Is the Fed now even stronger?

Key data to move markets today

EU: German CPI, Harmonised Index of Consumer Prices, Retail Sales, Unemployment Rate and Unemployment Change, French and Italian CPIs and speeches by ECB Vice President Boris Vujčić, ECB Chief Economist Philip Lane and ECB Executive Board members Piero Cipollone, Frank Elderson and Isabel Schnabel

UK: GDP and a speech by BoE Deputy Governor for Financial Stability Sarah Breeden

USA: Consumer Confidence, Housing Price Index, JOLTS Job Openings and Chicago PMI

CHINA: RatingDog Manufacturing PMI

Global Macro Updates

Supreme Court lets Fed Governor Lisa Cook remain during litigation. In a 5 - 4 decision in Trump vs Cook, the Supreme Court held that the president cannot remove Fed Governor Cook while lower courts continue to consider the case. Justices Roberts, Sotomayor, Kagan, Kavanaugh and Jackson joined the decision, while Justices Thomas, Alito, Gorsuch and Barrett dissented.

The opinion said accepting the government’s view that the president’s for-cause removal decision is unreviewable would effectively make the role at-will, a result it described as inconsistent with the Federal Reserve Act and the US tradition of central bank independence.

The Court also cited the president’s failure to provide Cook the procedural protections needed to contest the allegations. Citing precedent, the opinion said for-cause dismissal implied she was entitled to an opportunity to respond before termination. Chief Justice Roberts also found the social-media announcement of her removal insufficient.

In dissent, Thomas argued that apparent mortgage fraud constituted cause for removal and that federal courts lacked authority to grant the relief upheld by the majority. He added that the president was likely to succeed on the merits. Alito separately argued that lower courts had resolved some issues incorrectly, while Barrett said the case met the irreparable-harm standard by preventing the president from dismissing a subordinate.

Markets had focussed on whether the Court would reinforce Fed independence. Although the opinion strongly supports that principle, the case remains unresolved. Separately, the Supreme Court upheld the US President’s firing of Democratic FTC Commissioner Slaughter, while noting that the FTC role does not share the central bank’s tradition of insulation from plenary presidential control.

US Stock Indices

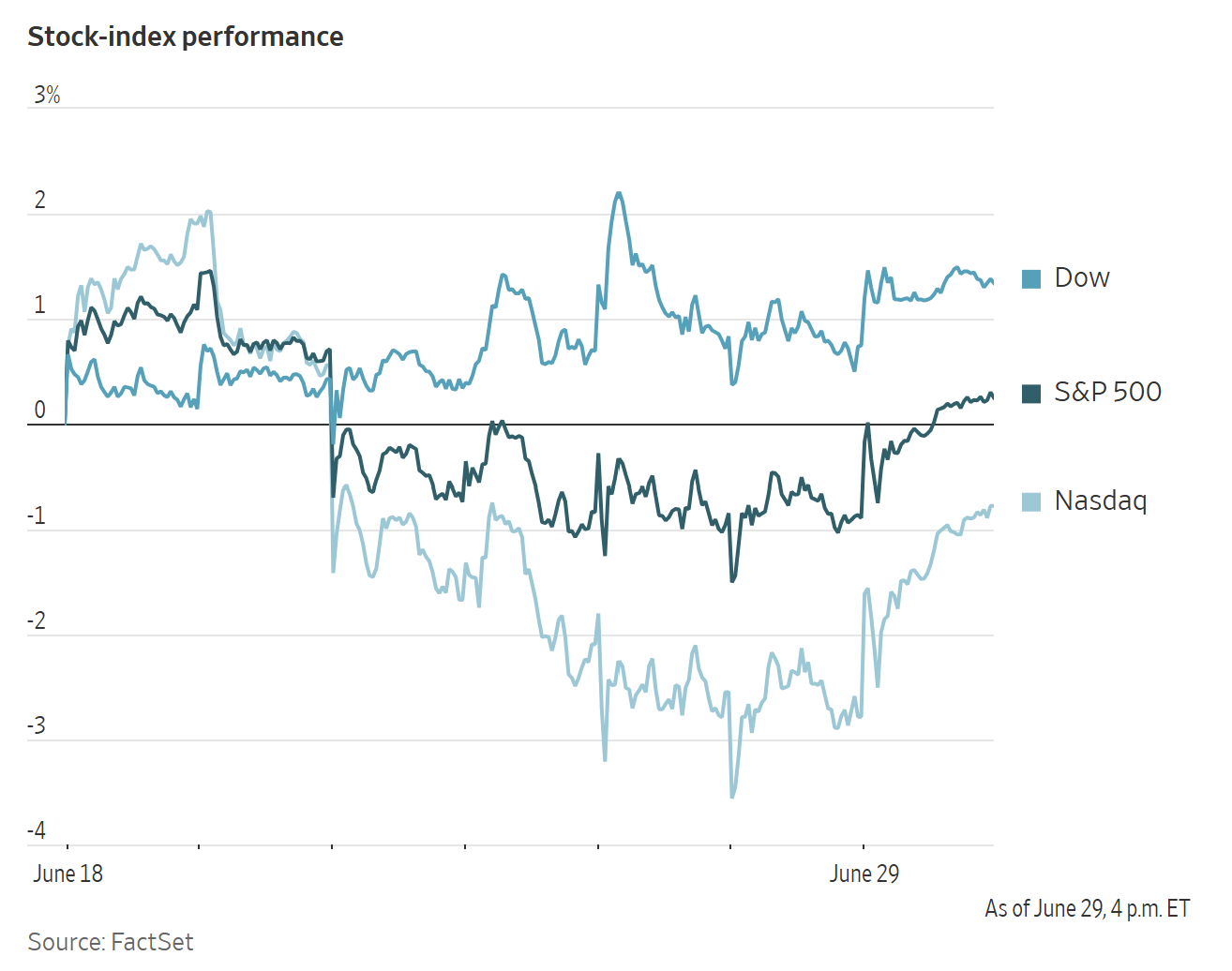

Dow Jones Industrial Average +0.59%

Nasdaq 100 +2.25%

S&P 500 +1.18%, with 6 of the 11 sectors of the S&P 500 up

Stocks advanced on Monday after last week’s selloff in technology shares. The Nasdaq Composite led US indices with a +2.07% gain, while the S&P 500 rose +1.18% to 7,440.43.

As equities approached the end of what is set to be their strongest quarter in six years, both the Nasdaq and S&P 500 ended five-session losing streaks. The Dow Jones Industrial Average, which added Alphabet to its 30 constituents, closed above 52,000 for the first time at 52,182.74, up 303.63 points, or +0.59%. Alphabet was the index’s top performer, rising +4.96%.

In corporate news, Verizon Communications and the UK’s BT Group agreed to form a joint venture serving more than 3,000 enterprise clients across over 180 countries, with about $4 billion in combined annual revenue. Verizon will pay BT $625 million to offset differences in value, ownership and tax liabilities. The transaction remains subject to regulatory approval.

Comcast plans to spin off NBCUniversal and Sky into a separate company that will include theme parks, film and television studios and the Peacock streaming service. Comcast will retain its cable-TV, broadband and wireless operations. Shareholders will own stakes in both companies after the separation, which is expected within a year pending board and regulatory approvals.

Rocket Lab agreed to acquire Iridium Communications for $54 per share in a cash-and-stock deal valuing Iridium at about $8 billion. The combination will pair Rocket Lab’s launch and satellite manufacturing capabilities with Iridium’s low-Earth-orbit network and radio spectrum. This will create an integrated company that can design, build, launch and operate its own constellations.

Martin Marietta Materials agreed to combine with building materials supplier Lhoist North America in a transaction valued at $13.5 billion, including debt. The company plans to finance the deal with $7 billion in cash and $6.5 billion in stock, according to a statement issued Monday.

S&P 500 Best performing sector

Consumer Discretionary +2.68%, with Tesla +8.46%, Amazon +3.20% and Norwegian Cruise Line +3.20%

S&P 500 Worst performing sector

Materials -1.86%, with Celanese -7.06%, Martin Marietta Materials -5.65% and Eastman Chemical -5.36%

Mega Caps

Alphabet +4.96%, Amazon +3.20%, Apple -0.72%, Meta Platforms +2.24%, Microsoft -1.18%, Nvidia +1.27% and Tesla +8.46%

Information Technology

Best performer: Corning +15.67%

Worst performer: Super Micro Computer -8.10%

Materials and Mining

Best performer: Corteva +0.91%

Worst performer: Celanese -7.06%

European Stock Indices

CAC 40 -0.21%

DAX -0.18%

FTSE 100 -0.23%

Commodities

Gold spot -1.77% to $4,016.02 an ounce

Silver spot -1.46% to $58.30 an ounce

West Texas Intermediate +0.60% to $70.42 a barrel

Brent crude -0.18% to $72.80 a barrel

Gold prices declined on Monday, weighed down by expectations of rising interest rates, a slight cooling of tensions in the Middle East and structural selling pressure given its recent fall below its 200-day moving average.

Spot gold fell -1.77% to $4,016.02 per ounce, after earlier dropping more than two percent during the session and reaching a more than seven-month low last week.

Spot silver also weakened, sliding -1.46% to $58.30 per ounce.

Oil benchmarks were mixed on Monday as attacks by the US and Iran highlighted the fragility of their interim peace agreement. However, cautious optimism around a continued recovery in energy shipments through the Strait of Hormuz limited gains.

Iranian and US technical teams working on the implementation of the interim peace deal are expected to meet in Doha in the coming days, a source told Reuters on Monday, after tit-for-tat weekend strikes threatened to derail the accord.

Brent crude futures settled 13 cents, or -0.18%, lower at $72.80 a barrel, while US WTI crude gained 42 cents, or +0.60%, to $70.42.

Brent declined last week for a third consecutive week, after crude shipments through the strait rose to their highest level since the US - Israeli-led conflict with Iran began in late February.

The US military conducted strikes on Iranian targets over the weekend following an attack on a Panama-flagged tanker in the Strait of Hormuz. Iran also launched missiles and drones at US military sites in Kuwait and Bahrain early on Sunday, shortly after the US President warned that Iran would cease to exist if it did not honour the agreement to end the war.

Iranian and Omani experts are set to begin talks in the coming days on redefining transit routes through the Strait of Hormuz, Iranian Deputy Foreign Minister Kazem Gharibabadi told state television on Monday. He added that Iran would seek to obstruct vessels operating outside the defined routes.

Reuters reported that shipping data indicate that Middle East producers continue to load oil and LNG despite renewed ship attacks in the Strait of Hormuz and heightened tensions between the US and Iran.

CBS reported that traffic through the Strait of Hormuz slowed over the weekend after Saturday’s strike on a vessel. Kpler data showed that 29 commodity vessels crossed on Saturday, while 12 transited on Sunday.

The Financial Express reported that West Asia’s crude oil supply had rebounded to around 14.6 million to 15 million bpd earlier this month, after nearly 2 million bpd returned following the preliminary US - Iran agreement.

Saudi Aramco resumed crude loadings at its Ras Tanura terminal in the Gulf last Friday after a nearly four-month halt, CNBC reported. Loadings continued even after a company helicopter crashed at Ras Tanura on Sunday, killing 14 people. The cause of the crash was not known.

Elsewhere, Ukraine carried out strikes over the weekend on two Russian oil refineries, including the Slavyansk refinery in the Krasnodar Krai region and another facility in the Yaroslavl region. Russian President Vladimir Putin acknowledged that Russia is facing fuel shortages following a wave of Ukrainian strikes on oil terminals, refineries and pipelines.

S&P Global reported that South Korea secured close to ninety percent of its monthly crude oil requirements in May despite the Middle East conflict, as refiners obtained ample Saudi crude through the Red Sea route.

Note: As of 4 pm EDT 29 June 2026

Currencies

EUR +0.36% to $1.1424

GBP +0.42% to $1.3255

Bitcoin +0.91% to $60,406.97

Ethereum +2.85% to $1,618.27

The dollar declined on Monday but remained near a 13-month high, supported by optimism over US economic growth and expectations for further Fed interest rate increases.

The Japanese yen also weakened to its lowest level against the US currency since 1986.

The dollar index dipped -0.26% to 101.08.

The euro rose +0.36% to $1.1424, after reaching a 13-month low against the dollar last week.

The yen touched ¥161.97 on Monday, its weakest level in 40 years, before trading -0.10% lower on the day at ¥161.90.

Sterling strengthened +0.42% to $1.3255, having reached its lowest level in seven months last week.

On the economic front, the main US focus this week will be Thursday’s June jobs report. Three consecutive months of stronger-than-expected payroll gains have supported the Fed’s hawkish shift. However, a turn in the labour market could prompt a more dovish reassessment of the policy path.

The data is expected to show that employers added 110,000 jobs last month, while the unemployment rate remained steady at 4.3%.

Fixed Income

US 10-year Bond -0.7 basis points to 4.380%

German 10-year Bund +1.0 basis points to 2.866%

UK 10-year Gilt -1.4 basis points to 4.724%

US Treasury yields edged lower on Monday.

The yield on the US 10-year Treasury note edged down -0.7 bps to 4.380%, after falling for three consecutive weeks. The yield on the 30-year bond declined -0.1 bps to 4.867%.

The two-year US Treasury yield, which typically moves in line with expectations for the federal funds rate, fell -0.2 bps to 4.113% after four consecutive declines.

The US Treasury yield curve, measured by the spread between two- and 10-year Treasury notes, stood at a positive 26.5 bps, narrowing 0.5 bps from Friday’s close.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing 32.2 bps of rate hikes in 2026, lower than the 41.5 bps priced in a week ago. Fed funds futures traders are now pricing in a 31.5% probability of a 25 bps rate hike at July’s FOMC meeting, compared to 36.3% last week.

Eurozone bond yields edged higher on Monday, while staying close to their lowest levels since early March.

Markets have reduced expectations for additional ECB and BoE rate increases since the interim ceasefire between Iran and the US reopened the Strait of Hormuz.

Germany’s 10-year bond yield rose +1.0 bps to 2.866% on Monday, after touching 2.830% last Friday, its lowest level since 10 March. The rate-sensitive two-year yield climbed +4.1 bps to 2.567%, remaining near Friday’s two-month low, while the 30-year yield added +0.7 bps to 3.418%.

Italy’s 10-year BTP yield rose +0.3 bps to 3.588%, near its lowest level since mid-March, leaving the spread over Bunds at 72.2 bps. France’s 10-year OAT yield increased +1.9 bps to 3.539%, with its spread over Bunds at 67.3 bps.

Note: As of 4 pm EDT 29 June 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.