Is divergence emerging as a dollar headwind?

This is our last daily market insights this year, but we will resume publication on 12th January, 2026. We wish all of our readers a very happy holiday season.

Key data to move markets today

EU: German GfK Consumer Confidence Survey, PPI, Bundesbank Monthly Report, and speeches by President of the DNB Olaf Sleijpen, and ECB Executive Board Members Piero Cipollone and Philip Lane

UK: Retail Sales

USA: Michigan Consumer Sentiment and Expectations Indices, UoM 1- and 5-year Consumer Inflation Expectations, and Existing Home Sales

JAPAN: BoJ Press Conference

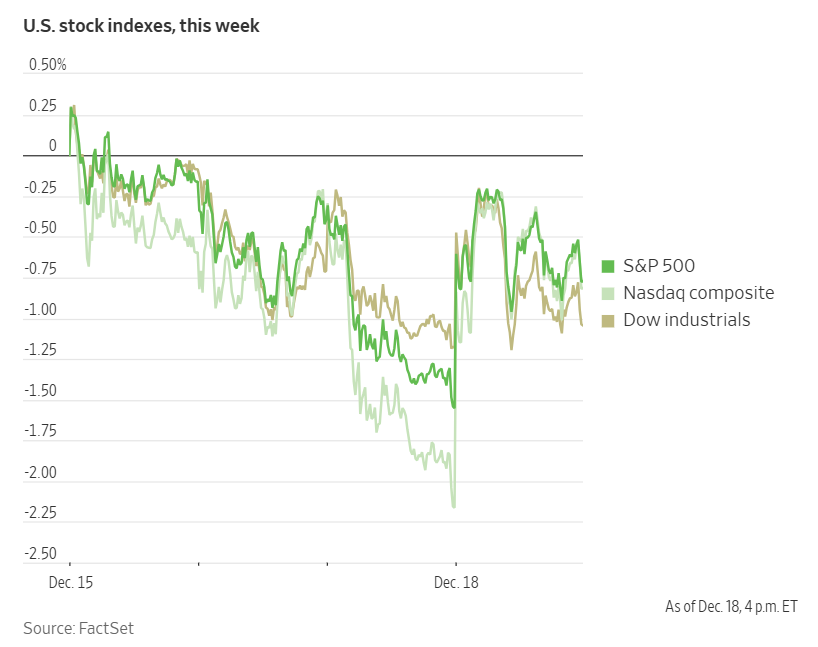

US Stock Indices

Dow Jones Industrial Average +0.14%

Nasdaq 100 +1.51%

S&P 500 +0.79%, with 6 of the 11 sectors of the S&P 500 up

A lower-than-anticipated inflation reading prompted a rally on Wall Street Thursday.

The Nasdaq Composite led the rally, gaining +1.38%. The Dow Jones Industrial Average edged higher by +0.14%, while the S&P 500 rose +0.79%. Both the Dow and S&P 500 ended a streak of four consecutive declines.

In corporate news, Elliott Investment Management disclosed a stake exceeding $1 billion in Lululemon Athletica and is advocating for Jane Nielsen, a former Ralph Lauren executive, to assume the Chief Executive role.

FedEx reported incurring an additional $25 million in expenses in November following last month’s UPS cargo plane crash, which resulted in the grounding of all MD-11 aircraft, including those in FedEx’s fleet. Company executives indicated that costs are expected to rise further in December, the peak season for parcel delivery, as FedEx increasingly relies on trucks and external carriers to fulfill demand.

ByteDance, the parent company of TikTok, has finalised agreements with investors to establish a new US joint venture. This move is intended to facilitate a deal that would prevent the app from being banned in the US due to national security concerns, according to a company memo reviewed by The Wall Street Journal.

TikTok CEO Shou Chew stated in the memo that TikTok USDS Joint Venture LLC will be owned 50% by a consortium of new investors—including Oracle, private-equity firm Silver Lake, and Abu Dhabi-based investment fund MGX, each holding a 15% stake. Additionally, 30.1% will be controlled by affiliates of certain existing ByteDance investors, while the remaining 19.9% will be retained by ByteDance.

BP appointed Meg O’Neill as chief executive officer, succeeding Murray Auchincloss after a two-year tenure, as the company seeks to recover from challenges associated with its transition toward renewable energy.

Renault has regained investment-grade status from S&P Global Ratings, which commended the French automaker’s refreshed product lineup and its expansion efforts outside Europe.

S&P 500 Best performing sector

Consumer Discretionary +1.78%, with Starbucks +4.94%, Lululemon Athletica +3.48%, and Tesla +3.45%

S&P 500 Worst performing sector

Energy -1.42%, with Diamondback Energy -4.59%, Marathon Petroleum -3.66%, and APA -3.33%

Mega Caps

Alphabet +1.91%, Amazon +2.48%, Apple +0.13%, Meta Platforms +2.32%, Microsoft +1.65%, Nvidia +1.87%, and Tesla +3.45%

Information Technology

Best performer: Micron Technology +10.21%

Worst performer: HP -4.01%

Materials and Mining

Best performer: Albemarle +4.28%

Worst performer: Nucor -1.78%

European Stock Indices

CAC 40 +0.80%

DAX +1.00%

FTSE 100 +0.65%

Commodities

Gold spot -0.14% to $4,331.19 an ounce

Silver spot -1.17% to $65.40 an ounce

West Texas Intermediate -1.49% to $56.05 a barrel

Brent crude -1.40% to $59.75 a barrel

Gold prices declined slightly on Thursday, with spot gold falling -0.14% to $4,331.19 per ounce. Earlier in the session, bullion had hovered near the record high of $4,381.21 reached on 20th October.

Spot silver also retreated, dropping -1.17% to $65.40 per ounce after reaching an all-time high of $66.88 in the previous session.

Oil prices closed lower on Thursday as market participants evaluated the potential for additional US sanctions on Russia and the supply risks arising from a blockade of Venezuelan oil tankers.

Brent crude settled at $59.75 per barrel, declining by 85 cents or -1.40%, while US WTI crude fell 85 cents, or -1.49%, to $56.05 per barrel.

On Thursday, the US President expressed optimism regarding progress in negotiations to end the war in Ukraine, stating he believes the talks are ‘getting close to something’ ahead of a scheduled US meeting with Russian officials this weekend.

According to a Bloomberg news report on Wednesday, which cited individuals familiar with the matter, the US is preparing a new round of sanctions targeting Russia's energy sector should Moscow fail to reach a peace agreement with Ukraine.

Additional measures against Russian oil could present a more significant supply risk to global markets than the recent US announcement to blockade tankers subject to sanctions entering or leaving Venezuela.

The UK enacted sanctions on 24 individuals and entities as part of its ongoing Russia sanctions regime, including penalties on Russian oil firms Tatneft and Russneft, as detailed in a government notice released Thursday.

The blockade of Venezuelan oil tankers has the potential to disrupt approximately 600,000 barrels per day of exports, primarily to China; however, around 160,000 barrels per day of shipments to the US are expected to continue without interruption.

Note: As of 4 pm EST 18 December 2025

Currencies

EUR -0.14% to $1.1723

GBP +0.04% to $1.3377

Bitcoin -0.68% to $85,396.20

Ethereum +0.06% to $2,821.03

On Thursday, the US dollar declined against both the Japanese yen and the Swiss franc following the release of inflation data that came in below expectations.

The euro experienced minor losses in volatile trading, as the ECB reaffirmed its policy stance and offered a more optimistic assessment of the eurozone’s economic outlook.

The dollar index edged up by +0.06% to 98.45, while the euro last traded -0.14% lower at $1.1723 against the US dollar.

Sterling strengthened slightly in response to the BoE’s fourth rate cut of the year. However, market participants revised their expectations for additional easing, with the next rate cut now anticipated in June rather than April. The pound rose by +0.04% to $1.3377.

Against the Japanese yen, the dollar slipped by -0.08% to ¥155.57. The BoJ is widely expected to raise short-term interest rates today from 0.50% to 0.75%, as persistently high food prices continue to drive inflation above the central bank’s 2% target.

Fixed Income

US 10-year Treasury -3.1 basis points to 4.125%

German 10-year bund -1.8 basis points to 2.852%

UK 10-year gilt +0.3 basis points to 4.490%

US Treasury yields declined on Thursday following data indicating that consumer prices increased less than economists had anticipated on a y/o/y basis last month. Notably, data lapses stemming from the US government shutdown have raised concerns regarding the accuracy of the release.

The headline Consumer Price Index rose 2.7% in November compared to the previous year, while core prices climbed 2.6%. These figures fell short of economists' expectations, who had forecast a 3.1% increase in the headline number and 3.0% for core inflation.

Ongoing concerns about data gaps have prompted traders to exercise caution when interpreting this week's releases as indicators of future Fed policy.

The government did not publish the October inflation data, as the necessary information could not be collected during the record 43-day shutdown.

The yield on the 2-year Treasury note, which is closely tied to expectations for Fed Funds rate outlook, fell by -3.0 bps on the day to 3.470%. It reached a session low of 3.433%, marking its lowest level since 17th October.

The yield on 10-year US Treasury notes declined by -3.1 bps to 4.125%, the lowest since 11th December.

The spread between the two- and 10-year Treasury yields narrowed by 0.6 bps to 65.5 bps.

Yields have remained largely range-bound in recent months, as market participants await new developments that could influence Fed policy. Additionally, trading volumes are expected to ease ahead of the upcoming Christmas holiday.

The US Treasury Department reported robust demand for its $24 billion auction of five-year Treasury Inflation-Protected Securities held on Thursday. The securities were sold at a high yield of 1.433%, nearly 1 bps below the level at which they traded prior to the auction.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing in 62.0 bps of cuts in 2026, higher than the 55.6 bps priced in last week. Fed funds futures traders are now pricing in a 26.6% probability of a 25 bps rate cut at January’s FOMC meeting, up from 24.4% a week ago.

Eurozone government bond yields declined modestly in response to the ECB well-telegraphed decision to maintain its policy rates unchanged.

The ECB offered a notably optimistic assessment of the euro area’s economic outlook, emphasising the region's resilience amid global trade disruptions.

German 10-year yields fell by -1.8 bps to 2.852%, having reached a recent peak of 2.894% last week—the highest since mid-March. On the front end of the curve, the 2-year Schatz yield rose by +0.3 bps to 2.146%, and on the long end of the curve, the 30-year yield also advanced by +0.2 bps to 3.487%.

Following the ECB’s announcement, money market participants recalibrated their expectations, now assigning roughly a 20% probability of a policy tightening by December 2026 and a 45% chance by March 2027; these figures are up from 12% and 35%, respectively, prior to the statement.

Last week, traders had attributed a greater than 50% likelihood to a tightening move in March 2027. With the ECB deposit rate holding at 2%, the implied probability of a rate cut in 2026 has declined to approximately 10%, down considerably from over 60% in mid-October.

Italy’s 10-year yield decreased by -2.8 bps to 3.540%, keeping the spread between Italian BTPs and German Bunds at 68.8 bps. French 10-year OAT yields also moved lower, declining by -2.2 bps to 3.555%.

Note: As of 5 pm EST 18 December 2025

Global Macro Updates

ECB keeps policy steady, medium-term inflation meets target. The ECB maintained its key deposit rate at 2% for the fourth consecutive meeting, following updated projections that reaffirmed inflation is expected to stabilise at the 2% target over the medium term. The latest forecasts indicate that headline inflation will remain below target for the next two years but return to 2.0% in the first projection for 2028.

The core inflation measure is now forecast at 2.2% for 2026, up from the previous estimate of 1.9%; it is expected to moderate to 1.9% in 2027 and return to 2.0% in 2028. The ECB revised its inflation outlook for 2026 upward, attributing the change primarily to a slower decline in services prices. On the growth front, the GDP forecast for 2025 was adjusted higher to 1.4% from the prior 1.2%, with expectations for 2026 also raised to 1.2% from 1.0%. GDP growth is projected to reach 1.4% in both 2027 and 2028.

The ECB’s communication remained unchanged, reiterating its commitment to a data-dependent, meeting-by-meeting approach. Ahead of the meeting, policymakers had downplayed concerns regarding a potential inflation undershoot in the coming year. President Lagarde previously noted that the ECB would not react to minor deviations from the target, suggesting that the threshold for additional policy easing remains high. Furthermore, Executive Board member Isabel Schnabel recently expressed support for market expectations that the next policy move is more likely to be a rate hike.

BoE lowers key rate by 25 bps after a narrow vote. As expected, the BoE reduced its key Bank Rate by 25 bps to 3.75% following a closely split vote by the Monetary Policy Committee (MPC), with the decision passing 5-4 after Governor Bailey, who had previously voted for unchanged policy in November, sided with the majority.

Governor Bailey emphasised that recent data confirm a more established disinflation trend, with inflation having peaked and Budget measures expected to further curb inflation. He noted that any additional policy easing would depend on developments in the inflation outlook and projected that the policy rate would continue its gradual decline. In the absence of new economic shocks, he suggested that individual rate-setting judgments would become more nuanced, potentially reflecting either the limited scope for further easing relative to the estimated neutral rate or uncertainties regarding the equilibrium rate level.

Regarding inflation, the Consumer Price Index (CPI) is forecast to decline to approximately 3% in Q1 2026, with Budget measures likely to reduce it by an additional 0.5 percentage points. Consequently, Bank staff have revised the CPI outlook closer to 2% for Q2 of 2026. While the labour market continues to show signs of loosening, forward-looking wage indicators remain elevated, and Bank staff now anticipate zero growth in Q4.

BoJ raises rates 25 bp as anticipated, maintains normalisation. BoJ unanimously approved a 25 bps rate increase, in line with expectations, raising the uncollateralised overnight call rate to 0.75%—its highest level since 1995. In its economic assessment, the BoJ highlighted ongoing domestic wage growth and cited sufficient evidence that the virtuous wage-price cycle remains intact, referencing a collection of anecdotal reports from its regional branches. While the BoJ acknowledged continued uncertainties regarding the US economic outlook and tariffs, it noted that these risks have declined. The Bank now considers it highly probable that the wage-price cycle will persist, enhancing the likelihood of achieving its price stability target in the latter half of the projection period.

The BoJ's statement reiterated that, with real rates still low, future rate increases will be implemented in line with improvements in economic activity and prices, without significant changes to its language or guidance. While there was general consensus on the policy decision, some dissention emerged regarding the economic assessment, resulting in a slightly more hawkish outlook. Board member Takata contended that both official and underlying Consumer Price Index (CPI) inflation had largely met the price stability target, whereas Tamura projected that underlying CPI inflation will generally align with the price stability goal from the middle of the forecast period onward. Attention now turns to Governor Ueda’s press conference for further clarification on policy guidance.

US CPI report. In November, US Consumer Price Index (CPI) data came in below expectations, with both headline and core inflation readings significantly cooler than anticipated. Core inflation eased to its slowest pace since March 2021. On an annualised basis, headline CPI increased by 2.7%, compared to the consensus estimate of 3.1% and the previous reading of 3.0%. Meanwhile, core CPI rose 2.6%, falling short of both the consensus and prior figures of 3.0%.

However, economists cautioned that the accuracy of these figures may have been affected by the government shutdown in October, which disrupted the Bureau of Labor Statistics' data collection efforts and resulted in gaps across numerous month-over-month components.

Despite this caveat, analysts underscored that the report delivered clear indications of moderating inflation. Shelter prices, which have played a significant role in recent persistently high inflation, increased by 3.0% y/o/y—the smallest gain in more than four years. Additionally, tariff-related categories such as apparel, footwear, and appliances remained stable. The data also signalled a continued moderation in vehicle pricing, with sequential declines in used car prices and stable new vehicle pricing.

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

Este artículo se presenta a modo informativo únicamente y no debe ser considerado una oferta ni solicitud de oferta para comprar ni vender inversión alguna ni los servicios relaciones a los que se pueda haber hecho referencia aquí. Operar con instrumentos financieros implica un riesgo significativo de pérdida y puede no ser adecuado para todos los inversores. Los resultados pasados no garantizan rendimientos futuros.

Regístrese para recibir perspectivas de los mercados

Regístrese

para recibir perspectivas

de los mercados

Suscríbase ahora

Creado por profesionales. Para profesionales.