.png)

About this report

This report provides a brief overview of the forces shaping change in emerging markets (EMs) as many are not just commodity producers, but increasingl important consumer markets in themselves. We consider the changing relationship between EM currencies and the USD and how the quest for renewables are changing emerging markets as well as the valuation of their currencies.We also review the potential impact of ESG investing on emerging markets growth and currencies. Finally, we consider how all of these factors may combine and what core risks still remain for investors into the EM space.

Executive Summary

Emerging markets provide the largest share of global growth, with access to a large and growing middle class, emerg-ing markets can provide attractive growth prospects and potential diversification benefits for portfolios.

However, the change to monetary policy in developed markets will be slow and this will continue to impact emerg-ing market economies. Despite better GDP forecasts for emerging markets, the poorer-than-expected data coming fromthe world’s largest emerging market, China, will worry investors in EM equity indices, affecting valuations in other EMs.This slowdown will also hit commodity producers in emerging markets that are reliant upon China as a source of demand.

There are some points of hope for EMs:

- The shrinking regulatory timeframes for decarbonisation and the push by investors for ESG products will also be supportive to EM growth and their currencies. Growing demand for commodities that will be required in the green transition, both in green energy production and supply as well as in transport and infrastructure, telecommunications and IT products.

- Many EMs, due to fiscal prudence during the pandemic, have less new debt than Developed Markets. They have grown their reserve balances and accumulated higher stocks of foreign exchange reserves. Many have also shifted out of dollar-denominated debt, reducing vulnerability to currency fluctuations.

- The end of global rate hikes will help reduce volatility, which will benefit higher-yielding EM currencies and bonds.

For investors it must be remembered that investing in emerging markets is often associated with particular domestic political risk factors, greater geopolitical risks, and more volatile economies with higher currency risks. Another con-sideration that will impact the future growth of EMs is the security of supply chains, especially as a trend towards in-creasing export restrictions may be playing a role in key international markets, with potentially sizable effects on both availability and prices of these materials.

In short, there is both caution and hope in the knowledge that Emerging markets is a wide-ranging asset class that may offer yield and returns that their developed market comparators cannot.

Setting the scene: Current situation

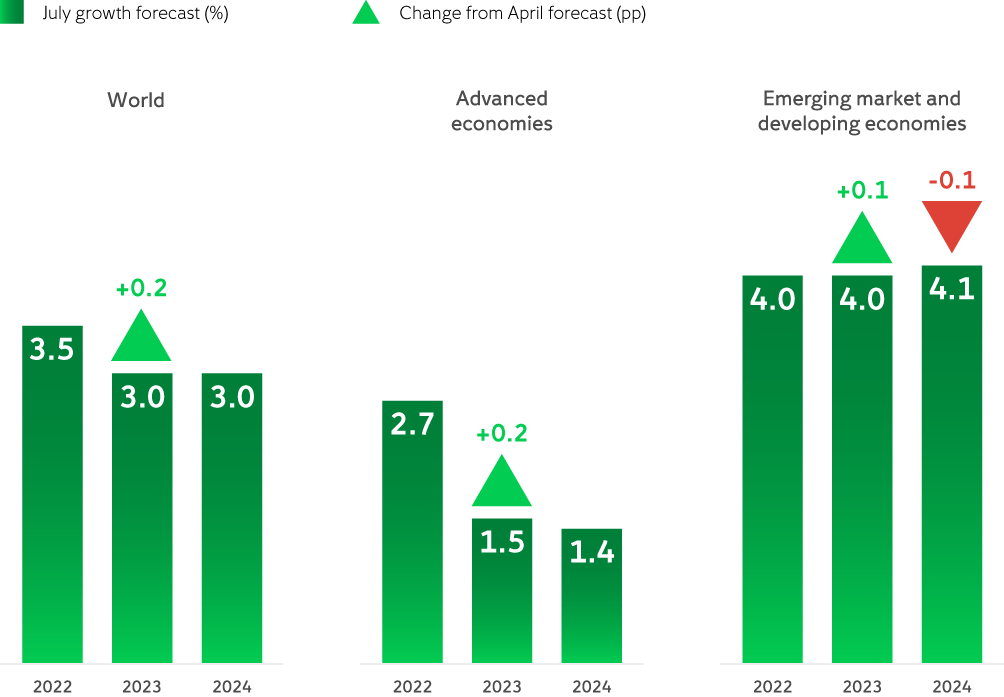

The Emerging Market (EM) landscape is very diverse. As noted by the IMF, emerging markets are generally identified based on such attributes as sustained market access, progress in reaching middle-income levels, and greater global economic relevance. They are characterised by faster growth than Developed markets (DMs) such as the US, UK and Europe, and relatively rapidly changing economic structures provide diverse investment opportunities. Growth has been stronger in EM markets than in DMs.

Chart 1.

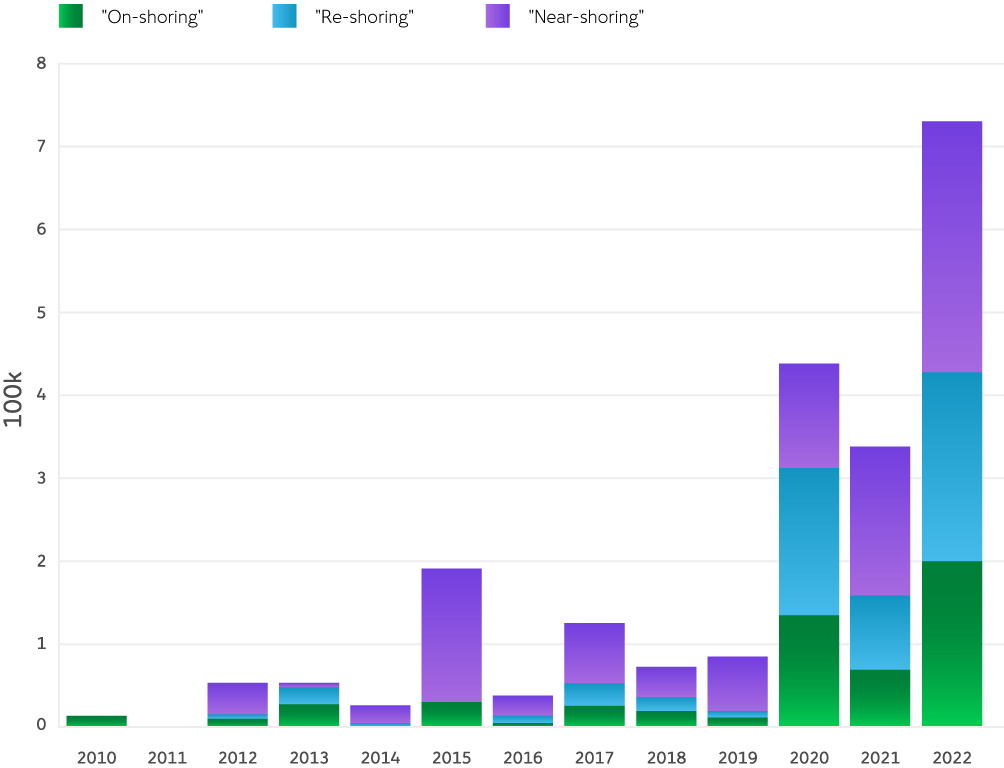

It is also likely over the next several years that EMs will increasingly be affected by the growth in reshoring (bringing production home) or “friend” shoring (sourcing inputs from suppliers in allied countries) in order to secure access to critical production inputs. Examples of this include, as noted by the ECB, China’s “dual circulation” strategy, the US Chips Act, and the European Union’s (EU’s) “open strategic autonomy.” As noted by HSBC, although firms may be talking more openly about the need to ‘nearshore’ or ‘reshore’ in earnings calls and surveys, the data suggest this process is yet to begin in earnest beyond some small moves from some manufacturers and some industries (such as semiconductors) seeing a more focused push to improve supply chain resilience.

Chart 2. Companies mentions of…

Source: Federated Hermes, HSBC, Asian Economics as of January 2023.

The US inflation problem and EMs

The US dollar has been appreciating since 2022. According to the IMF, in emerging market economies, a 10% US dollar appreciation, linked to global financial market forces, decreases economic output by 1.9% after one year, and this drag lingers for two and a half years.

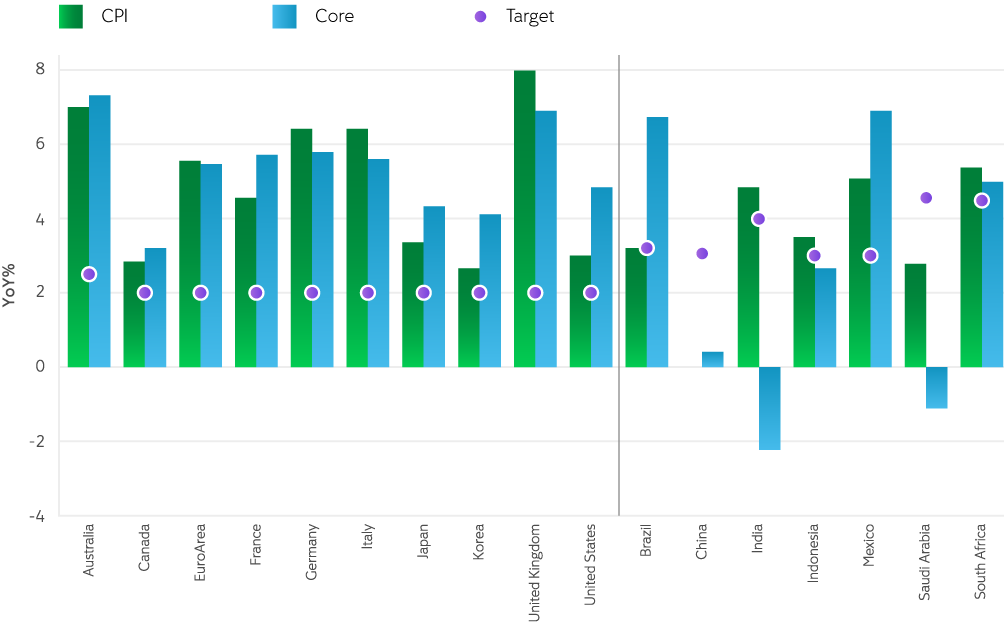

Despite continuing interest rate rises across the globe, fading base effects and falling producer prices indicate disinflation. However, core inflation remains well above target in Developed Markets (DMs) and it is clear that it will take longer for it to come down, particularly as service sector activity increases and demographic change means that labour market participation is not expected to grow significantly.

Chart 3. G20 Inflation vs Target

For EMs the situation is slightly different as EM central banks were generally quicker to react to inflation by tightening monetary policy sooner in the business cycle. Also, EMs largely did not have the fiscal outlays that many DMs experienced during the Covid pandemic. The fiscal prudence led to less new debt than in the US and other DMs and better external balances. They have grown their reserve balances and accumulated higher stocks of foreign exchange reserves. Many have also shifted out of dollar-denominated debt, reducing vulnerability to currency fluctuations. Emerging market currencies, such as the Mexican peso and Brazilian real, have strengthened versus the dollar, while their developed market peers (e.g., the Euro and Yen) have weakened since the start of the US Fed hiking cycle in 2022. And the spread between long-term emerging and developed market interest rates has stayed compressed.

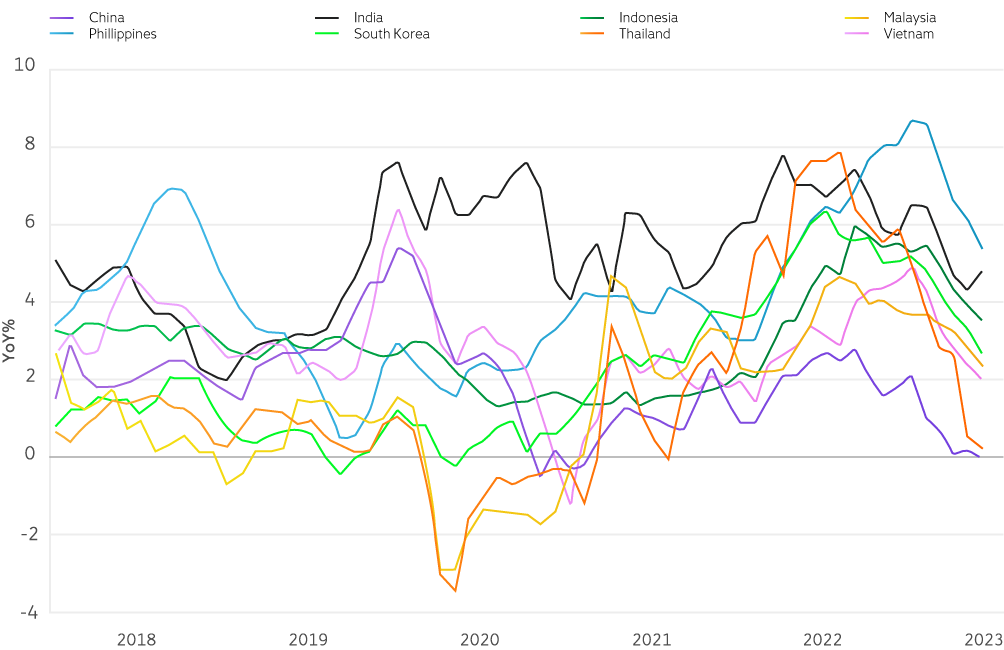

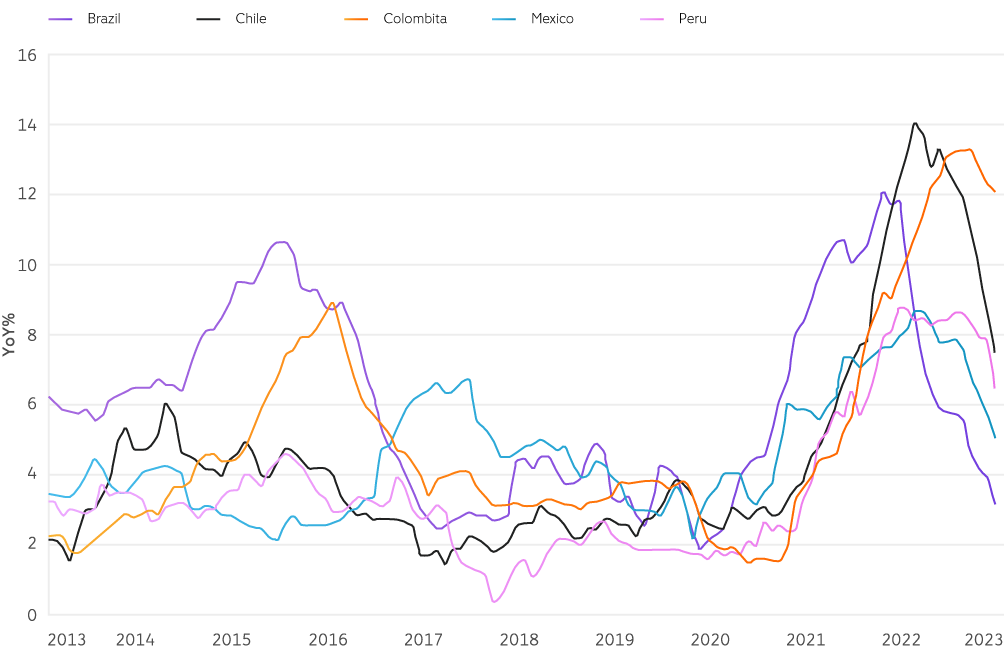

Chart 4. Inflation in Emerging Asia

Chart 5. Inflation in Latin America

Although developed market economies, namely the US, have managed to avoid recession this year, the slowdown that is starting to play out there is expected to hit emerging markets going into the second half of 2023. As noted by S&P, July's PMI data showed emerging markets expanding at the slowest pace in six months, supported chiefly by service sector growth as manufacturing output near-stalled. Rising borrowing costs, weakening trade conditions and inflation have also weighed on global EMs. However, there does appear to be EM country differentiation in terms of performance. Some EM fundamentals are normalising to pre-pandemic levels, while growth has remained surprisingly resilient.

Chart 6. Developing vs. Emerging Markets PMIs

Chart 7. Emerging Markets PMIs

How has the slowdown in DMs affected EM financial market performance?

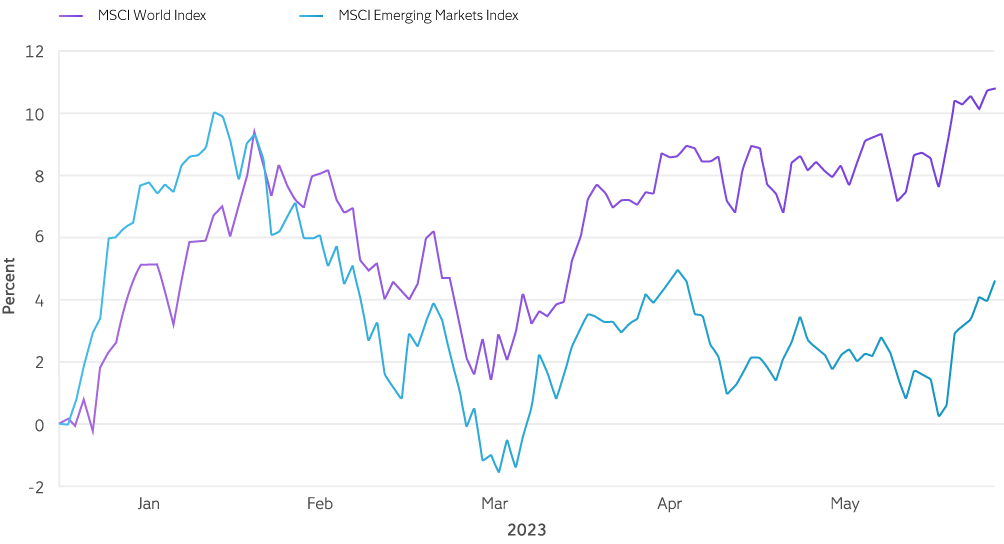

After a strong run since April, inflows into EM bond and equity markets have softened. Most EM currencies have depreciated in real terms, implying emerging value. According to the Institute for International Finance (IIF), portfolio flows to EM stood at $32.8 bn in July. Equity and debt flows were $17.6 bn and $15.2 bn. Chinese equities posted $7.7 bn in inflows.

Although the MSCI EM index was up by 11.7% by the end of July, EMs have lagged DMs so far this year, as DMs equities were up 19.3% with the S&P 500 up over 20% by the end of July. This differential in performance may be largely due to disappointing data following China’s reopening from the Covid pandemic. The MSCI Emerging Market Index top holdings are concentrated in Asia, with Chinese and Indian companies in the infotech, financial, and consumer discretionary sectors gaining particular prominence. Within the MSCI EM index just five countries – China (30.67%), Taiwan (14.77%), India (14.21%), South Korea (12.38%) and Brazil (5.49%) –account for more than 75% of the Index. According to Forbes, the performance of the MSCI emerging index stands at more or less the same level now as it did a decade ago.

Chart 8. Emerging stocks performance 1H 2023

As in DMs in 2023, performance has been supported through the information technology sector, the second-largest sector (20.27%) after financials (21.6%) in the MSCI Emerging Markets Index, as growth expectations for generative AI continue to grow. EM equities rallied by 6.3% in July, outperforming DM (+3%) for the first month since January. For many, EMs valuations remain attractive and, with the USD expected to weaken into 2024, EM’s stock markets could see a re-emergence of interest. However, this interest may be weighed down by deflation in China as weaker growth there will negatively impact its trade partners in emerging markets.

EM debt has added to gains this year, with returns of 5.5% across all segments despite significant volatility in US Treasury yields. This could be attributable to EM central banks reacting quickly to inflationary risks, initiating a series of rate hikes in 2021 which has allowed them to reap the benefits of falling core inflation sooner than we are seeing in developed market economies. However, the returns on EM corporate bonds were down 12% despite EM sovereigns outperforming US treasuries over the past 18 months. As EMs were generally, with the notable exception of Turkey, quicker to raise rates, there has been less issuance and rolling over of debt, a favourable supply/demand dynamic that should be supportive to EM bonds.

Chart 9. EM bonds vs US treasuries

EM currencies relationship with the US dollar

What is clear is that US dollar appreciation has weighed on EMs performance, both in equities and bonds. As the USD appreciates, due to tighter Fed policy or geopolitical concerns pushing investors to the safe haven that the USD provides, it pushes local interest rates to rise in response, making their debt less sustainable. This can make it harder for EMs to attract capital or may even drive capital flight. In short, the strengthening of the US dollar and weakening of EM currencies becomes a more complicated problem because the slowdown that is generally expected from a tighter interest rate policy regime, means less demand for imported goods and lower remittances for foreign, ie., non USD, economies. But this may no longer be the case for all EMs. As noted by the Federal Reserve Bank of Dallas, from early 2022 to mid-2023, emerging-market currencies depreciated only modestly based on a trade-weighted index of the dollar exchange rate of major US trading partners. At the same time, advanced economy currencies depreciated more than emerging-market currencies during this tightening cycle. This is because many EMs have been far more aggressive in their tightening cycle than the US and European central banks. EMs are also on course for higher GDP growth in 2023 and beyond. This faster pace of growth may translate into higher earnings and benefit these markets accordingly. In addition, more robust growth could support EM currencies versus the US dollar.

Another factor in the relationship between the USD and EMs is the shift over the past decade in the percentage of USD held by EMs. There has been a growing drop in USD in global EM central banks due to trade realignments, for example, with China demanding more Renminbi trade. For countries in the Asia Pacific region with strong trade ties and others, such as those in Sub-Saharan Africa, anxious to attract and maintain Chinese investment, their central banks have become very willing to add to their renminbi holdings compared to their European counterparts. There has also been growing interest by some emerging market economies, particularly those that are in or seeking to join the BRICS bloc, a group of countries that includes Brazil, Russia, China, India and South Africa, to replace the USD in interregional or bloc trade. Since the term was coined almost 22 years ago by Jim O’Neil, then an economist at Goldman Sachs, the bloc now, according to IMF data, contributes more to global GDP, in purchasing-power-parity terms, than the G7. Hippolyte Fofack at the African Export-Import Bank argues that because of their economic success, the BRICS are increasingly seen in the Global South as a viable force for multilateralism, noting that more than 40 countries – including Algeria, Egypt, Thailand, and the United Arab Emirates, but also key G20 members such as Argentina, Indonesia, Mexico, and Saudi Arabia – have expressed interest in joining the BRICS, and 22 have formally applied for membership. As a result, there has been growing global discussions around the creation of a block currency. But, as noted by US Treasury Secretary Janet Yellen in April this year,” the dollar is used as a global currency for reasons that are not easy for other countries to find an alternative with the same properties."

The entrenchment of global institutional arrangements, along with the breadth and depth of US financial markets, is highly likely to ensure the USD’s dominance for many more years. Jim O’Neil, now advisor at UK think-tank Chatham House, also thinks that a “BRICS bloc” currency is neither feasible nor desirable. Although acknowledging that the dollar’s dominance over the global financial system was not beneficial for emerging countries, he says “The dollar’s role is not ideal for the way the world has evolved. You’ve got all these economies who live on this cyclical never-ending twist of whatever the [US Federal Reserve] decides to do in the interests of the US.”

In short, although a “BRICS currency” does not appear to be realistically feasible, an enlarged BRICS group would, according to Mr Fofack, create a geopolitical coalition with the power to accelerate de-dollarization and lead the transition to a more multipolar world. However, he thinks that the use of local currencies in cross-border transactions has already yielded significant benefits for the BRICS, including lower transaction costs; a buffer against global volatility; increased trade among members, despite a challenging operating environment; and an easing of the balance-of-payments constraint associated with dollar funding. This de-dollarization, particularly in the context of commodities trading, may be a boon for countries like India, China, Brazil, Thailand and Indonesia as the ability to buy raw materials in domestic currencies may allow for a more lenient current account deficit. The USD will still reign supreme, but growing trade links between and among Emerging economies may result in greater non dollar currency stability as trading links between EMs deepen.

The Commodity and Currency impact

However, it isn’t just EM stocks and bonds that have suffered over the past year. EM currencies have also generally depreciated. This can be attributed to two main reasons: the US Federal Reserve’s aggressive monetary policy tightening and the impact this has had on commodity prices.

Commodities and EMs

Historically, commodities extraction and dependence on net exports were key factors driving emerging market growth as many EMs are net commodity exporters and in some Latin American countries, raw material exports still account for the majority of export volumes. Although there has been a reshaping of emerging markets economies into other industrial and service sectors, many EMs remained closely tied to and dependent upon the production of soft (eg., coffee, wheat, soybeans) and hard (eg., metals, oil, gas) commodities. As noted by the Bank for International Settlements (BIS), commodity price rises tend to stoke inflation and choke off growth in commodity-importing economies, while dollar appreciation tends to do the same outside the United States, especially in emerging market economies. The stagflationary effects of higher commodity prices exert themselves in part through higher consumer prices, which squeeze household incomes, and rising production costs for firms, which dampen investment. In short, the stagflationary effects of a stronger dollar come through its dominant role in global trade and finance.

However, there has been a change in the correlation between commodity prices and dollar exchange rate as DMs such as the US have become bigger commodity exporters. As noted by the BIS, a durable change in the commodity price-dollar nexus could lead to greater macroeconomic volatility and more difficult trade-offs between inflation and output stabilisation.

What may move the needle for EMs?

The global energy transition, a shift from carbon-intensive fuels to low-carbon alternatives, will put EMs at the centre of delivering key commodities for the foreseeable future.

Industrial metals, such as copper, zinc, aluminium and nickel, will be critical in the green transition as transport, industry, and heating are all increasingly going to be run on renewable energy to meet net zero or lower carbon emission targets and countries will be seeking to build out renewable energy sources and expand the grid. EMs will play a crucial part in meeting demand for the metals required to meet these green energy and renewables targets given their comparative advantage in extracting commodities cheaply and their overall control of supply and production. According to the IEA, global renewable capacity additions are set to soar by 107 gigawatts (GW), the largest absolute increase ever, to more than 440 GW in 2023. This is equivalent to more than the entire installed power capacity of Germany and Spain combined. This unprecedented growth is being driven by expanding policy support, growing energy security concerns and improving competitiveness against fossil fuel alternatives.

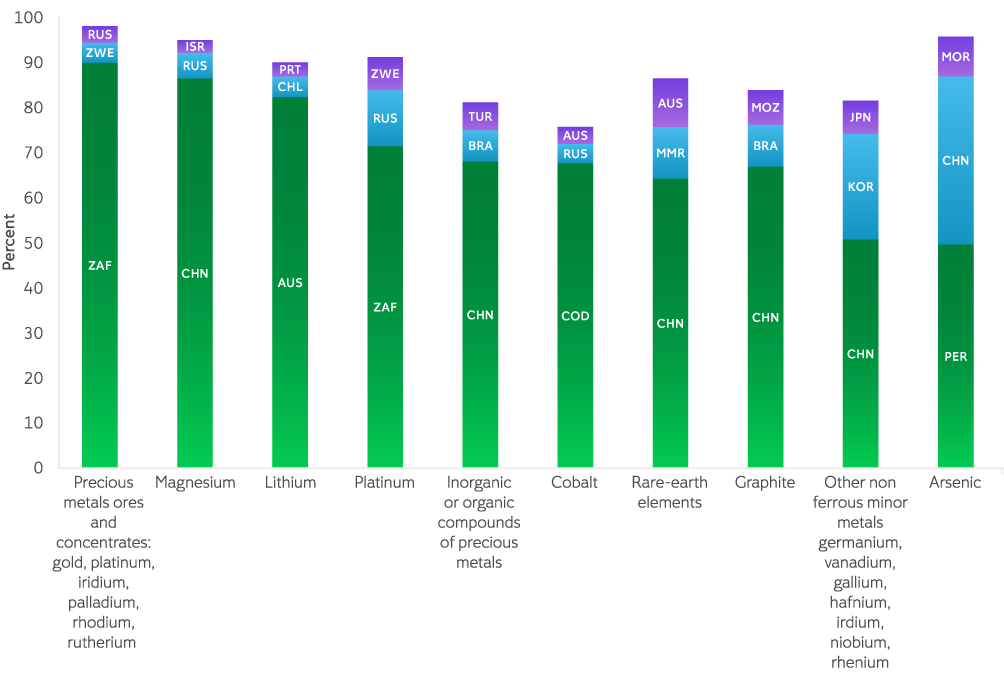

Emerging markets will also be important suppliers of manganese, cobalt, chromium and molybdenum, used in electric vehicles and in telecommunication technology. As noted by the OECD, growth in supply is not keeping pace with projected demand for the metals and minerals needed to transform the global economy from one dominated by fossil fuels to one led by renewable energy technologies. They note that both imports and exports of critical raw materials have also become increasingly concentrated amongst countries, but trade of these materials remains relatively well diversified, suggesting the possibility of significant disruption by disturbances to import or export flows of critical raw materials is limited.

Chart 10. Producers of critical raw materials for renewables

Chart 11.Commodity Price Forecasts

The influence of ESG

As the world faces growing social and environmental challenges, such as climate change, biodiversity loss, the cost-of-living crisis, and social inclusion, environmental, social, and corporate governance (ESG) concerns have particular relevance in emerging markets, where many of these challenges are most acute.

The pressures of increasingly stringent ESG requirements are coming from a wide mix of stakeholders. Intra-national regulators such as the EU and national governments are adopting tighter ESG frameworks and requirements that will hit emerging market companies, non-domestic companies investing in emerging markets, and financing sources. As noted by PwC, these ESG standards cover not just underlying projects that may be taking place in emerging market countries such as mining or energy exploration activities, but are increasingly being applied to the overall project supply chain including the construction companies involved and the financing sources that deploy new sources of liquidity into projects. This means that financing partners are demanding baselines that meet sustainable finance standards developed by the EU. Emerging ESG issues that are increasingly being asked to be addressed include the carbon transition, worker rights,and corporate governance.

The pressure pushing investment towards ESG is not just regulatory, but also coming from the growing interest by institutional and retail investors in ESG investment. Global ESG fund assets reached about $2.5 trillion at the end of 2022, according to Morningstar research. As we have moved into 2023, ESG funds have been battered by high inflation, rising interest rates, and recession fears, but global sustainable fund assets hit nearly $2.8 trillion at the end of June 2023. Morningstar reported that the global universe of sustainable funds attracted close to $8 billion of net new money in the second quarter of 2023 and was still better than the overall global fund universe, which returned to outflows of over $37 billion in the second quarter. Europe continued to comprise the majority share of the sustainable fund landscape, with 84% of global sustainable fund assets. Asia ex-Japan, of which China is the biggest sustainable market, with more than 72% of the region's asset base, ranks third in terms of sustainable fund market size.

Chart 12. Asset Class Flows, ESG v Conventional, H1 2023 (£bn)

Source: LSEG Lipper

Conclusion

What is clear is that commodity investors, EM currency investors and investors in companies operating in Emerging markets, need to focus on the security of supply chains. As companies seek to onshore or reshore for both geopolitical and economic reasons, particularly away from China, the reliance for some critical industries on Chinese supply, including renewables and the critical minerals and refined production processes owned by Chinese companies, then there needs to be much more attention paid to supply chain security.

When the Fed begins to cut policy rates and EM growth relative to advanced economies improves, the flow of funds into EMs will rise, causing currency appreciation. Although interest rate cuts in Brazil and Chile may have led markets to consider the emergence of an EM easing cycle, most EM central banks are likely to be cautious, especially in countries where rates are already close to neutral, including most of Asia. The end of global rate hikes will help reduce volatility and support the carry trade, and that will benefit higher-yielding EM currencies and bonds.

The short- to medium-term outlook for commodities could be supported by a weaker dollar as many key items are traded in dollars. Supply-chain disruptions resulting from the conflict in Ukraine and state sponsored renewables investment to tackle the climate crisis, may also help. The shrinking regulatory timeframes for decarbonisation will also be supportive to EM growth and their currencies due to increased demand for many of the commodities found in their borders.

However, there are a number of risks for investors in EMs to consider as well. One of the main risks to watch out for is the excessive tightening of financial conditions affecting economic growth. Some low-income countries have already been impacted by the higher cost of refinancing. Another key topic to look at is geopolitical risk, which is still high. Investors also need to monitor individual countries' domestic experiences and internal vulnerabilities which can increase EM fragmentation. The risks that could, for example, lead to greater supply chain disruption include shifts in domestic politics resulting in civil disputes, growing geopolitical risks including increasing friction with major trade partners, climate change effects, an ageing population or significant demographic imbalances, and misaligned decarbonisation measures.

References:

- Allianz: The “five Ds” of structurally higher inflation

- Bank for International Settlements (BIS):The changing nexus between commodity prices and the dollar: causes and implications

- Barrons: Yellen Says Sanctions May Risk Hegemony Of US Dollar

- Bloomberg: Decade of Emerging Markets’ May Be About to Regain Traction

- ECB: Friend-shoring global value chains: a model-based assessment

- ECLAC: Capital Flows to Latin America and the Caribbean in five charts: First half of 2023

- Federated Hermes: The 10 themes that could make or break an EM renaissance

- Financial Times:Brics creator slams ‘ridiculous’ idea for common currency

- Fortune: A much-feared emerging markets crisis didn’t happen. Is the global economy off the hook?

- Franklin Templeton: Emerging Markets Insights August 2023

- IEA: Renewable Energy Market Update - June 2023

- Federal Reserve Bank of Dallas: Emerging-market countries insulate themselves from Fed rate hikes

- IMF: Global Economy on Track but Not Yet Out of the Woods

- HSBC: Trade in 2023 and beyond Free to View Economics - Global Will weakness persist?

- JPMorgan Asset Management: Emerging Market Debt Quarterly Strategy

- Morningstar: Why Emerging Markets Underperform

- OECD: Supply of critical raw materials risks jeopardising the green transition

- Portfolio Institutional Magazine July August 2023: EM Debt: Crisis? What Crisis?

- Project Syndicate, Hippolyte Fofack, Chief Economist and Director of Research, African Export-Import Bank, The BRICS Come of Age

- PwC 2023: Miners capitalise on energy transition commodities, despite challenging road to net zero: PwC’s 20th annual Mine report

- Refinitiv :Emerging markets mid-year review

- S&P: Easing growth momentum keeps price inflation subdued across emerging markets

- Schroders: Emerging Markets Lens: Equity

- World Bank blogs: Commodity Markets Outlook in eight charts

Dit artikel wordt u alleen ter informatie verstrekt en mag niet worden beschouwd als een aanbod of uitnodiging tot het kopen of verkopen van beleggingen of gerelateerde diensten waarnaar hier mogelijk wordt verwezen.