Are UK markets bracing for a fiscal storm?

What to look out for today

Companies reporting on Tuesday, 12 May: Qnity Electronics, Zebra Technologies

Key data to move markets today

EU: German Harmonised Index of Consumer Prices, German ZEW Current Economic Situation and Economic Sentiment Surveys, Eurozone Economic Sentiment Survey and a speech by ECB Executive Board member Frank Elderson

USA: CPI, Monthly Budget Statement and speeches by New York Fed President John Williams and Chicago Fed President Austan Goolsbee

Global Macro Updates

UK political uncertainty. UK gilts underperformed other G7 benchmarks, with yields rising 9.2 bps on Monday. The 10-year yield moved back into the 5.00% area after easing late last week from an 18-year high of 5.10%. Political risk remained a key driver following local elections in which the ruling Labour party lost badly, alongside ongoing concerns about the potential economic impact of the Iran war.

Prime Minister Keir Starmer delivered a keynote speech defending his record and reiterated that he would not step down. He framed a ‘reset’ around a closer relationship with the EU, announced plans to nationalise British Steel and pledged additional support for youth employment. While details were limited, he did not entirely rule out the possibility of the UK joining the EU single market and customs union. He said the next summit on trade, the economy, defence and security would provide a platform to build on.

Rebel MP Catherine West, who had threatened to trigger a leadership challenge, backed down, but called for Starmer to leave by September. Former Deputy Prime Minister Rayner reiterated that change was needed and said it was a mistake to block Manchester Mayor Andy Burnham from standing as a member of parliament (MP). Prior to last week’s local election, multiple reports suggested MPs were coalescing around Burnham as the strongest candidate to win a general election. A longer timetable for Starmer’s departure would be more conducive to a Burnham leadership bid amid reports that Labour-left MPs were concerned an early leadership move by Health Secretary Wes Streeting could have blocked Burnham. Four ministerial aides also resigned, including allies of Wes Streeting. The Prime Minister is expected to signal his intention today. Dozens of Labour MPs have joined calls for him to deliver a timetable for his departure.

Investors appear focussed on the potential direction of fiscal policy, as a more left-leaning administration could favour higher taxes alongside increased spending and borrowing.

April CPI preview. April CPI data will be released at 08:30 ET. Consensus expects headline CPI to rise 0.6% m/o/m after a 0.9% increase in March, lifting the y/o/y rate to 3.7% from 3.3%. Core CPI is forecast to increase 0.3% m/o/m following a 0.2% gain in March, taking the y/o/y rate to 2.7% from 2.6%.

Previews again point to higher energy prices linked to the conflict in Iran as the primary source of upside pressure on headline inflation, particularly through gasoline. Some also expect firmer food prices, citing higher fertiliser costs and energy-related inputs after a flat reading in March.

On core inflation, previews highlight the potential for a firmer shelter reading (roughly double), reflecting a one-off effect related to last year’s government shutdown. Stripping out that impact, they argue the underlying shelter trend should continue to signal gradual disinflation.

Airfares are another frequently cited upside risk amid the surge in jet fuel costs. Previews also discuss potential tariff pass-through, although some firms expect that impulse to moderate. Used car prices appear to be the most contested component, given the recent lag between CPI measures and auction-price indicators.

US Stock Indices

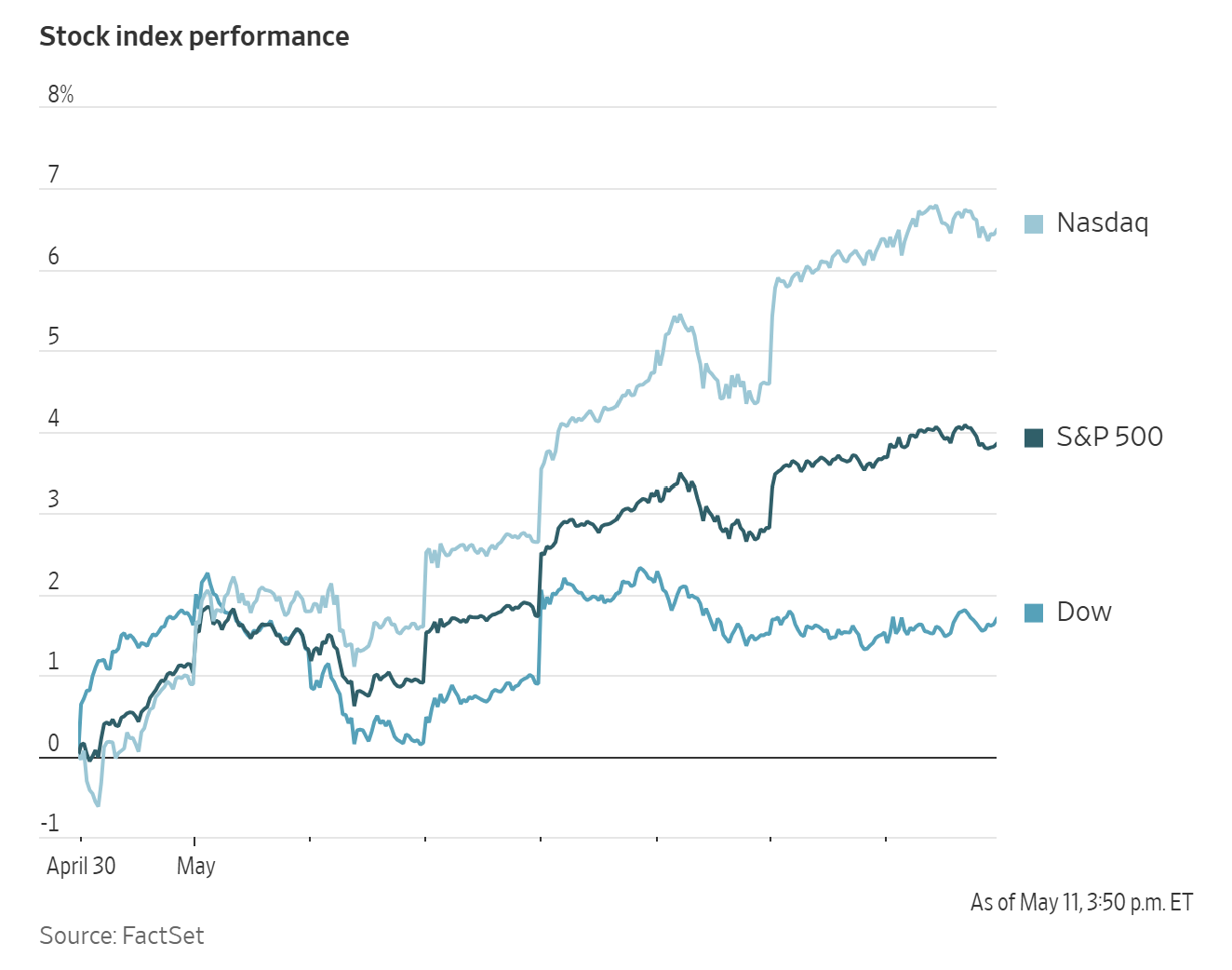

Dow Jones Industrial Average +0.19%

Nasdaq 100 +0.29%

S&P 500 +0.19%, with 6 of the 11 sectors of the S&P 500 up

US equities edged to fresh record highs on Monday, supported by gains in energy stocks and renewed enthusiasm for the AI theme. The S&P 500 rose +0.19% to a new all-time high. The Nasdaq Composite also set a record, adding +0.10%, while the Dow Jones Industrial Average gained +0.19%, or about 95.31 points.

Cerebras Systems increased the size of its IPO and is now seeking to raise up to $4.8 billion, as demand for the AI chipmaker and data-centre operator’s shares continues to build.

KKR is committing $300 million to a private credit fund it manages with Future Standard, as performance continues to deteriorate.

Barrick Mining said it will repurchase up to $3 billion of its shares, as the world’s third-largest gold producer seeks to bolster investor support ahead of the planned spinoff of its North American assets later this year.

Circle Internet Group shares rose on optimism surrounding the stablecoin issuer’s ARC blockchain initiative and as US lawmakers moved closer to considering a landmark digital-asset bill.

S&P 500 Best performing sector

Energy +2.63%, with Occidental Petroleum +3.98%, Diamondback Energy +3.95% and Exxon Mobil +3.53%

S&P 500 Worst performing sector

Communication Services -2.33%, with Charter Communications -4.57%, Match Group -3.22% and Walt Disney -3.05%

Mega Caps

Alphabet -2.59%, Amazon -1.59%, Apple -0.20%, Meta Platforms -1.77%, Microsoft -0.58%, Nvidia +1.96% and Tesla +3.89%

Information Technology

Best performer: Corning +10.94%

Worst performer: Super Micro Computer -5.23%

Materials and Mining

Best performer: CF Industries +8.22%

Worst performer: International Flavors & Fragrances -2.84%

Corporate Earnings Reports

Posted on Monday, 11 May

Circle Q1 2026 earnings, posting total revenue and reserve income of $694 mn vs $720.8 mn estimate, adjusted EBITDA of $151 mn vs $137.9 mn estimate, and EPS topping consensus. Stablecoin market share hit 28% vs 27.8% estimate, average USDC in circulation reached $75.2 bn vs $75.87 bn estimate, with year-end 2026 USDC circulation guidance at $77 bn.

Constellation Energy reported Q1 2026 adjusted operating EPS of $2.74 vs $2.53 estimate, with operating revenue of $11.12 bn vs $8.57 bn estimate. The company reaffirmed its FY 2026 adjusted operating EPS guidance of $11.00 to $12.00, against consensus of $11.53.

Monday.com Q1 revenue of $351 mn vs $339 mn estimate and EPS of $1.15 vs $0.88 expected, with FCF at $103 mn vs $88 mn forecast, RPO at $880 mn, up 33% y/o/y and customers over $100K ARR at 1,844, up 39% y/o/y. FY26 guidance raised to revenue $1.47 bn vs $1.46 bn expected and operating margin 13% vs 12% prior. Company launched AI Work Platform with native agents. CFO noted Q1 strong across financials ahead of expectations and AI productivity gains enabling revenue growth without proportional headcount increase for operating leverage.

Hims & Hers Health Q1 revenue of $608 mn vs $618 mn consensus, EPS of -$0.40 vs $0.02 estimate, EBITDA of $44 mn vs $46 mn estimate and gross margin of 65% vs 72% estimate, while subscribers met at $2.6 mn. Q2 guidance includes revenue of $690 mn vs $645 mn estimate and EBITDA of $45 mn vs $70 mn estimate. FY26 guidance raised revenue to $2.9 bn beating $2.8 bn estimate and EBITDA to $315 mn vs $319 mn estimate. Company reiterated 2030 targets of at least $6.5 bn revenue and $1.3 bn adjusted EBITDA with high conviction.

AST Space Mobile Q1 revenue of $15 mn vs $37 mn estimate and EPS of ($0.66) vs ($0.20). Cash position remained at $3.5 bn. Issued 2026 revenue guidance of $175 mn vs $181 mn estimate and reaffirmed target of 45 satellites by year-end 2026. Confirmed mid-June SpaceX Falcon 9 launch for BlueBird 8, 9 and 10, with BlueBird 11-33 in advanced assembly and 32 next-gen Block 2 satellites in production. Expanded Texas manufacturing capacity for Micron satellites, added three new U.S. government awards, expanded launch optionality and achieved 98.9 Mbps peak download speed to unmodified smartphone using Block 1 satellites.

Plug Power reported earnings with EPS of -$0.18 vs -$0.10 estimate and revenue of $163 mn vs $139 mn expected.

MARA Holdings reported earnings with EPS of -$3.31 vs -$2.30 estimate and revenue of $174 mn vs $184 mn estimate.

European Stock Indices

CAC 40 -0.69%

DAX +0.05%

FTSE 100 +0.36%

Commodities

Gold spot +0.42% to $4,734.16 an ounce

Silver spot +7.17% to $86.09 an ounce

West Texas Intermediate +3.77% to $98.25 a barrel

Brent crude +3.85% to $104.35 a barrel

Gold prices reversed earlier declines to edge higher on Monday amid volatile trading conditions.

Spot gold rose +0.42% to $4,734.16 per ounce, after having fallen more than one percent earlier in the session.

Shares of Indian jewellery retailers declined after Prime Minister Narendra Modi urged consumers to refrain from purchasing gold for a year to help protect foreign-exchange reserves. India is the world’s second-largest gold consumer.

Spot silver advanced +7.17% to $86.09 per ounce.

Oil prices settled more than three percent higher on Monday after the US President Donald Trump said the ceasefire with Iran was ‘on life support,’ leaving the Strait of Hormuz largely closed and offering no clear indication of when the conflict might end.

Brent crude futures rose $3.87, or +3.85%, to settle at $104.35 a barrel, while US WTI gained $3.57, or +3.77%, to close at $98.25. Brent touched an intraday high of $105.99 and WTI peaked at $100.37.

OPEC crude output fell by 830,000 bpd month over month to 20.04 million bpd in April, its lowest level since at least 2000 and below the 2020 COVID-era troughs, according to a Reuters survey. The US-Israeli war with Iran has kept the Strait of Hormuz effectively closed and prompted export curtailments.

March output was also revised down by 700,000 bpd following a change in a Saudi estimate. Kuwait recorded the largest decline, reflecting a full month of export disruptions, while Saudi Arabia and Iraq also posted lower production. The UAE (which exited OPEC effective 1 May) was the only Gulf member to increase output, supported by its Hormuz-bypassing export route. Venezuela and Libya also added barrels.

Aramco CEO Amin Nasser added on Monday that the market could lose approximately 100 million barrels per week if disruptions in Hormuz persist at the current pace. He said demand rationing is likely to continue while supply remains constrained, but expects a ‘very robust return to demand growth’ once trade and shipping normalise.

Kpler shipping data showed that three crude tankers exited the strait last week and on Sunday with tracking systems switched off. One vessel was loaded with Iraqi crude bound for Vietnam.

Note: As of 4 pm EDT 11 May 2026

Currencies

EUR -0.02% to $1.1782

GBP -0.21% to $1.3604

Bitcoin +1.93% to $81,799.55

Ethereum +1.12% to $2,340.15

The dollar traded modestly higher on Monday.

The dollar index inched up +0.06% to 97.91 after reaching an intraday high of 98.15, while the euro slipped -0.02% to $1.1782.

Sterling fell -0.21% to $1.3604, as UK Prime Minister Keir Starmer faced renewed political pressure after three ministerial aides resigned and more than 60 Labour lawmakers publicly called for his resignation.

Against the Japanese yen, the dollar rose +0.29% to ¥157.10.

Fixed Income

US 10-year Bond +5.4 basis points to 4.413%

German 10-year Bund +3.6 basis points to 3.043%

UK 10-year gilt +9.2 basis points to 5.004%

US Treasury yields rose across the curve on Monday after the US President swiftly rejected Iran’s response to a US peace proposal, lifting oil prices and reviving concerns about a renewed pickup in inflation.

The 2-year note yield, which closely tracks Fed fund rate expectations, rose +7.1 bps to 3.966%.

The 10-year yield increased +5.4 bps to 4.413%, and the 30-year yield rose +5.3 bps to 4.989%.

This week’s primary economic focus is consumer and producer price inflation, due Tuesday and Wednesday, respectively. They will be monitored closely for evidence that higher oil costs are feeding through into broader prices.

The Treasury saw soft demand at Monday’s $58 billion auction of three-year notes, the first sale in a $125 billion slate of coupon-bearing supply this week. The notes priced at a yield 0.5 bps above pre-auction trading levels, and the bid-to-cover ratio was 2.51x, the weakest since July.

The Treasury will also auction $42 billion in 10-year notes on Tuesday and $25 billion in 30-year bonds on Wednesday.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing 0.0 bps of rate hikes in 2026, lower than the 8.0 bps priced in a week ago. Fed funds futures traders are now pricing in a 0.0% probability of a 25 bps rate cut at June’s FOMC meeting, lower than last week’s 5.9% probability.

Eurozone yields rose on Monday across the maturity spectrum.

Germany’s rate-sensitive 2-year government bond yield rose +5.6 bps to 2.654%, with markets close to fully pricing in a ECB rate hike at its June meeting.

Markets have fully priced two 25 bps hikes across the ECB’s three meetings through September and see roughly a 75% chance of a third increase by year-end.

Germany’s 10-year yield rose +3.6 bps to 3.043%, while the 30-year yield advanced +2.9 bps to 3.572%.

ECB policymakers have said they stand ready to respond if elevated energy prices begin to spill over into broader inflation. Governing Council member Martin Kocher said in an interview published on Monday that “if the situation does not improve significantly, there will be no avoiding an interest rate move in the near future.”

“What is clear is that if the war drags on and energy prices remain high, the risk of second-round effects will increase,” Kocher added.

Other eurozone yields largely moved in line with Germany’s. Italy’s 10-year yield rose +5.6 bps to 3.788%, leaving the spread to Germany at 74.5 bps.

Investors also remained focused on the UK, where speculation is building over a potential leadership challenge to Prime Minister Keir Starmer. Britain’s 10-year yield rose +9.2 bps to 5.004%.

Note: As of 4 pm EDT 11 May 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

本文提供给您仅供信息参考之用,不应被视为认购或销售此处提及任何投资或相关服务的优惠招揽或游说。金融工具交易存在重大亏损风险,未必适合所有投资者。过往表现并非未来业绩的可靠指标。

由专业人士创建。 为专业人士。