Markets in June

June has been a largely positive month for US equities markets so far with the S&P 500 +3.05% MTD in June, the Dow Jones +1.69% MTD, and the Nasdaq 100 +4.20% MTD. Conversely European equity markets have had a mostly negative month on rising Middle East tensions worrying energy markets while the tariff dispute with the US remains unresolved. The STOXX 600 is -2.13 % MTD in June.

In the bond market, the benchmark 10-year Treasury yield fell in June. There appears to be a growing division within the Fed over the timing of the next rate cut. Despite the Fed stating during its June meeting that it has time to observe the impact of tariffs, there is increasing political pressure from the US President to cut rates.

Uncertainty around tariff negotiations and the potential impact of the latest spike in energy prices means that only one more cut is expected by the ECB this year. The UK will continue to walk a fine line between cutting rates to help grow the economy and concerns that inflation will remain well above target this year and is likely to remain on hold until there is greater clarity although market participants are still anticipating cuts in August and November..

The economic picture

Despite the dollar experiencing significant fluctuations throughout the month, the dollar index for June is -1.74% MTD. The dollar’s volatility has been due to uncertainty over US tariffs, a rush to safe havens, and investor concerns around debt sustainability given projected rise in the US debt to GDP level and the budget deficit. Headline inflation rose by 0.1% m/o/m in May, down from April’s 0.2%, while core CPI, excluding food and energy, was at 0.1% and 2.8%, respectively, compared with forecasts for 0.3% and 2.9%. The US labour market continued to show strength with nonfarm payrolls increasing a seasonally adjusted 139,000 in May. Unemployment was unchanged at 4.2%. Real average hourly earnings grew 0.3% from April to May and 1.4% y/o/y. The labour force participation rate fell slightly in May to 62.4% from April’s 62.6%, and the employment-population ratio declined by 0.3% to 59.7%.

On the growth front June Flash PMIs showed US business activity continued to grow in June though at a slower pace. Falling exports of goods and services acted as a drag on growth, in part offset by stock building by US companies, due to concerns over tariffs. The Flash Composite PMI in June came in at 52.8, down from May’s final reading of 53.0. The Flash services PMI came in at 53.1, down from May’s 53.7. The Flash Manufacturing PMI remained stable at: 52.0. However, as noted by S&P, price pressures rose sharply across both manufacturing and service sectors during June, the former reporting an especially steep increase, and again commonly linked to tariffs. Companies’ expectations about output in the year ahead dipped slightly in June. The Conference Board's consumer confidence index deteriorated by 5.4 points in June, falling to 93.0 from 98.4 in May. The Present Situation Index—based on consumers’ assessment of current business and labour market conditions—fell 6.4 points to 129.1. The Expectations Index—based on consumers’ short-term outlook for income, business, and labour market conditions—fell 4.6 points to 69.0, substantially below the threshold of 80 that typically signals a recession ahead. However, the University of Michigan consumer sentiment survey improved for the first time in six months, climbing 16% from last month but remaining about 20% below December 2024, when sentiment had exhibited a post-election bump. Year-ahead inflation expectations dropped from 6.6% last month to 5.1% in June. Long-run inflation expectations fell for the second straight month, edging down from 4.2% in May to 4.1% in June.

In the UK, inflation edged down in June, coming in at 3.4% from May’s 3.5%. Core inflation also fell slightly to 4.4% in May from April’s 4.5%. The BoE held rates at 4.25% at the June meeting with six members voting to leave rates unchanged and three voting for a 25 bps cut. The Bank’s statement said that it expects a significant slowing of pay growth over the rest of the year and it signalled a possible cut at its meeting in August due a weakening jobs market. The BoE’s MPC noted that problems with the UK’s labour market data continued to be a concern, but stated that May’s 109,000 fall in the UK’s official estimate of payrolled employees was the largest monthly contraction since May 2020. The Bank also noted that ‘global uncertainty remains elevated and that energy prices have risen owing to an escalation of the conflict in the Middle East.’ It said it will remain sensitive to heightened unpredictability in the economic and geopolitical environment and will continue to update its assessment of risks to the economy. It also said that ‘Monetary policy is not on a pre-set path.’ Traders are currently expecting 2 more rate cuts this year.

In terms of business activity in June, the S&P Global Flash Composite PMI for the UK came in at 50.7 in June, up from 50.3 in May. The Flash Services PMI was 51.3, up from May’s 50.9 and a 3-month high. The Flash Manufacturing PMI was also up, although still in contractionary territory at 47.7 from May’s 46.4. However, the monthly growth of price charged by businesses fell to 53.2 in June, from 55.4 in the previous month, the lowest since January 2021. This indicates that growth remains subdued. Strong cost pressures and subdued demand meant that UK private sector employment decreased for the ninth consecutive month. According to Chris Williamson, Chief Business Economist at S&P Global, the UK economy remained in a sluggish state at the end of the second quarter. He said the reading was consistent with GDP growth rising only by 0.1% in Q2, a marked slowdown from the 0.7% in Q1. He also stated that the reduction of inflationary pressures in the services sector, the stalling of growth and slowing employment may lead the BoE to cut rates in August.

Nevertheless, consumer confidence was slightly up in June with the GfK Consumer Confidence Index rising by 2 points to -18, marking a gradual rebound from May's -20 and April's -23. This was driven by improvements in how consumers see the general economy, with scores up three points (looking at last year) and up by five points (looking at the next 12 months). As noted by Neil Bellamy, Consumer Insights Director at GfKm ‘Confidence is still fragile because the dark shadow of inflation…with petrol prices set to rise in the coming weeks following the escalation of the conflict in the Middle East, and with ongoing uncertainty as to the full impact of tariffs, there is still much that could negatively impact consumers.’

The labour market is weakening with the number of staff on payroll falling by 109,000 in May. Since last October’s budget, the number of jobs lost is 276,000; this suggests firms may be cutting costs due to higher employer taxes and the rise in the minimum wage. According to the Office for National Statistics, wage growth slowed more than forecast, with pay growth excluding bonuses coming in at 5.2%, the slowest pace in seven months, and private-sector wage growth fell to 5.1% from 5.5%. Unemployment rose to 4.6%, the highest since the summer of 2021.

Eurozone inflation fell to 1.9% in May down from 2.2% in April. Core inflation, which excludes energy and food, was down to 2.3% from April’s 2.7%. Services inflation cooled significantly to 3.2% in May, down from April’s 4% reading. This drop in inflation is being supported by cooling wages. The ECB wage tracker indicated that negotiated wage growth of 4.7% in 2024 and 3.1% in 2025. With unsmoothed one-off payments, the tracker pointed to 2.9% growth in 2025. The ECB has previously stated that wage growth around 3% would be consistent with its 2% inflation target

On the growth front, the eurozone is contracting. The June eurozone HCOB Flash Composite PMI came in barely in expansionary territory at 50.2 and below expectations of 50.5. The HCOB Flash Services PMI held steady at 50. The HCOB Flash Manufacturing PMI came in at 49.4 in June 2025, the same as in May, and below forecasts of 49.8 and failing to grow for a 36th month. The pace of input cost inflation eased for the fourth consecutive month in June and was the weakest since last November. As noted by Dr. Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank,’The eurozone economy is struggling to gain momentum. Companies are still facing quite significant cost increases and raised their selling prices slightly more in June than in the previous month. This higher inflation in the service sector is partly offset by a deflationary environment in the goods sector. However, energy prices play an important role here. Until recently, they were still falling, but have risen sharply since the conflict between Israel and Iran.’

Global market indices

USA:

S&P 500 +3.05% MTD and +3.58% YTD

Nasdaq 100 +4.20% MTD and +5.83% YTD

Dow Jones Industrial Average +1.69% MTD and +1.03% YTD

NYSE Composite +1.53% MTD and +5.19% YTD

The Equally Weighted version of the S&P 500 is +1.58% so far in June, 1.47 percentage points lower than the benchmark.

The S&P 500 Information Technology sector is the top performer so far in June at +7.82% MTD, while Consumer Staples has underperformed at -3.07% MTD.

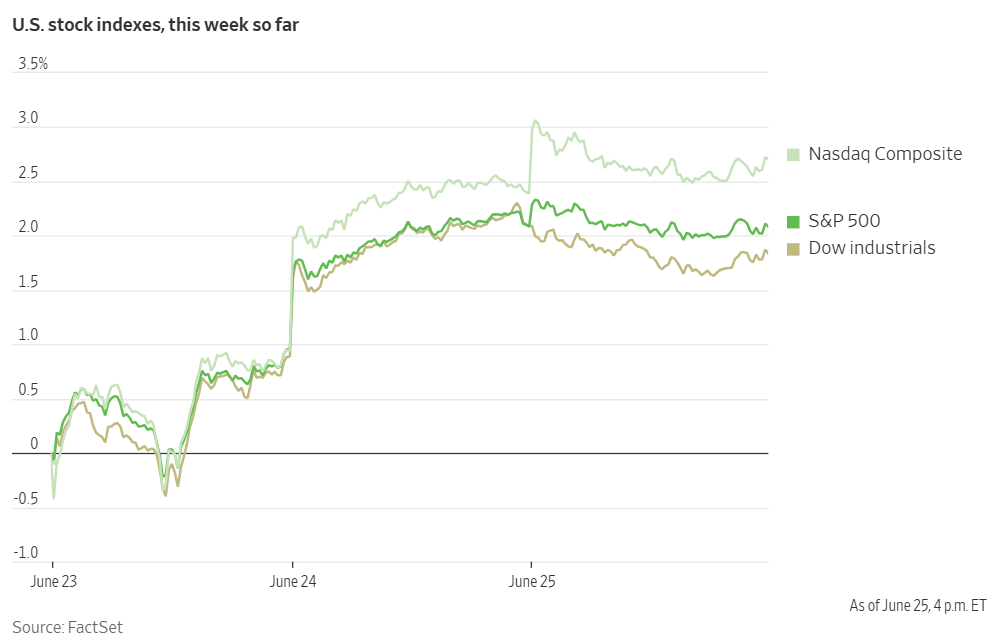

Major US stock indexes finished the session on Wednesday with mixed results. The S&P 500 wavered, ending just a few points shy of its all-time high at 6,092.16, while the Nasdaq Composite edged up +0.31%, leaving both indexes approximately one percent away from their respective record highs. In contrast, the Dow Jones Industrial Average declined by -0.25%, shedding 107 points to close at 42,982.43.

In corporate news, Nvidia once again became the world’s most valuable company with a $3.77 trillion market capitalisation compared with Microsoft’s $3.66 trillion after its shares rose +4.33% on Wednesday. The company's market capitalization has added nearly $1.5 trillion since April. According to the Financial Times, the rally came as Nvidia chief executive Jensen Huang gave a bullish outlook at the company’s annual shareholder meeting on Wednesday about its ability to continue its explosive growth over the next decade.

FedEx issued a cautionary outlook, warning that its profit for Q2 would be below expectations and opting not to provide guidance for the remainder of the fiscal year.

General Mills presented a fiscal year forecast that did not meet investors’ expectations.

Apple is reportedly prepared to implement further changes to its App Store policies. This move is aimed at appeasing EU antitrust regulators who issued an ultimatum after levying a €500 million fine against the company.

Europe:

Stoxx 600 -2.13% MTD and +5.78% YTD

DAX -2.08% MTD and +18.03% YTD

CAC 40 -2.50% MTD and%+2.40%YTD

FTSE 100 -0.61% MTD and +6.68% YTD

IBEX 35 -2.41% MTD and +19.12% YTD

FTSE MIB -1.53% MTD and +15.47% YTD

Source: FactSet

In Europe, the Equally Weighted version of the Stoxx 600 is -1.59% in June, 0.54 percentage points higher than the benchmark.

The Stoxx 600 Oil & Gas is the leading sector in June, +3.47% MTD, while Food & Beverages has exhibited the weakest performance at -7.24% MTD.

On Wednesday, within the STOXX Europe 600 sectors, the Autos & Parts sector outperformed, buoyed by a 1.9% y/o/y increase in European and UK car sales for May. In company-specific news, Aston Martin Lagonda rose on news of resumed US exports. In the parts segment, Continental was downgraded by the sell side after its Capital Markets Day.

Technology also performed strongly, tracking yesterday’s gains on the Nasdaq, which hit a record high for the first time since February. The sector's momentum was supported by robust fundamentals, strong growth prospects, and easing concerns over tariffs.

The Aerospace & Defence sector outperformed as a NATO summit got underway. Within this sector, Babcock International shares rose after reporting a strong Q1 earnings beat, announcing a new share buyback programme, and upgrading its margin guidance. Attention was also on news regarding the UK's procurement of the F-35A jet.

In contrast, the Health Care sector was broadly weak. Philogen shares fell after the company withdrew a drug application. However, there were some bright spots, as Idorsia’s and Evotec’s shares increased due to strategic initiatives.

Utilities also showed weakness, despite some positive developments like Befesa stock receiving an upgrade from Morgan Stanley.

Media was one of the biggest decliners, with WPP in the spotlight after its stock was downgraded due to concerns about the CEO transition and uncertainty regarding the company's execution strategy. Telecom and Real Estate were also notable decliners.

Global:

MSCI World Index +2.24% MTD and +6.53% YTD

Hang Seng +5.09% MTD and +22.01% YTD

Mega cap stocks have had a mostly positive performance in June in reaction to AI momentum. Nvidia +14.19%, Meta Platforms +9.45%, Microsoft +6.93%, Amazon +3.40%, and Apple +0.35%, while Tesla -5.46%, and Alphabet -0.62%.

Energy stocks have experienced a positive performance in June, with the Energy sector +4.40% MTD. Energy Fuels +14.43%, ExxonMobil +5.93%, Phillips 66 +5.42%, Chevron +4.78%, Shell +4.65%, Apa Corp +4.64%, ConocoPhillips +4.28%, Occidental Petroleum +4.02%, Halliburton +3.42%, Marathon Petroleum +3.08%, and Baker Hughes Company +1.43%.

Materials and Mining stocks have had a mostly positive performance so far in June. The Materials sector is +0.87% MTD. Nucor Corporation +17.24%, Sibanye Stillwater +12.62%, Newmont Mining +10.13%, and Albemarle +8.29%, Freeport-McMoRan +8.13%, Celanese Corporation +5.26%, and Yara International +2.84%, while Mosaic -1.83%.

Commodities

Gold is +1.33% MTD in June as Fed credibility, fiscal sustainability concerns and tariff uncertainties weighed on the US dollar. Gold is still +27.23% YTD.

Gold prices remained stable on Wednesday as market participants adopted a cautious stance ahead of the release of crucial US economic data. The ceasefire between Iran and Israel also tempered safe-haven demand, weighing on the precious metal.

Spot gold rose by +0.37% to $3,332.86 per ounce, recovering from its lowest price in over two weeks, which it reached in the previous trading session.

US President Donald Trump revealed the swift end to war between Iran and Israel, articulating his expectation of a future relationship with Tehran that would preclude the reconstruction of its nuclear programme.

Looking ahead, investors are keenly awaiting today's GDP figures and tomorrow's Personal Consumption Expenditures (PCE) numbers.

Oil prices recovered in June after the war between Israel and Iran began on 12th June. However, they were calmed by signs that the Strait of Hormuz would not be shut down, and a fragile ceasefire was announced by the US President. WTI +7.19% MTD and -9.30% YTD and Brent +5.82% MTD and -9.33% YTD.

Following a volatile trading session, oil prices concluded Wednesday with minimal changes, recovering from a significant decline earlier in the week. Brent crude futures settled marginally lower by 17 cents, or -0.25% to $67.62 a barrel, while WTI crude ended up 2 cents, or +0.03%, to $65.16. Both benchmarks pared some of the approximately 13% losses incurred earlier in the week.

The sharp decline was a direct consequence of the ceasefire announcement by the US President on Tuesday. This development reduced Middle East supply risk, leading to Brent settling at its lowest level since 10th June and WTI since 5th June.

Market sentiment was further bolstered by government data released on Wednesday, which revealed a drawdown in US inventories of crude oil, gasoline, and distillates for the previous week.

EIA report. According to the latest EIA weekly report, US crude oil and fuel inventories decreased last week, driven by a rise in both refining activity and demand.

For the week ending 20 June, crude inventories fell by 5.8 million barrels to a total of 415.1 million barrels. Crude stocks at the key Cushing, Oklahoma, delivery hub also decreased, declining by 464,000 barrels during the same period.

The report also highlighted an increase in refining operations. Refinery crude runs rose by 125,000 barrels per day, and utilisation rates increased by 1.5% to 94.7% of total capacity, marking their highest level since July 2024.

Fuel stockpiles also saw notable declines. Gasoline stocks fell by 2.1 million barrels to 227.9 million barrels, while distillate stockpiles, which include diesel and heating oil, decreased by 4.1 million barrels to 105.3 million barrels.

Demand, as indicated by gasoline supplied, also strengthened. This proxy for demand rose by 389,000 barrels per day (bpd) last week, reaching 9.7 million barrels per day—its highest level since December 2021.

Finally, the data showed that net US crude imports increased last week by 531,000 bpd.

Currencies

The dollar has had a particularly challenging June due to concerns over fiscal policy as President Trump’s tax bill is still being negotiated by Congress, the continuing uncertainty over the Trump administration’s tariffs, the US attack on Iran and the pressure on the Fed from the Trump administration. The dollar index is -1.74% MTD and -9.96% YTD. The GBP is +1.50% MTD and +9.44% YTD against the USD. The EUR is +2.71% MTD against the USD and +12.89% YTD.

The US dollar fell to multi-year lows against the euro and British pound on Wednesday as traders reassessed expectations for Fed interest rate cuts and refocused on US fiscal policies. These movements were relatively muted following the sharp drop in the dollar earlier this week, which was triggered by the ceasefire agreement between Israel and Iran.

The dollar had gained strength last week due to concerns over escalating Middle East tensions. This weakening has been exacerbated by growing expectations for more interest rate cuts this year.

Investors are also shifting their focus back to ongoing trade negotiations ahead of the Trump administration's self-imposed 9th July deadline. This deadline was set for negotiating deals with trading partners to avoid the implementation of so-called ‘reciprocal tariffs.’

The euro gained +0.41% to reach $1.1655, its highest level since October 2021. The single currency has also been bolstered by the expectation of increased fiscal spending within the eurozone. Meanwhile, the British pound was +0.38% to $1.3661, marking its highest point since January 2022.

In contrast, the dollar gained +0.21% against the Japanese yen, reaching ¥145.16. A summary from the BoJ's June policy meeting revealed that policymakers advocated for maintaining steady interest rates for the time being, citing uncertainty about the potential impact of US tariffs on Japan's economy.

Cryptocurrencies

Bitcoin +2.85% MTD and +14.43% YTD to $107,625.40.

Ethereum -5.35% MTD and -27.75% YTD to $2,431.74.

Bitcoin was +1.49% on Wednesday and Ethereum was -0.59% Bitcoin has had a positive month largely due to institutional and corporate demand further supporting its price recovery. Spot Bitcoin ETFs have seen continuous inflows since 9 June according to SoSoValue data. And, as noted by CoinShares, digital asset investment products saw their 10th consecutive week of inflows last week, totalling $1.24 billion, with YTD inflows reaching a record $15.1 billion.

A collaborative report by Glassnode and Avenir Group has also shown that Bitcoin is increasingly acting like a macro asset, with its performance now closely tied to broader financial market conditions. Their data shows growing positive correlations with traditional risk-on assets such as the S&P 500, Nasdaq and gold, while inversely tracking the US Dollar Index and credit stress indicators like high-yield spreads.

Note: As of 5:30 pm EDT 25 June 2025

Fixed Income

US 10-year yield -11.1 bps MTD and -28.4 bps YTD to 4.292%.

German 10-year yield +3.2 bps MTD and +20.3 bps YTD to 2.572%.

UK 10-year yield -16.7 bps MTD and -8.4 bps YTD to 4.484%.

US Treasury yields declined slightly on Wednesday afternoon as markets continued to evaluate the potential timeline for interest rate cuts. While yields on longer-term Treasuries rose earlier in the day, they receded during the afternoon trading session.

The yield on the US 10-year Treasury note declined slightly by -0.4 bps. The US 30-year yield was +0.3 bps at 4.839%, registering -9.9 bps MTD. On the short end of the curve, the two-year Treasury yield, which typically reflects interest rate expectations, was -3.8 bps to 3.793%, registering a monthly decline of -11.3 bps.

Fed Chair Jerome Powell addressed a US Senate panel on Wednesday, stating that while tariff plans could cause a one-time price increase, the risk of persistent inflation is significant enough to warrant caution when considering further rate cuts. The debate over the timing of the year's first rate cut has intensified recently, with some Fed officials, including Michelle Bowman and Christopher Waller, discussing the possibility of cuts beginning as early as July.

Looking ahead, several Fed officials are scheduled to speak publicly today, including Richmond Fed Governor Thomas Barkin, Cleveland Fed President Beth Hammack, Fed Governor Michael Barr, and Minneapolis Fed President Neel Kashkari.

Additionally, key economic data is slated for release today and tomorrow. The Commerce Department will issue its final estimate for Q1 GDP on Thursday, and the Labor Department will release initial unemployment claims. The most significant data of the week will be tomorrow's release of the Personal Consumption Expenditure price index for May.

The US Treasury sold $70 billion in 5-year notes. The auction saw tepid demand, with a bid-to-cover ratio of 2.36x. Yields on the 5-year notes remained flat in the afternoon, holding at 3.842%.

Current sentiment in the Fed funds futures market suggests that the Fed is most likely to resume its programme of interest rate cuts in September, with a 89.4% probability of doing so. According to CME's FedWatch Tool, markets priced in 62.2 bps of rate cuts this year on Wednesday, compared to about 47.0 bps a month ago.

Across the Atlantic, eurozone government bond yields increased on Wednesday as investors considered the implications of rising fiscal spending across the region and monitored developments in the Iran-Israel ceasefire.The yield on Germany's 10-year government bond rose by +2.5 bps to 2.572%. Similarly, yields on 30-year German bonds reached a near one-month high of 3.087% before stabilizing +2.5 bps higher at 3.051%. Conversely, the German 2-year yield, which correlates to ECB monetary policy expectations, declined by -1.9 bps to 1.839%.

Italy's 10-year yield rose by +1.6 bps to 3.483%. French 10-year OAT yields rose slightly, by +0.4 bps to 3.256%.

The German 10-year yield is +3.2 bps in June to 2.572%, while the UK 10-year yield is -16.7 bps MTD to 4.484%. The spread between US 10-year Treasuries and German Bunds has narrowed by 14.3 bps from 186.3 bps at the end of May to 172.0 bps now.

Throughout June, the 2-year Schatz increased by +5.8 bps to 1.839%, and on the long end of the maturity spectrum, the German 30-year yield is +7.1 bps.

A decline in risk appetite has led to a widening of yield spreads between the government bonds of highly indebted nations and those of safe-haven German Bunds. Risk sentiment has since improved, and these spreads have narrowed.

The Italian 10 year bond yield, a eurozone periphery benchmark, is -1.8 bps MTD to 3.483%. Consequently, the spread between Italian and German 10-year yields currently stands at 91.1 bps, narrowing by 5.0 bps from 96.1 bps at the end of May.

France’s 10-year OAT yield is +5.8 bps in June to 3.256%. The spread on French government bonds versus German Bunds widened to 68.4 bps, an increase of 2.6 bps from 65.8 bps at the end of May.

On Tuesday, Germany’s cabinet approved a draft budget that includes record investments. This was followed on Wednesday by NATO leaders' endorsement of a higher defense spending target, aiming for 5% of GDP by 2035.

Analysts anticipate that the increased supply of bonds resulting from higher fiscal spending will likely drive long-term yields upward across the euro area. However, the methods for financing this increased spending, particularly for defence, at both national and European levels remain unclear.

Money markets are currently pricing in an ECB deposit facility rate of 1.75% in December, a slight decrease from the 1.80% rate priced on Monday.

Note: Data as of 6:00 pm EDT 25 June 2025

What to think about in July 2025

The new NATO: At the conclusion of this week’s NATO meeting, members have agreed to raise defence spending to 5% of GDP by 2035, up from the long-standing 2% target set in 2014. This confirms that members have accepted that Europe now needs to accept more responsibility for its own defence. Two distinct spending pillars emerged from the meeting that may prove to be extremely relevant to investors.

Firstly, there is the 5% target split to consider. Essentially what this appears to entail is that 3.5% will be allocated for conventional defence including such things as personnel, operations, and most importantly, physical equipment, eg, tanks, aircraft, missiles. This additional spending should, quite obviously, be beneficial for producers of military hardware. The additional 1.5% will be allocated to non-conventional defence: infrastructure protection, cyberdefence, civil resilience, and industrial base support. Modern defence goes beyond military equipment and includes data centres as well as the protection of energy grid, undersea cables, and satellites. This means that this spending will support firms across cyberdefence and critical infrastructure protection. And, as we’ve seen during Covid, supply chains and cyber capabilities need to be protected as disruptions can seriously impact inflation, economic growth and challenge existing geopolitical alliances.

However, as noted by The Atlantic Council, the future of US commitment to European security is still not fully clear. While the United States agreed to communiqué language that reaffirmed an “ironclad commitment to collective defence as enshrined in Article 5 of the Washington Treaty,” during the meeting the US president did not specifically mention Article 5. It was not an unequivocal commitment to NATO’s mutual defence obligations that the president has previously questioned.

The tariff rollercoaster continues. Following the ceasefire between Iran and Israel, investors will once again be focussing on the US self-imposed 9th July deadline for agreements with the EU, China and other nations. It appears that many EU officials see at least a 10% tariff barrier remaining. As noted by Bloomberg news, those sectoral tariffs are based on Trump’s 232 authority, which is expected to be deployed against more industries such as pharmaceuticals and semiconductors. Meanwhile the US and Mexico are still negotiating steel and other tariffs. For Canada, the other partner in the United States-Mexico-Canada Agreement, Prime Minister Mark Carney and Trump agreed on the sidelines of this month’s G7 meeting in Alberta to strike a deal by 21 July. China, although making a preliminary deal in London earlier this month on rare earth metals and exchange students, still has to come to a fuller agreement. Other countries affected by the 90-day pause on reciprocal tariffs, such as Pakistan, are still rushing to negotiate. According to Reuters, after a meeting between Pakistan’s Finance Minister Muhammad Aurangzeb and US Commerce Secretary Howard Lutnick on Wednesday, trade talks between the two nations may be completed next week.

Key events in July 2025

The potential policy and geopolitical risks for investors that could affect corporate earnings, stock market performance, currency valuations, sovereign and corporate bond markets and cryptocurrencies include:

6-7 July BRICS+ Summit, Brazil. The summit will welcome its five newest members and nine partner countries for the second time and will likely look into further expanding the bloc. However Chinese President Xi Jinping will miss the BRICS leaders meeting. Premier Li Qiang will represent Xi at the meeting. Xi’s absence could diminish China’s previous efforts to use the BRICS bloc to expand China’s global influence.

17-18 July G20 Finance Ministers and Central Bank Governors’ Meeting, Zimbali, KwaZulu-Natal. Ongoing global trade tensions, concerns around the impact on global economic growth and increasing pockets of geopolitical uncertainty will likely top the agenda.

24 July ECB Monetary Policy Meeting. The ECB is widely expected to cut rates for an eighth time by 25 bps. However, Governor of the Bank of Greece, Yannis Stournara and Austrian central bank governor Robert Holzmann expect the ECB to pause after this cut while Executive Board member Isabel Schnabel and Bundesbank President Joachim Nagel have also urged caution on further loosening.

29-30 July Federal Reserve Monetary Policy meeting. The Fed, although showing signs of increasing divergence in policy opinion, with at least two policymakers suggesting a rate cut in July being appropriate, while Fed chair Jerome Powell insists that the FOMC still has time to wait and see, is largely expected to keep rates on hold until September. With tariff uncertainty still remaining and with the Bipartisan Policy Center (BPC) suggesting that the federal government risks defaulting on its debt sometime between 15 August and 3 October without action to address its debt ceiling and agree a budget, a notice that is likely to rile bond markets and negatively impact the dollar, the Fed is likely to continue to be cautious despite increasing pressure from the US president.

30-31 July Bank of Japan Monetary Policy Meeting. BoJ Governor Kazuo Ueda said the central bank will continue to raise interest rates if improvements in the economy keep the country on track to durably achieve its 2% inflation target. However, Board member Naoki Tamura has suggested that the bank may need to raise interest rates "decisively" to address inflation risks. In the 14 months since the BoJ abandoned its negative interest rate policy, it has raised rates by just 60 basis points.

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here.