Can the ECB beat the vibecession?

What to look out for today

Companies reporting on Friday, 27th February: BASF, Holcim, International Consolidated Airlines Group

Key data to move markets today

EU: Spanish and German Harmonised Indices of Consumer Prices, German Unemployment Change and Unemployment Rate, Spanish, French and German CPI, French GDP, and a speech by Austrian National Bank Governor Martin Kocher

UK: A speech by BoE Chief Economist Huw Pill

US: PPI, Core PPI, and Chicago PMI

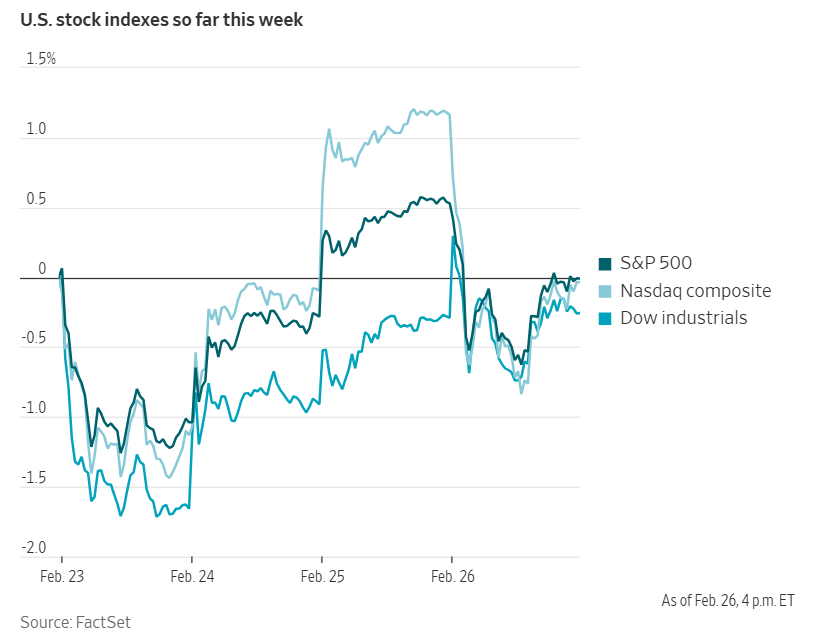

US Stock Indices

Dow Jones Industrial Average +0.03%

Nasdaq 100 -1.16%

S&P 500 -0.54%, with 7 of the 11 sectors of the S&P 500 down

Despite delivering another impressive earnings report on Wednesday evening, Nvidia’s shares declined in Thursday's trading session.

The world's largest publicly listed company reported record quarterly revenue of $68.127 billion, surpassing analysts' expectations and achieving its strongest growth rate in the past four quarters. Nevertheless, this performance did not prevent a -5.49% drop in Nvidia's stock price, which contributed to a -1.18% decline in the Nasdaq Composite.

The S&P 500 retreated by -0.54%, with technology stocks leading the downturn. Although the S&P 500 declined, approximately 350 of its constituent stocks finished higher. In contrast, the Dow Jones Industrial Average recorded a modest gain of +0.03%.

In corporate news, Paramount Skydance secured the acquisition of Warner Bros. Discovery after Netflix opted not to match the latest bid submitted by the David Ellison-led group for the prominent Hollywood company.

Accenture announced on Thursday that it had entered into a multi-year agreement with French startup Mistral AI. The partnership aims to assist enterprise clients, especially those in Europe, in adopting AI solutions.

S&P 500 Best performing sector

Financials +1.29%, with Nasdaq +5.48%, Fidelity National Information +4.04%, and Willis Towers Watson +3.86%

S&P 500 Worst performing sector

Information Technology -1.81%, with Dell Technologies -1.64%, KLA -1.45%, and Cadence Design Systems -1.40%

Mega Caps

Alphabet -1.88%, Amazon -1.29%, Apple -0.47%, Meta Platforms +0.51%, Microsoft +0.27%, Nvidia -5.49%, and Tesla -2.10%

Information Technology

Best performer: GoDaddy +8.95%

Worst performer: Corning -6.31%

Materials and Mining

Best performer: Newmont +2.10%

Worst performer: Albemarle -5.59%

Corporate Earnings Reports

Posted on Thursday, 26th February

Dell Technologies quarterly revenue +39.7% to $33.379 bn vs $31.672 bn estimate

EPS at $3.89 vs $3.53 estimate

David Kennedy, CFO, said, “We delivered record revenue of $33.4 billion in our fourth quarter, capping a record year for the company. Our strong execution drove record annual cash flow of more than $11 billion and record capital returned to shareholders of $7.5 billion. We have the portfolio, operating model and growing customer base to exceed our long-term growth targets in FY27, with expected revenue of $140 billion at the midpoint of our range and EPS growth of 25%.” — see report.

Vistra quarterly revenue +13.6% to $4.584 bn vs $5.789 bn estimate

EPS at $5.26 vs $2.60 estimate

Jim Burke, president and CEO, said, “I am proud of the 2025 performance of our Vistra team – this was truly a transformational year for our company. With our One Team mindset, we achieved several strategic milestones, including a 20-year power purchase agreement with AWS for up to 1,200 MW of carbon-free power at our Comanche Peak Nuclear Power Plant; the announcement and successful closing of our acquisition of the 2,600-MW gas portfolio from Lotus in just five months; commissioning of the 200-MW Oak Hill Solar Facility on our retired and reclaimed coal mine site, which includes a PPA also with AWS; significant construction progress at our Pulaski and Newton solar facilities in Illinois; execution of uprates across our Texas gas fleet; commencement of construction on two natural gas units totaling 860 MW at our Permian Basin plant, tripling its existing capacity; and TXU Energy becoming the top-rated large retail energy provider in the Texas Public Utility Commission rankings. In addition to this meaningful growth, the team also delivered a record year financially, further demonstrating the strength and consistency of our integrated business model.” — see report.

Coterra Energy quarterly revenue +40.4% to $1.959 bn vs $1.866 bn estimate

EPS at $0.39 vs $0.43 estimate

Tom Jorden, Chairman, CEO and President, said, “Coterra's strong fourth-quarter and full-year 2025 results were driven by efficient capital allocation and strong execution, and are a testament to the quality of our assets and the dedication and professionalism of our employees. Prioritizing safety, financial strength, and shareholder value creation, Coterra is well positioned for a highly capital efficient 2026. We are excited about the announced merger with Devon Energy and the opportunities created by the combined company. We remain focused on operational excellence and are preparing to integrate the two companies to unlock the value potential of the combined portfolio. This powerful combination builds directly on the foundation we have established, bringing together complementary assets and shared values, including rigorous economic evaluation, disciplined execution, and a common commitment to shareholder value creation.” — see report.

European Stock Indices

CAC 40 +0.72%

DAX +0.45%

FTSE 100 +0.37%

Commodities

Gold spot +0.37% to $5,183.81 an ounce

Silver spot -1.05% to $88.27 an ounce

West Texas Intermediate -0.15% to $65.47 a barrel

Brent crude -0.18% to $70.91 a barrel

Gold prices recorded a modest increase on Thursday due to uncertainty over US tariff policy. Spot gold rose by +0.37%, reaching $5,183.81 per ounce. Spot silver declined -1.05% to $88.27 per ounce.

Oil prices ended lower after a volatile trading session on Thursday, as investors closely monitored ongoing negotiations between the US and Iran regarding the OPEC member's nuclear programme. The market weighed potential supply risks, especially if tensions were to escalate.

Brent crude futures settled at $70.91 per barrel, down 13 cents or -0.18%. WTI futures closed at $65.47 per barrel, down 10 cents or -0.15%.

On Thursday, indirect negotiations between the US and Iran took place in Geneva with the aim of resolving their longstanding nuclear dispute and preventing conflict, following the US President’s order for increased military presence in the region.

Early in the session, oil prices rose by more than a dollar per barrel after media outlets reported that the discussions had stalled due to US insistence on zero uranium enrichment by Iran and the demand for delivery of all 60% enriched uranium to the US.

However, prices subsequently declined after both parties agreed to extend the negotiations into next week, easing immediate concerns over potential military action.

Iranian Foreign Minister Abbas Araqchi characterised Thursday’s meetings as the most substantive exchanges with the US to date, highlighting Iran’s clear articulation of its demands for the removal of sanctions and the process for obtaining relief. Araqchi confirmed that talks are scheduled to continue next week.

Oman’s Foreign Minister, Sayyid Badr Albusaidi, noted earlier that significant progress had been achieved during Thursday’s discussions.

Note: As of 4 pm EST 26 February 2026

Currencies

EUR -0.10% to $1.1797

GBP -0.56% to $1.3480

Bitcoin -2.12% to $67,474.22

Ethereum -3.34% to $2,030.53

The dollar index advanced by +0.14% to 97.79, while the euro edged -0.10% lower to $1.1797. Data released on Thursday revealed that the ECB had sold a portion of its dollar assets early last year, thereby reducing the dollar’s share in its foreign exchange reserves.

The British pound also weakened, falling -0.56% to $1.3480 against the dollar and slipping -0.10% versus the euro to 87.14 pence. Domestic political uncertainty continued to weigh on sterling, with market participants focusing on Thursday’s byelection in Manchester, which was widely seen as a significant test for Prime Minister Keir Starmer and the Labour Party.

The Japanese yen rebounded on Thursday after BoJ Governor Kazuo Ueda announced that any decision regarding interest rate increases at the central bank's upcoming March and April meetings would be guided by prevailing economic data. The yen appreciated by +0.15% against the US dollar, trading at ¥156.12 per dollar, after having touched a two-week low of ¥156.82 on Wednesday.

Governor Ueda emphasised that the BoJ stands ready to continue raising interest rates if Japan makes progress toward its economic and inflation targets. In contrast, a report earlier in the week indicated that Japanese Prime Minister Sanae Takaichi had voiced concerns about further rate hikes during its last meeting with Governor Ueda.

Fixed Income

US 10-year Bond -4.1 basis points to 4.008%

German 10-year -0.1 basis points to 2.700%

UK 10-year gilt -4.7 basis points to 4.276%

US Treasury prices advanced on Thursday as investors sought the safety of government bonds. This flight to quality pushed yields lower across the curve.

The 10-year Treasury yield declined -4.1 bps to 4.008% in afternoon trading, marking its lowest level since late November. Similarly, the 30-year yield fell -3.9 bps to 4.662%, reaching a trough not seen in over a week.

At the front end of the curve, the two-year yield, which closely tracks interest rate expectations, dropped -3.9 bps to 3.442%.

On the auction front, the US Treasury sold $44 billion in seven-year notes, with results broadly meeting market expectations. The auction cleared at 3.790%, nearly matching the anticipated rate at the bid deadline. The bid-to-cover ratio stood at 2.50x, slightly above the recent six-auction average of 2.46x.

Following the auction, seven-year Treasury yields fell an additional 4.0 bps to 3.772%.

The yield curve ended the day marginally flatter, with the spread between two-year and 10-year yields narrowing by 0.2 bps to 56.6 bps. Notably, the curve has flattened in 11 of the past 12 sessions, as short-term yields have risen relative to long-term Treasuries.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing in 55.0 bps of cuts in 2026, lower than the 59.5 bps priced in the previous week. Fed funds futures traders are now pricing in a 4.0% probability of a 25 bps rate cut at the 18th March FOMC meeting, down from 5.4% a week ago.

Eurozone government bond yields declined to multi-month lows on Thursday, reflecting a broad rally in the region’s fixed income markets.

Germany’s 10-year government bond yield dropped -1.0 bp to 2.700%, its lowest point since 28th November. The yield on Germany’s two-year bonds, sensitive to shifts in policy rate expectations, slipped -0.6 bps to 2.040%. The 30-year German yield fell -2.1 bps to 3.355%

Italy’s 10-year government bond yield decreased -0.5 bps to 3.303%. The yield spread between Italian bonds and Bunds stood at 60.3 bps.

Attention in the markets has now shifted to February inflation data from several eurozone countries, following confirmation that the bloc’s annual inflation rate for January was 1.7% as reported on Wednesday. Money market instruments continue to indicate that investors assign roughly a 30% probability to an ECB rate cut by December.

Note: As of 5 pm EST 26 February 2026

Global Macro Updates

Lagarde asserts inflation success, cautions on household sentiment. ECB President Christine Lagarde told lawmakers that the ECB has effectively brought inflation under control, noting that the headline Harmonised Index of Consumer Prices (HICP) registered at 1.7% in January compared to 2.0% in December 2025. She reiterated expectations for inflation to stabilise around the ECB’s 2% medium-term target. Nevertheless, President Lagarde highlighted an ongoing disconnect: households continue to perceive price increases as outpacing official measures. The ECB’s Consumer Expectations Survey (CES) for December 2025 revealed that the median perceived inflation rate over the past year stood at 3.2%, notably above the actual HICP figure of approximately 2.0%. This perception gap of 1.2 percentage points has persisted since 2020.

While forward-looking inflation expectations remain anchored, at 2.8% for the next 12 months and between 2.6% and 2.4% for the three to five-year horizon, this persistent perception bias may dampen consumer spending and drive higher wage demands. Recent German GfK data also stressed households’ preference for saving. The debate remains active, with some analysts cautioning about potential inflation undershoots, largely citing the euro’s recent appreciation and deflationary effects from low-cost Chinese imports.

The latest PMI surveys indicate that input cost inflation is accelerating at its fastest pace in more than two years.

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

本文提供给您仅供信息参考之用,不应被视为认购或销售此处提及任何投资或相关服务的优惠招揽或游说。金融工具交易存在重大亏损风险,未必适合所有投资者。过往表现并非未来业绩的可靠指标。

由专业人士创建。 为专业人士。