A better US consumer outlook ahead?

Key data to move markets today

EU: A speech by Banco de España Governor José Luis Escrivá

USA: FOMC Minutes

CHINA: CPI

Global Macro Updates

NY Fed consumer survey: higher inflation expectations, better labour market views. The latest New York Fed Survey of Consumer Expectations pointed to higher inflation expectations alongside a modest improvement in household views of the labour market and personal finances.

In the June survey, median one-year-ahead inflation expectations rose to 3.7%, the highest level since September 2023, from 3.5% in May. Three-year expectations increased to 3.3% from 3.1%, while five-year expectations were unchanged. Despite the upward move in near- and medium-term expectations, median inflation uncertainty declined across all time horizons.

Labour market perceptions also improved. Respondents assigned a lower probability to the US unemployment rate being higher over the next 12 months, although the measure remained above recent averages. The mean perceived probability of losing one’s job over the next year fell to 14.1% from 15.1% in May, moving below its trailing 12-month average. Meanwhile, expectations of finding a new job after a job loss rose to 44.9% from 43.7%, driven by respondents earning less than $50,000.

Household income expectations were broadly stable, with median expected income growth over the next year edging up to 3.0% while remaining within the narrow range observed over the past year. Credit conditions also appeared to improve, as the average perceived probability of missing a minimum debt payment declined by 1.8 percentage points to 10.8%, the lowest reading since April 2023.

Overall household sentiment strengthened. Respondents reported an improved assessment of their current financial situation compared with a year earlier, with fewer households describing conditions as worse and a larger share reporting improvement. Expectations for the year ahead also improved.

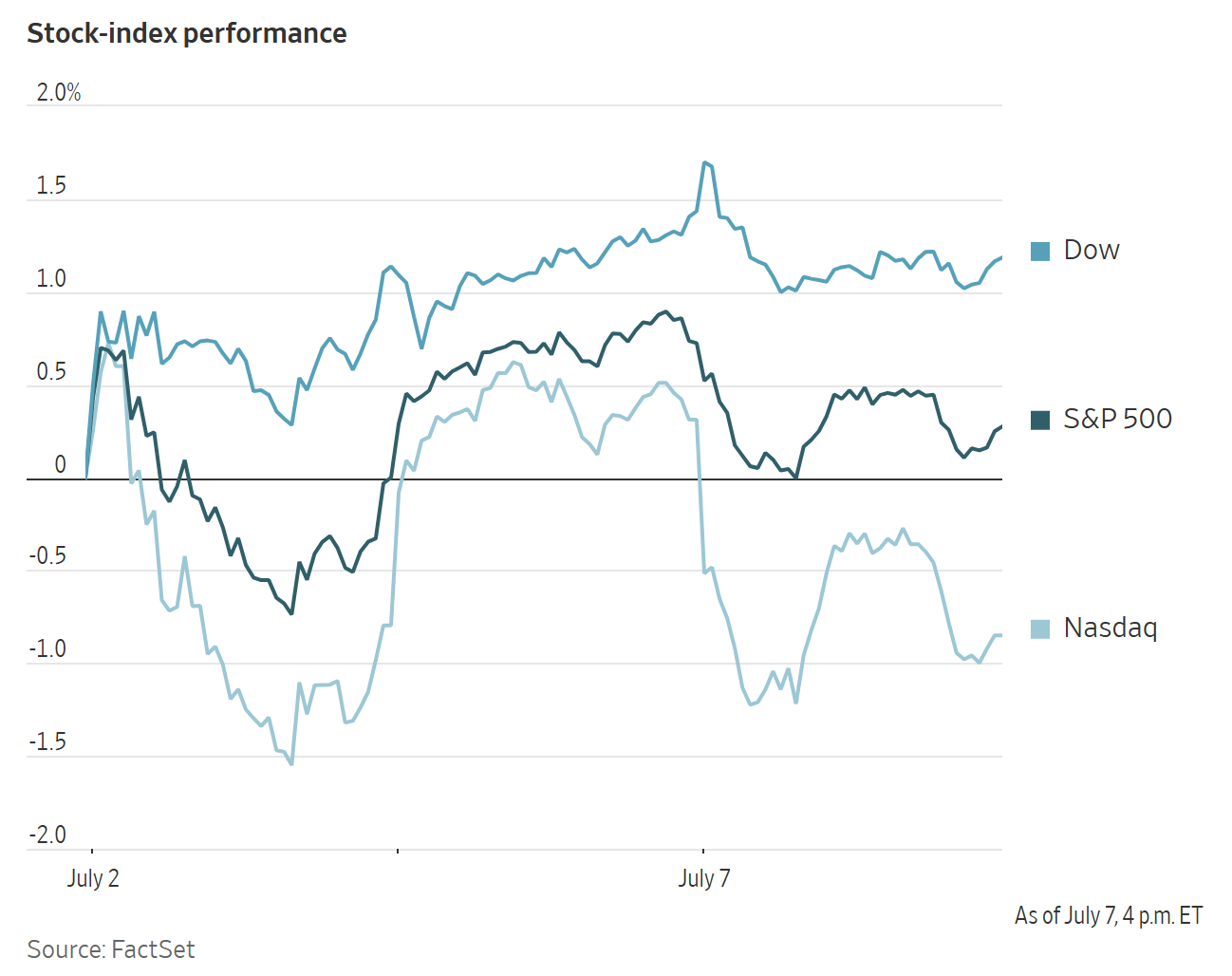

US Stock Indices

Dow Jones Industrial Average -0.25%

Nasdaq 100 -1.77%

S&P 500 -0.45%, with 5 of the 11 sectors of the S&P 500 down

US equities closed lower on Tuesday. The Nasdaq Composite fell -1.16%, to 25,818.69 weighed down by semiconductor stocks. The S&P 500 dropped -0.45% to 7,503.85. The Dow Jones Industrial Average slipped -0.25%, or 130.76 points, to 52,925.15.

In corporate news, SK Hynix’s planned $28 billion US listing is several times oversubscribed ahead of pricing on Thursday, according to people familiar with the matter, as reported by Bloomberg news. The South Korean memory chipmaker has drawn strong early demand from global long-only funds and technology-focussed investors. The company began marketing 177.9 million American depositary receipts (ADRs) on Monday, with the sale valued at about $28 billion based on Friday’s closing price for its common shares in Seoul. Roughly 1,000 institutional investors joined a management marketing call on Monday, Bloomberg reported. Each ADR represents one-tenth of a common share, and the offering is equivalent to about 2.5% of SK Hynix’s market value, which has more than tripled this year to above $1 trillion despite sharp volatility in global chip stocks.

Separately, demand for Amazon’s latest $25 billion bond offering was comparatively more restrained than for its previous record-sized deal. Peak orders reached $62 billion, according to people familiar with the matter. This was roughly half the demand seen for Amazon’s $37 billion bond sale in March, when investor appetite was amplified by enthusiasm surrounding the AI investment cycle.

In the banking sector, The Wall Street Journal reported that major banks, including JPMorgan Chase, held preliminary discussions about acquiring a Fiserv network that could allow them to bypass federal debit-card fee caps. The Durbin amendment to the 2010 Dodd-Frank law caps debit-card fees for large banks, although ownership of such a network could potentially provide an exemption. Some bank executives involved in the early talks were reportedly concerned about possible political backlash from lawmakers and regulators.

European Stock Indices

CAC 40 -0.51%

DAX -1.37%

FTSE 100 +0.13%

Commodities

Gold spot -1.40% to $4,105.70 an ounce

Silver spot -3.52% to $59.97 an ounce

West Texas Intermediate +5.15% to $72.13 a barrel

Brent crude +7.14% to $75.88 a barrel

Gold declined on Tuesday, with spot prices falling -1.40% to $4,105.70 per ounce.

China’s central bank extended its gold-buying streak to a 20th consecutive month, lifting reserves to 75.44 million fine troy ounces by the end of June from 74.96 million a month earlier.

Hong Kong also launched a central clearing system for gold and revived gold futures trading, reinforcing its ambition to become a regional reserve hub for bullion.

Spot silver weakened, dropping -3.52% to $59.97 per ounce.

Oil prices advanced sharply on Wednesday after the US military launched airstrikes against Ira, raising concerns that a fragile truce was deteriorating and that Middle East supply flows could again face disruption. The US is reported to have reimposed crude sales sanctions, revoking a temporary general licence authorising the sale and transaction of Iranian oil.

Brent crude futures rose $5.06, or +7.14%, to $75.88 per barrel, while US WTI crude gained $3.53, or +5.15%, to $72.13 per barrel.

US Central Command said the strikes followed Iranian attacks on three commercial vessels transiting the Strait of Hormuz, a critical waterway for transporting Middle Eastern oil to global markets.

Reuters also reported that a Saudi-flagged crude oil tanker was damaged near the Strait of Hormuz, close to the coast of Oman, while a Qatari LNG tanker suffered significant damage after being struck in the same area. Iran’s Foreign Minister Abbas Araghchi warned that negotiations on a final deal would not begin if US threats continued, following remarks from the US president that the US would ‘finish the job’ if no peace deal were reached with Iran.

Bloomberg news reported, citing Kpler data, that the Iran-approved corridor along the north side of the strait accounted for two-thirds of all transits in recent days, with the remainder crossing along the US-managed Oman route.

Japan is expected to receive additional Middle East crude supply this month, with two very large crude carriers loaded with Saudi crude heading for the Strait of Hormuz, Reuters reported, citing Kpler and LSEG data.

Saudi Arabia is also reportedly considering expanding the capacity of its crude oil pipeline to the western Red Sea coast. This would allow it to move more oil without relying on the Strait of Hormuz.

Shell said it expects to book significantly stronger oil and LNG trading results for Q2, reflecting heightened volatility in energy markets amid the Middle East conflict.

The US Transportation Department said US airline fuel costs rose eighty five percent in May to nearly $6.7 billion amid the Middle East conflict.

In India, fuel consumption reportedly fell 3.7% m/o/m in June to 19.24 million metric tons.

Note: As of 4 pm EDT 7 July 2026

Currencies

EUR -0.36% to $1.1433

GBP -0.28% to $1.3380

Bitcoin -1.63% to $63,392.91

Ethereum -2.21% to $1,772.92

The US dollar edged up to its highest level in a week on Tuesday. The US dollar index rose +0.27% to 101.12.

The euro slipped -0.36% to $1.1433, while sterling eased -0.28% to $1.3380.

The yen moved toward a fresh 40-year low after BoJ board member Toichiro Asada, the sole dissenter from the BoJ’s June decision to raise interest rates, told Reuters he would need to see signs of demand-driven inflation before supporting further hikes. The dollar strengthened +0.02% to ¥162.13, advancing for a third session and reaching its strongest level since 2 July.

Fixed Income

US 10-year Treasury +8.1 basis points to 4.556%

German 10-year Bund +4.6 basis points to 2.999%

UK 10-year Gilt +5.0 basis points to 4.853%

US Treasuries declined on Tuesday as investors prepared for a heavy auction schedule expected to test demand for US government debt.

On Tuesday, the Treasury sold $142 billion in US 6-week and 52-week bills, as well as $58 billion in 3-year notes. The US 3-year note auction was well received, pricing at a lower-than-expected 4.179% and indicating that investors did not require a yield concession to absorb the issue. Following the sale, US 3-year yields briefly trimmed their rise before moving higher again with the broader market, trading up +6.1 bps on the day at 4.208%.

The Treasury is scheduled to auction $72 billion in 17-week bills and $39 billion in 10-year notes today. On Thursday, it will sell $195 billion in 4-week and 8-week bills, along with $22 billion in 30-year bonds.

Against this backdrop, the US 10-year yield rose +8.1 bps to a four-week high of 4.556%, while the US 30-year yield climbed +6.8 bps to 5.056%, also reaching a four-week peak.

At the front end of the curve, the US 2-year yield rose +7.7 bps to 4.197%, rebounding after two days of declines.

The yield curve initially steepened for a fifth consecutive session, with the spread between US 2-year and 10-year yields widening to as much as 37.8 bps, the highest in three weeks. By afternoon trading, however, the spread was 35.9 bps, little changed from Monday’s 35.5 bps spread.

Eurozone bond yields rose on Tuesday as investors assessed the longer-term borrowing outlook, with attention centred on French political risk as well as Germany’s budget and fiscal policy.

Germany’s 10-year yield rose +4.6 bps to 2.999%, after earlier reaching its highest level since 19 June. Germany’s 2-year yield rose +4.1 bps to 2.595%.

Banca d'Italia Governor Fabio Panetta, a member of the ECB Governing Council, said the eurozone economic outlook remains fragile.

ECB Executive Board member Isabel Schnabel said the eurozone economy had not returned to its pre-Iran war state despite the decline in oil prices, as core inflation remained firm and price pressures persisted.

Money markets are pricing in one additional ECB rate increase this year.

In France, an appeals court upheld the conviction of the head of the populist National Rally, Marine Le Pen, for misusing EU funds, but shortened her ban on running for public office. This preserved her path to contest the 2027 presidential election.

The court also ruled that Le Pen must wear an electronic ankle tag for one year, a condition that could make a presidential campaign politically and logistically difficult. Le Pen has stated that she will make her fourth run for the Presidency.

French 10-year OAT yields rose +5.4 bps to 3.675%.

Note: As of 4 pm EDT 7 July 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

Tento článek je poskytován pouze pro informační účely a neměl by být považován za nabídku nebo výzvu k nákupu nebo prodeji jakýchkoli investic nebo souvisejících služeb, jejichž odkazy se v něm můžou vyskytovat. Obchodování s finančními nástroji je spojeno se značným rizikem ztráty a nemusí být vhodné pro všechny investory. Dřívější produktivita není spolehlivým ukazatelem budoucí produktivity.

Přihlásit se k odběru přehledů trhu

Přihlásit se k odběru

přehledů

trhu

Předplaťte si nyní

Založeno profesionály. Pro profesionály.