What’s next for the EU and UK deals?

What to look out for today

Companies reporting on Tuesday, 24th February: American Tower, Axon Enterprise, EOG Resources, First Solar, GoDaddy, Home Depot, HP, Keurig Dr Pepper, Mosaic, NRG Energy

Key data to move markets today

US: ADP Employment Change 4-week Average, Consumer Confidence, Housing Price Index, and speeches by Chicago Fed President Austan Goolsbee, Atlanta Fed President Raphael Bostic, Boston Fed President Susan Collins, Fed Governor Christopher Waller, Fed Governor Lisa Cook, and Richmond Fed President Thomas Barkin

US Stock Indices

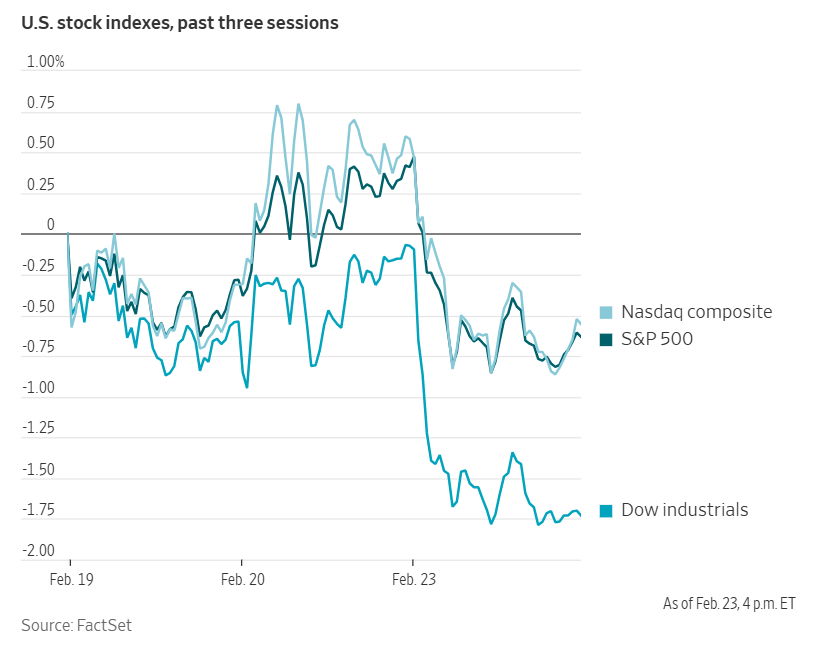

Dow Jones Industrial Average -1.66%

Nasdaq 100 -1.21%

S&P 500 -1.04%, with 5 of the 11 sectors of the S&P 500 down

US equities declined as renewed concerns over trade relations and developments in AI unsettled investors. The Dow Jones Industrial Average declined -1.66%, falling 821.91 points, with notable losses in American Express, Goldman Sachs, and JPMorgan exerting downward pressure on the index. The S&P 500 and Nasdaq Composite also posted declines, losing -1.04% and -1.13%, respectively.

Software companies faced additional headwinds following the release of a report by Citrini Research that heightened apprehension regarding the broader economic implications of AI. This growing unease has led traders to divest shares in companies perceived as vulnerable to disruption from AI technologies.

In corporate news, Anthropic CEO Dario Amodei is scheduled to meet with US Defence Secretary Pete Hegseth later today, according to a senior Pentagon official. The meeting comes amid ongoing contract negotiations, which remain stalled due to Anthropic’s insistence on implementing guardrails for the use of its AI technology.

Abbott Laboratories issued $20 billion in bonds to finance its acquisition of cancer-screening company Exact Sciences.

Gilead Sciences announced an agreement to acquire US cancer-focussed biotech Arcellx for up to $7.8 billion, aiming to strengthen its drug pipeline.

Merck & Co. revealed plans to divide its primary pharmaceutical unit into two separate entities. This move is designed to better showcase areas of growth as the company faces a looming patent expiration for its leading cancer drug, Keytruda.

Chevron emerged as the leading contender to assume control of Iraq’s second-largest oil complex from Russian producer Lukoil PJSC, following the signing of an agreement to enter exclusive negotiations regarding the oil field.

S&P 500 Best performing sector

Consumer Staples +1.46%, with Kroger +2.86%, Procter & Gamble +2.73%, and Mondelez International +2.69%

S&P 500 Worst performing sector

Financials -3.33%, with KKR -8.89%, Capital One Financial -8.84%, and American Express -7.20%

Mega Caps

Alphabet -1.02%, Amazon -2.30%, Apple +0.60%, Meta Platforms -2.81%, Microsoft -3.21%, Nvidia +0.91%, and Tesla -2.91%

Information Technology

Best performer: Akamai Technologies +4.87%

Worst performer: IBM -13.15%

Materials and Mining

Best performer: Albemarle +5.40%

Worst performer: FMC -6.57%

Corporate Earnings Reports

Posted on Monday, 23rd February

Domino’s Pizza quarterly revenue +6.4% to $1.536 bn vs $1.518 bn estimate

EPS at $5.35 vs $5.38 estimate

Russell Weiner, CEO, said, ‘In 2025 we demonstrated that when we execute our Hungry for MORE strategy it delivers MORE sales, MORE stores, and MORE profits. In our international business, we delivered a remarkable 32nd consecutive year of same store sales growth. In our U.S. business, we gained another point of market share, pacing well ahead of the QSR Pizza category, which grew again in 2025. These strong results flowed through to increased franchisee profits, showcasing our ability to drive store level profitability while providing incredible value for our customers. As we look ahead to 2026, it is our expectation that we will meaningfully increase our market share within a U.S. QSR pizza category that continues to grow. Our value and scale advantages will remain a differentiator, while our new brand campaign and e-commerce site will drive deliciousness and improved experiences. Domino’s has always been in the business of creating its own tailwinds and driving growth. That has been and will continue to be how we drive best in class results and long-term value creation for our franchisees and shareholders.’ — see report.

Dominion Energy quarterly revenue +20.3% to $4.093 bn vs $3.650 bn estimate

EPS at $0.68 vs $0.67 estimate

In its press statement, the company provided its 2026 guidance, stating, ‘The company announced its 2026 operating earnings guidance range of $3.45 to $3.69 per share with a midpoint of $3.57 per share which includes $0.07 per share of RNG 45Z income. The company extended through 2030 its long-term annual operating earnings-per-share-growth guidance of 5% to 7% off the original 2025 operating earnings per share guidance midpoint of $3.30 per share which excludes RNG 45Z, and indicated a bias to the upper half of the growth rate range in 2028 through 2030. The company also rearmed its existing credit and dividend guidance.’ — see report.

Diamondback Energy quarterly revenue -9.0% to $3.376 bn vs $3.149 bn estimate

EPS at $1.74 vs $1.78 estimate

In its press statement, the company provided its 2026 guidance, stating, ‘Full year 2026 oil production guidance of 500 - 510 MBO/d (926 - 962 MBOE/d). Full year 2026 cash capital expenditures guidance of $3.6 - $3.9 billion. Includes approximately $100 - $150 million of capital for exploratory development in the Barnett / Woodford and multiple tests to increase oil recoveries from the existing asset base. The Company expects to complete between 5.9 - 6.3 million net lateral feet in 2026. Q1 2026 oil production guidance of 502 - 512 MBO/d (930 - 966 MBOE/d). Q1 2026 cash capital expenditures guidance of $900 million - $975 million.’ — see report.

European Stock Indices

CAC 40 -0.22%

DAX -1.06%

FTSE 100 -0.02%

Commodities

Gold spot +2.43% to $5,227.75 an ounce

Silver spot +4.27% to $88.18 an ounce

West Texas Intermediate -0.03% to $66.29 a barrel

Brent crude -0.25% to $71.46 a barrel

Gold reached a three-week high on Monday. Spot gold advanced by +2.43%, trading at $5,227.75 per ounce, after earlier touching its highest level since 30th January. The precious metal previously set a record high of $5,594.82 per ounce on 29th January.

Mainland China, recognised as a major gold consumer, remained closed for the Lunar New Year holiday on Monday but is expected to resume operations on Tuesday.

Spot silver also recorded gains, climbing +4.27% to $88.18 per ounce, marking its highest level in more than two weeks. This may have been in reaction to violence in Mexico following the death of cartel leader, “El Mencho", who died in custody on Sunday shortly after being captured by Mexican special forces. Mexico is one of the largest silver producers in the world and the wave of violence across 20 Mexican states could upset silver production at a time when silver supplies are already under pressure. The Mexican silver sector has already experienced increasing threats with miners, including those at Vizsla Silver, being kidnapped as the cartels fight for control of these resources.

Oil prices edged lower on Monday but remained at a six-month high as markets awaited the third round of nuclear negotiations between the US and Iran.

Brent crude futures closed down by 18 cents, or -0.25%, at $71.46 per barrel. US WTI crude slipped by 2 cents, or -0.03%, to settle at $66.29 per barrel.

Iran has signalled its willingness to make concessions regarding its nuclear programme in exchange for the lifting of sanctions and formal recognition of its right to enrich uranium.

According to a senior US official, American envoys Steve Witkoff and Jared Kushner are scheduled to meet with the Iranian delegation in Geneva on Thursday.

Heightened concerns over the possibility of military conflict between Washington and Tehran drove both WTI and Brent crude prices up by more than five percent last week.

Meanwhile, in the US, a winter storm sweeping across the Northeast contributed to a roughly three percent increase in the diesel crack spread on Monday.

Note: As of 4 pm EST 23 February 2026

Currencies

EUR +0.03% to $1.1784

GBP +0.05% to $1.3489

Bitcoin -4.76% to $67,804.80

Ethereum -5.61% to $1,863.25

The US dollar experienced a modest decline on Monday, with the US dollar index slipping -0.10% to 97.70.

The euro edged higher by +0.03% to $1.1784, while the British pound also advanced, +0.12% to $1.3473. Additionally, the Japanese yen strengthened against the dollar, gaining +0.26% to trade at ¥154.65 per dollar.

On Monday, Fed Governor Christopher Waller indicated that he would consider maintaining interest rates at their current level during the FOMC March meeting, should forthcoming February employment data suggest the US labour market has ‘pivoted to a more solid footing’ following a weak performance in 2025.

Fixed Income

US Bond -5.5 basis points to 4.036%

German 10-year -2.5 basis points to 2.715%

UK 10-year gilt -4.5 basis points to 4.311%

US Treasuries rebounded on Monday, recovering from the selloff in the previous session, as investors weighed the implications of the Supreme Court's Friday decision to overturn President Donald Trump's broad use of emergency powers to impose tariffs. This ruling has injected renewed uncertainty into the bond market, fuelling heightened volatility.

The selloff on Friday was triggered by concerns that the Treasury would need to increase debt issuance to compensate for the anticipated refunding of tariff revenues to businesses, a likely outcome of the Supreme Court ruling. This added potential supply to a market already sensitive to deficit pressures.

As a result, Friday saw a significant rise in Treasury yields: the two-year yield posted its largest weekly increase in two and a half months, reflecting expectations that short-term borrowing costs may remain elevated. The 10-year yield also jumped, recording its biggest weekly gain in over a month and signalling a broader re-evaluation of term premiums.

However, on Monday, sentiment shifted as investors returned to Treasuries and moved away from riskier assets, responding to the fresh uncertainty surrounding the administration's trade policy direction. This swift shift in market sentiment highlighted the extent to which legal and policy changes related to tariffs can promptly influence investor behaviour.

In afternoon trading, the US 10-year yield fell -5.5 bps to 4.036%, after touching its lowest level since late November earlier in the session. The 30-year yield also declined; it was -2.1 bps at 4.705%.

On the short end of the curve, the two-year yield, closely tied to interest rate expectations, dropped -3.1 bps to 3.451%, after reaching a nearly two-week low earlier in the day.

The spread between two-year and 10-year yields narrowed to 58.5 bps, compared to 60.9 bps at the close on Friday, marking a flattening of the curve for the ninth consecutive session.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing in 59.0 bps of cuts in 2026, lower than the 63.5 bps priced in the previous week. Fed funds futures traders are now pricing in a 4.5% probability of a 25 bps rate cut at the 18th March FOMC meeting, down from 9.2% a week ago.

In the euro area, Bund yields remained close to multi-month lows on Monday, reflecting the cautious sentiment in global fixed income markets. Despite most existing tariff and trade agreements being defined through bilateral negotiations, and therefore largely unaffected by the US Supreme Court ruling, analysts noted persistent uncertainty surrounding future actions by the US administration.

US Trade Representative Jamieson Greer stated on Sunday that none of the countries with trade agreements in place had signalled intentions to withdraw. Nonetheless, the European Parliament postponed its vote on the EU - US trade deal for a second time on Monday, underscoring ongoing hesitation over transatlantic trade relations.

German government bonds reflected this cautious environment: the 10-year Bund yield dropped -2.5 bps to 2.715%, marking its lowest level since 1st December. The two-year German yield fell -1.9 bps to 2.044%, and the 30-year yield declined by -6.4 bps to 3.338%.

Italy’s 10-year government bond yield also fell, declining -2.5 bps, to settle at 3.325%. The yield spread between Italian bonds and Bunds stood at 56.9 bps, highlighting the relative stability in peripheral spreads.

Investors are now turning their attention to key data releases later in the week, including inflation reports from Germany, France, and Spain on Friday.

Economists have cautioned that a strengthening euro could intensify deflationary pressures from China’s robust export sector, potentially prompting the ECB to consider rate cuts. Data last week also indicated that the EU's trade surplus continues to narrow, as increased imports from China put pressure on domestic producers.

Note: As of 5 pm EST 23 February 2026

Global Macro Updates

US tariffs saga: Europe and UK navigate new trade barriers. The US has replaced International Emergency Economic Powers Act (IEEPA) tariffs with a new 15% global tariff under Section 122, while maintaining existing Section 232 sectoral tariffs on automobiles and metals. The overall impact on Europe is assessed as mildly negative. Analysts estimate that the shift increases the effective US tariff rate on EU imports by just 0.9 percentage points to 12.1%, and raises the rate for the UK by 2.9 points to 10.9%. However, several uncertainties remain, including whether the 15% rate will apply to countries that had previously negotiated lower tariffs. This ambiguity could lead European exporters to strategically delay shipments.

ECB President Christine Lagarde cautioned that these changes risk unsettling the business environment to which companies have become accustomed. In response, the European Parliament’s trade chief has proposed freezing the ratification of the EU - US trade agreement. Section 122 tariff is set to last only 150 days, with analysts highlighting Section 232 and Section 301 as more permanent alternatives should the US seek longer-term measures. Given that exemptions cover approximately half of EU exports and European shipments are already 10 – 20% below 2024 levels, much of the adverse impact may already be reflected in current pricing.

UK exporters are expected to incur an additional £2 billion to £3 billion in costs following the US tariff increase from 10% to 15%, according to the British Chambers of Commerce (BCC). While modest in absolute terms, this rise represents the largest tariff increase among the US’s top twenty trading partners and effectively adds a further 5% duty on UK exports under separate legislation.

The Times reports that UK officials are engaged in high-level discussions with their US counterparts and intend to reinforce rather than abandon the Economic Prosperity Deal agreed to last year by President Trump and Prime Minister Starmer. The BCC noted that the original agreement focussed less on headline tariffs and more on sector-specific exemptions, such as zero tariffs on pharmaceuticals and reduced duties on steel, thereby providing a foundation for broader negotiations.

These recent developments introduce some downside risk to the UK’s export outlook and heighten uncertainty for industries exposed to international trade. Nevertheless, markets are likely to interpret these events primarily in the context of ongoing UK - US negotiations, rather than as an immediate macroeconomic shock.

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

本文提供给您仅供信息参考之用,不应被视为认购或销售此处提及任何投资或相关服务的优惠招揽或游说。金融工具交易存在重大亏损风险,未必适合所有投资者。过往表现并非未来业绩的可靠指标。

由专业人士创建。 为专业人士。