Is the US service engine slowing?

Key data to move markets today

EU: German Industrial Production

UK: BoE Financial Stability Report and a speech by BoE External Member Catherine Mann

USA: ADP Employment Change 4-week Average

Global Macro Updates

US service sector expansion moves at a slower pace as costs cool. The Institute for Supply Management’s services index fell to 54.0 in June from 54.5 in May. A reading above 50 indicates growth in the services sector, which accounts for more than two-thirds of US economic activity.

New orders received by services businesses were down, dropping to 55.1 after surging to 57.3 in May. However, the prices paid index cooled, dropping to 67.7, which was 3.6 percentage points below May's 71.3 percent and its first time below 70 percent since February. The index has exceeded 60 percent for 19 straight months, maintaining its 12-month average of 68 percent. Although a welcome decline, this still high number underlines that inflation may remain elevated even if oil prices drop. Survey respondents suggested that tariff impacts are continuing to be a theme for increased price pressures. Inflation may also be attributable to businesses investing heavily in AI, which is driving up the prices of semiconductors and other technology.

The employment index rose by the most since 2024, coming in at 51.2 percent, a 3.3-percentage point increase from the 47.9 percent recorded in May and indicating higher headcount for the first time since February. The Inventories Index for June came in at 51.2 percent, down 11.3 percentage points from May's 62.5 percent. The Inventory Sentiment Index expanded for the 38th consecutive month, coming in at 52.6 percent, down 2.6 percentage points from May's 55.2 percent. Additionally, the Backlog of Orders Index remained in expansion territory for a fifth straight month, increasing 3.6 percentage points to 54.9 percent in June from May's 51.3. Tariff impacts continued to be a theme for increased pricing pressure. As noted by ISM, the Inventories Index dropped to its second-lowest level since October 2025, indicating that the buy-ahead phenomenon may be over. The Imports Index dropped into contraction territory for the first time in five months, down 49.4 percent in June, a decrease of 1.7 percentage points compared to its May reading of 51.1 percent.

Final June S&P Global Services PMI largely in line with the flash reading, coming in at 51.9 in June, from 51.5 in May.

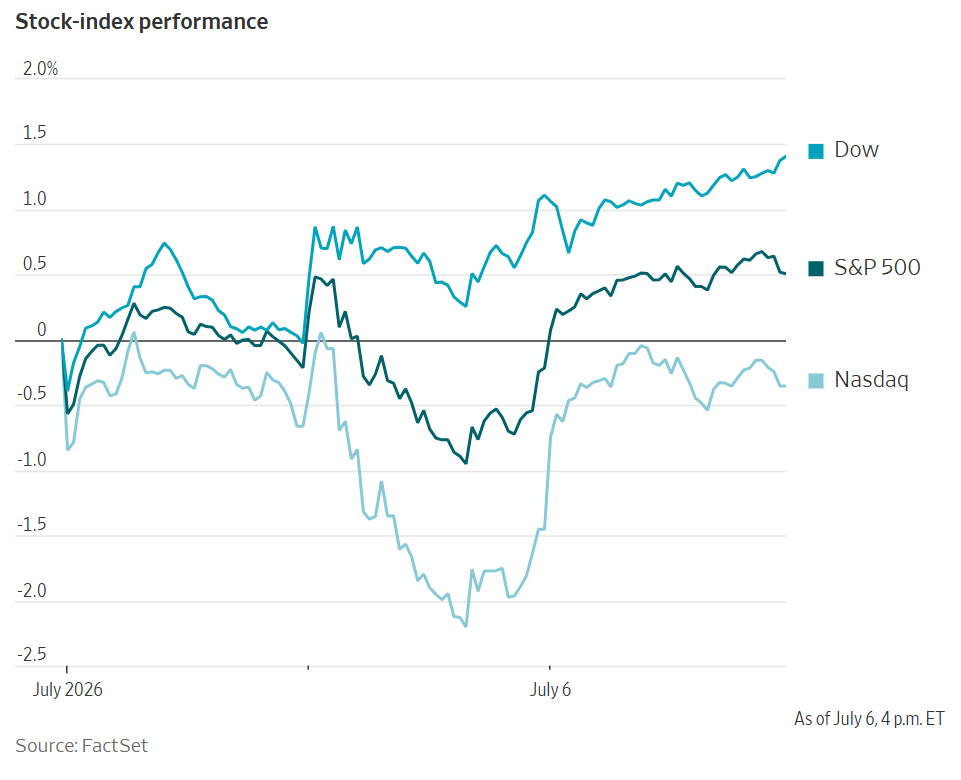

US Stock Indices

Dow Jones Industrial Average +1.12%

Nasdaq 100 +1.26%

S&P 500 +0.72%, with 5 of the 11 sectors of the S&P 500 up

The Dow closed at another record high on Monday, while tech stocks rose as traders brushed off their uncertainty over AI. The Nasdaq composite took the lead, gaining +1.12%, or 288.49 points, to 26,121.16. The Dow Jones Industrials edged up +0.29%, or 155.84 points, to 53,056, its 21st record close of the year. The S&P 500 was +0.72%, or 54.19 points, to 7,537.43.

In corporate news, Lockheed Martin agreed to buy naval defence business Ultra Maritime, which focuses on submarine detection systems, for $3.45 billion.

Microsoft announced that it would cut 4,800 jobs, or about 2.1% of its global workforce and divest up to five studies over the next year as part of a massive reorganisation of its struggling Xbox gaming business. The restructuring of its gaming division will involve 3,200 job cuts, including laying off 1,600 employees as of Monday.

In a deal that would rank just behind last month’s SpaceX IPO, South Korean chipmaker SK Hynix launched a US share sale on Monday to raise 43 trillion won (approximately $28.07 bn). In a filing on Monday, the company said it would sell 17.79 million new shares through ADRs on the Nasdaq; 10 ADRs will represent one common share. The company gave a reference price of 242,500 won per ADR, based on its closing price in South Korea. SK Hynix is a key supplier of high-bandwidth memory chips used in AI systems, with key customers including Nvidia and Alphabet's Google. However, in a signal that investor concerns about returns on massive AI investments, South Korea’s other big chipmaker, Samsung Electronics, shares tumbled as much as 10% in early Asia trade today, despite the company forecasting operating profit of Won 89.4 tn ($58.4 bn) for the second quarter, up 19-fold from a year ago.

Honeywell International’s spinoff Solstice Advanced Materials will acquire Element Solutions in a cash-and-stock deal valued at about $14.5 billion, creating a market leader in the specialty chemicals sector.

European Stock Indices

CAC 40 -0.33%

DAX +0.15%

FTSE 100 -0.26%

Commodities

Gold spot -0.26% to $4,164.09 an ounce

Silver spot -0.40% to $62.15 an ounce

West Texas Intermediate -0.26% to $68.60 a barrel

Brent crude -1.56% to $70.82 a barrel

Gold prices eased from two-week highs on Monday, with spot gold falling -0.26% to $4,164.09 per ounce after earlier reaching its strongest level since 22 June.

Silver also moved lower, declining -0.40% to $62.15 per ounce after briefly touching its highest level since 23 June.

Oil prices settled near levels seen before the Iran war, pressured by Saudi Arabia’s sharp reduction in official selling prices, OPEC+ approval of another production-target increase beginning in August and further recovery in exports through the Strait of Hormuz.

Brent crude futures settled at $70.82 per barrel, down $1.12, or -1.56%. WTI crude futures ended at $68.60 per barrel, down $0.18, or -0.26%.

OPEC-7 raised its combined output quotas for August by 188,000 bpd. The seven core OPEC+ members have increased their output quotas by nearly 800,000 bpd from April through July.

Saudi Arabia set the August official selling price for its flagship Arab Light crude to Asia at $1.50 per barrel below the Oman/Dubai average, marking the largest reduction in more than two decades.

Iran’s ambassador to Beijing said China and other friendly nations would receive special considerations as Tehran determines the level and nature of service fees charged to ships using the Strait of Hormuz, according to Bloomberg news.

Reuters also reported that Iran has begun discussions with Japanese companies regarding potential oil sales, although prospective buyers are seeking longer waivers and additional assurances.

Geopolitical risks remained in focus after Ukraine launched an overnight drone attack on St Petersburg and the surrounding region, striking the city’s oil terminal and broader port infrastructure. Separately, Ukraine’s military said on Monday that it had struck Russia’s largest oil refinery in Omsk, along with facilities in the Yaroslavl and Leningrad regions overnight.

The United Arab Emirates increased crude production to near-record levels above 3.8 million bpd in June following its decision to exit OPEC, according to Reuters.

Shipping groups Maersk and Hapag-Lloyd are set to resume some sailings through the Suez Canal, a route that accounts for roughly ten percent of global trade. Many shippers had abandoned the Asia-Europe corridor after attacks in the Red Sea by Yemen’s Houthis during the Gaza war. A Hapag-Lloyd spokesperson said returning to the route would shorten voyage times by approximately four weeks.

Note: As of 4 pm EDT 6 July 2026

Currencies

EUR +0.09% to $1.1445

GBP +0.27% to $1.3387

Bitcoin +2.36% to $64,444.68

Ethereum +2.86% to $1,812.90

The Japanese yen remained under pressure and near four-decade lows on Monday, increasing concerns about possible official intervention.

The yen traded -0.45% lower at ¥162.09 per dollar, close to last week’s low of ¥162.84, its weakest level since 1986. Traders remained cautious after a sudden wave of buying briefly lifted the currency on Thursday.

Investors are now awaiting Wednesday’s release of the minutes from the FOMC meeting held on 16 – 17 June for further insight into the interest-rate outlook.

The dollar index reached a 13-month high last week but has since retreated as expectations for a Fed rate increase at the 28 - 29 July meeting have faded. The index was trading -0.03% lower at 100.84.

The euro traded at $1.1445, up +0.09% and close to two-week highs, while sterling rose +0.27% to $1.3387.

Fixed Income

US 10-year Treasury -1.5 basis points to 4.475%

German 10-year Bund +1.3 basis points to 2.953%

UK 10-year Gilt +1.6 basis points to 4.803%

The US yield curve bull-steepened on Monday as Treasury yields declined, led by the front end of the curve.

The two-year yield, which is highly sensitive to Fed rate expectations, fell -6.1 bps to 4.120%, while the 10-year yield declined -1.5 bps to 4.475%.

The US Treasury auctioned three-month and six-month bills on Monday. It is also scheduled to sell a $58 billion three-year note today, a $39 billion 10-year note tomorrow and $22 billion of 30-year bonds on Thursday.

Market participants will be looking to the release of June’s FOMC minutes on Wednesday for further clues on the trajectory of interest rates under new Chair Kevin Warsh. However, analysts expect Warsh to limit any statements as to future interest rate moves. However, on Monday, Fed Governor Christopher Waller defended the use of forward guidance by the Fed, saying it can be a ‘valuable tool’ under the right circumstances.

Eurozone bond yields moved higher on Monday, with German benchmarks rising to their highest levels since late June.

Germany’s 10-year yield ended the day +1.3 bps higher at 2.953%, its highest level since 23 June.

Germany’s cabinet was expected to approve the first draft of the 2027 budget on Monday, with total borrowing of €203.6 billion, up from the €196.5 billion indicated in April.

Markets now view one additional 25-bp ECB rate increase this year as likely, if not certain, following last month’s move. However, expectations for a third increase have diminished, particularly after last week’s softer-than-expected inflation data.

That development has kept short-dated yields contained. Germany’s two-year yield stood at 2.554% on Monday, up +0.1 bps on the day.

Other eurozone yields underperformed Bunds. Italy’s 10-year BTP yield rose +5.4 bps to 3.722%, while France’s 10-year OAT yield edged -0.1 bps lower to 3.621%.

Note: As of 4 pm EDT 6 July 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

Tento článek je poskytován pouze pro informační účely a neměl by být považován za nabídku nebo výzvu k nákupu nebo prodeji jakýchkoli investic nebo souvisejících služeb, jejichž odkazy se v něm můžou vyskytovat. Obchodování s finančními nástroji je spojeno se značným rizikem ztráty a nemusí být vhodné pro všechny investory. Dřívější produktivita není spolehlivým ukazatelem budoucí produktivity.

Přihlásit se k odběru přehledů trhu

Přihlásit se k odběru

přehledů

trhu

Předplaťte si nyní

Založeno profesionály. Pro profesionály.