Fixed Income Briefing August 2023

- US GDP: Gross domestic product was revised from an initial reading of 2.4% down to an annual rate of 2.1% in the second quarter of 2023. The economy grew at a 2.0% pace in the January-March quarter.

- The US labour market showed some signs of weakening with payrolls dropping 177,00 last month and job openings at their lowest in over two years.

- Inflation accelerated with US headline inflation rising to 3.2% in July from June’s 3.0%.

- The Conference Board Consumer Confidence Index declined in August to 106.1 from a downwardly revised 114.0 in July.

- Flash PMIs in the US, UK and Eurozone were softer still in August. In the US the S&P Global US Composite PMI indicated only a fractional increase in output across the private sector midway through the third quarter. It was 50.4 in August, down from 52.0 in July. In the UK business activity continues to fall as the S&P Global/CIPS Flash UK Composite Output Index showed a drop to 47.9 in August, down from 50.8 in July. In the Eurozone the HCOB flash Composite PMI for the Eurozone dropped to its lowest level since November 2020, falling to 47.0, from 48.6 in July.

Yield curves

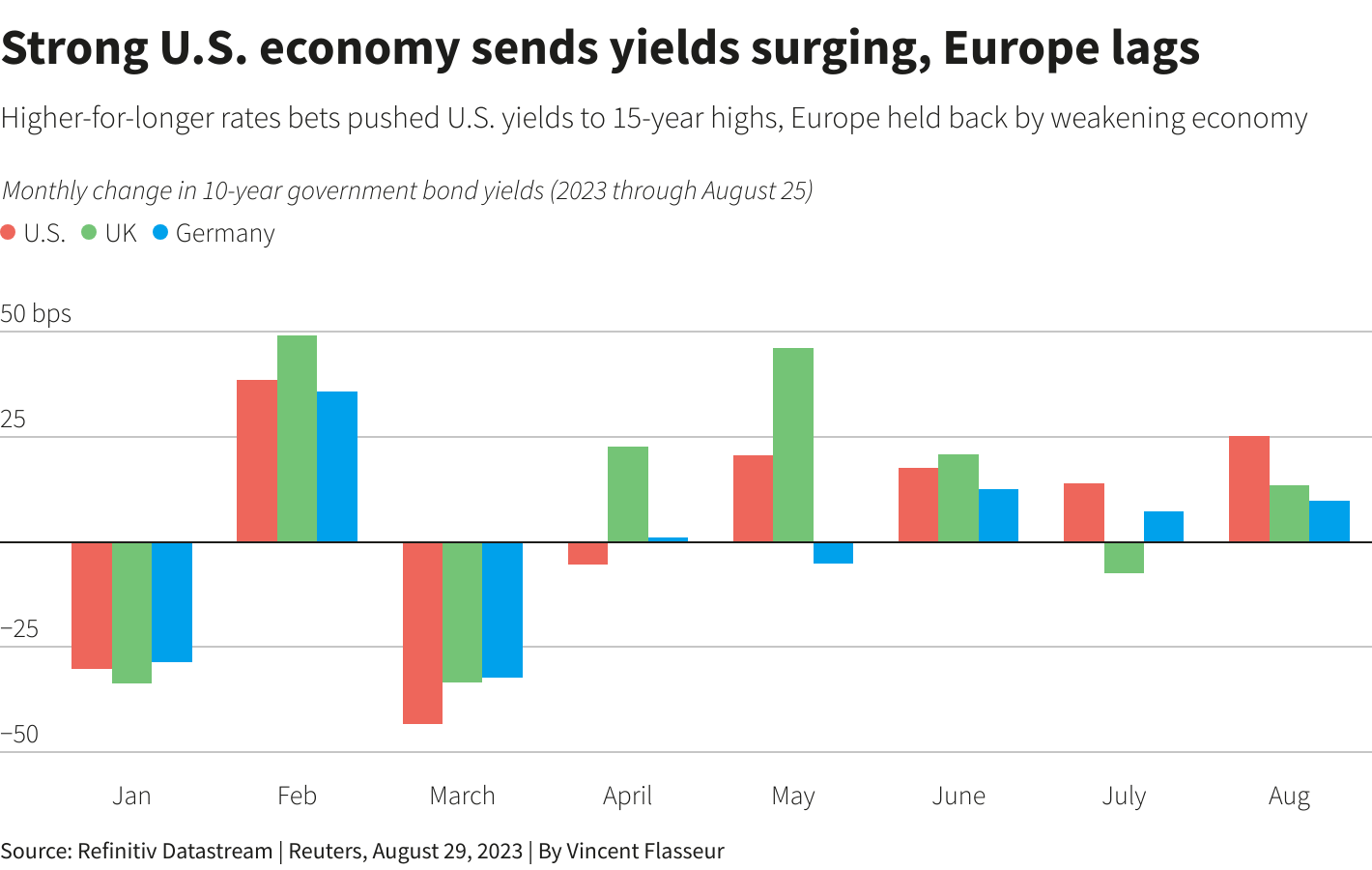

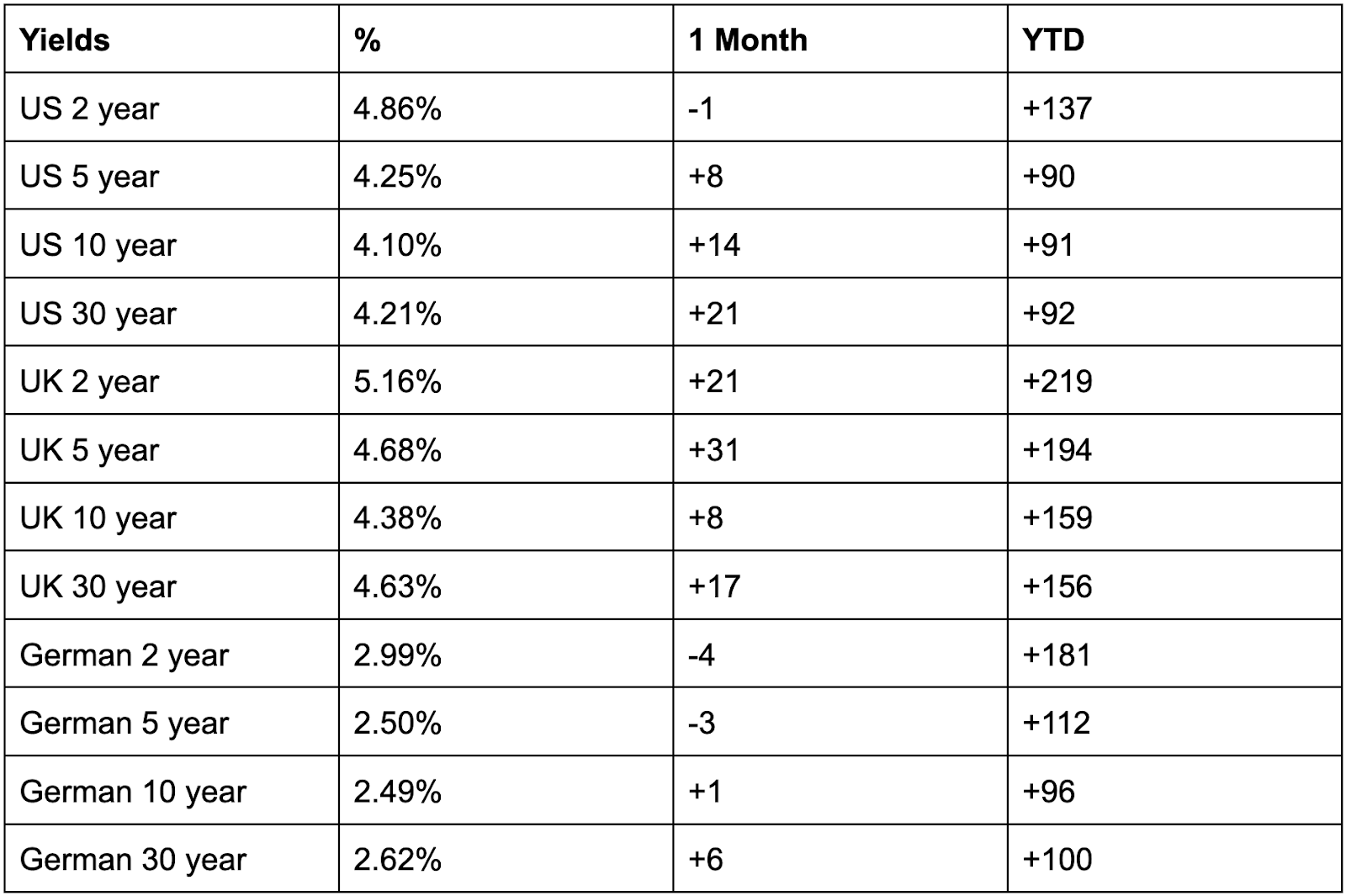

Rates across the US Treasury yield curve were up in August. The yield on the 2-year Treasury note, which is highly sensitive to expectations for the Fed Funds rate, is at 4.86%, up from 4.4% at the start of the year. The benchmark 10-year US Treasury note yield is at 4.10%, while the yield on the 30-year bond is at 4.21%.

A resilient US economy and rising borrowing needs pushed Treasury yields to their highest in over 15 years in August. There are growing expectations that interest rates will be paused but that they will be higher for longer. Fed Chair Jerome Powell reiterated during his speech at the Jackson Hole Economic Symposium in late August that inflation remains too high and that the Fed is prepared to raise rates further if appropriate, and that it intends to hold policy at a restrictive level until it is confident that inflation is moving sustainably down toward their objective.He emphasised that if economic growth remains strong, rates may need to increase further.

The US growth outlook remains positive but weaker despite consumer balance sheets still holding and solid levels of business investment. The labour market is softening but is still tight. Yields are likely to start to flatten out as we move into Autumn as the central banks get towards their peaks.

Source: Bloomberg 6:30 am EDT 31 August 2023

Global Economic and Market Review

In the UK, the inflation story improved in July as headline inflation came in at 6.8% in July. Despite a slowdown in headline inflation, core remained at 6.4% in July, the same as in June. Economic growth has decelerated with Composite PMI falling to 47.9, the lowest since January 2021. It was also the first time the UK index had dipped below the 50.0 level – which separates economic expansion from contraction – for six months. However, despite the slowing economy and rising worries over a declining housing market with mortgage rate approvals falling by nearly 10% between June and July, the Bank of England is widely expected to keep the tightening throttle on at its meeting in September and to raise rates another 25 basis points.

The ECB has said it will maintain its tightening course, however, markets are now anticipating that the ECB is near the peak of its tightening cycle. There are still potential headwinds including a rise in food and energy inflation due to geopolitical events and poor weather conditions. According to Worldgovernmentbond.com, the spread between Germany’s 10 Year and Italy’s 10 year is 163,3, down only 1 basis point this month. Germany’s spread vs the US is -158.3 basis points.

It is clear that differences in domestic interest rate paths that may emerge in September will continue to drive yields. The ECB and the BoE continue to face stickier inflation and greater structural issues, so despite slowing growth, may be more likely to sustain their hiking cycle into the Autumn. Another driver of yields will be borrowing needs with the US fiscal outlook deteriorating. Fitch Ratings, which lowered the US credit rating in early August citing fiscal pressures, expects the US government deficit to rise to 6.3% of GDP this year, and 6.6% next year, from 3.7% in 2022, and widen further thereafter. In Germany, Fitch forecasts the deficit will rise to 3.1% of GDP this year from 2.6% last year, but narrow to around 1% in the longer term. Lower debt issuance in Europe would favour European government bonds over Treasuries as larger fiscal deficits require more borrowing, resulting in higher interest rates and lower bond prices.

Key risks

Markets are anticipating that the Fed and the ECB will hit the pause button in September. Short-dated government bonds, which are subject to higher levels of volatility, are offering higher yields, which, if interest rates remain on course with expectations, should offer attractive income with limited risk. However, if core inflation, particularly in Europe and the UK, remains high, bond prices could still weaken if the ECB feels it needs to continue tightening well into the Autumn. Only if inflation continues to decelerate in line with ECB and Fed forecasts will the middle area (five to 10 years) of the curve become more attractive.

- Inflation fails to fall in line with projections, weighing on asset prices. If US core inflation does not fall as anticipated by the Fed, this will raise the risk of further tightening and may cause interest-sensitive stocks in the technology sector, financials, telecommunications, and infrastructure to decline.

- Policymakers actions lead to over tightening credit conditions. There are once again growing fears of stagnation in the UK and even in Europe as core inflation remains high due to still rising services sector wages and business activity is in decline.

- Geopolitical flare-ups and Climate change. Beyond the situation in Ukraine and the rising internal political conflict support for Ukraine it is causing in the US, other geopolitical issues surrounding China may emerge during September’s ASEAN meeting in Indonesia. There is also the still difficult Iran/US situation to consider and Turkey’s relationship with Europe.

DISCLAIMER: This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here.

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

本文提供给您仅供信息参考之用,不应被视为认购或销售此处提及任何投资或相关服务的优惠招揽或游说。金融工具交易存在重大亏损风险,未必适合所有投资者。过往表现并非未来业绩的可靠指标。

由专业人士创建。 为专业人士。