonds yielded 67.6 bps more than Bunds, up from 65.5 bps before the onset of the conflict.

Note: As of 4 pm EDT 16 March 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

本文提供给您仅供信息参考之用,不应被视为认购或销售此处提及任何投资或相关服务的优惠招揽或游说。金融工具交易存在重大亏损风险,未必适合所有投资者。过往表现并非未来业绩的可靠指标。

由专业人士创建。 为专业人士。