EXANTE Quarterly Macro Insights Q4 2024

Global market indices

Fixed Income

Commodity sector news

Regional news

Currencies

Cryptocurrencies

What to think about in Q1 2025

Economic and Geopolitical Risk Calendar

Q4 review

Global equities were mixed during Q4 with the US steaming ahead following Donald Trump's election victory. This victory put other markets under pressure given his suggested tariffs and fiscal policies. These contributed to global rising yields despite central bank cuts and dollar strengthening. US yields pushed higher on a strong labour market, continued economic growth and an expected rise in spending under the Trump administration. UK bond yields moved higher to price in higher debt issuance and higher inflation following the October budget, and eurozone yields increased on growing political volatility and rising public debt. The Fed lowered interest rates by 25 basis points (bps) in both November and December with the ECB also cutting rates by 25bps in October and December and the BoE cutting rates by 25 bps in November. However, in December there was a stock market sell-off after the Fed reduced the number of interest rate cuts expected in 2025. The Fed’s favourite inflation gauge, the core PCE price index, increased 2.8% year-on-year in November. The US economy remained strong with annualised GDP growth of 3.1% in Q3. Although US labour market data was mixed in Q4 due to distortions from strike actions and hurricanes, non-farm payroll numbers did increase, from just 36,000 in October to 227,00 in November to 256,000 in December, well above expectations and setting the stage for a volatile January.

In the eurozone, shares declined in Q4 as recession fears, particularly in the core EU countries of Germany and France, grew. In the UK, equities also fell over the quarter with businesses losing confidence in the economy following on from promised tax rises in the Autumn budget statement that included an increase in employer National Insurance contributions and the National Living Wage, both due to come into effect in April. Revisions to past data revealed the UK economy had performed more poorly than expected since the summer, with the Office for National Statistics revising down Q3 growth to zero from 0.1% previously.

US Indices for Q4 2024 and YTD

S&P 500 +2.07% QTD and +23.31% YTD

Nasdaq 100 +4.74% QTD and +24.88% YTD

Dow Jones Industrial Average +0.51% QTD and +12.88% YTD

NYSE -2.51% QTD and +13.32% YTD

According to the S&P Sector and Industry Indices, 7 of the 11 S&P 500 sectors were down in Q4. The best performing sector in Q4 2024 was Consumer Discretionary (+14.06%), followed by Communication Services (+8.60%), and Financials (+6.67%), whereas the Materials sector was -12.82%.

It was a mostly positive Q4 for the mega caps, as six members of the Magnificent Seven advanced, Tesla +53.36%, Amazon +17.74%, Alphabet +14.14%, Nvidia +10.58%, Apple +7.48%, and Meta Platforms +2.28%, while only Microsoft at -2.05% in negative territory.

In Q4 Energy stocks were -3.20% due to concerns around demand and lower forecasts. Major stocks were down including Marathon Petroleum -14.37%, Phillips 66 -13.33%, ExxonMobil -8.23%, Halliburton -6.40%, Occidental Petroleum -4.13%, and Chevron -1.65%, in Q4, while BP Plc, Shell, and Baker Hughes were +0.33% and +2.10%, respectively.

Basic materials stocks were -12.82% in Q4. Performance was negative across the board, with CF Industries Holdings -0.56%, Mosaic -8.22%, Albemarle Corporation -9.11%, Yara International -9.97%, Sibanye Stillwater -16.08%, Nucor Corporation -22.37%, Freeport-McMoRan -23.72%, and Newmont Mining -30.36%.

For Q4 2024, the estimated y/o/y earnings growth rate is 11.7%. This would represent the highest growth rate since Q4 2021. However, this estimate has been revised downward from 14.5% as of 30th September, primarily due to lower EPS estimates in seven sectors. Currently, 71 S&P 500 companies have issued negative EPS guidance for Q4 2024, compared to 35 with positive guidance.

Despite these downward revisions, historical trends suggest a potential for stronger growth. Based on the average improvement in earnings growth rate during past earnings seasons, the index may ultimately report y/o/y growth exceeding 14% for Q4 2024.

Over the past four quarters, actual earnings reported by S&P 500 companies have surpassed estimated earnings by an average of 4.9%. With 77% of companies exceeding mean EPS estimates, the earnings growth rate has increased by an average of 2.2 percentage points from the end of each quarter to the end of the corresponding earnings season. Applying this historical trend to the current Q4 2024 estimate of 11.9% suggests a potential actual growth rate of 14.1%.

Indeed, actual earnings growth has exceeded estimated growth in 37 of the past 40 quarters, with the only exceptions being Q1 2020, Q3 2022 and Q4 2022.

The estimated net profit margin for the S&P 500 in Q4 2024 is 12.0%. While slightly lower than Q3's 12.2%, it remains above the year-ago margin of 11.3% and the 5-year average of 11.6%.

Sector-level analysis reveals that six sectors are anticipated to report y/o/y net profit margin increases in Q4 2024, led by Financials (17.7% vs. 13.4%). Conversely, five sectors are projected to experience decreases, led by Energy (7.9% vs. 10.4%). Five sectors are expected to report margins above their 5-year averages, led by Information Technology (26.0% vs. 24.0%), while six are predicted to fall below, led by Materials (8.8% vs. 11.1%) and Health Care (7.7% vs. 9.6%).

Finally, during the week of 13th January, 20 S&P 500 companies, including three Dow 30 components, are scheduled to release Q4 2024 results.

European Indices Q4 2024

Stoxx 600 -2.92% QTD and +5.98% YTD

DAX +3.02% QTD and +18.85% YTD

CAC 40 -3.34% QTD and -2.15% YTD

IBEX 35 -2.38% QTD and +14.78% YTD

FTSE MIB +0.18% QTD and +12.63% YTD

FTSE 100 -0.78% QTD and +5.69% YTD

As of 14th January, according to LSEG I/B/E/S data for the STOXX 600, Q4 2024 earnings are expected to increase 1.9% from Q4 2023. Excluding the Energy sector, earnings are expected to increase 4.8%. Q4 2024 revenue is expected to increase 1.9% from Q4 2023. Excluding the Energy sector, revenues are expected to increase 5.0%. One company in the STOXX 600 has reported earnings by 14th January for Q4 2024, exceeding analysts estimates. In a typical quarter 54% beat analyst EPS estimates and 58% beat analyst revenue estimates.

Seven of the ten sectors in the index expect to see an improvement in earnings relative to Q4 2023. The Real Estate sector has the highest earnings growth rate for the quarter at 78%, while the Consumer Cyclicals has the weakest anticipated growth compared to Q4 2023 at negative 25.2%.

The forward four-quarter price-to-earnings ratio (P/E) for the STOXX 600 sits at 13.0x, below the 10-year average of 14.3x.

During the week of 20th January, 10 companies scheduled to report Q4 earnings.

Analysts expect positive Q4 earnings growth from ten of the sixteen countries represented in the STOXX 600 index. Ireland (284.6%) and Poland (39.9%) have the highest estimated earnings growth rates, while Austria (-22.7%) and Italy (-20.2%) have the lowest estimated growth.

Global Indices

Hang Seng -5.08% QTD and +17.67% YTD

MSCI World +1.67% QTD and +19.33% YTD

Fixed Income

US Treasuries 10-year yield +82.2 bps QTD and +69.5 bps YTD to 4.576%.

Germany’s 10-year yield +23.4 bps QTD and +36.0 bps YTD to 2.369%.

Britain’s 10-year yield +58.9 bps QTD and +102.9 bps YTD to 4.568%.

In December, the Fed cut interest rates by 25 bps, bringing the cumulative reduction since September to 100 bps. While maintaining an easing bias, the Fed signalled a more gradual pace of future rate cuts. The ECB also reduced its key interest rate by 25 bps to 3.00%, leaving the possibility of further reductions in 2025.

US Treasuries ended the year with a negative performance, returning -1.69% in December, following unexpectedly hawkish revisions to the Fed's dot plot. The median projection now anticipates only 50 bps of rate cuts in 2025, compared to the 100 bps previously anticipated in September. This negative sentiment extended to European sovereign debt, with German bunds declining 1.61% and UK gilts falling 2.55%.

Despite expressing confidence in continued easing of inflationary pressures, with the PCE price index rising to 2.4% y/o/y in November, Fed Chair Jerome Powell characterised the decision to lower the Fed funds rate to the 4.25%-4.50% range as a ‘closer call’ than market expectations implied. Driven by robust consumer spending on services, the US economy expanded at an annualized rate of 3.1% in Q3, exceeding the prior estimate of 2.8%.

The eurozone was hit by the collapse of both the French and German governments in Q4 with elections in Germany moved forward to February this year. Rising debt in France caused a widening of the spread between eurozone benchmark bonds (German 10-year Bunds) and French 10-year bonds. In addition, economic growth in Europe appears to be faltering. The ECB has warned of weaker-than-anticipated growth, revising its eurozone growth forecast for 2025 down to 1.1% from the previous estimate of 1.3%, citing heightened uncertainty stemming from the threat of a global trade war. Growth forecasts for 2026 and 2027 were also revised downward.

In the UK, the BoE voted to maintain its policy rate at 4.75%, with a 6-3 vote. However, concerns that restrictive monetary policy could hinder economic recovery intensified following the release of disappointing economic data. UK output contracted in September and October, while business surveys indicate declining confidence. With wage growth remaining robust, as evidenced by a 5.2% y/o/y increase in average weekly earnings in the three months to October, the BoE faces persistent inflationary pressures alongside a stagnating economy. Consequently, the yield on the 30-year UK gilt climbed to 5.18%, its highest level since 2002.

Commodities

Gold spot -0.26% QTD and +27.48% YTD to $2,623.81 an ounce.

Silver spot -7.04% QTD and +21.41% YTD to $28.87 an ounce.

West Texas Intermediate crude +5.37% QTD and +0.77% YTD to $71.72 a barrel.

Brent crude +4.10% QTD and -3.12% YTD to $74.64 a barrel.

Gold markets ended Q4 down after reaching an all-time high of just above $2,800 an ounce in October. However, it logged its best year since 2010 in 2024, up +27.48%, and outperformed all major asset classes. The key drivers for gold in Q4 were central bank purchases offsetting any drops in consumer demand, rising geopolitical risk, and growing concerns around rising inflation following Trump’s election and the potential implementation of tariffs. In addition, Fed rate cuts have contributed to higher net speculative positions in gold and increased holdings in gold exchange-traded funds (ETFs). According to World Gold Council data, flows of global physically backed gold ETFs turned positive in December, adding $778 million. Net speculative positions in gold futures and options have risen significantly since Q4 2023.

The outlook for crude oil in 2025 is characterised by a projected surplus of 0.9 million barrels per day (b/d) due to increased supply, coupled with a substantial spare capacity of approximately 6 million b/d, both of which exert downward pressure on prices. However, notable tail risks exist, including the potential imposition of tariffs by the incoming US administration and ongoing geopolitical uncertainties, which could trigger significant price fluctuations.

While easing energy prices may create incentives for increased drilling activity in the US, a substantial surge in US crude oil production is unlikely. US crude oil supply is projected to rise by only 0.4 million b/d to 13.7 million b/d in 2025, which would be insufficient to offset the potential decline in oil exports resulting from a possible pressure campaign on Iran. Furthermore, core OPEC+ members may be hesitant to fully compensate for lost sanctioned volumes, considering the context of improved diplomatic relations.

Several factors contribute to a bearish outlook for oil. OPEC+ is expected to pivot its strategy towards market defense, returning to a long-run equilibrium focus on strategically disciplining non-OPEC+ supply and strengthening internal cohesion. Additionally, OPEC+ possesses substantial spare capacity of approximately 6 million b/d, providing a buffer that could be deployed to mitigate price surges. Finally, while low shale reinvestment rates suggest capital discipline, slower decline rates and strong operational execution indicate continued robust production volumes from US shale.

Conversely, several factors contribute to a bullish outlook for oil. In the current underinvested environment, OPEC+ possesses inelastic pricing power to defend its fiscal breakeven levels, estimated to be around USD 80 per barrel. Furthermore, depleted Strategic Petroleum Reserves (SPRs) suggest that the US Department of Energy (DoE) will likely replenish its reserves should prices decline, effectively removing crude oil from global markets. Lastly, while geopolitical tensions remain high, the associated risk premium is currently low.

Following deficits in 2023 (-0.4 million b/d) and 2024 (-0.4 million b/d), the market is projected to shift to a surplus of 0.9 million b/d in 2025, driven by surging supply growth (2.1 million b/d) outpacing still healthy demand growth (1.2 million b/d).

Note: Data as of 5 pm EST 31 December 2024

Regional news

The US

While global growth has demonstrated resilience to policy tightening, significant divergences have emerged across countries. The outcome of November’s US election has heightened the risk of these divergences amplifying. Furthermore, the Fed's decision to avoid preemptive action based on assumptions about the incoming administration's policies, coupled with the inherent lags of monetary policy, may hinder its ability to effectively manage the economic consequences of the new president's agenda.

The US has led G7 nations in GDP growth over the past two years. This exceptional performance has generally benefited global growth, with US demand stimulating trade flows and asset prices. Amid promises of expansionary fiscal policy and buoyed by business confidence, the US economy is expected to maintain robust growth in the short term. Additionally, the proposed tariffs on imports could initially boost domestic economic activity by shifting demand from foreign to domestic goods, potentially improving the US trade deficit.

However, these initial positive effects may prove transient and could ultimately reverse. The most significant transmission channel for negative impacts is likely to be the erosion of business sentiment outside the US due to the threat of escalating trade tensions. China is expected to be most directly affected by the new US administration's policies, with potential spillover effects impacting its regional trading partners through weaker demand. While Europe may initially benefit from increased US demand, these gains could be offset by weaker growth in Asia and declining business confidence, particularly if tariffs are extended to European goods.

Within the US, increased demand in an economy already operating at full employment with a positive output gap will likely exacerbate inflationary pressures, which are already above target. Moreover, retaliatory measures from China and Europe could negatively impact US exporters, leading to a deterioration of the trade balance following any initial improvement.

Beyond the temporary initial stimulus, reduced imports and exports may contribute to an overall decline in economic activity. This, in conjunction with higher interest rates necessitated by rising inflation, could ultimately yield limited tangible benefits despite the tariff increases.

The Fed is deliberately avoiding speculation on how the proposed policies, including tariff increases, mass deportations, and tax cuts, might influence monetary policy. While analysing the potential effects of these measures, the Fed will refrain from incorporating them into policy decisions until they are formally enacted.

However, if the administration abruptly implements certain policies, such as those related to tariffs or immigration, the Fed's response effectiveness may be delayed, potentially limiting its ability to fully mitigate the economic impact. Higher import prices and labour shortages resulting from stricter immigration policies could further fuel inflation and elevate inflation expectations, which are already at high levels according to household surveys. This would increase uncertainty and necessitate more aggressive monetary tightening, potentially leading to higher interest rates, particularly if the fiscal outlook deteriorates.

Public debt levels have been rising globally and the US is no exception. US debt has reached record levels, and its long-term trajectory is unsustainable. The Congressional Budget Office (CBO) projects that gross federal debt will exceed 122% of GDP by 2034, surpassing any previous point in US history. The federal budget deficit is projected to widen to -6.3% of GDP in the 2025-2034 period, significantly exceeding the -3.8% average over the past 50 years.

These estimates are likely conservative, as they assume that the corporate and personal tax cuts implemented under the 2017 Tax Cuts and Jobs Act (TCJA), which are scheduled to expire at the end of 2025, will not be extended. Given Republican control of both Congress and the White House, this outcome appears unlikely. If these tax provisions are extended, the deficit would deepen further, and debt could potentially climb above 136% of GDP by 2034. Furthermore, the CBO's projections assume no US recession within the next decade, a return to normal inflation levels, and correspondingly low debt financing costs. The prospect of higher-for-longer interest rates, or in fact a higher neutral rate, poses a significant challenge to debt serviceability. While some investors believe that spending cuts could reduce the deficit, this may not be possible given the degree of mandatory spending within the budget.

Approximately 43.5% of the $6.7 trillion Federal budget is mandatory spending, legally obligated for eligible recipients. This includes Social Security, primarily pensions for retirees, and Medicare, a government-funded health insurance programme for those over 65. Trump has, as of yet, not proposed cuts to these programmes and, in fact, campaigned on expanding Social Security benefits. Furthermore, 14% of the budget is allocated to interest payments on the national debt, a non-discretionary expense.

Discretionary spending, which is not permanently mandated and requires annual approval from lawmakers, represents 42.5% of total spending. While these programs may appear to be easier targets for cuts, they include defense spending (12%), which is relatively inflexible.

Therefore, only 30% of the Federal budget could realistically be subject to significant spending reductions. This portion still includes agencies such as transportation, education, agriculture, and Homeland Security, which provide essential government functions. Notably, the US already allocates a considerably smaller share of its budget to these functions compared to other advanced economies.

High levels of debt ultimately constrain fiscal space and limit the government's ability to respond to economic downturns. Debt also crowds out investments that could promote growth and increases the risk of sovereign distress. Should the administration implement all proposed measures, investor confidence in the risk-free status of US Treasuries could be undermined, potentially leading to increased volatility in the US bond market.

The eurozone

The eurozone continued to experience a slowdown in growth in Q4 with the Composite Purchasing Managers' Index (PMI), which includes both manufacturing and services, remaining below 50 (the point of expansion), coming in at 49.6 in December 2024, following November's 48.3 figure. The weakest performers were the three biggest economies in the bloc, Germany, France and Italy, posting Composite PMIs of 47.5, 48, and 49.7 respectively in December. In contrast, Spain and Ireland saw continued expansions in economic activity in Q4, with private sector output in Spain in December rising at the fastest pace since March 2023.

European government bond performance was significantly influenced by political developments in Q4. Italian government bonds (BTPs) outperformed their French (OATs) and German (bunds) counterparts, as both France and Germany faced political instability.

France experienced a credit rating downgrade by Moody's, which cited ‘political fragmentation’ as a potential impediment to fiscal consolidation. This downgrade followed a no-confidence vote that ousted Michel Barnier's minority government, forcing President Emmanuel Macron to navigate the complexities of forming a new government for the second time this year.

In Germany, the three-party governing coalition collapsed in November after Chancellor Olaf Scholz sacked his finance minister. This paves the way for new elections to be held in February 2025.

Amid concerns that political instability and potential trade conflicts with the US could hinder economic growth in the region, the ECB implemented its fourth interest rate cut of 2024 in December, lowering the deposit rate to 3.00%. Despite these challenges, both European corporate bonds and high-yield debt demonstrated positive performance over the quarter.

Performance across European equities was varied. France's CAC 40 was the weakest performer, declining by -3.34%, additionally, Spain's IBEX fell by -2.38%, while Germany's DAX index increased by +3.02%.

In Q4, sector performance exhibited a distinct bias towards sectors that would benefit from a weakened euro and loosening monetary policy. Sector-wise, Stoxx Euro 600’s top performers included Travel & Leisure +8.00%, Banks +4.72%, Financial Services +2.12%, Insurance +1.26%, and Telecom +0.09%. Conversely, Oil & Gas -0.09%, Industrial Goods and Services -0.40%, Technology -1.84%, Personal & Household Goods -3.11%, Construction and Materials -3.29%, Autos & Parts -3.44%, Utilities -7.25%, Retail -8.17%, Health Care -9.12%, Food & Beverages -9.97%, Basic Resources -10.28%, and Chemicals -11.31% sectors lagged behind.

The Granolas include: SAP with a Q4 return of +15.61%, conversely LVMH -7.70%, Novartis -8.70%, Sanofi -8.90%, ASML -8.97%, AstraZeneca -9.67%, Roche -10.26%, GSK -11.21%, Nestlé -11.86%, L'Oréal -14.97%, and Novo Nordisk -20.67%, all retracted.

The UK

In Q4 the UK economy was hit by rising concerns around stagnation and subdued growth. December’s PMI data revealed the weakest private sector performance since October 2023, with the composite PMI coming in at 50.4 and a sharp decline in new orders. The seasonally adjusted Manufacturing PMI fell to an 11-month low of 47.0 in December, down from 48.0 in November. Business confidence dropped due to rising payroll costs following on from the new Labour government’s first Autumn budget on 30 October with drops in demand leading to the steepest fall in employment since January 2021. The economy grew 0.1% in November, below the forecasted 0.2%, following a 0.1% contraction in both October and September. In the three months to November, the economy registered no growth compared with the previous three months. Output was also flat in the third quarter, a sharp slowdown from the 0.4% expansion in the previous quarter.

UK equities fell over Q4, returning -0.35% due to growing fiscal concerns following on from the Budget and the rise in long-term bond yields. Although interest rates came down over the quarter, there was a re-pricing of future interest rate cuts after Chancellor of the Exchequer, Rachel Reeves, announced a £40 billion tax increase and there were rising concerns over projected borrowing. Consequently, 10-year gilt yields rose, ending the quarter at 4.57%, and the pound depreciated against the dollar. Bond futures markets have now priced in just 2 interest rate cuts in 2025. Core inflation was 2.5% in December 2024, down from November’s 2.6%, with core inflation rising by 3.2% in the 12 months to December 2024, down from 3.5% in November. In addition, the pace of wage growth slowed in December, with services inflation slowing to 4.4% from 5% previously.

Asia ex-Japan

During Q4 2024, Asia Pacific ex Japan equity markets underperformed global equities. Among the larger markets, China, Hong Kong, and South Korea experienced significant declines in local currency terms.

Despite further efforts by authorities to bolster economic activity, China's stock market declined with activity remaining weak due to still falling property prices and weak consumer confidence. These efforts included a substantial $1.4 trillion package to facilitate local government debt refinancing and a 25 bps reduction in the one-year loan prime rate.

South Korea's stock market also retreated amid indications of weakening economic growth and a depreciating Korean won. Financial markets were further unsettled by President Yoon Suk Yeol's unsuccessful attempt to impose martial law in early December.

In contrast, Taiwan and Singapore were among the better-performing markets in the region. Taiwan's strong performance was driven by robust growth in its technology sector. Taiwan remains the best-performing index market in 2024 at +28.47%. South Korea’s KOSPI Index fell by -7.47%, followed by China's Hang Seng Index at -5.08%. The broader MSCI Asia Index fell by -1.09%, while Taiwan's TAIEX Index outperformed with a gain of +3.65%. The MSCI Asia ex-Japan Index recorded a loss of -4.56%.

Emerging markets

The US presidential election results presented a challenge for emerging market (EM) equities during Q4 2024. The MSCI Emerging Markets Index declined in US dollar terms, reflecting investor apprehension regarding the potential impact of the President-elect's proposed tariffs, particularly on China.

Brazilian equities exhibited notable weakness, with the Brazilian real depreciating against the US dollar amid heightened concerns regarding the nation's fiscal trajectory and economic challenges. Equities in South Africa underperformed the broader MSCI Emerging Markets Index.

Within emerging markets, the MSCI Emerging Markets Index generated a loss of -4.56% in Q4 2024. The MSCI India Index fell by -8.89%. The MSCI South Africa index also traded in negative territory, at a -4.16% loss. The FTSE Thailand Index registered a loss of -1.60% in Q4 2024, contrasting with its +12.87% return in Q3.

Performance in Latin America, as reflected by the MSCI Latam Index, was negative at -9.38%. Brazil's Bovespa Index underperformed with a -8.75% loss, while Colombia's MSCI Index outperformed its EM peers at +3.40%. Mexico's S&P/BMV Index also underperformed, registering a loss of -5.65%, as uncertainty surrounding the bilateral relationship with the US weighed on investor sentiment.

Eastern Europe presented a mixed picture. Poland's WIG Index declined by -4.44% in Q4, while Hungary's BUX Index rose by +7.35%. Turkey's BIST 100 Index experienced a modest gain of +0.37%.

Currencies

The US dollar strengthened throughout Q4 of 2024, with the US Dollar Index rising by +7.65% during the quarter and +7.06% on a year to date basis. The rise in the dollar can be attributed to both the strength of the US economy and concerns about potential inflationary pressures due to the incoming President-elect's suggested commercial and immigration policies.

In contrast, the Euro experienced a decrease of -7.01% against the USD during Q4, while the GBP was -6.42% in Q4 on growing divergence of inflationary expectations across the Atlantic. , will amplify in the nearthe slowest to move within its rate cutting cycle. Sterling was the best performing G10 currency against the USD through 2024 but has dropped sharply against the US dollar since the beginning of the 2025.

Cryptocurrencies

Bitcoin +47.68% QTD MTD +122.26% YTD to $93,381.00

Ethereum +28.56% QTD +45.20% YTD to $3,345.56

Crypto markets rose dramatically in Q4 with Bitcoin hitting the $100,000 mark in December 2024 before falling due to a more cautious Fed signalling a slowdown in rate cuts in 2025. The total market cap of cryptocurrencies grew by +45.7% in Q4, ending the quarter at $3.91 Trillion according to CoinGecko data.

Bitcoin and other cryptocurrencies were bolstered by President-elect Trump’s promises to create a national Bitcoin reserve, to ensure the federal government never sells off its Bitcoin holdings, to support US-based Bitcoin mining, and to create a more friendly regulatory environment at the Securities and Exchange Commission (SEC). Bitcoin ETFs saw $16.5B of net inflows in Q4, with the majority going to BlackRock and Fidelity while some ETFs registered outflows during the quarter. Bitcoin was also supported over the quarter by increased purchases from corporate investors such as MicroStrategy, which purchased 1070 Bitcoins over Q4.

Note: As of 5:00 pm 31 December EDT 2024

What to think about in Q1 2025

What is becoming increasingly clear is that geopolitical risks and market volatility are likely to increase in Q1. This is due to the uncertainty surrounding Trump 2.0 with his possible tariff restrictions resulting in heightened trade and geopolitical frictions as well as the strong likelihood that the Fed will not be cutting rates more than once in 2025,

There are still concerns around the frothiness of equity markets. FactSet estimates that the S&P 500 will achieve a y/o/y earnings growth rate of 14.8% for the 2025 calendar year. This projection surpasses the trailing 10-year average (2014 - 2023) of 8.0%.

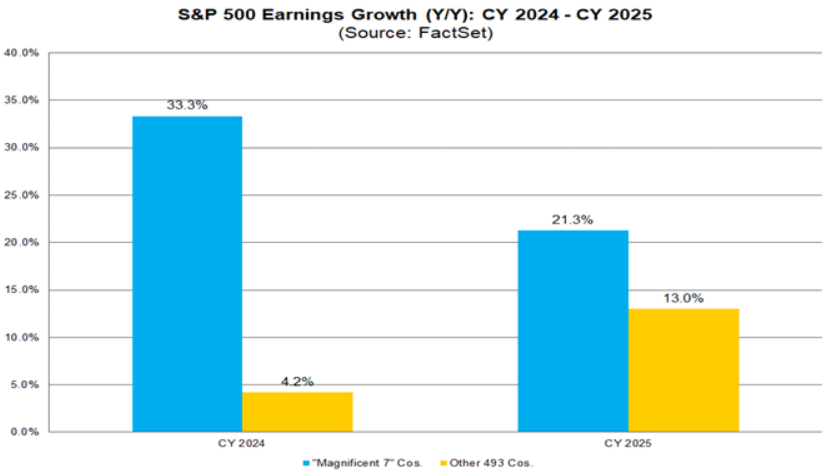

Notably, analysts anticipate significant earnings growth improvement in 2025 for companies beyond the Magnificent Seven. While these seven companies are predicted to achieve 21% earnings growth, the remaining 493 companies in the index are expected to see 13% growth. This figure represents a substantial increase from the anticipated 4% earnings growth for these companies in 2024.

All eleven S&P 500 sectors are projected to report y/o/y earnings growth in 2025. Six sectors are poised for double-digit growth: Information Technology, Health Care, Industrials, Materials, Communication Services, and Consumer Discretionary. Furthermore, both the Financials and Utilities sectors are projected to achieve growth of 9.0%.

The estimated net profit margin for the S&P 500 in 2025 is 13.0%, exceeding the 10-year average of 10.8%. Should this materialize, it would mark the highest annual net profit margin since FactSet began tracking this metric in 2008, surpassing the current record of 12.6% set in 2021.

As of 10th January, the 12,301 stock ratings within the S&P 500 were distributed as follows: 54.5% Buy, 39.7% Hold, and 5.8% Sell. Energy (63%), Communication Services (62%), and Information Technology (62%) boast the highest percentages of Buy ratings, while Consumer Staples (41%) has the lowest.

In 2025, investors should anticipate more divergent global growth outcomes compared to 2024. Uncertainties in trade policy, particularly concerning Europe, China, and potentially the US, present downside risks to growth. This divergence is also projected within regions. For instance, Germany's automotive and manufacturing sectors are facing increased competition from China, while Portugal, Greece, and Spain are experiencing growth fueled by tourism, Recovery Fund disbursements, and expansion in high-value services. While recent stimulus measures in China have mitigated downside risks by addressing structural debt imbalances among local governments, new uncertainties have emerged surrounding US-China trade relations. Encouragingly, Chinese policymakers have adopted a more pronounced pro-growth stance, and investors will be closely monitoring policy actions aimed at managing debt imbalances and stimulating domestic demand.

Every major developed market (DM) economy is poised to enter 2025 with lower inflation than at the beginning of 2024. The stabilisation of goods and energy prices, anchored inflation expectations, and the slow normalisation of wages are all contributing to disinflation in the services sector. Energy prices, however, face two-sided risks: geopolitical instability could disrupt supply and drive prices upward, while the easing of regulatory hurdles for US oil and gas production could exert downward pressure.

The US inflation trajectory faces three primary upside risks, all connected to potential policies of the President-elect’s administration. The first is a genuine reacceleration of the economy, which is currently tracking above 2% growth and could be further stimulated by pro-growth policies such as deregulation and tax cuts. The second risk stems from the potential imposition of across-the-board tariffs, although this is not the base case most analysts expect, downside growth risks might outweigh the one-time price increase. The final risk involves substantial restrictions on immigration and deportations, which could trigger a labour supply shock. However, logistical and resource constraints limit the likelihood of this outcome. Among these risks, a reacceleration of economic growth is the most significant concern.

In 2024, G10 central banks implemented a cumulative 800 bps of policy rate cuts, a reversal from the 1,200 bps of rate hikes in 2023. Currently, seven G10 central banks are engaged in monetary easing cycles. The ECB has implemented four rate cuts, the Fed three, and the BoE two. Smaller central banks, such as the SNB and the BoC concluded 2024 with 0.50% adjustments. More rate cuts are anticipated in 2025, although the pace and ultimate level of adjustments will diverge among countries. The BoJ stands alone as the sole hiker, driven by a virtuous cycle between wages and prices and with policy rates still exceptionally low at 0.25%. The UK is facing one of the weakest growth trajectories, despite the expansionary Autumn budget, reflecting the anticipated negative impact of the rise in national insurance contributions on hiring. Consequently, the BoE is projected to ease more aggressively than currently implied by its projections and market pricing. Open economies, such as the Euro area, may be more susceptible to heightened trade policy uncertainty, potentially dampening business investment and broader growth and inflation outcomes, leading policy rates below estimated neutral levels.

The potential US policy mix complicates the Fed's path, but the health of the economy is expected to take precedence in driving policy in the near term. As the year progresses, the inflation and labour market ramifications of new policies should become clearer, helping to determine whether the Fed’s easing cycle will conclude or be extended.

The first 100 days of the Trump administration will be critical for assessing legislative priorities. If implemented, tariffs could impact growth and inflation through various direct and indirect channels. A universal increase in tariffs would pose the primary risk to global expansion and financial markets. Predicting the international response and any retaliatory measures to higher tariffs is challenging. China is likely to be the initial target for US tariffs, which would exacerbate existing domestic challenges stemming from the housing downturn. Since the 2018-19 trade war, Chinese policymakers have developed potential retaliatory measures, including a ban on exports of several rare earth minerals to the US. Recent policy rhetoric reflects a reinforced pro-growth stance. However, the extent and effectiveness of the stimulus remain uncertain.

In Europe, a one-off tariff shock would likely have a more substantial impact on growth than on inflation, necessitating further monetary easing. If universal tariffs trigger a global trade war, investors will need to assess the impact on supply chains and any associated fiscal easing offsets to determine whether the hit to demand or supply predominates. The latter scenario would be inflationary and complicate the ECB's response.

The substantial increase in public debt following the Covid-19 pandemic, combined with limited prospects for near-term fiscal consolidation and political uncertainty, could lead to volatility in sovereign bond markets, as observed in the UK in 2022 and France in 2024. The experience in France underscores the political challenges associated with enacting fiscal consolidation, which can heighten policy uncertainty and weigh on investment and economic activity. However, political change can also catalyze an expansion in fiscal measures that may unlock growth opportunities. Germany stands out as a key example in this regard. Possessing the largest fiscal space among major developed markets, Germany's debt-to-GDP ratio is 64%, compared to over 120% in the US. The constitutional debt brake rule restricts the cyclical deficit to 0.35% of GDP, requiring a two-thirds parliamentary majority for amendment. Germany has underperformed its peers in recent years due to the drag on industrial activity from high energy prices and China's evolution from a key export market to a primary competitor. The upcoming election in February could expand fiscal options, potentially leading to increased investment spending and a revitalization of the economy. This would benefit the broader Euro area and help mitigate potential headwinds from a more hawkish US trade policy.

Economic and Geopolitical Risk Calendar

In addition to monetary and fiscal policy changes, there are other factors that could affect market performance in Q1 2025. Geopolitical tensions remain high with President-elect Trump continuing to pressurise NATO allies to increase their contributions. There is also the continuing war in Ukraine along with a rising risk of confrontation with China over its claims around the Spratly Islands in the South China sea. Traders will be focussed on the potential consequences of expected changes in tariff policy and tax policy, as well as the growing concerns around the debt ceiling, market liquidity and potential shifts in fiscal policy and debt sustainability.

Other potential policy and geopolitical risks for investors that could negatively affect corporate earnings, stock market performance, currency valuations, sovereign and corporate bond markets and cryptocurrencies include:

January 2025

1 January Canada takes over the G7 Presidency. With Prime Minister Justin Trudeau resigning on 6 January and the country's parliament suspended until 24 March while a new leader is chosen, this may make coordinating G7 policies a bit more difficult. Canada is set to host the G7 Leaders' Summit in June 2025.

20 January Presidential inauguration, USA. Donald Trump will be once again sworn in as US president.

24 January Bank of Japan Monetary Policy meeting. The BoJ is looking increasingly likely to raise rates at this meeting with Governor Kazuo Ueda suggesting on 15 January that the central bank would raise rates if broadening wage hikes underpinning consumption and allowing companies to keep hiking prices for goods and services continues. .However, the BoJ has been monitoring the potential moves by President-elect Trump and will likely only raise rates at this meeting if nothing that will create global volatility emerges in Trump’s inauguration speech on 20 January

29-30 January ECB Monetary Policy meeting. With growth in key member states France and Germany remaining low, despite inflation rising to 2.4% in December and likely to remain above target, the ECB will have to balance out the risks of restrictive policy on growth.vs potential inflation pressures stemming from energy markets and US trade policies. The ECB is expected to continue its rate cutting cycle with 3 to 4 cuts this year.

31 January - 1 February Federal Reserve Monetary Policy Meeting. Although December’s lower than expected PPI and CPI numbers brought some relief,with core CPI increasing by 0.2% after rising 0.3% four straight months, the stronger than expected December NFP report of 256,000, makes it highly unlikely that the Fed will look to cut rates again at this meeting. A strong labour market and continuing growth means inflation is still above target. Policymakers will also wish to consider the implications of any new tariffs imposed by President-elect Trump.

February 2025

6 February Bank of England Monetary Policy Meeting. With inflation falling slightly in December and stagflation concerns growing, there may be more room for the BoE to cut rates again. However inflation is expected to rise again in the first half of the year due to higher energy prices and still strong wage growth.Two rate cuts have been priced in for this year by the market, but much will depend on the implementation of tariffs by the Trump administration and the consequent impact that would have on UK yields and the GBP. The BoE is likely to continue to take a gradual approach given these persistent inflationary pressures.

March 2025

5-6 March European Central Bank Monetary Policy Meeting. The ECB there will still likely be some degree of concern about core inflation stickiness.

18 March Bank of Japan Monetary Policy Meeting. The BoJ will be closely monitoring the growth in wages and service price trends. If a rate rise is not implemented in January, it is likely to be implemented in March.

20 March Bank of England Monetary Policy Meeting. The BoE MPC may decide that the risks to economic growth are greater from a higher policy than the return of inflation. Given growing stagflation concerns, with businesses likely to become ever more cautious due to the implementation of tax rises announced by the government last fall, which are due to come into effect in April, the bank will likely feel pressured to cut rates at this meeting. It will most likely consider the stickiness of wage inflation before making any more cuts..

21-22 March Federal Reserve Monetary Policy Meeting. The Fed will be watching for inflationary pressures from a still strong labour market. The economy is projected to continue to grow despite the high rate environment with price pressures remaining on the high side. As long as there is no significant weakening of the labour market, the Fed is unlikely to cut until June at the earliest.

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

Tento článek je poskytován pouze pro informační účely a neměl by být považován za nabídku nebo výzvu k nákupu nebo prodeji jakýchkoli investic nebo souvisejících služeb, jejichž odkazy se v něm můžou vyskytovat. Obchodování s finančními nástroji je spojeno se značným rizikem ztráty a nemusí být vhodné pro všechny investory. Dřívější produktivita není spolehlivým ukazatelem budoucí produktivity.

Přihlásit se k odběru přehledů trhu

Přihlásit se k odběru

přehledů

trhu

Předplaťte si nyní

Založeno profesionály. Pro profesionály.