What is the clearing price for regime change?

Corporate Earnings News

Companies reporting on Monday, 2nd March: Norwegian Cruise Line Holdings, AES

Key data to move markets today

EU: German Retail Sales, HCOB Manufacturing PMIs for Italy, France, Germany and the eurozone, and speeches by ECB President Christine Lagarde, ECB Executive Board member Frank Elderson, and Bundesbank President Joachim Nagel

UK: A speech by BoE Deputy Governor Dave Ramsden

US: S&P Global Manufacturing PMI, ISM Manufacturing PMI, Employment and New Orders Indices, and Prices Paid

JAPAN: Unemployment Rate

Global Macro Updates

US-Iran conflict. The events unfolding in the Middle East over the weekend mark a substantial escalation in geopolitical risk, with the focus squarely on Iran, Israel, and the United States. The most pivotal development was the death of Iran’s Supreme Leader, Ayatollah Ali Khamenei, alongside several senior security figures. In response, an interim leadership structure was rapidly established; however, real operational authority has largely remained with the Islamic Revolutionary Guard Corps, underscoring the regime’s institutional continuity rather than any indication of collapse.

In the wake of these events, Iran issued formal notices regarding vessel interdiction and threatened to close the Strait of Hormuz — a critical maritime chokepoint through which approximately one-fifth of the world’s seaborne oil and a significant share of LNG transit. Although Iran’s Foreign Minister has since clarified that there is no intention to close the Strait, and it remains technically open, commercial shipping has nonetheless ground to a halt. This is chiefly due to insurance underwriters withdrawing war-risk coverage, making the insurance market, rather than military action, the primary barrier to resumed oil flows. Restoring normal operations will thus require the reinstatement of insurance coverage, not merely improved physical security.

Financial markets are poised to react through a heightened geopolitical risk premium rather than a fundamental reassessment of global growth. Initially, a pronounced risk-off sentiment is likely to prevail, with expectations of higher oil and gold prices, declining government bond yields in advanced economies, wider credit spreads, and selling pressure on equities. Transmission to markets will primarily occur via the energy, shipping, and logistics sectors. Oil prices are expected to reflect the risk of potential supply disruption rather than actual shortages, with the extent and persistence of elevated prices depending on how swiftly normal shipping resumes. Logistical disruptions are anticipated to persist, with high insurance premiums, rerouted cargoes, and ongoing air traffic interruptions further exacerbating trade and transportation challenges. If a sustained shutdown of energy shipments through the Strait of Hormuz is not averted, a surge in energy prices risks reigniting inflation in developed economies, derailing central bank rate-cutting plans in some countries and negatively affecting business confidence.

These developments introduce a renewed stagflationary impulse to the global economy. Over the next days, developments will focus on four fronts: potential diplomatic engagement between the US and Iran; the reopening of the Hormuz trade corridor dependent on insurance reinstatement; the cohesion of Gulf Cooperation Council unity and response; and the restoration of civilian infrastructure across the Gulf as the clearest signal of either stabilisation or renewed escalation.

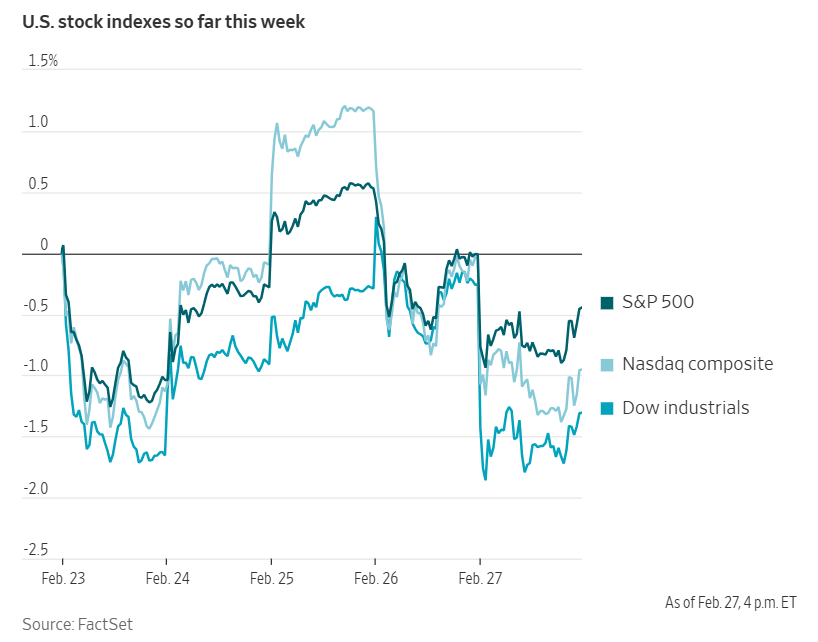

US Stock Indices

Dow Jones Industrial Average -1.05%

Nasdaq 100 -0.30%

S&P 500 -0.43%, with 2 of the 11 sectors of the S&P 500 down

Equity markets declined on the final trading day of February, ending a month characterised by heightened concerns around the impact of AI on the broader market.

The Nasdaq Composite fell -0.92%, resulting in a cumulative monthly loss of -3.38%. The S&P 500 retreated -0.43% on the day and closed February down -0.87%. The Dow Jones Industrial Average declined -1.05% on Friday, equivalent to a loss of 521.28 points, yet managed to eke out a modest monthly gain of +0.17%. The Dow extended its monthly winning streak to ten consecutive months, the longest such run since 2018.

Both the S&P 500 and the Nasdaq registered their weakest monthly performances since the onset of heightened trade tensions last spring. Software and Technology were among the sectors most adversely affected. Financial institutions either invested in or disrupted by the advancement of AI technologies were also badly affected.

According to LSEG I/B/E/S data, y/o/y earnings growth for the S&P 500 in Q4 is projected to be +14.3%. This jumps to +14.7% when excluding the Energy sector. Of the 479 companies in the S&P 500 that have reported earnings to date for Q4 2025, 72.4% have reported earnings above analyst estimates, with 72.7% of companies reporting revenues exceeding analyst expectations. The y/o/y revenue growth is projected to be 9.0% in Q4, increasing to 9.8% when excluding the Energy sector.

Information Technology at 91.0%, is the sector with most companies reporting above estimates. Additionally, with a surprise factor of 7.4%, it is the sector that has beaten earnings expectations by the highest surprise factor. Within Materials, 46.2% of companies have reported below estimates. Industrials is the sector with the lowest surprise factor, exceeding estimates by just 0.1%. The S&P 500 surprise factor is 5.2%. The forward four-quarter price-to-earnings ratio (P/E) for the S&P 500 sits at 21.9x.

14 S&P 500 companies are scheduled to release their Q4 earnings reports this week.

In corporate news, Moody’s Investors Service announced on Friday that it had placed Paramount Global under review for a potential downgrade, following the successful bid by parent company Paramount Skydance to acquire Warner Bros. Discovery. Paramount Global currently holds Moody’s lowest investment grade rating of Baa3; a downgrade would reclassify the firm into speculative grade, or junk status. While the acquisition of Warner Bros. is expected to bolster margins and diversify revenue streams for Paramount Skydance, Moody’s cautioned that it would also significantly increase the company’s leverage and debt complexity.

Lynas Rare Earths CEO, Amanda Lacaze, expressed optimism about finalising a rare-earths supply agreement with the US Department of Defence before her scheduled departure in June. Progress on Lynas’s proposed heavy rare-earths processing facility in Texas remains stalled pending the outcome of these negotiations.

Block announced plans to reduce its workforce by nearly half as part of a broader strategic realignment towards AI. The company, led by Jack Dorsey, concurrently raised its outlook for gross profit.

S&P 500 Best performing sector

Health Care +1.77%, with Molina Healthcare +5.25%, IQVIA Holdings +4.79%, and Centene +4.54%

S&P 500 Worst performing sector

Information Technology -2.17%, with Enphase Energy -7.65%, Zebra Technologies -4.71%, and Nvidia -4.16%

Mega Caps

Alphabet +1.39%, Amazon +1.00%, Apple -3.21%, Meta Platforms -1.34%, Microsoft -2.24%, Nvidia -4.16%, and Tesla -1.49%

Information Technology

Best performer: Dell Technologies +21.93%

Worst performer: Enphase Energy -7.65%

Materials and Mining

Best performer: Dow +3.99%

Worst performer: Albemarle -3.39%

Corporate Earnings Reports

Posted on Friday, 27th February

BASF quarterly revenue -3.3% to €14.032 bn vs €14.147 bn estimate

EPS at €0.00 vs loss per share €0.10 estimate

Markus Kamieth, CEO, said, ‘We therefore mainly focused on the things we can control within the framework of our ‘Winning Ways’ strategy. We successfully started up the major plants at our new Verbund site in Zhanjiang. We also accelerated our cost savings programs and significantly streamlined BASF’s organization. Moreover, we progressed swiftly and successfully with the announced portfolio measures.’ — see report.

Holcim full-year 2025 revenue -30.6% to CHF 15.724 bn vs CHF 15.827 bn estimate

EPS at CHF 0.70 vs CHF 3.28 estimate

Kim Fausing, Chairman, said, ‘2025 was a transformative year for Holcim, as

we began to deliver on our NextGen Growth 2030 strategy as the leading partner for

sustainable construction. I was excited by the launch of our strategy, which aims to unlock significant growth and value creation in the months and years to come. And we started from day one after the successful spin-off of the North American business, generating strong profitable growth for the full year.’ — see report.

International Consolidated Airlines Group quarterly revenue -0.9% to €7.979 bn vs €8.017 bn estimate

EPS at €0.14 vs €0.15 estimate

Luis Gallego, CEO, said, ‘We reported another year of exceptional performance in 2025, delivering for our customers with continued improvements in on-time performance and customer satisfaction. Execution of our strategy and transformation programme is creating value for shareholders, with adjusted EPS growth of 22.4% and, in line with our disciplined capital allocation framework, we have grown the dividend per share by 8.9% and are announcing today a further return of excess cash of €1.5 billion. We are confident as we look to the future, with compelling market dynamics, long-term secular growth and a clear plan to leverage our business model and deliver our strategy.’ — see report.

European Stock Indices

CAC 40 -0.47%

DAX -0.02%

FTSE 100 +0.59%

Commodities

Gold spot +2.17% to $5,296.50 an ounce

Silver spot +6.93% to $94.39 an ounce

West Texas Intermediate +2.78% to $67.29 a barrel

Brent crude +3.24% to $73.21 a barrel

Gold approached a one-month high on Friday, marking its seventh consecutive month of gains due to heightened geopolitical tensions, central bank buying, on expectations of rate cuts, US policy uncertainty, safe-haven demand against currency inflation fears, and investor momentum.

Spot gold was +2.17% to $5,296.50 an ounce, reaching its highest level since 30th January. Over the past week, prices advanced +3.78%, while February saw a monthly gain of +8.88%.

Spot silver increased +6.93% to $94.39 an ounce, contributing to a weekly rise of +11.61%. Silver saw a monthly increase of +11.55%.

On Friday, oil prices climbed by more than two percent, as market participants remained cautious about potential supply disruptions amidst the ongoing stalemate in nuclear negotiations between the US and Iran. Brent crude futures settled at $73.21 per barrel, marking an increase of $2.30, or +3.24%, while US WTI crude concluded at $67.29 per barrel, up $1.82, or +2.78%.

Both the Brent and WTI benchmarks reached their highest trading levels since July and August, respectively, and posted weekly gains of +2.19% and +1.48%. Brent advanced +3.55% and WTI +2.36% in February.

OPEC+ boosts output amid crisis in the Middle East. On Sunday, OPEC+ announced a measured increase in oil production, agreeing to boost output by 206,000 barrels per day (bpd) for April. This decision comes amid significant disruptions to oil flows caused by the ongoing US-Israeli conflict with Iran and subsequent retaliatory actions, which have affected several key members of the producer group in the Middle East.

Historically, OPEC+ has responded to supply disruptions by raising output to stabilise the market. However, analysts note that the group presently has limited spare capacity, with Saudi Arabia and the United Arab Emirates being the only members capable of contributing meaningful additional supply. Even these nations are likely to face difficulties in exporting oil until normal navigation resumes in the Gulf.

Since Saturday, oil, gas, and other shipments traversing the Strait of Hormuz — a crucial passage accounting for over one fifth of global oil transit — have almost entirely ceased. This halt was prompted by Iranian warnings declaring the area closed to navigation. As a result, hundreds of vessels anchored and remained stationary, with reports of several ships coming under attack. Additionally, according to the Financial Times, insurers told ship owners on Saturday they would cancel policies and raise coverage prices for vessels travelling through the Gulf and Strait of Hormuz after the US and Israel attacked Iran.

OPEC+ confirmed its decision to raise production by 206,000 bpd starting in April, following discussions that considered options ranging from 137,000 to 548,000 bpd, according to Reuters. This increase ends a three-month suspension of production hikes, though it constitutes less than 0.2% of global supply.

The Sunday meeting comprised eight OPEC+ members, Saudi Arabia, Russia, the UAE, Kazakhstan, Kuwait, Iraq, Algeria, and Oman. These nations collectively agreed to increase production quotas by approximately 2.9 million bpd from April through December 2025, about three percent of global demand. Furthermore, the group will pause further increases from January to March 2026, reflecting anticipated seasonal demand weakness.

Note: As of 4 pm EST 27 February 2026

Currencies

EUR +0.16% to $1.1816

GBP +0.04% to $1.3485

Bitcoin -2.97% to $65,473.00

Ethereum -5.39% to $1,921.17

The dollar index slipped by -0.15% to 97.65 on Friday. Despite a weekly decrease of -0.14%, the dollar index nonetheless secured a +0.52% gain for February, its first monthly advance since October. In contrast, the euro rose +0.16% to $1.1816. It was +0.31% over the week but retreated by -0.27% during the month.

Sterling edged up by +0.04% against the dollar on Friday to $1.3485. The British pound registered a modest increase of +0.02% for the week; however, it ended a three-month streak of gains with a -1.48% decline in February.

Against the Japanese yen, the dollar eased by -0.04% on Friday yet finished the week +0.65% higher at ¥156.06. Over the course of February, the US currency advanced by +0.84% versus the yen.

Fixed Income

US 10-year Bond -5.6 basis points to 3.952%

German 10-year -4.4 basis points to 2.656%

UK 10-year gilt -4.2 basis points to 4.234%

US Treasuries advanced on Friday, underpinned by robust safe-haven demand as investors remained cautious amid escalating geopolitical tensions in the Middle East.

Yields across the curve reached notable lows. The 10-year yield slipped below 4.0% for the first time since late November, while the five-year yield fell to its lowest level since mid-October, and the seven-year yield reached a four-month low.

By the afternoon, the 10-year yield had declined -5.6 bps to 3.952%, following its lowest point since late November. This contributed to a weekly fall of -13.9 bps, while the monthly drop of -28.6 bps in February marked the steepest monthly decline in a year.

Long-dated yields fell, with the 30-year Treasury yield descending to a four-month low, down -8.3 bps at 4.618%. Over the week, the 30-year yield declined by -10.8 bps. It was -25.7 bps for February, the largest monthly decrease since February 2025.

At the short end, the two-year yield, closely tied to interest rate expectations, declined -9.4 bps to 3.387%. Earlier in the session, it reached a 10-day low and ended the week -9.5 bps lower. On a monthly basis, the two-year yield shed -15.2 bps, its largest monthly drop since August.

However, Treasury yields partially retraced some losses following the release of producer price data, which exceeded market expectations.

The Producer Price Index (PPI) for final demand rose by 0.5% in January, following a downwardly revised increase of 0.4% in December. This outpaced economists’ consensus, which had anticipated a 0.3% gain.

The yield curve steepened on the day, with the spread between two-year and 10-year yields widening to 56.50 bps from 52.7 bps at Thursday’s close. Despite this, the curve has flattened in 11 of the past 13 sessions, as short-term yields have declined less sharply than those on longer-dated Treasuries. Over February, the spread between two-year and 10-year yields flattened by 13.4 bps.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing in 55.0 bps of cuts in 2026, lower than the 59.5 bps priced in the previous week. Fed funds futures traders are now pricing in a 7.4% probability of a 25 bps rate cut at the 18th March FOMC meeting, down from 3.5% a week ago.

On Friday, Germany’s benchmark 10-year yield recorded its largest monthly decline since Liberation Day, as global government bonds benefitted from investor anxiety amid growing geopolitical concerns.

The yield on German 10-year Bunds fell -4.4 bps to 2.656%, reaching its lowest level since 13th November. Over the week, the yield declined -8.4 bps, while February saw a total decrease of -19.1 bps. The two-year German yield, sensitive to interest rate expectations, dropped -3.0 bps to 2.016%. Across the week, it was down -4.7 bps, and for the month, it registered a reduction of -6.4 bps.

At the longer end of the curve, Germany’s 30-year yield decreased -5.7 bps to 3.319% on Friday, contributing to a weekly fall of -8.3 bps and a monthly drop of -17.8 bps.

Earlier in the week, ECB President Christine Lagarde indicated that policymakers anticipate inflation will stabilise around the 2% target over the medium term.

Italy’s 10-year yield declined -2.5 bps on Friday, resulting in a weekly fall of -7.2 bps to 3.278%. Over the course of February, it dropped -18.7 bps. The spread between Italian BTP 10-year yields and German Bunds widened slightly to 62.2 bps, compared with 61.8 bps at the end of January.

The yield on France’s 10-year OAT bond fell -2.2 bps to 3.227% on Friday, marking its sixth consecutive day of declines and its lowest level since June. French yields outperformed Bunds, declining -20.4 bps over February. The spread between French and German 10-year yields narrowed to 57.1 bps on Friday, its lowest since 10th June. This spread contracted by 1.3 bps during February.

Note: As of 5 pm EST 27 February 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

本文提供給您僅供資訊參考之用,不應被視為認購或銷售此處提及任何投資或相關服務的優惠招攬或遊說。金融商品交易涉及重大損失風險,可能不適合所有投資者。過往績效不代表未來表現。

由專業人士建立。為專業人士打造。