Is the dollar’s war premium back?

Corporate Earnings News

Companies reporting on Wednesday, 4th March: Broadcom, Fair Isaac, Brown-Forman, Dycom Industries

Posted on Tuesday, 3rd March

Best Buy quarterly revenue -1.1% to $13.81 bn vs $13.88 bn estimate

Adjusted EPS at $2.61 vs $2.47 expected

During the earnings call, CEO Corie Barry said, “data sources indicated market share was ‘at least flat,’ attributing the quarter’s results to slightly softer consumer demand for our industry during the holiday quarter.“ As noted by Yahoo Finance, Barry outlined mitigation actions, including pulling inventory forward, extending vendor forecast horizons, ensuring favorable terms, specifying configurations to meet price points, narrowing assortments to improve in-stocks, and educating customers through tools like trade-in, financing, refurbished options, and easy upgrades with Geek Squad. On the guidance range, Barry said the high end assumes higher prices offset by lower units, while the low end assumes broader inventory constraints. — see report.

Target quarterly revenue -1.5% to $30.45 bn vs $30.48 bn expected

Adjusted EPS $2.44 vs. $2.16 expected

According to CNBC, during the earnings call Chief Financial Officer Jim Lee said that Target will step up its spending this year to support the company’s turnaround. He said capital expenditures will total about $5 billion this fiscal year, an increase of more than $1 billion from last fiscal year. He also said that spending will go toward Target’s supply chain, technology and investment in stores. It plans to open more than 30 new stores and remodel more than 130 stores this fiscal year. — see report.

CrowdStrike Holdings revenue +23% to $1.31 bn vs $1.30 bn estimate

Adjusted EPS $1.12 vs $1.10 expected

George Kurtz, CrowdStrike's Founder and CEO, said, “FY26 will go down in our history books as CrowdStrike's best year yet. We achieved $5.25 billion in ending ARR - the fastest and only pure-play cybersecurity software company to achieve this milestone - driven by a record $1.01 billion of net new ARR, our first year exceeding $1 billion of net new ARR. We also delivered record operating and free cash flow for both the quarter and year. Our record results showcase the durability of our growth and cash flow generation. As enterprises rapidly adopt AI, CrowdStrike is mission-critical infrastructure - securing AI across every layer from GPU to agent to prompt. The AI revolution is creating a massive growth opportunity for CrowdStrike, one that our technology, team, and ecosystem are well positioned to continue winning.” — see report.

Key data to move markets today

EU: Spanish, French, Italian, German and Eurozone HCOB Services PMI, German and Eurozone Composite PMIs, Eurozone PPI, Eurozone Unemployment Rate, Italian GDP and speeches by ECB Executive Board member Piero Cipollone, ECB Vice President Luis de Guindos, and Italian Central Bank Governor Fabio Panetta

UK: S&P Global Composite and Services PMIs

US: ADP Employment Change, S&P Global Composite and Services PMIs, ISM Services Employment Index, New Orders Index, PMI, Prices Paid, and Fed’s Beige Book

Global Macro Updates

Stock and bond markets fell on Tuesday as the war with Iran intensified. Israel and the US hit targets across Iran, prompting Iranian retaliatory strikes around the Gulf including an attack on the US embassy in Riyadh, Saudi Arabia. Israel also attacked the Iranian-proxy group Hizbollah in Lebanon.

Oil prices continued to rise on Tuesday as Iran threatened to attack any vessel attempting to transit the Strait of Hormuz. As noted by CNBC, President Donald Trump said he had ordered the US International Development Finance Corporation to provide political risk insurance and financial guarantees for maritime trade traveling the Gulf. He also said the US Navy could begin escorting oil tankers through the Strait of Hormuz if necessary.

The primary mechanism through which the Middle East conflict benefits the US dollar is the ‘terms-of-trade’ shock. As a net exporter of petroleum and energy products, the US experiences a vastly different economic outcome from surging oil prices than its peers in Europe and Asia. For a net energy importer, a rise in oil prices functions as an external tax, draining domestic income and worsening the trade balance. Conversely, for the US, higher energy prices can support domestic production investment and trade surpluses in the energy sector, even if they pose a headline inflationary risk to consumers.

The dollar’s rise is self-perpetuating in an energy shock. Because global energy prices are denominated in USD, an increase in oil prices requires foreign central banks and corporations to acquire more dollars to settle transactions. This creates a dollar-energy spiral where the rising price of the commodity drives the exchange rate higher, which in turn increases the effective cost of energy for non-US economies, further damaging their growth prospects and weakening their currencies.

Inflation expectations provide an important transmission channel across asset classes. Oil‑driven upside surprises to headline CPI can delay or reduce the probability of rate cuts, particularly from a Fed already wary of re‑accelerating inflation. Higher or more persistent US policy rates relative to those in Europe and Japan widen rate differentials in favour of the dollar and mechanically support the currency via the carry channel. For fixed income, that mix argues for renewed outperformance of shorter‑dated US government bonds versus equivalent European or Asian paper, as markets price a shallower easing cycle in the US and a more aggressive response elsewhere.

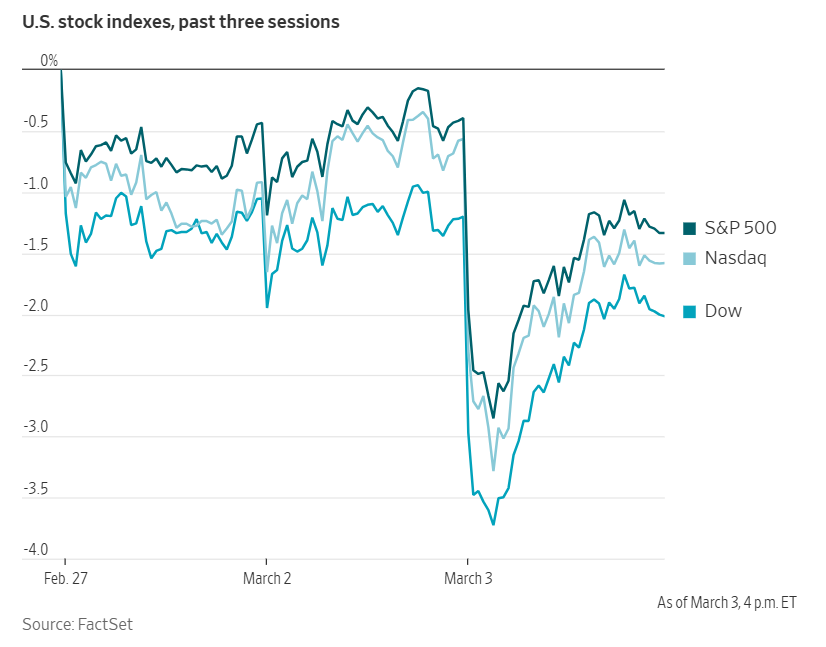

US Stock Indices

Dow Jones Industrial Average -0.83%

Nasdaq 100 -1.09 %

S&P 500 -0.94 %, with all of the 11 sectors of the S&P 500 down

Markets were down on Tuesday as the disruption to the Strait of Hormuz, a critical chokepoint that carries roughly 20% of the world's oil supply, raised the risk of an energy-driven inflation surge. Wall Street’s “fear gauge”, the VIX, hit its highest level in more than three months.

The S&P 500 closed the day -0.94% or down 64.99 points. The Dow Jones Industrial Average lost almost 1,300 points before paring its losses to 403.51 points, or -0.83%, to 48,501.27. The Nasdaq Composite lost 232.17 points, or -1.02%, to 22,516.69.

In corporate news, Apple updated its MacBook Air and MacBook Pro, adding faster processors and raising prices.

Intel announced that board Chair Frank Yeary plans to retire and current Intel board member and veteran chip executive Craig Barratt will succeed Yeary as chair after the company's annual shareholder meeting in May.

S&P 500 Best performing sector

Financials -0.18%, with Cboe Global Markets +2.33%, Erie Indemnity +2.03%, and JPMorgan Chase +0.91%

S&P 500 Worst performing sector

Materials -2.69%, with Newmont -7.75%, Albemarle -7.55%, and Freeport McMoRan -3.98%

Mega Caps

Alphabet -0.96%, Amazon +0.16%, Apple -0.37 %, Meta Platforms +0.23 %, Microsoft +1.35 %, Nvidia -1.33%, and Tesla -2.70%

Information Technology

Best performer: Workday +7.16%

Worst performer: Sandisk -8.67%

Materials and Mining

Best performer: CF Industries Holdings +1.92 %

Worst performer: Newmont -7.75 %

European Stock Indices

CAC 40 -3.46 %

DAX -3.44 %

FTSE 100 -2.75 %

Commodities

Gold spot -4.56% to $5,083.94 an ounce

Silver spot -8.48% to $81.85 an ounce

West Texas Intermediate +4.70% to $74.56 a barrel

Brent crude +4.71 % to $81.40 a barrel

On Tuesday gold prices were weighed down by a stronger dollar, rising bond yields and reduced expectations of a rate cut by the Fed this month.

Spot gold fell -4.56% to $5,083.94 an ounce. Spot silver fell -8.48% to $81.85 an ounce, hitting its lowest level since the 20th of February.

US WTI was +4.70%, or $3.33 to $74.56 a barrel for its highest settlement since June after rising more than 6% on Monday. Brent crude reached a session high of $85.12, marking its highest price since July 2024, before retreating after President Trump announced that the military campaign had neutralised numerous Iranian naval and air targets. Brent ended the day at $81.40 per barrel, +4.71%, or $3.66, on the day after a 6.7% rally in the prior session.

Amid escalating tensions in the Middle East, Israeli and US forces launched extensive strikes across Iran on Tuesday. These actions prompted swift Iranian retaliatory attacks throughout the Gulf region and led to the conflict spreading into Lebanon.

Iraq, the second-largest crude producer in OPEC, responded to the crisis by reducing its oil production by nearly 1.5 million barrels per day. As storage facilities approach capacity, these production cuts may more than double in the coming days, since the country is unable to export crude due to the ongoing conflict.

President Donald Trump stated that US and Israeli airstrikes were expected to last four to five weeks, but cautioned that the duration could extend further. He also noted that the US was considering support for oil tanker insurance in response to the rising threats.

The conflict’s impact on energy markets is global. India and Indonesia have begun seeking alternative energy sources, while some Chinese refineries have either shut down or expedited scheduled maintenance. Since hostilities commenced, Qatar has halted liquefied natural gas production, Israel has stopped output at select gas fields, and Saudi Arabia has closed its largest refinery.

To mitigate export disruptions, Saudi Aramco is attempting to reroute crude shipments through the Red Sea, circumventing the increasingly hazardous Strait of Hormuz where attacks have severely impeded shipping operations.

The crisis has driven US diesel futures up nearly 10%, reaching their highest levels since October 2023. US gasoline futures climbed almost 4%, rising to $2.46 per gallon, the highest since July 2024. Refining profit margins, measured by crack spreads, have soared to levels not seen since 2023.

Europe’s natural gas benchmark, TTF, surged by +43.3% to 62.09 euros per megawatt hour, following a +35.1% gain on Monday after QatarEnergy suspended all LNG production. The Henry Hub benchmark in the US rose +5.8% to $3.132.

Note: As of 4 pm EST 3 March 2026

Currencies

EUR -0.63% to $1.1613

GBP -0.34% to $1.3359

Bitcoin -2.16% to $67,937.94

Ethereum -3.70% to $1,967.97

The dollar climbed again on Tuesday, to reach multi-month peaks against the euro, sterling and yen as investors continued to seek out safe‑haven assets as the war in the Middle East spread and concerns around inflation rose.

The dollar index rose +0.53% to 99.04. The euro was down -0.63% to $1.1613, while the British pound weakened -0.34% to $1.3359.

The BoE is scheduled to convene later this month, with policymakers expressing differing views on whether to prioritise controlling inflation or fostering economic growth. Market participants currently estimate a 30% probability of an interest rate reduction, compared to a 75% likelihood observed on Friday.

The dollar strengthened +0.22% against the Japanese yen to ¥157.68.

Fixed Income

US 10-year Bond +3.2 basis points to 4.072%

German 10-year +5.5 basis points to 2.766%

UK 10-year gilt +9.6 basis points to 4.407%

US Treasury yields climbed for a second consecutive session on Tuesday, although they retreated from their earlier highs. The escalation of the conflict with Iran, continued to drive oil prices upward and intensified concerns about inflation.

New York Fed John Williams emphasised that it is premature to assess the war's effects on US inflation and economic growth. He noted, however, that the American economy is significantly less reliant on imported oil than in the past and has demonstrated resilience in the face of energy price fluctuations.

Minneapolis Fed President Neel Kashkari acknowledged that the conflict has increased uncertainty regarding the US economic outlook, thereby complicating the outlook for monetary policy.

Kansas City Fed President Jeffrey Schmid reiterated his opposition to further interest-rate reductions. He stated that the US labour market remains balanced and inflation remains elevated. While he did not specifically address the potential ramifications of the conflict in Iran, his comments suggest a cautious stance on monetary easing.

The two-year US Treasury yield, which typically reflects market expectations for Fed fund rates, was +2.5 bps to 3.506% from 3.481% late on Monday.

The yield on the US 10-year Treasury note was +3.2 bps to 4.072%. The 30-year bond yield was +2.9 bps to 4.706%.

The US Treasury yield curve, as measured by the spread between the two- and ten-year Treasury yields, stood at 61.2 bps.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing in 47.3 bps of cuts in 2026, lower than the 55.3 bps priced in the previous week. Fed funds futures traders are now pricing in a 2.6% probability of a 25 bps rate cut at the 18th March FOMC meeting, up from 2.5% a week ago.

The recent escalation of the US-Israeli air war against Iran has triggered a sharp two-day selloff in global government bonds, highlighting the strain on markets already anxious about inflationary pressures.

European government bonds experienced broad declines across all maturities and regions. In an interview with the Financial Times, ECB Chief Economist Philip Lane cautioned that a prolonged conflict in the Middle East could lead to a significant surge in eurozone inflation and dampen economic growth.

German bond yields reflected this volatility, with the two-year yield rising by +5.9 bps to 2.154%, reaching 2.236%, the highest level in a year and marking the largest two-day increase over the same period. At the longer end, the 30-year yield moved up by +2.3 bps to 3.382%.

Among European peers, Italy’s 10-year yield underperformed. It fell by -13.9 bps to 3.499%, widening the spread over German Bunds by 8.4 bps to 73.3 bps.

Europe’s heavy reliance on imported oil and gas has exacerbated market concerns. Energy prices have surged as shipping through the Strait of Hormuz has nearly come to a standstill.

As a result of these uncertainties, traders now assign a 17% probability to an ECB interest rate cut by year-end, a notable decline from approximately 40% last week.

Eurozone inflation rose more than expected last month, reaching 1.9% y/o/y. According to ECB analysis, a sustained spike in oil prices of this magnitude could increase inflation by 0.5 percentage points. Nevertheless, the ECB is expected to maintain that it is premature to determine the conflict’s full impact during its meeting later in March.

Note: As of 4 pm EST 3 March 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

本文提供给您仅供信息参考之用,不应被视为认购或销售此处提及任何投资或相关服务的优惠招揽或游说。金融工具交易存在重大亏损风险,未必适合所有投资者。过往表现并非未来业绩的可靠指标。

由专业人士创建。 为专业人士。