Policy ambition meets economic gravity

What to look out for today

Companies reporting on Wednesday, 25th February: APA, Lowe’s Companies, Nvidia, Paramount Skydance, Pinnacle West Capital, Raymond James Financial, Salesforce, TKO Group

Key data to move markets today

EU: German GDP, German GfK Consumer Confidence, and Eurozone Harmonised Index of Consumer Prices

US: Speeches by Richmond Fed President Thomas Barkin, Kansas City Fed President Jeff Schmid, and St Louis Fed President Alberto Musalem

US Stock Indices

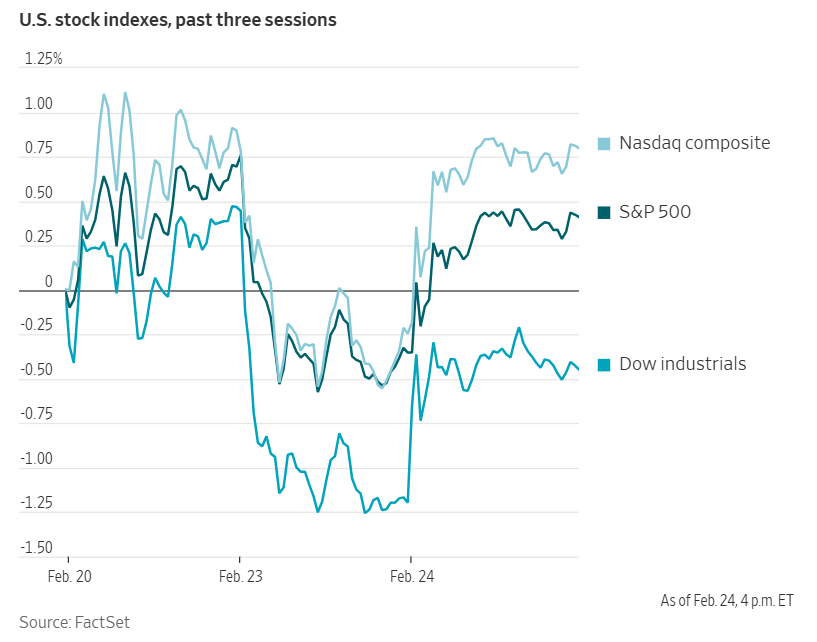

Dow Jones Industrial Average +0.76%

Nasdaq 100 +1.09%

S&P 500 +0.77%, with 9 of the 11 sectors of the S&P 500 up

A massive chip deal announced on Tuesday contributed to a recovery in stock prices following Monday’s decline, which was driven by concerns surrounding AI disruption.

Prior to the opening bell, Meta Platforms revealed plans for a purchase exceeding $100 billion in AI chips from AMD. This disclosure propelled shares of AMD, a competitor to Nvidia, +8.77%. Companies that had experienced notable losses on Monday, including IBM and Oracle, saw their stock prices rebound.

The Nasdaq Composite advanced +1.04%, while the S&P 500 and Dow Jones Industrial Average rose +0.77% and +0.76%, respectively.

In corporate news, sources familiar with the situation reported that the Pentagon has informed Anthropic that its military contracts may be terminated on Friday unless the artificial intelligence startup complies with government requirements for the use of its technology.

Warner Bros. Discovery is currently evaluating a renewed takeover proposal from Paramount Skydance, valued at $31 per share and featuring improved terms. This development marks the latest chapter in the ongoing contest for control of one of Hollywood’s most renowned studios.

Home Depot announced that a key sales metric had surpassed expectations for the most recent quarter, supported by steady consumer demand. Nevertheless, the retailer cautioned that broader macroeconomic challenges persist.

Novo Nordisk has disclosed plans to reduce the US list prices of its leading medications, Wegovy and Ozempic, beginning next year. This move comes as the pharmaceutical company seeks to regain a greater share of the obesity treatment market.

S&P 500 Best performing sector

Consumer Discretionary +1.46%, with Booking +5.11%, Expedia +5.10%, and Royal Caribbean Group +4.58%

S&P 500 Worst performing sector

Health Care -0.53%, with Molina Healthcare -5.06%, CVS Health -3.66%, and Humana -3.60%

Mega Caps

Alphabet -0.25%, Amazon +1.60%, Apple +2.24%, Meta Platforms +0.32%, Microsoft +1.18%, Nvidia +0.68%, and Tesla +2.39%

Information Technology

Best performer: Keysight Technologies +23.05%

Worst performer: Fair Isaac -4.21%

Materials and Mining

Best performer: Albemarle +5.24%

Worst performer: Steel Dynamics -2.62%

Corporate Earnings Reports

Posted on Tuesday, 24th February

Home Depot quarterly revenue -3.79% to $38.198 bn vs $38.090 bn estimate

EPS at $2.53 vs $2.72 estimate

Ted Decker, Chair, President and CEO, said, “Throughout fiscal 2025, our teams did an incredible job engaging with our customers and growing market share, and I would like to thank them for their hard work and dedication. For the fourth quarter, our results were largely in-line with our expectations, reflecting the lack of storm activity in the third quarter and ongoing consumer uncertainty and pressure in housing. Adjusting for storms, underlying demand was relatively stable throughout the year.” — see report.

Keurig Dr Pepper quarterly revenue +10.5% to $4.499 bn vs $4.361 bn estimate

EPS at $0.60 vs $0.59 estimate

Tim Cofer, CEO, said, “2025 was another strong year for KDP. We delivered on our guidance, navigated the dynamic operating environment with agility, and executed well in the marketplace with winning innovation and robust commercial activation of our brands. In 2026, we intend to build upon our momentum with the acquisition and integration of JDE Peet's and progress towards the subsequent separation into two advantaged pure play companies.” — see report.

Mosaic quarterly revenue +5.6% to $2.974 bn vs $2.934 bn estimate

EPS at $0.22 vs $0.49 estimate

Bruce Bodine, President and CEO, said, “Mosaic made significant progress in 2025. We fortified our assets to ensure reliable production, delivered meaningful cost and efficiency progress and divested non-core assets. Deferred demand and higher raw material costs negatively impacted our year end results, but demand is expected to recover as we move toward the planting season.” — see report.

European Stock Indices

CAC 40 +0.26%

DAX -0.02%

FTSE 100 -0.04%

Commodities

Gold spot -1.67% to $5,140.55 an ounce

Silver spot -1.22% to $87.11 an ounce

West Texas Intermediate -0.32% to $66.08 a barrel

Brent crude -0.31% to $71.24 a barrel

Gold prices declined on Tuesday, retreating from a three-week peak, as profit-taking activity and a strengthening US dollar exerted downward pressure.

Spot gold fell -1.67%, settling at $5,140.55 per ounce. Earlier in the session, prices reached their highest level in three weeks.

The US dollar index advanced +0.18%, thereby rendering dollar-denominated bullion more expensive for investors holding other currencies.

Spot silver declined -1.22% to $87.11 per ounce, following a rise of +4.27% on Monday that brought prices to a more than two-week high, driven by heightened concerns over miner safety after violent incidents involving cartels in Mexico.

Oil prices declined slightly on Tuesday, closing less than one percent lower, as Iran expressed its readiness to take all necessary measures to achieve a nuclear agreement with the US. This development follows several weeks of heightened US military presence in the Middle East.

Brent crude futures settled at $71.24 per barrel, a decrease of 22 cents, or -0.31%. US WTI futures declined by -0.32%, closing at $66.08 per barrel, down 21 cents.

Iran, the third-largest crude oil producer within OPEC, is scheduled to engage in a third round of nuclear negotiations with the US on Thursday in Geneva, as announced by Oman's Foreign Minister Badr Albusaidi on Sunday.

Trading firms and purchasers of Venezuelan oil have begun chartering the first very large crude carriers to export from Venezuela since the initiation of a supply agreement between Caracas and Washington. These shipments, expected to accelerate in March, aim to increase deliveries, particularly to India, according to industry sources and available data.

The European Commission is preparing to submit a legal proposal on 15th April to permanently ban imports of Russian oil. This initiative will follow Hungary's parliamentary elections by three days, according to EU officials and a document reviewed by Reuters.

Additionally, Russia's oil pipeline monopoly, Transneft, has reduced its crude intake by approximately 250,000 barrels per day, according to sources familiar with the matter per Reuters. This action comes after Ukrainian drone strikes targeted a pumping station that services several major oil hubs and ports.

Note: As of 4 pm EST 24 February 2026

Currencies

EUR -0.11% to $1.1771

GBP -0.01% to $1.3487

Bitcoin -0.80% to $64,056.00

Ethereum -0.47% to $1,854.41

The US dollar index advanced +0.18% to 97.88 on Tuesday, while the euro depreciated -0.11% to $1.1771. Sterling experienced a marginal decline of -0.01%, settling at 1.3487.

The Japanese yen weakened on Tuesday, slipping -0.80% to ¥155.88 per dollar, following a news report indicating that Prime Minister Sanae Takaichi had expressed her reservations about further interest rate hikes to BoJ Governor Kazuo Ueda. This development has raised concerns regarding the timing of the next rate increase and suggests the possibility of friction over monetary policy, potentially complicating the BoJ’s coordination with the newly strengthened administration.

In the wake of these reports, traders are currently pricing in a 50% probability of a rate hike in April and a 65% chance of an increase by June.

Fixed Income

US 10-year Bond -0.1 basis points to 4.035%

German 10-year -0.6 basis points to 2.709%

UK 10-year gilt -0.7 basis points to 4.304%

On Tuesday, short-term US Treasury yields remained confined within a narrow range, registering modest gains as investors assessed the implications of the Supreme Court’s decision to block President Trump’s tariffs imposed under emergency powers.

At the front end of the yield curve, the two-year Treasury yield, closely tied to market expectations of Fed fund rates, rose +2.1 bps, reaching 3.472%.

During afternoon trading, the 10-year yield edged down -0.1 bps to 4.035%. This follows Monday’s session, when the 10-year yield touched its lowest level since late November.

The yield on the 30-year US Treasury declined -1.9 bps to 4.686%.

The US Treasury conducted a $69 billion auction of two-year notes on Tuesday, yielding lackluster results. The auction priced at 3.455%, slightly above the anticipated yield at the bid deadline, indicating that investors sought a modest premium. The bid-to-cover ratio stood at 2.63x, below the three-auction average of 2.66x.

In contrast, the previous two-year note auction in January proceeded smoothly, with end-user demand, comprising both indirect and direct bids, reaching its highest level since February 2025.

The yield curve flattened for the tenth consecutive session on Tuesday, as the spread between two- and 10-year yields narrowed to 56.3 bps, down from 58.5 bps at the close of the previous session.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing in 55.0 bps of cuts in 2026, lower than the 59.5 bps priced in the previous week. Fed funds futures traders are now pricing in a 2.0% probability of a 25 bps rate cut at the 18th March FOMC meeting, down from 7.4% a week ago.

Eurozone government bond yields extended their decline on Tuesday, as increased safe-haven demand supported the market. Italy's 10-year yield fell to its lowest level in more than a year, while France's benchmark yield reached a six-month low.

Germany's 10-year yield declined -0.6 bps to 2.709%, after briefly touching a two-month low of 2.697% earlier in the session. Shorter-maturity, rate-sensitive European yields saw more modest movements, with Germany's 2-year yield slipping -0.3 bps to 2.044%. At the longer end of the curve, Germany's 30-year yield rose by +4.1 bps to 3.379%.

Other European yields mirrored this shift in yields. Italy's 10-year yield dropped -0.5 bps to 3.320%, after marking a low of 3.315%, a level not seen since December 2024. The yield spread between German and Italian government bonds stood at 61.1 bps.

France's 10-year yield also declined, falling -1.7 bps to 3.267%, its lowest point since August 2025.

Note: As of 5 pm EST 24 February 2026

Global Macro Updates

POTUS touts economic accomplishments in SOTU address. President Trump highlighted his administration’s economic achievements during Tuesday’s State of the Union address, emphasising progress in reducing inflation, increasing incomes, and lowering prescription drug prices. He presented a legislative agenda for his second year that included a call for Congress to support a proposal prohibiting institutional investors from purchasing single-family homes. Trump also outlined a retirement savings initiative that would enable the government to match up to $1,000 in contributions for workers without access to a 401(k) plan. He reiterated support for his healthcare plan, unveiled in January, which would direct government subsidies to consumers; however, these proposals are expected to encounter resistance in Congress.

President Trump moderated his criticism of the Supreme Court’s decision to overturn IEEPA tariffs, stressing the continued authority to impose tariffs under separate trade statutes, and noted that most countries remain committed to existing trade agreements. Immigration was a major theme of the address, with Trump citing enforcement actions and a decline in illegal border crossings. He appointed Vice President Vance to lead anti-fraud initiatives, which he asserts will benefit the federal budget. Trump confirmed an agreement with major technology companies to assume greater responsibility for energy costs. Regarding Iran, he offered no new policy updates, reaffirming his preference for a diplomatic resolution while asserting that Tehran must never acquire nuclear weapons.

February consumer confidence rises on better labour market outlook. The February reading for US consumer confidence exceeded market expectations, registering at 91.2 compared to the consensus forecast of 88.0 and up from January’s 89.0. Despite this increase, the Present Situation Index declined by 1.8 points to 120.0, and the Expectations Index decreased by 4.8 points to 72.0, indicating some caution regarding future conditions.

Labour market perceptions showed modest improvement. The share of consumers describing jobs as “plentiful” rose to 28.0% from January’s 25.8%. However, 20.6% of respondents indicated that jobs were “hard to get,” up from 19.0% previously, and 15.7% anticipated more job opportunities in the future, a slight increase from 14.8% in January.

Inflation expectations over the next twelve months remained largely unchanged, though they continued to be elevated. According to the report, open-ended responses from consumers remained generally pessimistic, with inflation and price levels cited most frequently as concerns. Additionally, mentions of trade and political issues increased in February, while apprehensions about the labour market lessened somewhat.

In related economic data, the Richmond Fed Index declined to -10.5 in February, compared to a consensus estimate of -2.5 and January’s reading of -6.0. Within the report, shipments fell to -13 from -5, new orders moved down to -9 from -6, and the employment index edged lower to -7 from -6. Notably, the average growth rates for both prices paid and prices received slowed during February, with firms anticipating continued moderation in pricing pressures over the next year.

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

Tento článek je poskytován pouze pro informační účely a neměl by být považován za nabídku nebo výzvu k nákupu nebo prodeji jakýchkoli investic nebo souvisejících služeb, jejichž odkazy se v něm můžou vyskytovat. Obchodování s finančními nástroji je spojeno se značným rizikem ztráty a nemusí být vhodné pro všechny investory. Dřívější produktivita není spolehlivým ukazatelem budoucí produktivity.

Založeno profesionály. Pro profesionály.