What are the tail-risks beneath the surface?

Corporate Earnings News

Companies reporting on Monday, 9th March: HP, Oracle

Key data to move markets today

EU: German Factory Orders and Industrial Production, Eurozone Sentix Investor Confidence, Eurogroup meeting, and a speech by ECB Executive Board member Frank Elderson

JAPAN: GDP

Global Macro Updates

Tail risks rising: rethinking Gulf energy market security. The prevailing consensus across oil derivatives markets is that the current disruption to Persian Gulf energy flows is logistical, not structural. That view, while data-supported, may be dangerously complacent.

As of Friday, as noted by Reuters, the Brent futures curve pointed to acute but temporary supply tightness. The front-month to six-month spread had widened to roughly $10, the steepest backwardation since 2022, while 30-day Brent implied volatility surged 17.5 percentage points to 68%, even as the 60- and 90-day tenors rose a more modest 5.9 and 2.8 points, respectively. The 2027 Brent strip was trading below $70 per barrel, and producers used the rally to hedge forward production, introducing natural selling pressure into longer-dated volatility. In short, risk premiums are concentrated at the front of the curve. The market is pricing a sprint, not a marathon.

But since Friday the situation has escalated materially. Qatar's Energy Minister warned that a couple more weeks of Strait of Hormuz closure could push crude toward $150 per barrel, coupled with Kuwait's forced production cuts on exhausted storage and Iraq's 1.5 million barrels per day (bpd) shut-in. Over 350 tankers remain anchored outside the Strait, and even after the US International Development Finance Corporation announced a $20 billion maritime reinsurance plan, traders remain skeptical that vessels will transit until the Iranian drone and missile threat subsides. If the front of the curve reprices further, or the disruption begins to look structural, the consequences will radiate well beyond energy. As reported by Reuters, Citigroup has warned that a prolonged shock could aggressively de-anchor inflation expectations in Emerging markets (EM), with low-reserve economies like Argentina, Sri Lanka, and Turkey facing heightened capital flight risk. Middle Eastern dollar-denominated bonds from Qatar, Oman, and Saudi Arabia have also come under pressure, with risk-off sentiment spilling into Egyptian and Turkish sovereign debt. However, the 32 members of the IEA hold strategic reserves as part of a collective emergency system designed for oil price crises and, according to the Financial Times, G7 finance ministers will discuss a possible joint release of these petroleum from reserves co-ordinated by the International Energy Agency, in an emergency meeting on Monday. The overall disruption underlines the importance of energy security and how closely it is tied to national security.

Critically, even if the market is correct that the disruption is logistical rather than structural, the operational realities of shutting in production introduce a non-linear risk the futures curve may be underweighting. Oil wells cannot simply be toggled on and off. When production is halted, whether due to storage exhaustion or drone threats, wellbore fluids separate, gas pressure forces liquids back into producing formations, and organic precipitates and emulsions begin forming, particularly in wells with depleted reservoir pressure. If multiple Gulf producers attempt simultaneous restarts, competition for rigs and crews could extend recovery further, as it did through the 2020 COVID shut-in cycle.

The damage cascades beyond crude. Qatar's force majeure on LNG, accounting for roughly one fifth of global supply, triggered a 70% surge in European gas and a near 40% spike in Asian LNG. Even under the most optimistic scenario, according to Reuters, Qatari liquefaction needs at least a month to reach full capacity once restarted. Downstream, the disruption is metastasising into petrochemicals: Asia imports roughly four million tonnes of naphtha monthly from the Middle East, and with that flow severed, steam crackers in South Korea, China, and Indonesia have already declared force majeure or begun cutting run rates, rippling through the entire olefins-to-polymers value chain.

Beneath the energy headlines lies a vulnerability the market has yet to price at all. As Bloomberg news' Javier Blas detailed, roughly 100 million people across GCC nations depend on nearly 450 desalination plants for drinking water, facilities powered by the very infrastructure now under attack. A declassified CIA assessment flagged water as the region's true ‘strategic commodity’ decades ago, and a leaked US Embassy cable warned that Riyadh would need to evacuate within a week if the Jubail desalination plant were seriously damaged. Iran has already struck UAE power infrastructure supporting desalination, and several Iranian officials have issued explicit warnings about targeting water facilities. While such an attack would constitute a massive escalation, Tehran (outmatched militarily) has demonstrated a willingness to pursue soft civilian targets, from Saudi refineries to the Fujairah storage terminal, as part of a strategy to impose asymmetric economic pain. Any disruption to desalination operations would be unmanageable via the derivatives markets, constituting a humanitarian crisis with the potential to halt the region's economic activities altogether. Such an event would amplify risk-off capital flows into safe havens, while prompting a withdrawal from all asset classes linked to Gulf exposure.

There are also other risks such as the rising cost of fertiliser, to consider and the impact this will have on global food prices. The Middle East is a key supplier of fertiliser, exporting some 45 per cent of global supply and the price of urea, a key source of nitrogen used in agriculture, has surged by over 25%. As noted by Reuters, shipments from the Middle East are likely to drop not only because transit through the Strait of Hormuz has all but stopped, but also due to cuts in production. It comes at a particularly critical time as farmers in the northern hemisphere are now heading into planting season. The futures curve may be pricing a logistical crisis, but the range of tail risks, from prolonged Strait closure to infrastructure targeting to cascading shut-ins that take months to reverse, suggests the market's confidence in a quick resolution deserves more scrutiny than it is getting.

February NFP report. February's nonfarm payrolls fell by 92,000, below the consensus forecast of 55,000 – 60,000 and January's revised figure of 126,000 (previously reported as 130,000). December was also revised into negative territory, resulting in a total two-month downward adjustment of 69,000. The average job growth over the past three months now stands at just 17,000. The unemployment rate increased to 4.4%, compared to expectations for a steady 4.3%. Meanwhile, average hourly earnings rose by 0.4%, defying predictions of a decrease to 0.3%.

Analysts noted that the report contained several complicating factors, making it difficult to draw a clear signal about the state of the labour market. A moderation had been anticipated following January's robust figures. Healthcare was expected to be weak due to strike activity, and its influence is considered to be a one-off factor, likely to reverse next month.

Additional areas of weakness were also identified. Weather was acknowledged as a significant factor impacting certain sectors, particularly construction and leisure/hospitality.

Focus remained on the unemployment rate, given its importance to Fed policymakers. The labour-force participation rate edged down to a cycle low of 62.0%, though this decrease was less pronounced due to annual population adjustments included in the report. The release clarified that the unemployment rate itself was not affected by these adjustments.

US Stock Indices

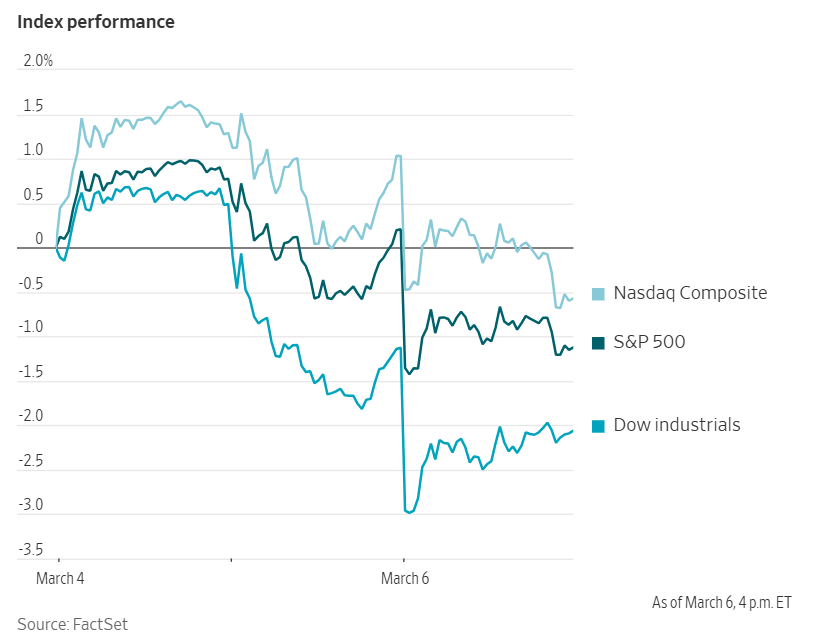

Dow Jones Industrial Average -0.95%

Nasdaq 100 -1.51%

S&P 500 -1.33%, with 9 of the 11 sectors of the S&P 500 down

Oil prices continued their relentless rise amid the escalating military conflict in the Middle East, surpassing $90 and registering their largest weekly gain on record. By Monday morning trading in Asia, as noted by Bloomberg news, Brent was 15% higher at around $106 a barrel, but much lower than the session peak of $119.50. West Texas Intermediate was near $102.

On Friday, investor concerns regarding the Iran conflict intensified, resulting in notable declines across major US equity indices. The Dow Jones Industrial Average fell by 453 points or -0.94%, and closed the week -2.87%; its sharpest drop since April. The S&P 500 declined -1.33%, down -2.06% on the week. The Nasdaq Composite slipped -1.59% on Friday, down -1.59% for the week.

According to LSEG I/B/E/S data, y/o/y earnings growth for the S&P 500 in Q4 is projected to be +14.1%. This jumps to +14.6% when excluding the Energy sector. Of the 491 companies in the S&P 500 that have reported earnings to date for Q4 2025, 72.7% have reported earnings above analyst estimates, with 72.6% of companies reporting revenues exceeding analyst expectations. The y/o/y revenue growth is projected to be 9.2% in Q4, increasing to 10.0% when excluding the Energy sector.

Information Technology at 91.4%, is the sector with most companies reporting above estimates. Additionally, Energy and Information Technology, both with a surprise factor of 7.0%, are the sectors that have beaten earnings expectations by the highest surprise factor. Within Materials, 46.2% of companies have reported below estimates. Utilities is the only sector with a negative surprise factor, falling short of estimates by 2.9%. The S&P 500 surprise factor is 4.8%. The forward four-quarter price-to-earnings ratio (P/E) for the S&P 500 sits at 21.6x.

7 S&P 500 companies are scheduled to release their Q4 earnings reports this week.

In corporate news, BlackRock shares declined after the asset manager imposed restrictions on withdrawals from one of its flagship private credit funds for the first time. The HPS Corporate Lending Fund, a non-traded business development company marketed to individual investors, announced it would not repurchase shares beyond its stated 5% liquidity threshold per quarter, following investor redemption requests exceeding 5% of total shares for the first time. The fund received requests to redeem 9.3% of shares in the most recent quarter, according to a letter sent to investors on Friday.

Bloomberg news reported that Boeing is nearing completion of a 500-aircraft order for 737 Max jets, which is expected to be unveiled during the US President’s forthcoming state visit to Beijing. Negotiations are also ongoing for a widebody aircraft sale, including approximately 100 Boeing 787 Dreamliner and 777X jets, with an announcement anticipated at a later date. This agreement would conclude years of discussions between Boeing and Chinese airlines and mark the end of a prolonged order drought from the world’s second-largest aviation market.

Nike anticipates recording a charge of $300 million related to its cost-reduction initiatives, including workforce reductions. In January, the company announced plans to lay off roughly 775 employees, representing 1% of its workforce.

S&P 500 Best performing sector

Consumer Staples +0.29%, with Kroger +3.55%, Bunge Global +3.07%, and Kraft Heinz +2.98%

S&P 500 Worst performing sector

Consumer Discretionary -1.96%, with Carnival -5.04%, Chipotle Mexican Grill -4.56%, and Ralph Lauren -4.26%

Mega Caps

Alphabet -0.87%, Amazon -2.62%, Apple -1.09%, Meta Platforms -2.38%, Microsoft -0.42%, Nvidia -3.01%, and Tesla -2.17%

Information Technology

Best performer: ServiceNow +3.29%

Worst performer: Teradyne -10.65%

Materials and Mining

Best performer: CF Industries Holdings +4.51%

Worst performer: Celanese -6.15%

European Stock Indices

CAC 40 -0.65%

DAX -0.94%

FTSE 100 -1.24%

Commodities

Gold spot +1.72% to $5,169.92 an ounce

Silver spot +2.50% to $84.33 an ounce

West Texas Intermediate +15.72% to $91.27 a barrel

Brent crude +10.58% to $92.91 a barrel

Gold advanced on Friday following softer US payrolls data, which sustained expectations of a potential Fed rate cut. Spot gold rose +1.72% to reach $5,169.92 per ounce. However, spot gold finished the week down -2.39%, its first weekly decline in five weeks.

The US dollar index posted its strongest weekly increase in more than a year, rising +1.23%. This appreciation in the dollar has rendered dollar-denominated gold more expensive for international buyers, contributing to the decline in gold prices.

Silver climbed +2.50% to $84.33 on Friday, yet ended the week -10.66% lower.

US crude futures surged over ten percent on Friday, driven by disruptions in global oil supplies resulting from the escalating conflict in the Middle East.

Brent crude futures closed at $92.91 per barrel, up $8.89 or +10.58%. WTI settled at $91.27 per barrel, up $12.40 or +15.72%.

During the previous week, WTI advanced by +35.64% and Brent rose by +26.91%, marking the most substantial weekly gains since the COVID pandemic in the spring of 2020.

For the second consecutive day, US crude futures outperformed Brent, as refiners globally sought alternative crude sources to compensate for the shortfall in Middle Eastern supply.

According to Qatar's energy minister, as reported by the Financial Times, all Gulf energy producers may be compelled to halt exports within weeks, a move that could potentially drive oil prices to $150 per barrel.

With the Strait effectively closed for a week, approximately 140 million barrels of oil, equivalent to approximately 1.4 days of global demand, have been prevented from reaching the market.

The conflict has now spread across the principal energy-producing regions of the Middle East, causing widespread disruptions to output and resulting in the shutdown of both refineries and liquefied natural gas facilities.

The prospect of intervention by the US Treasury Department to counter rising energy costs briefly saw prices decline by more than one percent early on Friday.

On Thursday, the Treasury granted 30-day waivers to certain companies, permitting them to purchase sanctioned Russian oil. The initial waivers were issued to Indian refiners, who have procured millions of barrels of Russian crude.

Note: As of 4 pm EST 6 March 2026

Currencies

EUR +0.10% to $1.1619

GBP +0.41% to $1.3411

Bitcoin -4.02% to $68,283.73

Ethereum -4.67% to $1,983.35

The Swiss franc, traditionally regarded as a safe-haven currency, rallied on Friday amid heightened tensions in the Middle East. In contrast, the US dollar experienced declines in what proved to be a volatile trading session.

The dollar fell -0.50% against the Swiss franc, reaching CHF 0.7764. The dollar index declined -0.19% on the day, settling at 98.86. Nonetheless, it posted a weekly gain of +1.23%, marking its strongest advance since mid-November 2024.

The euro recorded a +0.10% increase on Friday, while sterling was +0.41% against the US dollar to reach $1.3411. Over the course of the week, however, the euro declined -1.67%, representing its largest weekly fall since April 2024. Sterling also weakened over the week, falling -0.55%.

In afternoon trading, the dollar edged higher versus the yen, rising +0.14% to ¥157.79. For the week, the greenback advanced +1.11%, marking its third consecutive weekly gain against the yen.

Fixed Income

US 10-year Bond -0.9 basis points to 4.133%

German 10-year +1.6 basis points to 2.861%

UK 10-year gilt +9.2 basis points to 4.573%

US Treasury yields at the short end of the curve declined in volatile trading on Friday, following disappointing payrolls data that strengthened expectations the Fed may accelerate interest rate cuts. The two-year US Treasury yield fell -1.4 bps to 3.577% after touching 3.631%, its highest since 20th November. However, the yield on the 30-year bond edged up +0.5 bps to 4.761%.

The yield on the US 10-year Treasury note slipped -0.9 bps to 4.133%, after reaching a three-week peak of 4.187% earlier in the session.

Global yields surged last week, as the ongoing conflict with Iran has driven oil prices higher and exacerbated fears of inflation, which may prompt the Fed and other central banks to pause monetary easing. According to CME Group's FedWatch Tool, Fed funds futures traders are pricing in 37.8 bps of cuts in 2026, lower than the 61.9 bps priced in the previous week. Fed funds futures traders are now pricing in a 4.5% probability of a 25 bps rate cut at the 18th March FOMC meeting, down from 7.4% a week ago.

Over the week, the yield on the 10-year note increased +18.1 bps, its sharpest weekly rise since early April, while the two-year yield climbed +19.0 bps, also marking its largest weekly gain since early April. The 30-year yield advanced +14.3 bps during the week.

The US Treasury yield curve, measured as the spread between two- and 10-year Treasury notes, stood at 55.6 bps, narrowing by 0.9 bps compared to the previous week’s 56.5 bps.

Eurozone bonds experienced their most pronounced weekly selloff in a year on Friday.

Germany’s 10-year government bond yield increased by +1.6 bps on Friday, culminating in a +20.5 bps rise over the week, the largest advance since March 2025.

The yield on the two-year Schatz, sensitive to ECB rate expectations, rose +8.4 bps to 2.234%. It ended the session with a weekly gain of +21.8 bps, the steepest in nearly three years. Conversely, the 30-year bund declined -1.8 bps on Friday to 3.421%, registering a more modest weekly increase of +10.2 bps.

The week’s market movements underscore the unpredictability of traditional safe havens during the current shock, with inflation concerns now overshadowing their typical defensive attributes.

Money markets reflected a 50% probability of an ECB rate hike by July.

Italy’s 10-year government bond yield climbed +7.1 bps in Friday’s afternoon trading and underperformed its European counterparts throughout the week, rising +28.8 bps. The spread against bunds widened to 77.7 bps, an increase of 8.3 bps from the previous week’s 69.4 bps.

France’s 10-year yield advanced +5.6 bps on Friday and ended the week +22.2 bps higher, leaving the spread over bunds 1.7 bps above the preceding week at 67.2 bps. Over the week, the spread between French OATs and Italy’s BTPs widened from 3.9 bps to 10.5 bps.

Note: As of 4 pm EST 6 March 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

本文提供給您僅供資訊參考之用,不應被視為認購或銷售此處提及任何投資或相關服務的優惠招攬或遊說。金融商品交易涉及重大損失風險,可能不適合所有投資者。過往績效不代表未來表現。

由專業人士建立。為專業人士打造。