Will tech deliver the beat?

What to look out for today

Companies reporting on Tuesday, 28 April: Booking Holdings, BP, Centene, Coca-Cola, Corning, Ecolab, Fair Isaac, General Motors, Novartis, Mondelez International, Robinhood Markets, Sherwin-Williams, Spotify, Starbucks, Teradyne, UPS, Visa, Waste Management

Key data to move markets today

JAPAN: Unemployment Rate and BoJ Interest Rate Decision, Monetary Policy Statement, Outlook Report and Press Conference

EU: ECB Bank Lending Survey and a speech by ECB President Christine Lagarde

USA: ADP Employment Change 4-week average, Housing Price Index and Consumer Confidence

Global Macro Updates

Reporting week: can tech save the day? The peak week of Big Tech earnings arrives against the backdrop of a powerful rally in US equities, led predominantly by the technology sector. In recent weeks, investor positioning has increasingly reflected confidence in the durability of the AI-driven growth cycle, with hyperscalers at the centre of both, earnings expectations and capital allocation narratives. This strength, however, also raises the bar meaningfully into results, setting up a potential inflection point where strong prints may be required simply to sustain current valuations.

At the core of the debate is the unprecedented scale of investment. Alphabet, Meta, and Microsoft are collectively expected to deploy in excess of $400 billion in CapEx in 2026, with total hyperscaler AI-related capex approaching or exceeding $600 billion when including Amazon. The key question for markets is no longer whether AI demand is real, but whether revenue monetisation is materialising quickly enough to justify the pace and magnitude of this spend. Recent data points offer partial validation: Microsoft has guided Azure y/o/y growth of 37% to 38% for Q1, moderating slightly from prior quarters; Alphabet’s Google Cloud delivered 48% y/o/y growth; and Meta continues to demonstrate improving ad monetisation through AI-driven tools. Together, these serve as critical proof points, but also highlight that expectations are already calibrated to strong outcomes.

Earnings this week, beginning with Amazon, Alphabet, Microsoft, and Meta on 29 April, followed by Apple on 30 April, will therefore be less about confirming strength and more about exceeding an increasingly demanding threshold. AI demand trends remain central, with hyperscalers reporting unprecedented inflection in GPU and compute demand. However, investor scrutiny has intensified, particularly around AWS and Google Cloud, where expectations for sustained acceleration are elevated. At the same time, CapEx remains firmly in focus. Industry commentary points to continued upside risk in spending plans, supported by strong chip-related revenue growth and rising compute demand, reinforcing the view that returns on AI investment remain attractive, though increasingly back-end loaded.

Within this context, dispersion across names could prove decisive. Microsoft faces a high bar for Azure, where even modest deceleration could trigger debate around near-term digestion in AI demand. Meta’s substantial CapEx commitments have drawn mixed reactions, with some investors questioning the visibility of near-term returns relative to hyperscalers, despite evidence of improving monetisation. Amazon’s AWS trajectory will be closely watched for confirmation that enterprise AI adoption is translating into sustained revenue acceleration. Apple, meanwhile, introduces a different dimension, with expectations centred on an AI-driven upgrade cycle, though meaningful strategic updates are likely deferred to its June developer conference.

From a market perspective, the implications are asymmetric. A broad-based ‘triple beat’ across Alphabet, Meta and Microsoft, particularly on cloud growth, would reinforce the AI infrastructure thesis, validate current CapEx trajectories and likely extend valuation support across the broader ecosystem, including semiconductors and equipment providers. However, anything short of this, whether through marginal cloud deceleration, softer guidance, or increased uncertainty around monetisation timelines, could catalyse a shift in narrative toward a digestion phase.

Given the magnitude of the recent rally and the concentration of gains in AI-linked equities, the setup increasingly resembles a classic ‘sell-the-news’ dynamic. Even fundamentally strong results may struggle to drive incremental upside unless they decisively exceed already elevated expectations. As such, this earnings cycle is less about proving the AI story and more about determining whether current valuations have already priced in much of that optimism.

BoJ maintains policy rate, communicates a hawkish outlook. As widely anticipated, the BoJ kept its policy rate unchanged at 0.75%. The key highlight of this meeting was the 6-3 vote split, an uncommon level of dissent, with all three dissenting members advocating for a 25 bps rate hike.

Board members Hajime Takata, Naoki Tamura and Junko Nakagawa all called for a hike to 1%. Takata stated that the price stability target had been largely achieved and that risks to inflation were increasingly tilted to the upside due to international factors.

Tamura, who had previously supported holding rates steady since the December rate hike, returned to a hawkish position. He echoed concerns that inflation risks were significantly skewed to the upside and recommended moving the policy rate closer to a neutral level.

Nakagawa, the new dissenter, also emphasised that inflation risks remain tilted upward, even under continued accommodative financial conditions and despite uncertainties in the Middle East.

The April Outlook Report revealed substantial adjustments to Japan’s economic forecasts, primarily due to higher crude oil prices. There were significant upward revisions to core CPI inflation, now projected at 2.8% for fiscal year 2026 (up from 1.9%) and 2.3% for fiscal year 2027 (up from 2.0%). While the press had anticipated an upgrade, the extent of these changes had not been clear.

Projections for inflation excluding fresh food and energy were also raised, indicating levels will remain in the upper 2% range through fiscal year 2028. Conversely, GDP forecasts were revised downward, with fiscal year 2026 growth cut in half to 0.5%.

The BoJ described risks to its forecasts as being skewed to the upside for inflation and to the downside for growth, particularly in fiscal year 2026. The bank underscored the need for vigilance regarding the potential realisation of upside inflation risks.

This assessment aligns with the dot plot, showing that seven out of nine board members perceive upside risks to inflation for fiscal years 2026 and 2027. Meanwhile, a majority of five members expect downside risks to GDP growth in fiscal year 2027, with the outlook for that year considered balanced.

Domestic economic fundamentals are anticipated to remain constructive. Headwinds stemming from the Middle East are expected to slow growth momentum but not derail the overall recovery. Key support factors include government policy, accommodative financial conditions and robust corporate profits, with the virtuous wage-price cycle projected to persist. The BoJ reaffirmed its commitment to achieving the price stability target from the second half of fiscal year 2026 through fiscal year 2027, updating its language to reflect the inclusion of fiscal year 2028 in the forecast horizon.

Forward guidance was explicitly maintained, emphasising a continued stance toward rate hikes as underlying inflation approaches 2% and real interest rates remain significantly low. The BoJ simplified its language to convey that policy rates will continue to rise in response to economic and financial developments, with the timing and pace of adjustments dependent on ongoing monitoring of global risks, particularly those related to the Middle East.

US Stock Indices

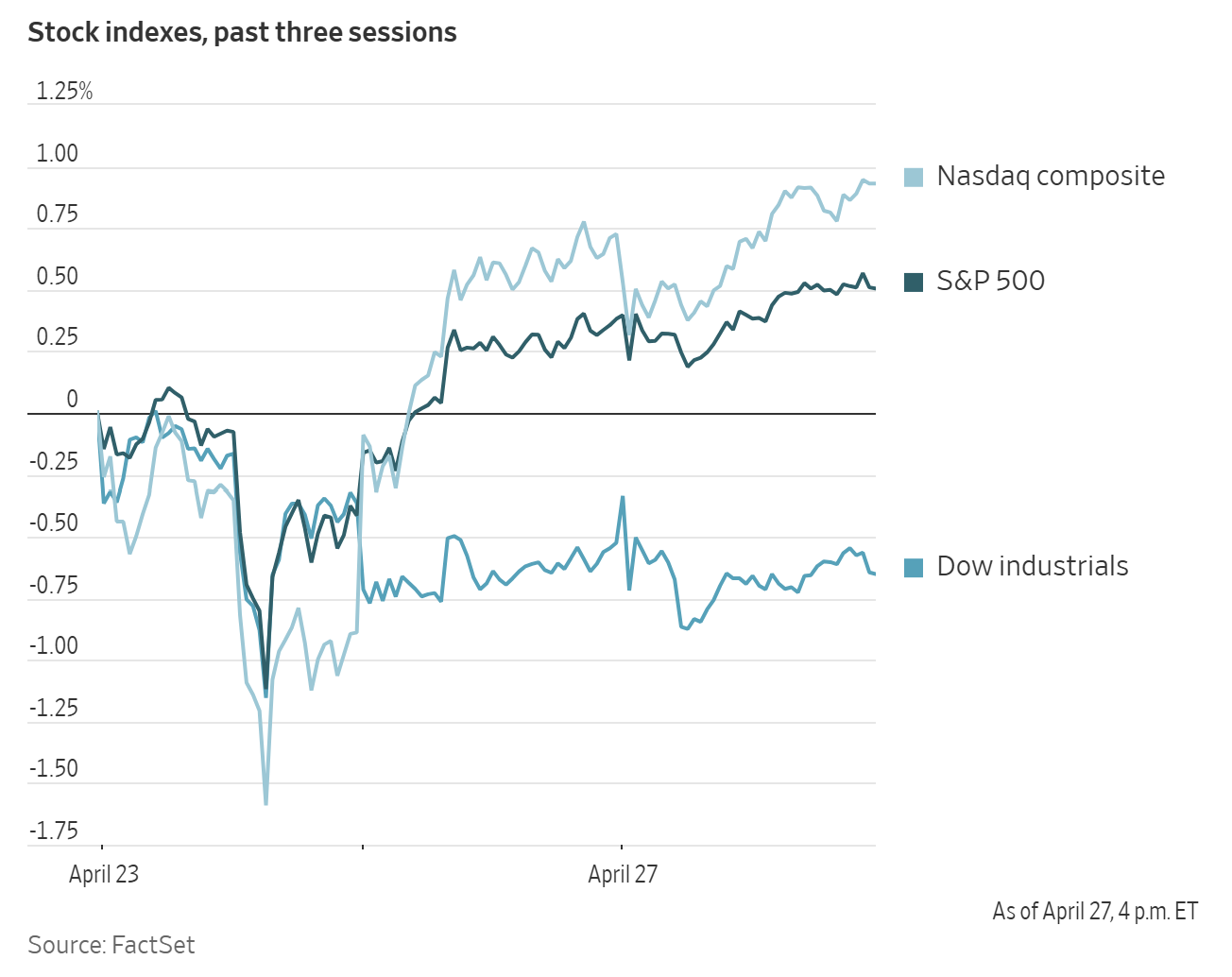

Dow Jones Industrial Average -0.13%

Nasdaq 100 +0.01%

S&P 500 +0.12%, with 3 of the 11 sectors of the S&P 500 up

In muted trading on Monday, the S&P 500 still managed to rise +0.12% to 7,173.91 points, keeping it on track for its best monthly performance since 2020. The Dow Jones Industrial Average fell 62.67 points or -0.13% to 49,168.04 points, while the Nasdaq Composite was +0.20% or up 50.50 points to 24,887.10.

In corporate news, Microsoft and OpenAI have agreed to drop Microsoft’s exclusive right to sell the startup’s AI models, although Microsoft remains as OpenAI's primary cloud partner with a licence to the startup's intellectual property through 2032. The change to the previous agreements means that OpenAI can pursue deals with other cloud-computing developers like Amazon Web Services.

In one of the biggest deals by an Indian company, Sun Pharmaceutical Industries has agreed to acquire New York-listed women’s health-care company Organon & Co.

S&P 500 Best performing sector

Communication Services +0.94%, with EchoStar +3.51%, Applovin +2.68% and Alphabet +1.81%

S&P 500 Worst performing sector

Consumer Staples -1.18%, with Keurig Dr Pepper -3.66%, Hershey -2.61% and Brown-Forman -2.54%

Mega Caps

Alphabet +1.72%, Amazon -1.09%, Apple -1.27%, Meta Platforms +0.53%, Microsoft +0.05%, Nvidia +4.00% and Tesla +0.63%

Information Technology

Best performer: Sandisk +8.11%

Worst performer: Corning -4.48%

Materials and Mining

Best performer: Albemarle +5.95%

Worst performer: Newmont -3.83%

Corporate Earnings Reports

Posted on Monday, 27 April from The Pulse, our real-time AI-driven news tool. Available exclusively on the EXANTE Web Platform

Verizon reported Q1 adj EPS $1.28 vs est $1.21 beat, operating revenue $34.44 bn vs $34.8 bn est miss, business revenue $7.42 bn in line, consumer revenue $26.45 bn vs $26.63 bn est miss, adj EBITDA $13.4 bn vs $13.14 bn est beat. Total postpaid phone net additions 55,000, core prepaid 115,000. Raised FY adj EPS guidance to $4.95-$4.99 from prior $4.90-$4.95, reaffirmed FY FCF at least $21.5 bn, cash flow from ops $37.5B-$38 bn, capex $16 bn-$16.5 bn. CEO stated multi-billions potential from AI support; in discussions with hyperscalers to integrate fiber and 5G assets for AI infrastructure.

Domino's reported Q1 2026 results before open, with global retail sales up 3.4% ex-FX, US same-store sales up 0.9%, and international same-store sales down 0.4%. CEO noted positive US order count and market share growth.

European Stock Indices

CAC 40 -0.19%

DAX -0.19%

FTSE 100 -0.56%

Commodities

Gold spot -0.57% to $4,681.85 an ounce

Silver spot -0.24% to $75.50 an ounce

West Texas Intermediate +2.58% to $97.33 a barrel

Brent crude +2.26% to $108.29 a barrel

On Monday, gold prices declined as investors closely monitored the ongoing conflict in the Middle East and the stalled peace negotiations between Washington and Tehran.

Spot gold decreased -0.57%, reaching $4,681.85 per ounce.

Spot silver also fell, declining -0.24% to $75.50 per ounce.

Oil prices advanced by over two percent on Monday, extending their gains from the previous session. This increase was driven by stalled efforts to resolve the US-Iran conflict, which has resulted in the prolonged closure of the critical Strait of Hormuz.

Brent crude futures for June delivery rose by $2.39, or +2.26%, closing at $108.29 per barrel—the highest settlement since 7 April. This marks the contract’s sixth consecutive day of gains. Similarly, US WTI crude for June climbed $2.45, or +2.58%, to reach $97.33 per barrel.

Ship-tracking data indicated substantial disruptions in the region, with six Iranian oil tankers compelled to turn back due to the ongoing US blockade.

Nonetheless, ship-tracking data also showed that a liquefied natural gas tanker operated by the United Arab Emirates' Abu Dhabi National Oil Company successfully traversed the Strait of Hormuz and was approaching India as of Monday.

Over the weekend, President Trump cancelled Witkoff and Kushner’s planned trip to Pakistan for peace negotiations that were scheduled for Saturday, stating that Iran could contact him if they wished to discuss a deal. During the same period, Iran’s Foreign Minister Abbas Araghchi visited Pakistan and Oman and was in Moscow on Monday to address the ongoing conflict. Both crude benchmarks began to strengthen around 8:30 am EDT following Iran’s announcement that its military should control the Strait of Hormuz.

Reportedly, Iran has submitted a new proposal to the US, offering to reopen the strait contingent on the cessation of hostilities and assurances that the conflict will not resume. According to the White House Press Secretary, the President discussed the proposal with his team but was not really considering it. Secretary of State Rubio clarified on Fox News that Iran’s reopening of the strait does not involve coordinating with Iran, seeking permission, or paying for passage.

Additionally, local news reported flaring and alarms at the Whiting, Illinois refinery overnight. The facility, owned by BP, is recognised as the largest refinery in the PADD 2 region.

Note: As of 4 pm EDT 27 April 2026

Currencies

EUR +0.13% to $1.1720

GBP +0.21% to $1.3535

Bitcoin -1.01% to $76,790.53

Ethereum -1.23% to $2,287.48

On Monday the US dollar softened, with the dollar index slipping -0.03% to 98.48. The euro appreciated +0.13% to reach $1.1720, while the pound climbed +0.21% against the dollar, trading at $1.3535. Conversely, sterling weakened by -0.10% versus the euro, falling to 86.70 pence.

The Japanese yen was little changed, holding steady at ¥159.37 per dollar.

Fixed Income

US 10-year Bond +3.8 basis points to 4.345%

German 10-year Bund +4.4 basis points to 3.041%

UK 10-year gilt +2.9 basis points to 4.973%

US Treasuries declined on Monday, following generally weaker-than-anticipated demand in front-end auctions.

On Monday, the US Treasury auctioned $166 billion in 13-week and 26-week bills, in addition to $139 billion in two-year and five-year notes. The government is scheduled to auction $44 billion in seven-year notes today.

The generally subdued reception for Treasury notes on Monday highlighted the challenges the government faces in attracting sufficient demand as high supply converges with uncertainties surrounding monetary policy and inflation expectations.

In afternoon trading, the 10-year yield rose +3.8 bps to 4.345%. Last Friday, this tenor registered its largest weekly gain since mid-March. The 30-year US Treasury yield increased +4.0 bps to 4.952%.

At the short end of the curve, the two-year yield, sensitive to interest rate expectations, rose +1.5 bps to 3.802%. The two-year yield also recorded the largest weekly increase since 16 March last Friday.

The two-year note auction was deemed fair to somewhat weak, pricing at a yield slightly above the bid deadline rate, indicating investors required a modest concession to absorb the supply.

The five-year note auction was notably underwhelming, with weaker demand metrics reflecting investor caution toward intermediate maturities, which are particularly sensitive to changing expectations for the path of the federal funds rate.

End-user demand for the five-year note, combining both indirect and direct bids, was slightly lower at 87%, compared to the 12-auction average of approximately 89%.

Investor attention now turns to this week’s FOMC meeting, which marks Jerome Powell's final scheduled meeting as Fed Chair.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing in 7.8 bps of rate cuts in 2026, lower than the 8.4 bps priced in a week ago. Fed funds futures traders are now pricing in a 0.0% probability of a 25 bps rate hike at this FOMC meeting, equal to last week’s 0.0% probability.

Eurozone short-term government bond yields edged higher on Monday as market participants turned their attention to this week's ECB meeting.

Although policymakers are expected to maintain interest rates when they convene on Thursday, investors will closely examine the ECB's statement and President Christine Lagarde's press conference for insights regarding the outlook for the eurozone economy and any indications of potential policy adjustments.

Current market pricing suggests there is approximately a 20% probability that the ECB will increase rates by 25 bps this week and a 75% likelihood by the June meeting. There are expectations for at least one, possibly two, such hikes by July.

Germany's two-year yield rose +2.7 bps on Monday, reaching 2.578%. The 10-year yield increased +4.4 bps to 3.041%, while the 30-year yield advanced +4.1 bps to 3.567%.

Bond yields in other eurozone countries moved in tandem with Bund yields, as Italy's 10-year BTP yield increased +3.6 bps to 3.838%.

Beyond the ECB meeting, traders will monitor upcoming announcements from several other major central banks. The Fed will release its policy statement on Wednesday, and the BoE will make its announcement on Thursday. Both institutions are expected to hold rates steady.

Note: As of 4 pm EDT 27 April 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

本文提供给您仅供信息参考之用,不应被视为认购或销售此处提及任何投资或相关服务的优惠招揽或游说。金融工具交易存在重大亏损风险,未必适合所有投资者。过往表现并非未来业绩的可靠指标。

由专业人士创建。 为专业人士。