Is private credit the proverbial canary?

Key data to move markets today

EU: Spanish Harmonised Index of Consumer Prices and Eurozone Industrial Production

UK: GDP, Manufacturing Production, and Consumer Inflation Expectations

US: Core Personal Expenditure Price Index, GDP, Core Personal Consumption Expenditures, Personal Income, Personal Spending, Durable Goods Orders, Nondefence Capital Goods Orders, Michigan Consumer Expectations Index, Michigan Consumer Sentiment Index, JOLTS Job Openings, and University of Michigan 1-year and 5-year Consumer Inflation Expectations

Global Macro Updates

Private credit turbulence. Concerns regarding private credit have resurfaced, following a report from the Financial Times which reveals that JPMorgan Chase has reduced the valuation of certain loans within the portfolios of private credit groups. As a result of this change, the amount of credit available to these entities has been restricted.

The report clarifies that this change in valuation does not trigger margin calls. Rather, it represents a proactive measure to restrict credit availability, and is considered to be more conservative than the approach adopted by other institutions. This move is widely interpreted as an indication of increased caution among traditional banks, particularly in relation to loans issued to software companies deemed vulnerable to disruption from AI.

These developments coincide with news that Cliffwater, a prominent private credit firm, has recently faced redemption requests exceeding 7% from its flagship fund, according to Bloomberg news. This follows similar pressure from investors on funds managed by BlackRock, Blackstone, and Blue Owl.

In an effort to enhance transparency regarding the valuation of private credit portfolios, Apollo has announced its intention to begin reporting the net asset value (NAV) of its credit funds on a monthly basis, with the aim of progressing towards daily NAV disclosures and incorporating third-party valuations in the future, as reported by Bloomberg news. Some analysts anticipate that additional funds will adopt similar practices, which could help alleviate redemption requests by providing greater clarity.

Although private credit concerns had recently been overshadowed by geopolitical developments involving Iran, UBS analysts in late February forecasted a significant increase in private credit default rates, potentially rising to 15%, as a consequence of rapid and profound disruption caused by AI.

Trump’s attempts at tariff justifications round two? In a late filing on Thursday US Trade Representative Jamieson Greer’s office said it would begin a probe under Section 301 of the Trade Act focussed on whether 60 trading partners, including the UK, the EU and Canada had adequate rules against importing goods made with forced labour. Greer said the investigations would also determine “how the failure to eradicate these abhorrent practices impacts US workers and businesses.” If any of these countries are found to have done this, it would allow the Trump administration to impose fresh tariffs. This followed Wednesday’s announced probe into more than a dozen major economies including China, the European Union, Mexico, India, Japan, South Korea, Taiwan, Switzerland, Norway and Vietnam under Section 301 of the Trade Act focussed on alleged excess capacity and production in manufacturing sectors. As noted by the Financial Times, taken together, the trade actions could help the Trump administration raise duties back to the level they were at before the US’s top court ruled the president could not use emergency powers to impose tariffs.

Fog of war increases risk premia as Iran attempts to reassert deterrence. In his first statement since assuming the role of Supreme Leader, Mojtaba Khamenei asserted that the Strait of Hormuz should remain closed and employed as leverage against adversaries. He further called for the immediate closure of all United States military bases in the region, warning that those remaining would face attacks. He did not give the statement himself; it was read out on Iranian state TV. There are numerous reports that Khamenei was severely wounded in the strike that killed his father, the previous Supreme Leader.

The statement said that studies are underway to potentially open new fronts in the conflict, without specifying locations. According to The New York Times, some Western officials have raised concerns that Iran may activate sleeper cells within Europe.

In an interview with CNBC, US Energy Secretary Wright stated that the US Navy is not yet prepared to escort oil tankers through the Strait of Hormuz, although such operations are expected to commence in the near future. Secretary Wright added that the Iranian campaign is projected to last weeks rather than months, echoing recent statements from President Trump and other administration officials regarding a shorter timeline for the conflict.

A series of attacks on ships in the Middle East was a central focus on Thursday morning. Six vessels in total were targeted in the Gulf, including two oil tankers off the coast of Iraq. These incidents prompted Iraqi authorities to suspend all oil terminal operations. India is reportedly engaged in negotiations with Iran to secure safe passage for more than 20 tankers through the Strait of Hormuz. Since 28th February, Iran has exported approximately 14 million barrels of oil.

US officials disclosed to NBC news that the threat posed by Iranian drones and other weaponry remains too significant to permit US naval escorts at present. The report also noted that the White House believes it has until the end of March before escalating petrol prices become a critical political issue. Additionally, intelligence assessments have cast doubt on the ability of Kurdish militias to sustain prolonged resistance against Iranian security services, due to insufficient firepower and manpower.

US Stock Indices

Dow Jones Industrial Average -1.56%

Nasdaq 100 -1.73%

S&P 500 -1.52%, with 8 of the 11 sectors of the S&P 500 down

The Dow Jones Industrial Average concluded Thursday at its lowest point of the year. The Dow declined by -1.56% to 47,677.85 points, marking its lowest closing level since 1st December. Meanwhile, the S&P 500 fell -1.52%, while the Nasdaq Composite declined by -1.78%.

In corporate news, Atlassian, the software company behind Jira and Trello, announced plans to reduce its workforce by approximately 10% in order to increase investments in AI.

GlobalFoundries initiated a secondary offering of 20 million shares and announced a share buyback valued at approximately $300 million.

Honda projected a potential impact of up to $15.7 billion resulting from a review of its EV strategy and anticipates posting a net loss for the fiscal year.

Firefly Aerospace successfully completed the launch of its Alpha Flight 7 mission.

Blue Owl Capital defended its recent $1.4 billion loan sale from three of its funds, stating that the transaction included neither backstops nor hidden incentives. The asset manager continues to be a focal point for those anticipating a reckoning in the private credit market.

Tesla has obtained government approval to convert its investment in Elon Musk’s xAI into a minority stake in SpaceX ahead of the rocket company’s anticipated IPO.

S&P 500 Best performing sector

Energy +0.98%, with Occidental Petroleum +5.09%, ConocoPhillips +2.76%, and Phillips 66 +2.71%

S&P 500 Worst performing sector

Industrials -2.52%, with Southwest Airlines -7.34%, Old Dominion Freight Line -6.64%, and United Rentals -5.99%

Mega Caps

Alphabet -1.69%, Amazon -1.47%, Apple -1.94%, Meta Platforms -2.55%, Microsoft -0.75%, Nvidia -1.54%, and Tesla -3.14%

Information Technology

Best performer: HP +2.65%

Worst performer: GoDaddy -6.69%

Materials and Mining

Best performer: Celanese +14.75%

Worst performer: International Paper Company -7.79%

European Stock Indices

CAC 40 -0.71%

DAX -0.21%

FTSE 100 -0.47%

Commodities

Gold spot -1.87% to $5,078.89 an ounce

Silver spot -2.66% to $83.50 an ounce

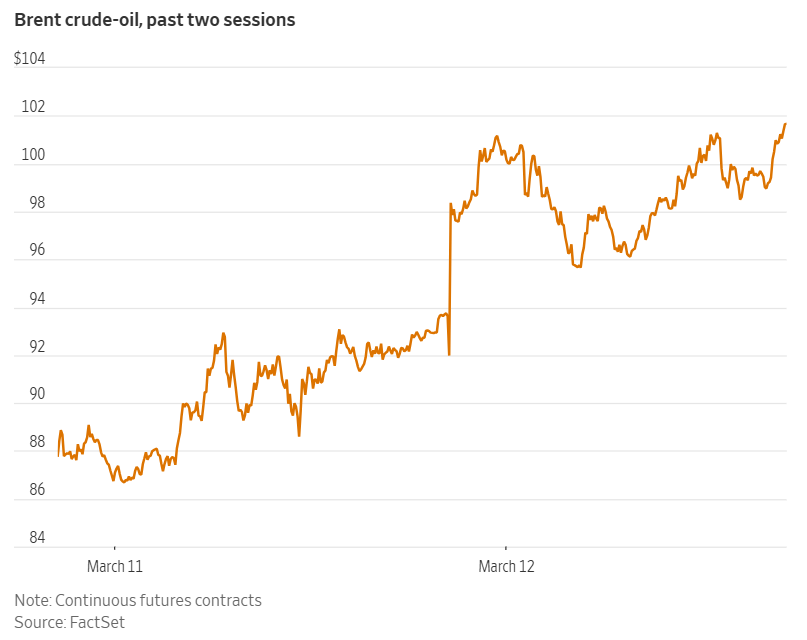

West Texas Intermediate +6.10% to $96.39 a barrel

Brent crude +8.67% to $101.75 a barrel

Gold prices declined by more than one percent on Thursday, weighed down by the strength of the US dollar. Spot gold fell -1.87%, reaching $5,078.89 per ounce.

Spot silver also retreated, dropping -2.66% to $83.50 per ounce.

Chile’s Central Bank boosts gold reserves for the first time in over two decades. Chile’s Central Bank has undertaken its first significant gold purchase since at least 2000, incorporating a ‘limited portion of gold’ into its reserves to enhance risk diversification amid increasingly frequent and complex episodes of external uncertainty, the institution announced on Thursday.

In February, the bank increased its gold holdings to $1.108 billion, a substantial rise from $42 million in January, bringing gold to 2.2% of its total reserves.

Central Bank documents confirm that this is the first gold acquisition in over two decades. ‘The most recent assessment identified changes in the correlations among eligible assets, so adding a limited portion of gold aids in improving the portfolio’s risk diversification,’ the bank stated to Reuters.

According to the Central Bank, this decision resulted from periodic technical evaluations aimed at determining the optimal composition of currencies and instruments within the reserves.

The strategic role of gold as a safe-haven asset, the bank emphasised, “enhances portfolio protection against scenarios of financial stress, especially in a context where episodes of external uncertainty have become more frequent and complex.”

Oil prices rose more than five percent on Thursday, reaching their highest levels in nearly four years due to escalating attacks by Iran on oil and transport infrastructure throughout the Middle East. The nation's supreme leader asserted his intention to maintain the closure of the strategic Strait of Hormuz, a critical chokepoint for global oil shipments.

Brent crude futures closed up $8.12 or +8.67% to $101.75 per barrel. WTI settled at $96.39, up $5.54, or +6.10%. Both benchmarks ended at their strongest levels since August 2022.

Iraqi security sources reported that two fuel tankers operating in Iraqi waters were struck by Iranian boats equipped with explosives. As a result, an Iraqi official confirmed to state media that all operations at the country's oil ports have been entirely suspended.

In a precautionary move, Oman relocated all vessels from its primary oil export terminal at Mina Al Fahal, situated just outside the Strait of Hormuz.

In response to surging energy prices, the Trump administration is considering a temporary waiver of the century-old Jones Act. This measure aims to facilitate the unrestricted movement of energy and agricultural goods between US ports, according to White House Press Secretary Karoline Leavitt.

The International Energy Agency (IEA) described the conflict as causing the most significant disruption to oil supplies in the history of global markets. This statement came a day after the IEA authorised the release of a record 400 million barrels from strategic reserves.

Despite the announcement, market participants remain skeptical regarding the actual volume that will be released, as a detailed allocation has not yet been disclosed. Current inventories, consisting primarily of crude and some refined products, are only sufficient to cover approximately 25 days of the ongoing supply interruption. China has imposed an immediate ban on exports of refined petroleum products for March, a preemptive measure aimed at averting possible domestic shortages stemming from the ongoing turmoil in the Middle East.

According to the IEA's latest monthly oil market report, Gulf nations in the Middle East have collectively reduced oil output by at least 10 million barrels per day, which represents nearly 10% of global demand.

On the geopolitical front, Lebanon's Hezbollah launched the largest rocket attack of the current conflict on Wednesday, provoking Israeli airstrikes that reverberated in Beirut. This escalation heightened concerns about the potential involvement of Yemen's Houthi forces alongside Iran, which could further impede Red Sea shipping routes.

Amid these developments, Saudi Arabia has increased crude exports from its Red Sea port of Yanbu.

Note: As of 4 pm EDT 12 March 2026

Currencies

EUR -0.54% to $1.1511

GBP -0.45% to $1.3347

Bitcoin -0.62% to $70,325.60

Ethereum -0.51% to $2,063.03

The US dollar strengthened on Thursday with the dollar index climbing to its highest point since November, rising +0.50% to 99.74 in afternoon trading.

The euro hovered near its lowest level since November, falling -0.54% to $1.1511. The British pound also fell, down -0.45% to $1.3347.

The Japanese yen remained at values that heightened the risk of potential intervention by Japanese authorities. The yen depreciated by -0.30% to ¥159.33 per dollar after briefly reaching 159.43, its weakest level since 14th January.

Fixed Income

US 10-year Bond +3.8 basis points to 4.269%

German 10-year +2.1 basis points to 2.961%

UK 10-year gilt +8.6 basis points to 4.713%

On Thursday, two-year Treasury yields reached their highest level in six months, driven by escalating Iranian attacks on energy and transportation infrastructure in the Gulf region. These developments have intensified concerns over renewed inflationary pressures, raising expectations that US interest rates may remain elevated for an extended period.

The yield on the two-year Treasury note, closely aligned with market expectations for Fed policy, rose +8.4 bps to 3.745%. This marks the highest closing level since 22nd August and represents the most significant single-day increase since June.

The yield on the 10-year US Treasury note advanced +3.8 bps to 4.269%, the highest point observed since 5th February. The 30-year Treasury yield remained unchanged at 4.885%.

The spread between two-year and 10-year Treasury yields narrowed by 4.6 bps to 52.4 bps. Earlier in the session, the curve had flattened to 49.4 bps, the narrowest since 28th November. US Treasuries exhibited minimal reaction to Thursday’s economic data, which indicated a decrease in the number of Americans filing initial claims for unemployment benefits last week.

The Treasury Department observed robust demand during Thursday’s $22 billion auction of 30-year bonds, ending a cumulative $119 billion issuance of coupon-bearing securities for the week. The bonds were sold at a high yield of 4.871%, which was 1.0 bps below pre-auction levels, and featured a bid-to-cover ratio of 2.45x.

In contrast, the government experienced subdued demand for a $58 billion auction of three-year notes on Tuesday and a $39 billion sale of 10-year notes on Wednesday.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing in 17.5 bps of cuts in 2026, lower than the 42.3 bps priced in the previous week. Fed funds futures traders are now pricing in a 0.9% probability of a 25 bps rate cut at the 18th March FOMC meeting, down from 3.5% a week ago.

On Thursday, German government bond yields remained near their multi-year highs as markets increased their expectations for additional rate hikes by the ECB.

The yield on Germany’s 10-year government bond rose +2.1 bps to 2.961%, after briefly reaching 2.963%, marking its highest level since October 2023. The 2-year Schatz rose +4.8 bps to 2.425%, and the 30-year German bund advanced +2.4 bps to 3.518%.

Money markets have now fully priced in an ECB rate hike by July, with a second increase widely anticipated by December. In late February, prior to the onset of the war, traders had assigned approximately a 40% probability to an ECB rate cut before year-end.

Economists largely discount the likelihood of any policy change at next week’s meeting, contending that the Strait of Hormuz would need to remain closed for several months before the ECB would consider monetary tightening.

ECB board member Isabel Schnabel noted that the surge in inflation following the pandemic has left a lasting impact on businesses and consumers, who now recognisze that prices can rise rapidly and settle at higher levels. She emphasiszed that the ECB stands ready to act swiftly should inflationary pressures appear likely to become entrenched.

Italy’s 10-year BTP yield increased +8.8 bps, reaching 3.751%. The yield spread between Italian government bonds and Bunds widened by 6.7 bps to 79.0 bps.

The French spread versus Bunds reached 67.1 bps, following a +6.4 bps increase in the French OAT 10-year yield.

Note: As of 4 pm EDT 12 March 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

本文提供給您僅供資訊參考之用,不應被視為認購或銷售此處提及任何投資或相關服務的優惠招攬或遊說。金融商品交易涉及重大損失風險,可能不適合所有投資者。過往績效不代表未來表現。

由專業人士建立。為專業人士打造。