Global market indices

Currencies

Cryptocurrencies

Fixed Income

Commodity sector news

Key data to move markets

Global macro updates

Global market indices

US Stock Indices Price Performance

Nasdaq 100 +5.12% MTD +30.76% YTD

Dow Jones Industrial Average -3.25% MTD +15.28% YTD

NYSE -6.34% MTD +12.66% YTD

S&P 500 -2.66% MTD +23.11% YTD

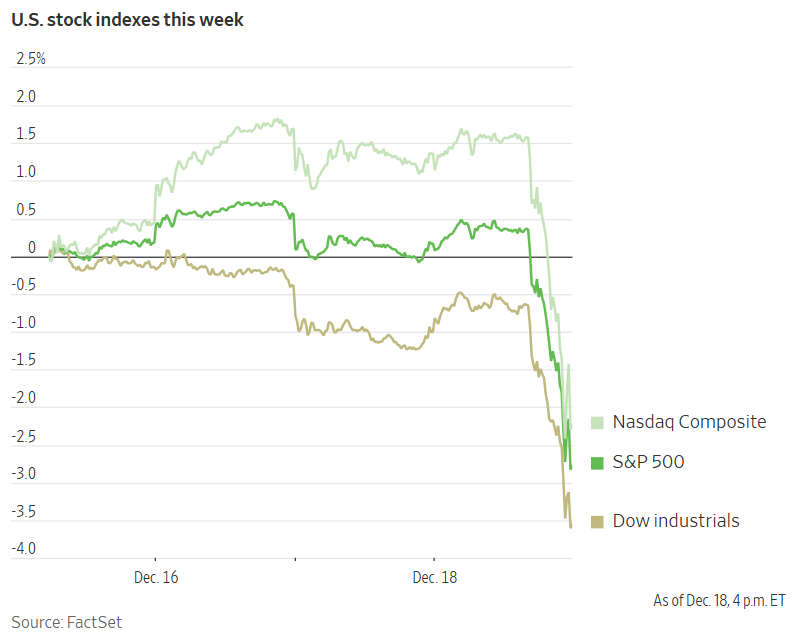

The S&P 500 is -3.48% over the past week, with 8 of the 11 sectors down MTD. The Equally Weighted version of the S&P 500 is -1.88% this week, its performance is -4.10% MTD and +13.67% YTD.

The S&P 500 Consumer Discretionary is the leading sector so far this month, up +4.33% MTD and +31.65% YTD, while Energy is the weakest at -11.66% MTD and -0.06% YTD.

This week, Consumer Staples outperformed within the S&P 500 at -1.94%, followed by Information Technology and Consumer Discretionary at -2.34% and -3.21%, respectively. Conversely, Energy underperformed at -6.70%, followed by Materials and Real Estate, at -5.71% and -5.69%, respectively.

US equity markets experienced a significant correction on Wednesday, with major indices registering substantial declines following the Fed's monetary policy announcement. While the FOMC lowered the federal funds rate by 25 bps, in line with market expectations, investor sentiment was dampened by the Committee's signalling of a more measured approach to future rate reductions.

The Dow Jones Industrial Average was -2.6%, shedding 1,123 points to conclude at 42,326.87. Despite an initial advance, the blue-chip index ultimately recorded its most pronounced decline since August, extending its streak of daily losses to ten consecutive sessions – the longest such period since 4th October, 1974.

The S&P 500 also suffered its worst session since August, falling -2.9%, below the 6,000 level, driving all 11 of its sectors lower. The Nasdaq 100 index fared even worse, declining -3.6%, its steepest drop in five months.

The magnitude and velocity of Wednesday's market correction underscore the Fed’s shift towards a more cautious policy stance, particularly in light of persistent inflationary pressures. This recalibration comes after a period of robust gains in equity markets, with the S&P 500 having surged more than +10% since the FOMC's 31st July meeting, where the Committee had signaled a prioritization of labor market expansion.

Historically, such pronounced declines in the S&P 500 on Fed decision days have been rare. The last comparable instance occurred on 17th September, 2001, when the index plummeted nearly 5% in the aftermath of the terrorist attacks. More recently, the S&P 500 experienced a 12% plunge on 16th March, 2020, following the Fed's emergency weekend meeting during the onset of the COVID-19 pandemic.

As concerns about a less accommodative Fed and rising government deficits have intensified, market breadth has deteriorated significantly. On Wednesday, declining stocks on the S&P 500 outnumbered advancing stocks for a 13th consecutive session, the longest such streak since at least 1978.

In corporate news, shares of General Mills declined after the breakfast cereal maker lowered its profit outlook, citing consumer resistance to higher food prices. Barclays announced plans to increase annual bonuses for its traders and bankers by as much as 20%. Merck disclosed a deal worth up to $2 billion to acquire the rights to an experimental weight-loss pill from a Chinese drugmaker. Furthermore, AMD made a strategic investment in cloud provider Vultr at a valuation of $3.5 billion.

US stocks

Mega caps: The Magnificent Seven had a mostly negative performance this week. Alphabet -3.58%, Amazon -4.23%, Apple +0.63%, Meta Platforms -5.61%, Microsoft -2.58%, Nvidia -7.47%, and Tesla +3.62%.

Energy stocks underperformed this week, as the Energy sector itself was -6.70%. This week, WTI and Brent are -0.46% and -0.79%, respectively. The Energy sector’s YTD performance is -0.06%. Over the week BP -2.70%, Shell -2.95%, ExxonMobil -4.91%, Occidental Petroleum -5.05%, Baker Hughes -5.70%, ConocoPhillips -6.20%, Apa -6.88%, Chevron -7.77%, Hess -8.87%, Halliburton -10.45%, Phillips 66 -10.75%, Marathon Petroleum -11.13%, and Energy Fuels -14.77%.

Materials and Mining stocks had a negative performance this week, with the Materials sector itself -5.71%, bringing the sector’s YTD performance to -0.73%. CF Industries -6.00%, Yara International -7.54%, Mosaic -9.30%, Freeport-McMoRan -9.98%, Newmont Corporation -10.97%, Sibanye Stillwater -12.44%, Albemarle -12.81%, and Nucor -14.79%.

European Stock Indices Price Performance

Stoxx 600 +0.82% MTD +7.40% YTD

DAX +3.14% MTD +20.84% YTD

CAC 40 +2.07% MTD -2.10% YTD

IBEX 35 -0.20% MTD +15.00% YTD

FTSE MIB +2.70% MTD +13.06% YTD

FTSE 100 -1.11% MTD +5.97% YTD

This week, the pan-European Stoxx Europe 600 index was -1.06%. It was +0.15% on Wednesday, closing at 514.43.

This month so far in the STOXX Europe 600, Technology is the leading sector, +6.46% MTD and +10.03% YTD, while Utilities is the weakest at -4.32% MTD and -3.45% YTD.

This week, Technology outperformed within the STOXX Europe 600 with a +1.39% gain, followed by Banks and Personal & Household Goods at +0.02% and -0.52 %, respectively. Conversely, Basic Resources underperformed at -5.82 %, followed by Chemicals and Oil& Gas, -3.12% and -2.68%, respectively.

Germany's DAX index was -0.02% on Wednesday and closed at 20,242.57. It was -0.77% for the week. France's CAC 40 index was +0.26% on Wednesday, closing at 7,384.62. It was -0.52% for the week.

The UK's FTSE 100 index was -1.28 % this week to 8,195.20. It was -0.81% on Wednesday.

European markets demonstrated a mixed performance on Wednesday, with banks leading the upswing in trading. Unicredit increased its stake in Commerzbank to 28% through the execution of new derivative contracts. EFG International received an upgrade to ‘buy’ at UBS, based on its attractive valuation and improving earnings momentum.

The Energy sector also exhibited strength, with crude oil prices recovering from Tuesday's decline. This rebound is potentially linked to reports suggesting an imminent Gaza ceasefire is unlikely. Technology stocks trended higher as well, possibly buoyed by Nvidia's confirmation that its Blackwell project remains on schedule, coupled with press reports indicating robust sales to major clients. Furthermore, Nokia was upgraded to ‘buy’ at DNB. Analysts cited anticipated organic sales growth in 2025, strong earnings momentum driven by the Network Infrastructure segment, and the potential for a shift in its investor base from value-oriented to growth-oriented investors.

Conversely, the Food and Beverage sector lagged with minimal news driving the decline. The chemicals sector also underperformed, influenced by REC Silicon's disclosure of unsuccessful qualification test results for its ultra-high purity polysilicon. In contrast, IMCD announced its acquisition of YCAM's life science business in South Korea. Utilities experienced downward pressure, potentially due to forecasts predicting mild weather conditions in Europe over the coming weeks.

Other Global Stock Indices Price Performance

MSCI World Index +0.17% MTD +20.43% YTD

Hang Seng +3.77% MTD +18.23% YTD

This week, the Hang Seng Index was +2.09%, while the MSCI World Index was -0.86%.

Currencies

EUR -2.10% MTD -6.18% YTD to $1.0350.

GBP -1.28% MTD -1.24% YTD to $1.2566.

The euro was -1.40% against the USD over the past week, while the British pound was -1.43%.

The US dollar exhibited broad-based strength on Wednesday, appreciating against its major counterparts and reaching a two-year high. The FOMC reduced its benchmark federal funds rate by 25 bps, setting the target range at 4.25% to 4.50%. However, policymakers signaled their intention to potentially pause further rate cuts in the coming year, citing the ongoing stability of the labour market and persistent inflationary pressures. During his post-meeting press conference, Fed Chair Jerome Powell emphasised the importance of proceeding cautiously in the rate-cutting cycle, highlighting the need for clear evidence of progress in curbing inflation. He also acknowledged signs of softening in the labour market.

This more cautious outlook contributed to a rise in US Treasury yields, with the yield on the 10-year note climbing 11.4 basis points to 4.519%. As a result, the US dollar index was +1.23% to reach 108.26, its highest level since November 2022. The Dollar Index is +1.50% so far this week. The euro bore the brunt of the dollar's strength, depreciating by -1.36% to $1.0350 and touching a three-week low.

The dollar's strength extended to the Japanese yen, with the dollar +0.87% to reach ¥154.78, a three-week high. This move came ahead of today’s BoJ's monetary policy announcement, where policymakers are widely expected to maintain their current stance.

Similarly, the BoE is anticipated to keep its policy rate unchanged later today. Sterling edged lower against the dollar following the Fed's decision, weakening by -1.13% to $1.2566 and falling to a three-week low.

The pound's decline versus the dollar coincided with the release of UK inflation data, which met analysts' expectations. Consumer prices rose by 2.6% y/o/y in November, although services inflation remained elevated at 5.0%. However, wage data earlier this week indicated a 5.2% rise in the August to October 2024 period, wiping out expectations of a rate cut today. Traders currently anticipate 57 bps of monetary easing by the end of 2025, compared to 55 bps projected just before the release of the inflation data.

The pound also weakened against the euro, with the euro +0.23% to 82.70 pence. Last week, the euro reached 82.51 pence, its lowest point against the pound since March 2022.

However, investors maintain a generally positive outlook for the pound, anticipating that the significant divergence in bond yields between the UK and the euro area will ultimately support the British currency. Markets anticipate the ECB's deposit rate will fall to 1.8% by December of next year, down from its current level of 3%.

Today, Sweden's Riksbank is widely expected to implement a rate cut of up to half a percentage point, while Norway's Norges Bank is projected to leave its policy rate unchanged.

Note: As of 5:00 pm EST 18 December 2024

Cryptocurrencies

Bitcoin +3.24% MTD +139.35% YTD to $101,422.00.

Ethereum +1.48% MTD +58.92% YTD to $3,698.46.

Bitcoin is -0.51% and Ethereum -3.61% so far this week. Bitcoin and other crypto currencies were hit not just by the Fed’s 25 bps cut on Wednesday, but more by the commentary from Fed Chair Jerome Powell which suggested both fewer cuts and a slower pace in 2025 as inflation will be at 2.5% at the end of next year, with the 2% goal not being hit until 2027. As noted by Coindesk.com, Bitcoin's seven-day call-put skew shows that Deribit-listed put options offering downside protection and expiring in one week are trading at the highest implied volatility premium to call options since September, according to data source Amberdata. Bitcoin was also affected by Chair Powell’s comments that the Fed was “not allowed” to own the cryptocurrency and was not going to look to Congress to change these rules. This has put a dent into the hopes of the US building a “Strategic Bitcoin Reserve” as suggested by President-elect Trump in the run-up to November’s election.

Note: As of 5:00 pm EST 18 December 2024

Fixed Income

US 10-year yield +34.4 bps MTD +63.8 bps YTD to 4.519%.

German 10-year yield +15.8 bps MTD +24.0 bps YTD to 2.249%.

UK 10-year yield +31.6 bps MTD +102.4 bps YTD to 4.563%.

US Treasury 10-year bond yields are +24.4 bps this week. US Treasury yields experienced a notable surge on Wednesday following the Fed's decision to lower interest rates by 25 bps. This upward movement in yields was driven by the Fed's signalling of a more gradual pace of easing in the coming year, citing the persistent stability of the labour market and the presence of inflation that has proven more resistant than usual.

During afternoon trading, the yield on the 10-year US Treasury note reached its highest point since late May, touching 4.51% in the immediate aftermath of the rate announcement. By the end of the trading session, the yield had risen by +11.4 bps to settle at 4.519%, marking its most significant daily gain in approximately five weeks.

This upward trend was also evident in longer-term maturities, with the 30-year US Treasury yield climbing to a four-week high. It ultimately closed at 4.648%, reflecting a +6.9 bps increase and its largest one-day gain since 12th November.

Shorter-term yields exhibited similar behaviour. The yield on the two-year US Treasury note, which is particularly sensitive to shifts in the interest rate outlook, was +9.4 bps to reach 4.336%. This followed an earlier climb to a new three-week high in response to the FOMC’s statement. The two-year yield's rise represented its most substantial daily increase in over two months.

With this latest adjustment, the benchmark federal funds rate now rests within a target range of 4.25% to 4.50%. In its accompanying policy statement, the FOMC acknowledged the continued solid expansion of economic activity, highlighting the sustained low unemployment rate and the persistence of somewhat elevated inflation.

The FOMC's decision was not unanimous, as Cleveland Fed President Beth Hammack dissented, favouring maintaining the policy rate at its previous level.

In the wake of the Fed's announcement, US rate futures have recalibrated their expectations for future rate cuts. Current market pricing indicates a mere 32 bps in cumulative rate reductions for 2025, down from 49 bps projected immediately prior to the release of the FOMC statement.

Market expectations for a 25 bps rate cut at the conclusion of the FOMC's 28th - 29th January meeting have decreased. According to the CME Group's FedWatch Tool, the probability of such a cut now stands at 16.8%, down from 20.9% a week ago.

Across the Atlantic, the German 10-year yield was +11.7 bps this week, while the UK 10-year yield was +24.2 bps this week. The spread between US 10-year Treasuries and German Bunds currently stands at 227.0 bps, 12.7 bps higher than last week.

Italian bond yields, a benchmark for the eurozone periphery, were +20.4 bps this week to 3.409%. Consequently, the spread between Italian and German 10-year yields is 116 bps, 8.7 bps wider than last week.

French 10-year government bond yields also increased this week by +15.5 bps to 3.055%. The yield premium over German 10-year yields widened by 3.8 bps this week to 80.6 bps.

Eurozone bond yields remained relatively stable on Wednesday as market participants awaited the Fed's interest rate decision later in the day.

This period of anticipation comes amidst a flurry of central bank activity. Within a 36-hour timeframe, the BoJ, BoE, Sweden's Riksbank, and Norway's Norges Bank are all scheduled to announce their respective interest rate decisions.

The German 10-year Bund yield has risen approximately +12 bps since the ECB rate cut last Thursday. Despite the reduction, the ECB's accompanying statement emphasised that the fight against inflation was not over, prompting traders to temper their expectations for further rate cuts in the coming year.

Data released on Wednesday confirmed that eurozone inflation for November stood at 2.2%, a slight downward revision from the preliminary estimate of 2.3%.

Reflecting the shift in rate expectations, Germany's two-year bond yield, which is highly sensitive to ECB policy, declined by -2 bps to 2.035%.

Germany's 10-year Bund yield edged higher by +1.6 bps to reach 2.249%. Similarly, Italy's 10-year bond yield increased by +2.3 bps to 3.409%, resulting in a spread of 116.0 bps between Italian and German bond yields.

The divergence in monetary policy between the BoE and the ECB was evident in the widening spread between British and German 10-year government bond yields. This spread reached its highest level in 34 years on Wednesday, expanding to 231.4 bps.

Commodities

Gold spot -0.77% MTD +27.84% YTD to $2,584.98 per ounce.

Silver spot -4.25% MTD +23.66% YTD to $29.33 per ounce.

West Texas Intermediate crude +2.62% MTD -2.56% YTD to $70.00 a barrel.

Brent crude +1.60% MTD -5.26% YTD to $72.99 a barrel.

Gold prices are down -4.86% this week. Gold prices experienced a significant decline on Wednesday, falling over 2% to a one-month low. This downturn followed the Fed signalling a more gradual approach to future rate reductions, citing concerns about persistent inflationary pressures. This announcement triggered a rally in the US dollar and a surge in bond yields, both of which exerted downward pressure on gold prices.

Spot gold dropped by -2.28% to reach $2,589.91 per ounce, its lowest level since November 18th.

The Fed's announcement spurred a broad-based strengthening of the US dollar, with the dollar index climbing more than 1% to a two-year high. This appreciation of the dollar rendered gold more expensive for buyers holding other currencies, further contributing to the decline in gold prices.

This week, WTI and Brent are -0.46% and -0.79%, respectively.

Oil prices concluded Wednesday's trading session on a higher note, buoyed by a reported decline in US crude inventories and the Fed's decision to lower interest rates as anticipated. However, the extent of these gains was limited as the Fed indicated a more measured approach to future rate cuts.

According to data released by the Energy Information Administration (EIA), US crude oil and distillate inventories decreased in the week ending 13th December, while gasoline inventories experienced an increase. Encouragingly, total product supplied, a key indicator of oil demand, reached 20.8 million barrels per day, representing a notable rise of 662,000 barrels per day from the previous week.

Despite the initially positive reaction to the EIA report, both Brent and US crude futures surrendered their earlier gains and briefly dipped into negative territory in post-settlement trading. This shift coincided with the Fed's monetary policy announcement, which prompted a surge in the US dollar. The dollar index reached a year-to-date high of 108.26, exerting downward pressure on dollar-denominated oil prices.

EIA report: strong export demand offsets rising gasoline stockpiles. In the week ending 13th December, the Energy Information Administration (EIA) reported a decline in US crude oil and distillate inventories, attributed to a surge in exports, while gasoline stockpiles experienced an increase.

Specifically, crude oil inventories decreased by 934,000 barrels, settling at 421 million barrels. This coincided with a significant rise in US crude oil exports, which climbed by 1.8 million barrels per day (bpd) to reach 4.89 million bpd. The EIA also noted an increase of 108,000 barrels in crude oil stocks at the Cushing, Oklahoma delivery hub, bringing the total to 23 million barrels. This export activity was likely stimulated by the widening spread between Brent and US WTI futures observed in late November, which reached nearly $4.50 per barrel, encouraging flows to higher-priced markets across the Atlantic. As of Wednesday, this spread had narrowed to approximately $3.40 per barrel.

Refinery operations saw a slight downturn, with crude runs decreasing by 48,000 bpd and utilization rates dipping by 0.6 percentage points to 91.8%. However, the four-week average utilization rate remained robust at 92%, exceeding the 90.7% recorded during the same period last year.

Despite the increase in gasoline stocks, which rose by 2.3 million barrels to 222 million barrels, overall product supplied – a key indicator of demand – demonstrated strength, reaching 20.8 million bpd, a notable increase of 662,000 bpd from the previous week.

Countering the trend in gasoline, distillate stockpiles, encompassing diesel and heating oil, fell by 3.2 million barrels to 118.2 million barrels. This decline is particularly noteworthy given that distillate demand reached its highest point since March 2022.

Finally, the EIA reported a reduction in net US crude imports, which fell by 1.13 million bpd.

Note: As of 5:00 pm EST 18 December 2024

Key data to move markets

EUROPE

Thursday: GfK Consumer Confidence Survey, and EU Leaders Summit.

Friday: EU Leaders Summit, German PPI, French PPI, Italian PPI, Industrial Sales, Consumer and Business Confidence, and Eurozone Consumer Confidence.

Monday: Spanish GDP.

Tuesday: Christmas Day, markets closed.

Wednesday: Boxing Day, markets closed.

UK

Thursday: BoE Interest Rate Decision, BoE Minutes, Monetary Policy Report.

Friday: Retail Sales.

Monday: GDP.

Tuesday: Christmas Day, markets closed.

Wednesday: Boxing Day, markets closed.

US

Thursday: Initial and Continuing Jobless Claims, GDP, Personal Consumption Expenditure Prices, Philadelphia Fed Manufacturing Survey, and Existing Home Sales.

Friday: Personal Consumption Expenditures (PCE) Price Index, Core PCE, Personal Income, Personal Spending, Michigan Consumer Sentiment Index, and UoM 5-year Consumer Inflation Expectation.

Monday: Consumer Confidence. The stock and bond markets will close early for Christmas Eve.

Tuesday: Durable Goods, Nondefense Capital Goods Orders, and New Home Sales. US markets will be closed for Christmas.

JAPAN

Thursday: National Consumer Price Index (CPI), and Core CPI.

Monday: BoJ Monetary Policy Meeting Minutes.

CHINA

Thursday: PBoC Interest Rate Decision.

Global Macro Updates

FOMC delivers expected rate cut, signals slower pace of future reductions. The December FOMC meeting concluded with a widely anticipated 25 basis point reduction in the federal funds rate, bringing it to a range of 4.25% to 4.50%. The accompanying release highlighted Cleveland Fed President Hammack's dissent, who favoured maintaining the existing rate.

The Fed’s updated Summary of Economic Projections (SEP) revealed a projected median federal funds rate of 3.875% at the end of 2025, a revision from the previous 3.375%. This implies an expectation of 50 basis points of total cuts next year, a more conservative outlook than the analyst consensus, which had largely anticipated three 25 basis point cuts in 2025 compared to the four projected in September's FOMC. The reverse-repo rate was adjusted downward to 4.25% from 4.55%, a move that had been considered possible by some analysts. Notably, the Fed's longer-run median rate forecast was revised upward to 3.0% from 2.9%, while the inflation forecast for 2025 saw an increase, with headline PCE inflation now projected at 2.5% compared to the previous estimate of 2.1%.

The FOMC statement itself saw minimal alterations. A notable addition was a new clause regarding the "extent and timing of additional adjustments," which was initially interpreted by some as a hawkish signal.

During the subsequent press conference, Chair Powell explained that the slower pace of possible rate cuts reflects expectations of higher inflation, although he affirmed that the inflation narrative remains "broadly on track." He further emphasised the Fed's capacity to adopt a more cautious approach to rate reductions given the economy's current strength. "Today was a closer call, but we decided it was the right call," Powell stated, later adding, "From here, it's a new phase, and we're going to be cautious about further cuts."

The labour market continues to exhibit a delicate balance, characterised by low hiring rates alongside low layoffs. Robust income growth has underpinned strong consumption, and Fed officials are closely monitoring job growth to ensure it settles at a pace conducive to maintaining a stable unemployment rate.

While the recent rate cuts have offered immediate relief to consumers with credit card balances and small businesses with variable-rate debt, long-term borrowing costs for mortgages, auto loans, and corporate debt have risen in recent months as investors have scaled back their expectations for aggressive rate cuts in the coming year.

BoE expected to hold rates amid economic stagnation. The UK's inflation trajectory and the BoE policy response are under renewed scrutiny following the release of November's inflation data. Headline inflation accelerated to 2.6% in November, surpassing the prior month's 2.3% and diverging further from the BoE's target. While this aligned with consensus expectations, core inflation came in slightly below forecasts at 3.5% (versus 3.6% expected and 3.3% previously), and services inflation held steady at 5.0%, just below the consensus of 5.1%. The primary drivers of the price increase were the transport sector, housing, and household services.

These figures are notable in light of the BoE's November Monetary Policy Report, which projected inflation to rise to around 2.5% by the turn of the year, a near-term path that was lower than its August projections. Preliminary findings on the impact of a more expansionary fiscal policy suggested it would add 0.2% to CPI in Q1 2025. Despite yesterday's higher-than-expected CPI data and Tuesday's upside surprise in wage growth, the BoE's policy direction is unlikely to shift significantly. Policymakers are widely anticipated to maintain the current interest rate at today's meeting and continue a gradual approach to easing. However, there is a growing concern that persistent domestic inflation could pose the most significant risk to the BoE's outlook.

The currency market has responded favorably to the interest rate differential between the UK and the Eurozone, with GBP/EUR trading around the 1.21 level. The BoE's cautious stance on monetary policy, contrasting with the ECB’s signals of a more aggressive rate-cutting cycle for 2025, continues to underpin Sterling's strength. The spread between UK 10-year gilts and German bunds has widened to over 2.3 percentage points. This marks the largest premium since German reunification and surpasses the peak reached following Liz Truss's ‘mini’ Budget two years ago.

This widening spread comes ahead of the BoE's final policy meeting of the year today. Investors are betting that persistent inflation will deter the central bank from cutting its benchmark rate, despite the stagnating economy. Recent data showed an unexpected contraction in GDP for a second consecutive month in October, further highlighting the economic challenges.

The recent rise in gilt yields has pushed government borrowing costs back near the one-year high reached last month following Chancellor Rachel Reeves' October Budget, which briefly unsettled investors with increased debt issuance plans. Yields have risen from less than 4.2% two weeks ago as traders now anticipate just two quarter-point rate cuts from the BoE next year, down from four expected in October. If gilt yields surpass the levels seen during the Truss administration, Chancellor Reeves may face pressure to raise taxes or cut spending to address concerns about fiscal sustainability. These higher borrowing costs are further undermining the UK's fiscal position.

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

Questo articolo viene fornito all'utente soltanto a scopo informativo e non deve essere considerato come un'offerta o una sollecitazione di un'offerta di acquisto o di vendita di investimenti o servizi correlati che possono essere qui menzionati.