About this report

We provide a brief summation of the forces shaping wealth creation and distribution around the world using secondary and tertiary data. We examine how the wealthy, both High Net Worth Individuals (HNWIs) and Ultra High Net Worth Individuals (UHNWIs), are changing in the post Covid years in terms of who they are and where they are. We also review how their goals have changed as markets have undergone significant volatility in the post Covid world. We review how they themselves are in the process of undergoing generational, gender and consequent behavioural change. Finally, we consider how all of these factors are influencing what they want to invest in, how they want to invest in terms of instruments and asset classes and what they now seem to want from advisors, managers and other service providers to achieve their wealth goals.

Executive Summary

The wealthy are changing. It is not just that the number of HNWIs, comprising those with at least USD 1 million of investable assets, or even UNHWIs, comprising those with USD 30 million of assets, are growing as a percentage of the total global population. It is that the background, experience and expectations of these ultra rich is changing at an unprecedented rate with more women and more people from traditionally less developed countries or regions, now being classified as wealthy. This is being further emphasised by a simultaneous and unprecedented intergenerational wealth transfer.

Given the structural changes taking place in the composition of the globally wealthy, financial service providers such as banks, wealth managers, wealth advisors, fintechs and other auxiliary services must consider a number of factors if they are to continue to grow their businesses. These factors include:

- The wealthy are on the move. Immigration and demography are changing the place and face of the wealthy.

- The wealthy are embracing technology. When it comes to advisory and investing services, there is a significant regional variation in what the most important investment goals are.

- The asset classes and the reasons for investing in those assets are also changing amongst the wealthy. There is a growing need for advice to understand the implications of new asset classes and instruments in wealth maintenance and growth.

When it comes to empowering wealthy clients, they are really looking for financial services providers that allow them to easily, and increasingly digitally, access not just their accounts, but their entire financial planning, risk assessment, and portfolio management journeys. And, as we experience greater generational change that includes the transfer of intergenerational wealth as well as the development of new wealth itself, we should expect to see greater diversity in the types of assets that these wealthy use, eg., an increased willingness to include tokenised digital assets in their portfolios along more traditional asset classes such equities, as well as the reasons for using them, eg., the interest in ESG linked investments globally are likely to continue to rise as long as there are reliable and traceable ESG scores available to investors.

Setting the scene: The current situation

For the past twenty years global economic growth was underpinned by a relatively benign geopolitical world, with increasing globalisation, the development of multi-country supplies chains, and the widespread availability of cheap credit helping to fuel global wealth. However, the growth of global financial wealth halted in 2022, declining, according to the management consultancy BCG’s Global Wealth Report 2023, by 4% to $255 trillion. Thedownturn followed a strong year in 2021, during which financial wealth rose by more than 10%, one of the sharpest rises in over a decade. The change was due to the effects of global health pandemic, an energy crisis, the sudden re-emergence of geopolitical tensions and war, the collapse in supply chains, the rise of nationalistic policies that led to corporate rethinking on re-shoring and “friend-shoring,” and the consequent rise in inflation from supply constraints in addition to changing labour market dynamics in the US, UK and Europe. These changes prompted global equity and bond markets to fall in tandem, culminating in the worst performance for traditional portfolio holdings since the 1930s. For many, the traditional diversified portfolio was not a place of safety in these changed circumstances. The MSCI WorldMid & Large Cap index was down 18%, the S&P 500 by 19%, the FTSE 250 by 17%, the Nikkei by 9% and China’s CSI 300 by 22%.

The ultra wealthy and the global economy

Global UHNW population, real GDP and equities

Number of UHNW individuals and annual change in real GDP and equities

Sources: Wealth-X; International Monetary Fund, World Economic Outlook, July 2022 and Morgan Stanley Capital International (MSCI).

According to the Wealth-X Ultra Wealth Report, the global number of UNHWIs, generally agreed to include those with a net worth of at least $30 million, is now at just over 390,000 individuals. The management consultancy Capgemini noted in its Global Wealth Report 2023 that HNWI wealth and population totals fell by 3.6% and 3.2% respectively in 2022, while research by British property consultancy Knight Frank found that the wealth of UHNWIs declined by 10% in 2022 (equivalent to $10.1 trillion) with Europe experiencing the sharpest fall at 17% while, Africa demonstrated the most resilience with only a 5% decrease. So, although in 2021 data analysis organisation Wealth X predicted a 10% rise in UHNWIs for 2022, the total figures declined due to the war in Ukraine and the consequent impact this had on supply chains, markets, currencies and risk and linked trading conditions.

Despite these events, it seems that investors have a positive outlook for 2023 driven by asset repricing, perceived value opportunities, and an anticipated economic rebound. According to BCG’s Global Wealth Report 2023, global financial wealth is expected to rebound in 2023 by roughly 5% to reach US$267 trillion, while Credit Suisse’s Global Wealth Report 2022 suggested that global wealth will increase by US$169 trillion by 2026, a cumulative rise of 36% since 2022, and that the number of millionaires will exceed 87 million individuals over the next five years. Contributing factors to this expected growth are an overall improving global macroeconomic outlook and the ongoing rebound in stock markets (especially in the US, following the massive drops in equities and bonds in 2022), strong growth in Asia-Pacific (particularly in the tech and start-up sectors), and growth in the Middle East. However, China, which was expected to be a significant contributor to global growth in 2023, has thus far disappointed with weaker-than-expected domestic growth and there are increasing calls for the Chinese central bank and government to create more accommodative support to grow the economy.

How the wealthy are changing around the globe

According to Credit Suisse’s Global Wealth Report 2022, by the end of 2021, global wealth totaled an estimated USD 463.6 trillion, an increase of 9.8% from 2020 and far above the average annual +6.6% recorded since the beginning of the century. Excluding exchange rate movements, aggregate global wealth grew by 12.7%, making it the fastest annual rate ever recorded. However, the events of 2022 changed all that. Research from Knight Frank found that although four in ten UHNWIs saw their wealth increase in 2022, the overwhelming trend was negative. As noted by Capgemini's Global Wealth Report 2023, the global HNWI population dropped by 3.3% to 21.7 million, while the value of its wealth decreased by 3.6% to US$ 83 trillion. This marked the steepest drop in ten years (2013-2022) with North America registering the steepest wealth decline (-7.4%), followed by Europe (-3.2%) and Asia-Pacific (-2.7%). In contrast, Africa, Latin America, and the Middle East showed resilience by registering financial growth in 2022 due to strong performances in the oil and gas sectors. Knight Frank said the losses experienced by the wealthy were also due to changes in residential property values, commercial property values, fixed income, and other assets. And, it notes, a large part of the change in wealth was also driven by USD appreciation through 2022 and into 2023, which has hit emerging markets hardest.

HNWI financial growth declined in Europe, APAC, and North America

Source: Capgemini Research Institute for Financial Services Analysis, 2023.

Note: Chart numbers and quoted percentages may not total 100% due to rounding

And it isn’t just HNWIs who were hit, UNHWIs were also impacted by these shifts. According to the Wealth-X Ultra Wealth Report, for the first time since 2018, the UHNW global community shrank by 6% to 392,410 people – and the group’s total wealth dwindled by 11%, falling to $41.8 trillion. In fact, research by Alrata has shown that in 2022 there were just 3,194 billionaires across the globe.

The importance of geography

Where the wealthy live has changed over the Covid and post Covid pandemic period. As noted by residence and citizenship planning consultancy Henley & Partners in their Private Wealth Migration Report 2023, following on from the pandemic, the numbers of millionaires migrating are rising; 84,000 are estimated to have migrated in 2022 and 122,000 and 128,000 are forecast to migrate in 2023 and 2024. The increase in global geopolitical risks over the past couple of years and the consequent increase in security, political and economic risks has prompted affluent individuals and families globally to diversify their domicile portfolios via investment migration to enhance economic mobility and protect their lifestyles, wealth, and legacies.

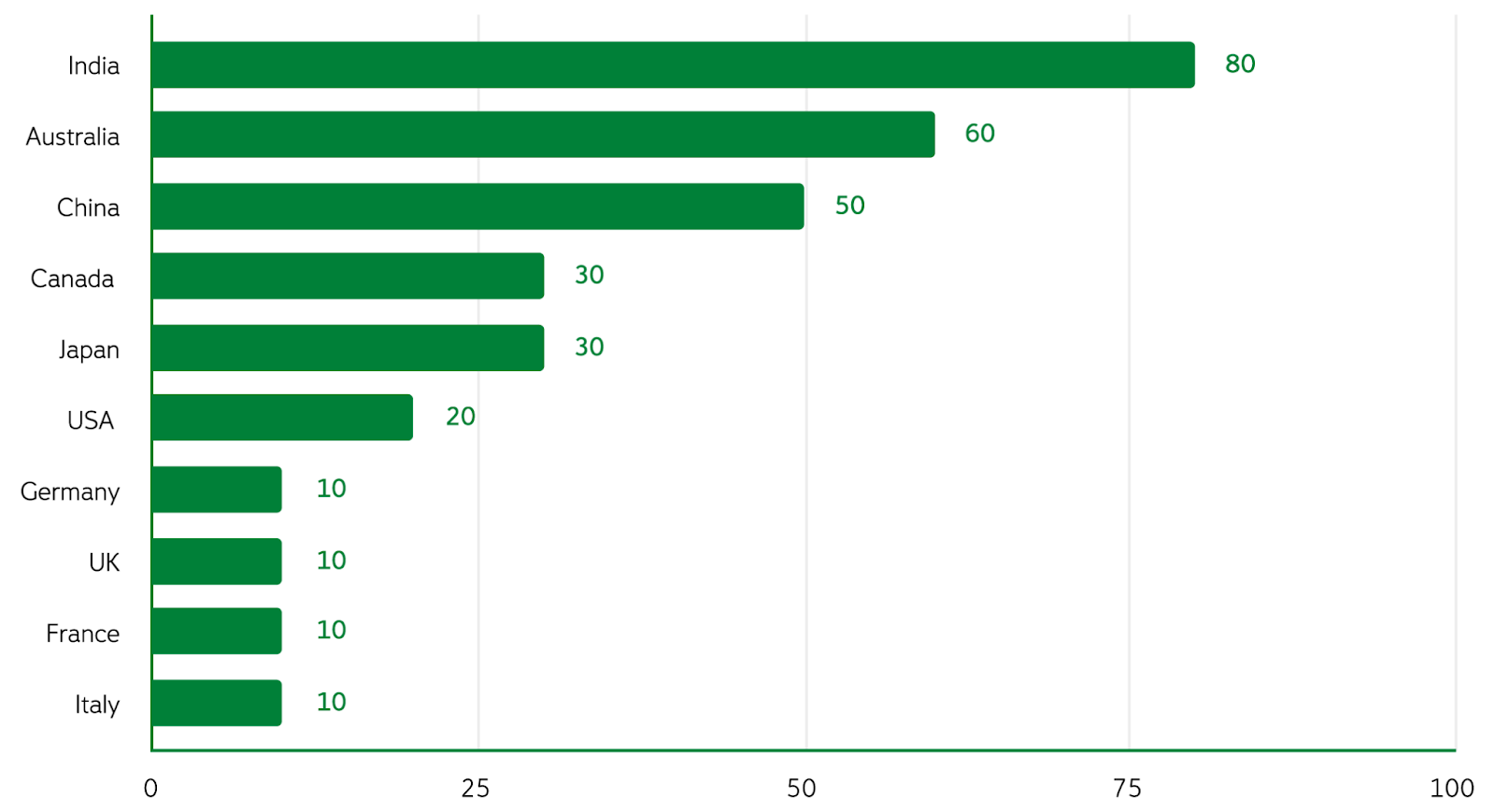

HNWI Global Migration

Source: The Henley Private Wealth Migration Report 2023

The countries that consistently attract wealthy people through migration tend to have healthy economies with relatively low crime rates and good business opportunities. Essentially, this means that in times of growing geopolitical and macroeconomic risk, there will be an increase in cross border activities. BCG notes in its wealth report that cross-border wealth rose by 4.8% in 2022 to reach $12 trillion globally as geopolitical tensions and other macro forces made certain investors reluctant to remain in their home domiciles. And, as the exchequers or treasuries in the host countries know they will benefit from any potential increase in the inflow of HNWIs and UHNWIs, they develop programmes to actively encourage applications for residency.

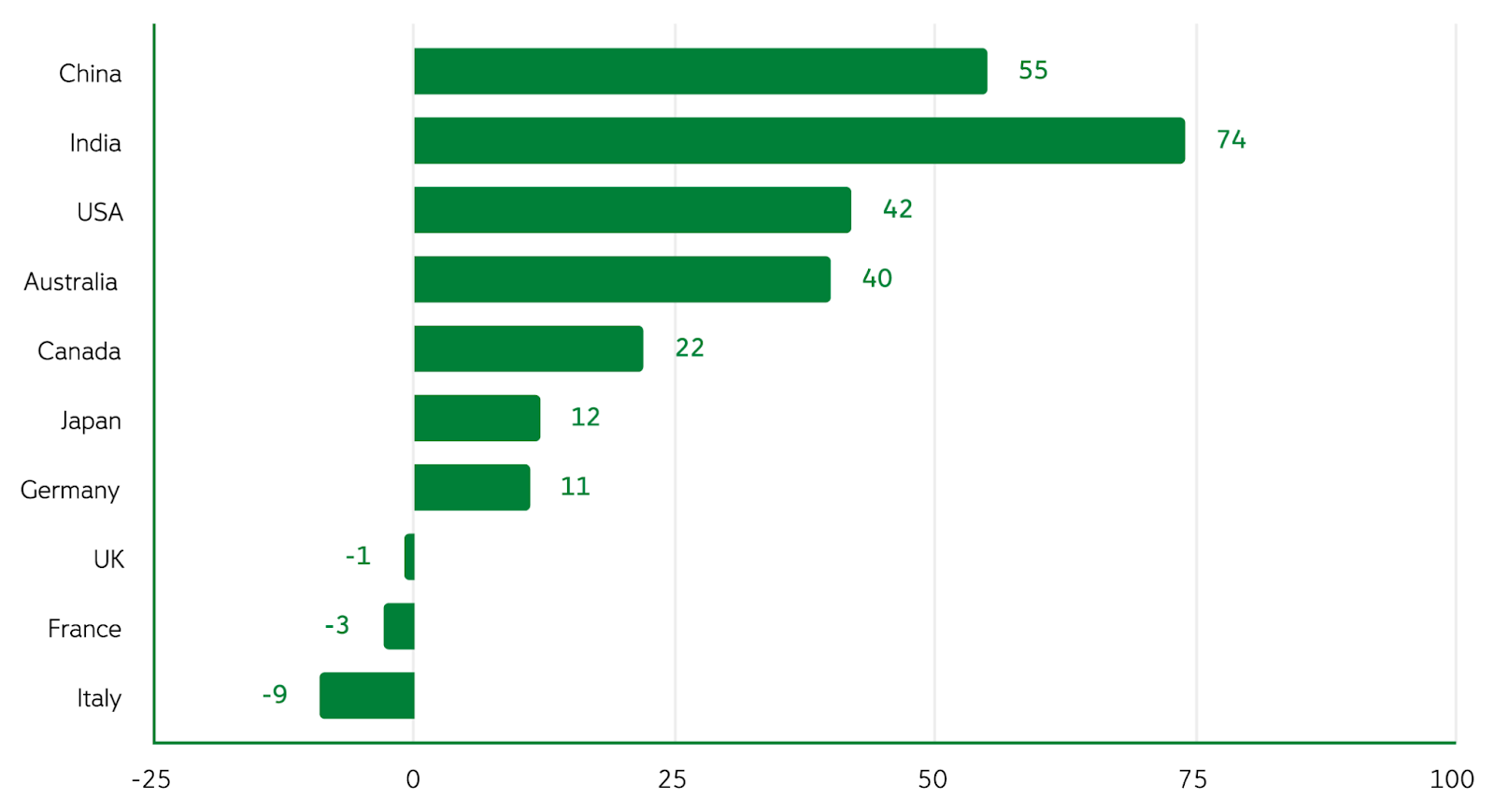

In the Henley & Partners Wealth Migration Dashboard, nine of the top 10 countries for net inflows of HNWIs in 2023 host formal investment migration programmes and actively encourage foreign direct investment in return for residence rights. It notes the top five destinations for net inflows of high-net-worth individuals in 2023 are projected to be Australia, the UAE, Singapore, the USA, and Switzerland. However, those countries with a propensity for civil unrest, domestic political and regulatory uncertainty and geopolitical conflict will likely see an outflow. Knight Frank suggests the largest net outflows of millionaires are expected to come from China, India, the UK, Russia, and Brazil.

HNWI Growth % in USD Terms

HNWI Growth % in US Dollar terms Forecast (to 2031)

Source: Henley Private Wealth Migration Dashboard 2023

Emerging markets: the new home of the wealthy

The Wealth-X Ultra Wealth Report showed a wealth shift from East to West. The Asia Pacific Region now accounts for 31.3% of the world’s UHNW individuals and 29.7% of the world’s ultra wealth. The Middle East has been boosted as markets look for alternatives to Russia’s energy supplies. This is also reflected in the relocation of the wealthy to new areas. According to Knight Frank, alternatives to Western investor visa schemes are growing, with surging applications in Turkey, as well as the more flexible offerings in Dubai, Singapore and Hong Kong.

Although the Middle East has traditionally been a source of immigration to other destinations, Henley & Partners think that Dubai is now becoming a regional hotspot. Its migration dashboard shows most incoming millionaires in 2023 are expected to come from India, with large numbers also coming from the UK, Russia, Lebanon, Pakistan, Turkey, Egypt, South Africa, Nigeria, Hong Kong, and China. They are turning to the UAE for several reasons, including its increasingly diversified economy, its low tax rates, its amenities such as shopping and luxurious real estate. Dubai has also developed a very pragmatic approach with its Golden Visa scheme, which makes longer term residency a possibility. However, one of the primary drivers of its increasing popularity for many wealthy people coming from politically unstable countries with rising incidents of civil unrest is its safe haven status, particularly in the volatile Middle East and Africa region.

Latin America should also remain on the radar as wealth there continues to grow. Although there are important differences in the growth prospects of the region with Brazil, Colombia, and Mexico all expected to grow, while others such as Chile and Peru are more likely to experience slowdown. Despite Latin America as a whole experiencing a decline in HNWIs and UHNWIs in the Covid period, Capgemini's Global Wealth Report 2023 notes that wealth in Latin America grew by 2.1%, in Africa by 1.6% and in the Middle East by 1.5%. Latin America also saw the largest growth in population of HNWIs in 2022 at a rate of 4.7%. According to the report, HNWI wealth in Latin America stood at a total of $9.2 trillion at the end of 2022, up from $7.4 trillion in 2015.

The gender element

The Wealth-X Ultra Wealth Report indicated that ongoing transfer of wealth from male to female UHNWIs was continuing despite the fall in the overall number of UHNWIs in 2022. Wealthy women now represent 11% of all global UHNWIs. In fact, just under 18% of young billionaires are women although that number is growing, particularly in Asia.

The report finds that UHNW women are, on average, far more likely to have inherited at least some of their wealth; and have a greater interest (or be working directly) in philanthropy. Asset allocation also differs between ultra wealthy women and men: real estate and luxury goods, which account for 13% of all assets among UHNW women, is three times greater than the allocation among their male counterparts.

Generational change

Alrata, in its Billionaire Census 2023, states that the median age of a billionaire is 67 years old and it defines “Young'' billionaires as those 50 years old or younger. This group accounts for only 10% of the billionaire population. And as to where that wealth is coming from, technology is the primary industry for the largest share of under-50s in both Asia and North America, whereas, in Europe, the focus remains very much on banking and finance. What is clear from the research is that there is a need for wealth managers, advisors and other service providers to recognise that the behavioural traits, experiences and abilities of the wealthy will differ significantly by generation. They will also be influenced by the changing geographies the “newer” wealthy have grown up in and the cultural context in which they operate.

According to that report, the standout trend is the larger prevalence of solely inherited wealth among the younger cohort of billionaires. This is partly attributable to the higher female representation in the under 50 population, as inheritance is a far more common source of wealth among women than men. However, it is not just billionaires passing on their wealth. Globally, there are a growing number of intergenerational wealth transfers happening for the first time. Many of these fortunes, created over recent decades – particularly in newer wealth markets – are being passed down to younger family members. Even in the US, we are seeing a new wealth transfer take place. According to the New York Times, of the $84 trillion projected to be passed down from older Americans to millennial (those born 1980-1996) and Gen X (those born 1965-1979) heirs through 2045, $16 trillion will be transferred within the next decade. High-net-worth and ultrahigh-net-worth individuals — those with at least $5 million and $20 million in cash or easily cashable assets — make up only 1.5% of all US households, but, together, they constitute 42% of the volume of expected transfers in the US through 2045, according to the financial research firm Cerulli Associates. PwC has suggested that globally, there will be a US$68 trillion transfer of wealth from baby boomers to millennials by 2030.

What do the wealthy want?

When it comes to understanding what the wealthy want in terms of wealth consolidation and wealth building, it isn’t always clear. The Covid pandemic with its lockdowns and move to digital interactions changed what the wealthy prioritise most and the type and channels for advice in relation to their wealth.

What are the wealthy's priorities?

The priorities for the wealthy are changing with much of the change being dependent on the region or country the wealthy are based in. It is clear that inflation, market volatility and interest rate movements have been the biggest concerns for the wealthy over the past two years and are likely to continue to influence their risk profiles and management requirements over the next 12-24 months.

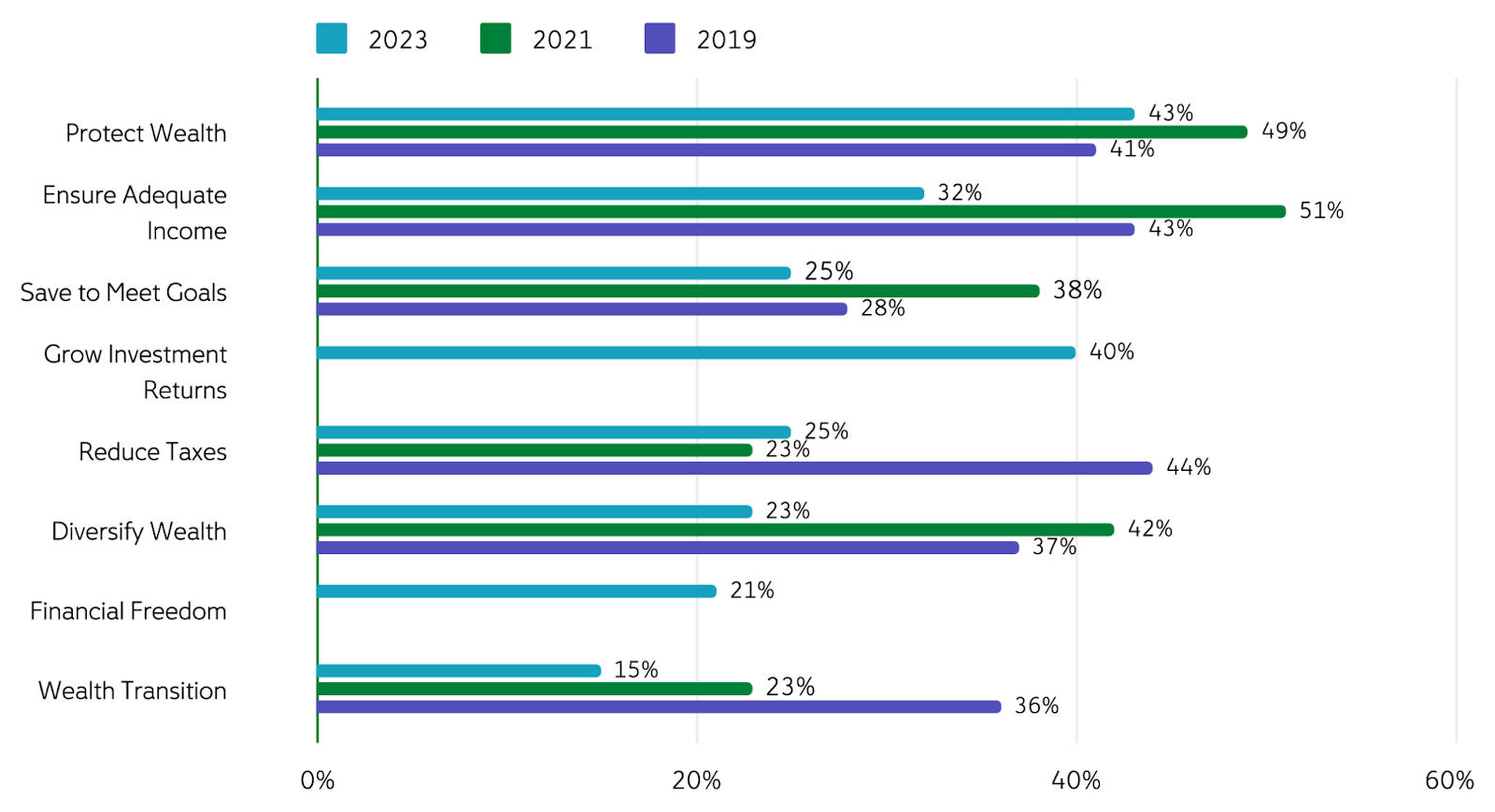

At a global level, investors are also looking for advice and tools to maintain and secure their positions. The EY Global Wealth Management Report 2023 found that investors’ three leading goals are now protecting against inflation, strengthening investment returns and ensuring financial security. Their survey found that over the past couple of years, there has been a 30% decrease in the importance placed on purposeful financial legacy goals, such as transition of wealth to family and charity. Knight Frank has found a similar response in its surveys with the main focus on capital accumulation, capital preservation, income generation, and diversification with philanthropy falling very far behind.

Top Financial Goals

Source: 2023 EY Global Wealth Management Research Report

They’ve also noticed that there is a regional element to this change in priorities as well. Their research indicates that HNWIs across Asia-Pacific are looking for growth, while preservation is the number one goal in Europe and America. This may be due the economic slowdown starting to take shape in Europe and the UK, and the possibility of recession in 2024 in the US if and when labour markets finally loosen as interest rates remain higher for longer. It could be due to Asia-Pacific having a higher percentage of younger and self made HNWIs and UHNWIs that are more focused on growth. In the UK the situation is slightly different. A survey by RBC Wealth Management shows that inheritance tax (IHT) is the number one immediate concern for HNWIs in the UK across age groups and gender. IHT is of particular concern for almost half of those aged 66+ (45%), but 72% of all respondents feel they need guidance on taxation and efficient planning. The same survey found that 33% of women are concerned about maintaining their lifestyle in later life vs 21% of men. From a generational perspective, 80% of 25-34 year olds felt the weight of the responsibility of managing and preserving wealth, and 82% of 35-54 year olds felt the need for guidance in educating the next generation about wealth management.

However, in Latin America, given the limitations of the banking sector and the fact that many investors are worried by economic, social and political volatility in their countries and want to have access to global markets in order to achieve jurisdictional diversification, the focus for many would also be wealth preservation.

How have their investments changed?

As noted by Capgemini's Global Wealth Report 2023, HNWIs have shifted their investment interests, largely in response to growing market complexity and volatility. According to the EY Global Wealth Management Report 2023, 40% of the 2,700 of their clients they surveyed across 7 geographies think that managing their wealth has become more complex over the last two years, while only 14% say it has gotten easier. The same survey indicated that 45% felt that their investment needs had become more complex. This may be due to changing global performance dynamics resulting from geopolitical events as well as the introduction of new investment products such as digital assets and the growing availability of online and hybrid offerings. PwC has noticed that shifts in investment allocation—including greater demand for exchange-traded funds (ETFs)—are transforming the competitive landscape and the frontiers for growth. But the wealthy have been reacting to the changes in the markets as global rates continue to rise; the focus on equity investments have shifted from growth to value. There also have been significant reallocations: (a) those towards passive investments as investors look for a transparent, liquid and low-cost option; and (b) those towards private markets as investors ramp up the search for returns and hedges against market volatility.

For many HNWIs, the continuing market uncertainties have left them changing the focus of their investment portfolios. Both Capgemini and Knight Frank found that HNWIs are increasing their cash and cash equivalent holdings due to rising interest rates. Knight Frank found that they are also looking to reduce debt levels because of these high rates with the appetite to deleverage highest among Europeans. UBS has found that there has been a revival of fixed income and active management as a means of portfolio diversification with the most favoured diversification strategy currently focussing on high-quality short-duration fixed income.

Percentage of clients looking for more advice in investment services

Source: 2023 EY Global Wealth Management Research Report

The wealthy are also looking at new products to invest in. Although EY says clients are relatively satisfied with the performance of core investment products such as actively managed funds and passive funds like ETFs or index trackers, newer asset classes such as cryptocurrencies or non-fungible tokens (NFTs) are spiking interest as well as ESG investing. However, ESG may be limited by uncertainties around ESG risk measurement. Capgemini found that 63% of participants in their 2023 HNWI survey said they had requested reliable and traceable ESG scores for their assets. Alternatives are also of interest but are not as well understood as other asset classes despite private debt and private equity markets opening up more for individual investors. Capgemini found that interest in other alternative investments such as hedge funds, FX and commodities has fallen.

How have their investing styles changed?

It is not just the primary products investors are interested in that is changing; there is an increasing desire to spread assets between multiple providers. EY found that a third of their clients were increasing allocations to active investments and increasing exposures to savings and deposits. Although, according to EY, the wealthy are increasingly working with FinTechs to manage their wealth. The wealthy have become more comfortable with virtual interactions including advisory services. EY’s research indicated that the number to work with Fintechs will double from 9% to 18% over the next three years – attracted by the sector’s low charges, specialised digital experiences and low-friction switching. That growth is expected to be even more dramatic in Europe (increasing from 11% of clients to 23%), Asia-Pacific (14% to 26%) and the Middle East (8% to 41%). They also found that their wealth management clients increasingly preferred virtual consultations with over 40% in their 2023 survey listing it as their most preferred channel for planning and advice activities; this is a sharp jump up from the 12% that cited it as their preferred method in 2021.

The wealthy want to be able to access their relationship managers virtually as well as in-person. This means equipping advisors with the tools and training to effectively use digital collaboration tools to be able to provide more pro-active interactions thereby allowing wealthy clients to feel they are receiving a more personalised engagement.

Preferred engagement channel

Source: 2023 EY Global Wealth Management Research Report

Another important element that should be taken into consideration is the use of generative AI. The wealthy, particularly younger generations, are more likely to want to use AI in generating investment ideas, and checking those ideas through various scenarios against how individual securities might help their portfolios, from both a performance and risk viewpoint. Although AI will not replace traditional advisory services as the “human” touch is still wanted and welcomed, it is becoming clearer the technology will undoubtedly be a key driver for the wealthy in choosing their financial services providers. It will create cost efficiencies for finance service suppliers through the onboarding processes, and, if managed correctly it will, as suggested by EY, create the seamless element of a client’s larger portfolio management.

Finally, given the transfer of wealth that is taking place generationally, there is also likely to be further demand for ESG products if appropriate due diligence frameworks are in place.

Conclusion

Significant risks remain for the global economy. Inflation remains sticky in major economies and interest rates, although widely expected to pause later this year and start to come down in 2024, are still rising along with geopolitical risk.

However, HNW and UHNW investors are looking beyond these risks, seeking to find new ways to preserve existing wealth while growing it. And, as we start to see a further acceleration of generational shifts in wealth align with a rising proportion of the ultra wealthy originating from and living in emerging economies, we should also expect to see more wealthy that are comfortable with and seek out financial services and financial service providers that are able to provide access to new technologies such as generative AI that may help clients better understand how different scenarios may affect their portfolio allocations based on their risk preferences. There will be increasing pressure to get the customer proposition right against a backdrop of an unprecedented transfer of wealth from baby boomers to millennials, from traditionally “rich” developed countries to faster growing and possibly even more entrepreneurial Emerging markets.

Looking forward, financial service providers of all types including banks, fintechs, wealth advisors and wealth managers, will need to streamline and improve relationship management through technology by offering their existing and future clients a one stop experience with easily accessible and efficient omnichannel interactions that provide a customisable and personalised client experience.

Sources

- Altrata Billionaire Census 2023 https://altrata.com/reports/billionaire-census-2023

- BCG Global Wealth Report 2023: Resetting the Course https://web-assets.bcg.com/fb/64/e10897864913a480415d0e1fe3c6/bcg-global-wealth-report-2023-june-2023.pdf

- Capgemini World Wealth Report 2023 https://www.capgemini.com/insights/research-library/world-wealth-report/

- Credit Suisse Global Wealth Report 2022 https://www.credit-suisse.com/about-us/en/reports-research/global-wealth-report.html

- EY Global Wealth Management Report 2023 https://www.ey.com/en_gl/walth-management-research

- Frank Knight. The Wealth Report: Outlook 2023 https://content.knightfrank.com/resources/knightfrank.com/wealthreport/the-wealth-report---apr-2023.pdf

- Henley & Partners Africa Wealth Report 2023 https://www.henleyglobal.com/publications/africa-wealth-report-2023

- Henley & Partners Private Wealth Migration Report 2023 https://www.henleyglobal.com/publications/henley-private-wealth-migration-report-2023

- Henley & Partners Wealth Migration Dashboard https://www.henleyglobal.com/publications/henley-private-wealth-migration-dashboard

- PwC 2023 Global Asset and Wealth Management Survey https://www.pwc.com/gx/en/industries/financial-services/asset-management/publications/asset-and-wealth-management-revolution-2023.html

- RBC Wealth Management https://www.rbcwealthmanagement.com/en-eu/newsroom/2023-02-13/new-research-reveals-top-concerns-of-high-net-worth-individuals-in-2023

- The New York Times, Talmon Joseph Smith, “The Greatest Wealth Transfer in History Is Here, With Familiar (Rich) Winners,” https://www.nytimes.com/2023/05/14/business/economy/wealth-generations.html

- Wealth–X World Ultra Wealth Report 2022 https://altrata.com/reports/world-ultra-wealth-report-2022

- UBS Global Family Office Report 2023 https://www.ubs.com/global/en/family-office-uhnw/reports/global-family-office-report-2023.html

DISCLAIMER: While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

Questo articolo viene fornito all'utente soltanto a scopo informativo e non deve essere considerato come un'offerta o una sollecitazione di un'offerta di acquisto o di vendita di investimenti o servizi correlati che possono essere qui menzionati.