- The market's attention will be on the November NFP on 6 December. October core PCE was in line with consensus, rising 0.3% m/o/m, while September core PCE was unrevised at 0.3%. On an annualised basis, core PCE was 2.8%, in line with consensus.

- The dollar index has risen for the majority of November and closed at 106.87 yesterday. It is more than +5% YTD and +2.38% this month. The dollar has been rallying on expectations that President-elect Donald Trump will, as threatened during his campaign and suggested again on 25 November, increase tariffs on the US’ main trading partners, thereby pushing inflation upwards and limiting the Federal Reserve’s ability to cut interest rates. The US labour market continues to show strength with the latest jobless claims falling by 2,000 to 213,00 in the week ended 23 November according to the US Labor Department. However, continuing claims were at 1,907,000, above consensus and near a three-year high.

- On the growth front the US continues to expand. GDP increased at a 2.8% annualised pace in Q3 , the second estimate of the figures from the Bureau of Economic Analysis showed today. It was driven by consumer spending which advanced 3.5%, the most this year. The Flash Composite PMI in November increased to 55.3 from October’s 54.1, highest level since April 2022. Higher activity reflected rising demand, with new orders picking up sharply to register the strongest upturn in business inflows since May 2022.The Flash Services PMI jumped to 57.0 from October’s 55.0, a 32-month high. However the manufacturing sector remains in contractionary territory, with the Flash US Manufacturing PMI coming in at 48.8. Although a 4-month high, it was only slightly up from October’s 48.5.

- In addition, consumers are feeling more confident. The Conference Board's consumer confidence index increased in November to 111.7, up 2.1 points from 109.6 in October. The Present Situation Index—based on consumers’ assessment of current business and labor market conditions, increased by 4.8 points to 140.9. The Expectations Index, based on consumers’ short-term outlook for income, business, and labor market conditions— ticked up 0.4 points to 92.3, well above the threshold of 80 that usually signals a recession ahead. According to Dana M. Peterson, Chief Economist at The Conference Board, November’s increase was mainly driven by more positive consumer assessments of the present situation, particularly regarding the labour market. Compared to October, consumers were also substantially more optimistic about future job availability, which reached its highest level in almost three years. Meanwhile, consumers’ expectations about future business conditions were unchanged and they were slightly less positive about future income.

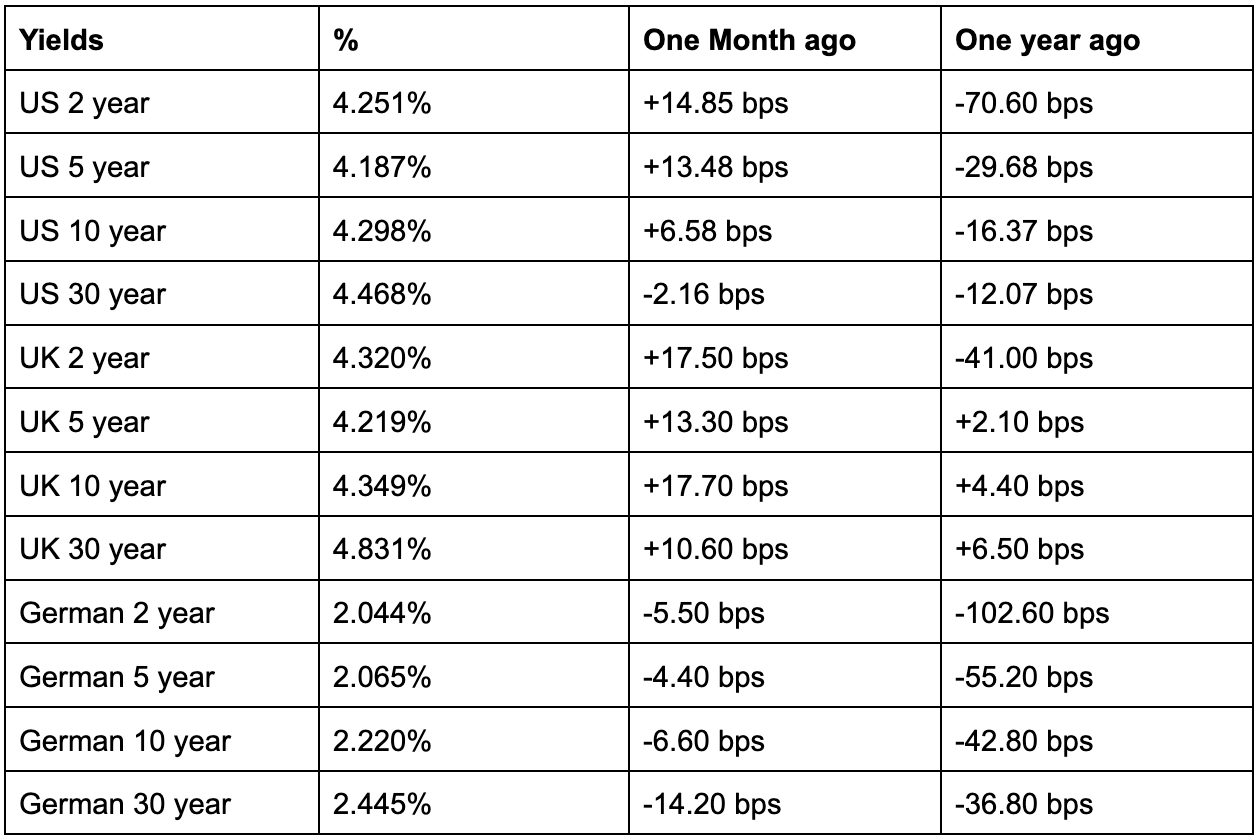

- Treasury yields steepened this month as investors focused on the election of Donald Trump and the risk his declared intentions in relation to tariffs and tax cuts may bring. There are concerns that the rise in bond yields may derail the Fed from being able to cut rates further in the business cycle. The yield on the 2-year Treasury note, which is highly sensitive to movement of the Fed Funds rate, had risen from 4.095% on 29 October to 4.251% on 26 November. The benchmark 10-year US Treasury note yield has also continued to rise. It ended on 26 November at 4.298%, up from October’s 4.255%, while the yield on the 30-year bond had also risen from September’s 4.084% to 4.488%. According to the CME FedWatch tool, there is a 66.5% chance of a 25-basis-point cut at the December meeting.

Yield swings

US Treasury yields have climbed since the election of Donald Trump and on signs of a still resilient US economy.

Source: FactSet

Source: FactSet 5:15 PM EST 26 November 2024

Global Economic and Market Review

US yields have largely been rising since September. This has had a significant impact across major developed and emerging market sovereign bonds. In the UK, the situation for bond markets has been even more difficult following the release of the Labour government’s budget on 30 October. Yields have risen despite the BoE cutting rates by 25 bps to 4.75% during its 6 November meeting on expectations of further debt issuance and tax rises hitting business investment, employment, and growth. Inflation rose in October with the headline rate rising by 2.3% in the 12 months to October 2024, up from 1.7% in September. On a monthly basis, inflation rose by 0.6% in October 2024. Core CPI (excluding energy, food, alcohol and tobacco) rose by 3.3% in the 12 months to October 2024, up from 3.2% in September; the CPI goods annual rate rose from negative 1.4% to negative 0.3%, while the CPI services annual rate rose from 4.9% to 5.0%.

The UK economy appears to be stagnating. The Flash Composite PMI fell into contractionary territory in November, falling to 49.9, down from October’s 51.8 and a 13-month low. The survey suggested that a loss of confidence was driven partly by the payroll tax increase on businesses announced in the 30 October budget. Firms’ expectations for activity in the year ahead were the most pessimistic since late 2022. The Flash Services PMI also dropped to 50.0, down from October’s 52.0 and also a 13-month low. The Flash Manufacturing PMI continued to fall and reached a 9-month low, hitting 48.6 and down from October’s 49.9. However, consumer confidence is actually increasing, with the GfK Consumer Confidence Index for November up by 3 points to -18, marking its first improvement in three months. This gain may be attributed to the BoE’s second rate cut earlier this month, bringing the interest rate to 4.75% in November, while wage growth continued to outpace inflation.

However, although the likelihood of further rate cuts still exists, it is highly unlikely to happen in December. Any further cuts will be gradual as there are still concerns for BoE policymakers as labour market data continues to show inflationary pressures. Pay growth excluding bonuses slowed to only 4.8% in the three months through September. While the pace was the slowest since mid-2022, it is still too high for the BoE’s 2% target BoE Deputy Governor Clare Lombardelli said the UK has made “good progress on disinflation” but “the more persistent components of inflation and uncertainties around how the labour market will evolve are cause for concern.”

In the eurozone, markets are fully expecting a further 25 bps cut at December's meeting while also pricing in a 50% chance of a 50 bps cut. Eurozone inflation rose in October to 2.0%, up from 1.7% in September. Core inflation, excluding volatile items such as food, energy, alcohol, and tobacco, remained at 2.7% in October. Services inflation rose to 4.0% from September’s 3.9%. According to Factset estimates, eurozone headline inflation in November, due to be reported on 29th November, ahead of the 12 December ECB meeting, is forecast to be 2.4% higher than November 2023 levels, while core inflation, is expected to stay stable at 2.9% year on year in November, in line with October’s reading. On the growth front, the eurozone Flash Composite PMI came in at 48.1, down from October’s 50.0 and a 10-month low. The Flash Eurozone Services PMI was also at a 10 month low, at 49.2, down from October’s 51.6. (October: 51.6). 10-month low. The Flash Eurozone Manufacturing PMI was also lower, at 45.2 from October’s 46.0. The poor growth figures have fed concerns about the prospects for the eurozone and the euro. Markets are already worried about the collapse of Germany’s government and the early elections in February, the increasing chance of a collapse in the French government, and the threatened trade tariffs from the next Trump administration. It is also worrying that the French bond market may be on the brink as the premium investors demand to hold 10-year French government bonds over German bonds has reached the highest level since 2012. The potential fall of the current government could drive it higher.

However, unlike much of the world, yields in the benchmark German 10-year yield fell in November as expectations of further rate cuts by the ECB came to the fore. The German 10-year yield was -6.60 bps as of 26 November at 2.20%, while the UK 10-year yield was +17.70 bps as of 26 November at 4.349%. The spread between US 10-year Treasuries and German Bunds expanded by +22 bps over the month. It stands at 208, significantly up from October’s 192.76 bps. The gap between Italy and Germany's 10-year yields, a gauge of investor sentiment towards the eurozone's more indebted countries, is, according to Worldgovernmentbond.com, now at 126.7 basis points,up from September’s 121.7 basis point differential.

Global bond markets are likely to continue to remain volatile in Q4 as more of President-elect Trump’s cabinet nominations and policy measures are announced. The slowdown in Europe along with growing concerns around the UK’s future growth given the negative reception by businesses and investors to the budget, are likely to contribute to currency depreciation in the euro area, while the Pound Sterling may also come under pressure on growth fears and the population’s growing dissatisfaction with the new government. Although a ceasefire has been brokered between Israel and Hezbollah in Lebanon, the risks of widening tensions in the Middle East have not fully dissipated, particularly as President-elect Trump has suggested a more aggressive stance towards Iran, harking back to his “maximum pressure” policy his previous administration imposed against Iran. There is still the ongoing war in Ukraine which has seen an escalation in recent weeks. And of course, there are still signs of growing trade fragmentation due to rising tariffs between the US, Europe and China, which will continue to affect yields and, in turn, the US dollar. There are also unresolved policy issues related to immigration that will affect labour markets, government revenues, and fiscal priorities. In addition, it is not clear if the stimulus package by China to address the problems of the country’s local government debt held off balance sheets and lay the foundation for sustainable growth will really work.

Given the expected high level of volatility that will likely play out in bond markets over the next few months, investors may wish to consider adding in some inflation protection into their portfolios along with yield-spread targeting. Although the ECB is likely to continue to cut rates it will worry about the value of the euro and the likelihood that it will reach dollar parity if the Fed maintains a high rate environment.

Key risks

- Inflation risks re-emerge, weighing on asset prices. Inflation had been falling in the UK and in the eurozone but now appears to be on the up once again as rising energy prices and still above the central banks target wage increases pile on inflationary pressure. There are also risks that headline inflation may rise due to some commodity prices rising if the tariffs threatened by Donald Trump do indeed come into being.

- Policymakers over or undershoot. Central banks are being very cautious about getting the balance between supporting their economies while fighting future inflation risks. In Europe there have been warnings that the ECB could undershoot the inflation rate (causing people to delay spending and further weakening economic growth). The dollar is likely to be supported by higher yields on rising inflation expectations (should tariffs come into being as suggested). This means that we will see a growing monetary policy divergence between Europe and the US, with the UK caught in the middle.

- Geopolitical tensions and events. Tensions in the Middle East are still high and likely to go higher once Trump is sworn in. The continuing war in Ukraine is still a large risk for European economies. The tensions in the South China Seas between China and the Philippines remains an issue as does the relationship between China, Taiwan, and the US. The Trump administration is expected to take on a more strategic and business-driven approach and will likely push for increased militarisation of the Asia-Pacific region leading Chinese authorities to ramp up their own preparations for any conflict.

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

Dit artikel wordt u alleen ter informatie verstrekt en mag niet worden beschouwd als een aanbod of uitnodiging tot het kopen of verkopen van beleggingen of gerelateerde diensten waarnaar hier mogelijk wordt verwezen. Handelen in financiële instrumenten omvat een aanzienlijk verliesrisico en is mogelijk niet geschikt voor alle beleggers. In het verleden behaalde resultaten bieden geen betrouwbare indicatie voor toekomstige resultaten.